Download as pdf or txt

You might also like

- Proposal For Bulk Import/Sale of Automotive Gas OilDocument9 pagesProposal For Bulk Import/Sale of Automotive Gas OilBode OluwashanuNo ratings yet

- Renewal LeaseDocument29 pagesRenewal LeaseAicha CamaraNo ratings yet

- Matdip301 Advanced Mathematics-IDocument2 pagesMatdip301 Advanced Mathematics-IHari PrasadNo ratings yet

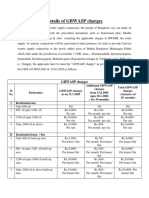

- GBWASP BCC ChargesDocument8 pagesGBWASP BCC ChargesshivaiahvNo ratings yet

- Residential Application FormDocument4 pagesResidential Application FormLagiono SovanivaluNo ratings yet

- SECTION #1 Financial StatementDocument3 pagesSECTION #1 Financial StatementashibhallauNo ratings yet

- Bill of QuantitiesDocument3 pagesBill of QuantitiesVuthpalachaitanya KrishnaNo ratings yet

- Tasad Conservation Area - Carbon Trade SummaryDocument2 pagesTasad Conservation Area - Carbon Trade Summaryindra lukmanNo ratings yet

- Agro Eco Tourism Project in BriefDocument24 pagesAgro Eco Tourism Project in BriefbimalNo ratings yet

- Details of GBWASPChargesDocument2 pagesDetails of GBWASPChargesGANESH NNo ratings yet

- CLSS EWS Leaflet Oct2019 PDFDocument2 pagesCLSS EWS Leaflet Oct2019 PDFmonakgohelNo ratings yet

- Skyview Manor CaseDocument3 pagesSkyview Manor CaseNisa SasyaNo ratings yet

- Line GraphDocument20 pagesLine GraphTran Do Thu HaNo ratings yet

- Self AssessmentDocument2 pagesSelf AssessmentAmit JakharNo ratings yet

- The Avenue 100sqft, Food CourtDocument1 pageThe Avenue 100sqft, Food CourtMuhammad Bilal DarNo ratings yet

- International Financial Management: Exchange Rate DeterminationDocument19 pagesInternational Financial Management: Exchange Rate Determinationmagma rachmaniNo ratings yet

- Investment Proposal'sDocument15 pagesInvestment Proposal'sKiran MNo ratings yet

- Slow and Stead Group: BY: Hemant NurshidDocument25 pagesSlow and Stead Group: BY: Hemant NurshidalamnurshidNo ratings yet

- Amendment: David - Stueve@ks - GovDocument17 pagesAmendment: David - Stueve@ks - GovJAGUAR GAMINGNo ratings yet

- Whips Policy Brief Property Tax Reform Final PassageDocument10 pagesWhips Policy Brief Property Tax Reform Final PassagerealmiamibeachNo ratings yet

- FO82453735DC4Document8 pagesFO82453735DC4Willy MwangiNo ratings yet

- Sesi 7 - Skyview Manor CaseDocument3 pagesSesi 7 - Skyview Manor CasestevenNo ratings yet

- Property Tax Calculations For BangaloreDocument7 pagesProperty Tax Calculations For BangaloreNaveen KumarNo ratings yet

- 1758-Minta Yuwana-Soal Kumpulan 1Document5 pages1758-Minta Yuwana-Soal Kumpulan 1AuliaMukadisNo ratings yet

- Majestic Lodge : Colin Drury, Management and Cost Accounting - Majestic LodgeDocument3 pagesMajestic Lodge : Colin Drury, Management and Cost Accounting - Majestic LodgechitraNo ratings yet

- Skyview ManorDocument4 pagesSkyview ManorDwi Handoyo MiharjoNo ratings yet

- Tumbocon Vs Ombudsman GR 238103, 238223 06january2020Document15 pagesTumbocon Vs Ombudsman GR 238103, 238223 06january2020CJNo ratings yet

- Qatar Real Estate Market Annual Report 2008Document9 pagesQatar Real Estate Market Annual Report 2008r.nair9865100% (2)

- (#2) Supply-Demand and Philippine Economic ProblemsDocument16 pages(#2) Supply-Demand and Philippine Economic ProblemsBianca Jane GaayonNo ratings yet

- Vacation House enDocument3 pagesVacation House enAT_BuiNo ratings yet

- Global Futures and Foresight - Hotel Outlook 2020 - Update On The Future of Travel and Tourism in The Middle East V1!03!06 07Document8 pagesGlobal Futures and Foresight - Hotel Outlook 2020 - Update On The Future of Travel and Tourism in The Middle East V1!03!06 07nina2191919No ratings yet

- Sector Profile Tourism in India: An IntroductionDocument7 pagesSector Profile Tourism in India: An Introductionavinal malikNo ratings yet

- Horwath - Industry Report Tourism Hospitality CountrywiseDocument12 pagesHorwath - Industry Report Tourism Hospitality CountrywisejogisinghNo ratings yet

- 1033-F (W B)Document2 pages1033-F (W B)Jaydip GhughuNo ratings yet

- australia---sydney-cbd-office-q2-2024Document2 pagesaustralia---sydney-cbd-office-q2-2024yenyew.tay.2022No ratings yet

- 2019 10 April Memorandum Part 1Document21 pages2019 10 April Memorandum Part 1Sandisiwe GugusheNo ratings yet

- Dwnload Full Engineering Economy 15th Edition Sullivan Test Bank PDFDocument35 pagesDwnload Full Engineering Economy 15th Edition Sullivan Test Bank PDFserenafinnodx100% (14)

- Texas Pacific Land Trust 10K NotesDocument13 pagesTexas Pacific Land Trust 10K NotesSugar RayNo ratings yet

- UniCredit - Gold MarketDocument11 pagesUniCredit - Gold Marketderailedcapitalism.comNo ratings yet

- NY-DOT Cost 710 - 0611Document207 pagesNY-DOT Cost 710 - 0611akamola52No ratings yet

- Decree 1241-2022 (Unofficial English Translation)Document4 pagesDecree 1241-2022 (Unofficial English Translation)Kusuma WijajaNo ratings yet

- On January 1 2011 Secada Co Leased A Building To PDFDocument1 pageOn January 1 2011 Secada Co Leased A Building To PDFAnbu jaromiaNo ratings yet

- Qatar Real Estate 112007Document50 pagesQatar Real Estate 112007neettiyath1No ratings yet

- Final Fy10 MemoDocument9 pagesFinal Fy10 Memoraleighpublicrecord.orgNo ratings yet

- Residential Target Market Analysis Manistee CountyDocument48 pagesResidential Target Market Analysis Manistee CountyArielle BreenNo ratings yet

- Skyview ManorDocument3 pagesSkyview ManormargaretadeviNo ratings yet

- Orca Share Media1667227729136 6992859933231245460Document24 pagesOrca Share Media1667227729136 6992859933231245460meraheNo ratings yet

- Fees Strucure MBA 2022Document2 pagesFees Strucure MBA 2022Bhavesh SharmaNo ratings yet

- 2 - House Property Problems 22-23Document5 pages2 - House Property Problems 22-2320-UCO-517 AJAY KELVIN ANo ratings yet

- Barton Deakin Brief: NSW Government Housing ReformsDocument6 pagesBarton Deakin Brief: NSW Government Housing Reformsbhanish2001No ratings yet

- FA DCF Modelling Test 1Document21 pagesFA DCF Modelling Test 1vikasNo ratings yet

- NVT Life Square PricingDocument1 pageNVT Life Square PricingaseerahmedNo ratings yet

- Housing 2017Document12 pagesHousing 2017Radharani SharmaNo ratings yet

- Description: Tags: 47 2007Document7 pagesDescription: Tags: 47 2007anon-376981No ratings yet

- UAE Real Estate Update - June 2013Document4 pagesUAE Real Estate Update - June 2013Francisco GonzalezNo ratings yet

- SK Sbu 2016Document78 pagesSK Sbu 2016anon_715077295No ratings yet

- BP 220 Resolution No. 725Document5 pagesBP 220 Resolution No. 725Bernadeth MirasolNo ratings yet

- Tower 17 Booklet (Final Version)Document8 pagesTower 17 Booklet (Final Version)zahidNo ratings yet

- UK Property Letting: Making Money in the UK Private Rented SectorFrom EverandUK Property Letting: Making Money in the UK Private Rented SectorNo ratings yet

- Pacific Private Sector Development Initiative: A Decade of Reform: Annual Progress Report 2015-2016From EverandPacific Private Sector Development Initiative: A Decade of Reform: Annual Progress Report 2015-2016No ratings yet

- Terms & Conditions: Al Ameen Travels Vriddhachalam RW25CL1104Document1 pageTerms & Conditions: Al Ameen Travels Vriddhachalam RW25CL1104yrafeeuNo ratings yet

- Tax Invoice: Fasmugoo BuildwareDocument1 pageTax Invoice: Fasmugoo BuildwareyrafeeuNo ratings yet

- JCB Generator BrochureDocument8 pagesJCB Generator BrochureyrafeeuNo ratings yet

- Information Form: Maldives Islamic BankDocument5 pagesInformation Form: Maldives Islamic BankyrafeeuNo ratings yet

- LED LIGHT PHILLIPS - Specs1Document4 pagesLED LIGHT PHILLIPS - Specs1yrafeeuNo ratings yet

- Particle Counting PDFDocument7 pagesParticle Counting PDFyrafeeuNo ratings yet

- Idose4 - Whitepaper - Technical - Low Res - PDF Nodeid 8432599&vernum - 2 PDFDocument40 pagesIdose4 - Whitepaper - Technical - Low Res - PDF Nodeid 8432599&vernum - 2 PDFOmarah AbdalqaderNo ratings yet

- Navyfield Full ManualDocument11 pagesNavyfield Full Manualmarti1125100% (2)

- Pe 4Document5 pagesPe 4slide_poshNo ratings yet

- At The AirportDocument6 pagesAt The AirportAlen KuharićNo ratings yet

- Clarkson Lumber Case QuestionsDocument2 pagesClarkson Lumber Case QuestionsJeffery KaoNo ratings yet

- Compressor Control, Load Sharing and Anti-SurgeDocument6 pagesCompressor Control, Load Sharing and Anti-SurgeJason Thomas100% (1)

- D Internet Myiemorgmy Intranet Assets Doc Alldoc Document 15367 JURUTERA OCTOBER 2018Document52 pagesD Internet Myiemorgmy Intranet Assets Doc Alldoc Document 15367 JURUTERA OCTOBER 2018Leanne ChewNo ratings yet

- GST Accounting EntriesDocument24 pagesGST Accounting EntriesRamesh KumarNo ratings yet

- Whole Systems Thinking As A Basis For Paradigm Change in EducationDocument477 pagesWhole Systems Thinking As A Basis For Paradigm Change in EducationMaría Teresa Muñoz QuezadaNo ratings yet

- New M Tech Programme in Computer Science and Engineering Artificial Intelligence Data Analytics Self Financing Mode Admissions 2023 - 0Document6 pagesNew M Tech Programme in Computer Science and Engineering Artificial Intelligence Data Analytics Self Financing Mode Admissions 2023 - 0Himesh KumarNo ratings yet

- Tutorial TransformerDocument2 pagesTutorial TransformerMohd KhairiNo ratings yet

- Anna University of Technology, TiruchirappalliDocument2 pagesAnna University of Technology, TiruchirappallisanjeevrksNo ratings yet

- HIVER Waivers sp22 Fady ElmessyDocument2 pagesHIVER Waivers sp22 Fady ElmessyFady Ezzat 1No ratings yet

- Proprietary & Confidential: This Is A Static Sensitive Device. Handle & Store Appropriately To Prevent Esd DamageDocument2 pagesProprietary & Confidential: This Is A Static Sensitive Device. Handle & Store Appropriately To Prevent Esd DamagePawan PalNo ratings yet

- Siun Sote Objection Related To Social Welfare and Health Care Services or Treatment FormDocument2 pagesSiun Sote Objection Related To Social Welfare and Health Care Services or Treatment FormShahnaz NawazNo ratings yet

- 03AdvancedThinkAhead4 ExamSkillsPrac Mod5-6Document3 pages03AdvancedThinkAhead4 ExamSkillsPrac Mod5-6mariasanztiNo ratings yet

- Computerized Accounting Using Tally - Erp 9 - Student GuideDocument546 pagesComputerized Accounting Using Tally - Erp 9 - Student Guideshruti100% (1)

- 10 DM Commandments EbookDocument9 pages10 DM Commandments EbookLily KimNo ratings yet

- Module 1: Authentic Assessment in The ClassroomDocument10 pagesModule 1: Authentic Assessment in The ClassroomSir Log100% (1)

- Steel Body - Lever Hoists: A e B A e B A e BDocument1 pageSteel Body - Lever Hoists: A e B A e B A e BtylerlhsmithNo ratings yet

- Fermentation of Cucumbers Brined With Calcium Chloride Instead of Sodium ChlorideDocument6 pagesFermentation of Cucumbers Brined With Calcium Chloride Instead of Sodium ChloridedupitosariNo ratings yet

- BCH Filled FormDocument2 pagesBCH Filled Formcecertificateqvc1No ratings yet

- 1468 Water Soluble Salts Bresle Method Iso 8509Document2 pages1468 Water Soluble Salts Bresle Method Iso 8509osgamNo ratings yet

- Exports Driven by Hallyu Increasing South Korea's Economic Growth - Cultural Diplomacy ApproachDocument17 pagesExports Driven by Hallyu Increasing South Korea's Economic Growth - Cultural Diplomacy ApproachAnastasya doriska MasliaNo ratings yet

- Workstationst Modbus® Instruction Guide: Gei-100696EDocument41 pagesWorkstationst Modbus® Instruction Guide: Gei-100696EЕсет ДаулетжанNo ratings yet

- Equity ApplicationDocument3 pagesEquity ApplicationanniesachdevNo ratings yet

- Charusat 6th SemDocument1 pageCharusat 6th SemdhruvilNo ratings yet

- Graded Quesions Complete Book0Document344 pagesGraded Quesions Complete Book0Irimia Mihai Adrian100% (1)

- 1800 Mechanical Bender: Instruction ManualDocument42 pages1800 Mechanical Bender: Instruction ManualPato Loco Rateria100% (1)