Download as pdf or txt

You might also like

- Walter Piston, Mark DeVoto - Harmony 5th Ed Book 1 (Edited)Document216 pagesWalter Piston, Mark DeVoto - Harmony 5th Ed Book 1 (Edited)saghiNo ratings yet

- Test Bank For Cognitive Neuroscience The Biology of The Mind Fifth Edition Fifth EditionDocument36 pagesTest Bank For Cognitive Neuroscience The Biology of The Mind Fifth Edition Fifth Editionshashsilenceri0g32100% (50)

- The Women Who Knew JesusDocument7 pagesThe Women Who Knew JesusKiki Shakespaere Thompson67% (3)

- Reimaging The Career Center - July 2017Document18 pagesReimaging The Career Center - July 2017Casey Boyles100% (1)

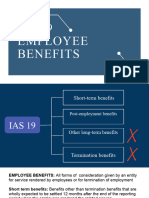

- Employee Benefits 03Document11 pagesEmployee Benefits 03Nelva Quinio33% (3)

- History and Components of CompensationDocument42 pagesHistory and Components of CompensationNekoh Dela Cerna75% (4)

- Leave PolicyDocument3 pagesLeave PolicyShiva PillaiNo ratings yet

- CHAPTER 11 ACTFADocument41 pagesCHAPTER 11 ACTFACriselda ClemensoNo ratings yet

- Lesson Employee BenefitDocument18 pagesLesson Employee BenefitDesiree GalletoNo ratings yet

- Ias 19 - Employee Benefits QUESTION 57-17Document9 pagesIas 19 - Employee Benefits QUESTION 57-17Janella Gail ArenasNo ratings yet

- Ias 19Document43 pagesIas 19Reever RiverNo ratings yet

- Notes On PayrollDocument10 pagesNotes On PayrollMoo-usa BaoNo ratings yet

- DaysHospitality Policy and Procedure Manual Section3Document22 pagesDaysHospitality Policy and Procedure Manual Section3kasi2009No ratings yet

- Chapter 6 Employee Benefits (Part 2)Document21 pagesChapter 6 Employee Benefits (Part 2)not funny didn't laughNo ratings yet

- Mastering Withholding TaxesDocument15 pagesMastering Withholding TaxesvicsNo ratings yet

- Employee Benefits Ias19Document42 pagesEmployee Benefits Ias19krishnaguptaNo ratings yet

- Unit 7 E-Tutor PresentationDocument18 pagesUnit 7 E-Tutor PresentationKatrina EustaceNo ratings yet

- Q2 WordDocument22 pagesQ2 WordNishita DagaNo ratings yet

- ALZONA - OE Employee CompensationDocument5 pagesALZONA - OE Employee CompensationJames Ryan AlzonaNo ratings yet

- Pederson CPA Review FAR Notes PensionDocument8 pagesPederson CPA Review FAR Notes Pensionboen jaymeNo ratings yet

- Contribut Ions To Pension and TrustsDocument3 pagesContribut Ions To Pension and TrustsMiracle GraceNo ratings yet

- IAS 19 - Employee BenefitDocument49 pagesIAS 19 - Employee BenefitShah Kamal100% (2)

- Module 12 - PAS 19 Employee BenefitsDocument6 pagesModule 12 - PAS 19 Employee BenefitsAKIO HIROKINo ratings yet

- Compensation HRM 3Document5 pagesCompensation HRM 3Alamin tahaminNo ratings yet

- BSBFIM501 Manage Budgets and Financial Plans Learner Instructions 2 (Implement Financial Management Approaches)Document7 pagesBSBFIM501 Manage Budgets and Financial Plans Learner Instructions 2 (Implement Financial Management Approaches)vipulclasses01 vipulclass0% (1)

- Chapter 3 Payroll 2011 EditedDocument29 pagesChapter 3 Payroll 2011 Editedendashaw100% (2)

- KSF - Relocation Policy V1.0Document6 pagesKSF - Relocation Policy V1.0rakhi.chadagaNo ratings yet

- Employee BenefitsDocument31 pagesEmployee BenefitsHazel PachecoNo ratings yet

- Monika Rehman Roll No 10Document19 pagesMonika Rehman Roll No 10Monika RehmanNo ratings yet

- Cliff Notes - PM RetirementDocument5 pagesCliff Notes - PM RetirementJohnathan JohnsonNo ratings yet

- Financial Management Integrity Bulletin CPDDocument6 pagesFinancial Management Integrity Bulletin CPDJuharto UsopNo ratings yet

- Payroll CycleDocument21 pagesPayroll CyclemurshidalbimaanyNo ratings yet

- LKAS 19 2021 UploadDocument31 pagesLKAS 19 2021 Uploadpriyantha dasanayake100% (2)

- Sessi 22Document33 pagesSessi 22Theresia SherinNo ratings yet

- Tax Exempt and Government Entities (TE/GE) Employee PlansDocument34 pagesTax Exempt and Government Entities (TE/GE) Employee PlansIRSNo ratings yet

- CompensationBenefits PolicyDocument24 pagesCompensationBenefits PolicyMido Mido100% (1)

- Master of Business Administration-MBA Semester IV: Subject Code - Subject NameDocument8 pagesMaster of Business Administration-MBA Semester IV: Subject Code - Subject NameroshreshNo ratings yet

- CH 28 - Employee Benefits PDFDocument7 pagesCH 28 - Employee Benefits PDFJm SevallaNo ratings yet

- Accounting Policy Powerpoint PresentationDocument130 pagesAccounting Policy Powerpoint PresentationPrincess JoemNo ratings yet

- Payroll Policy Sample - 2Document2 pagesPayroll Policy Sample - 2Apoorva BellavarNo ratings yet

- HR RESEARCH 9Document16 pagesHR RESEARCH 9عبد الرحيم محمودNo ratings yet

- Performance and Reward Management Kmbnhr04Document20 pagesPerformance and Reward Management Kmbnhr04Haris AnsariNo ratings yet

- Descriptive Guidelines On Flexi Pay ComponentsDocument5 pagesDescriptive Guidelines On Flexi Pay Componentsshannbaby22No ratings yet

- 5#fiscal Planning & Financial ManagementDocument36 pages5#fiscal Planning & Financial Managementوجد عمرNo ratings yet

- Cfas Pas 19Document4 pagesCfas Pas 19Zyribelle Anne JAPSONNo ratings yet

- PAS 19 Employee Benefits: Short-Term Employee Benefits Are Employee Benefits (Other Than Termination BenDocument5 pagesPAS 19 Employee Benefits: Short-Term Employee Benefits Are Employee Benefits (Other Than Termination BenKaila Clarisse CortezNo ratings yet

- 2013 Itc TB GlossaryDocument24 pages2013 Itc TB Glossaryzhyldyz_88No ratings yet

- Employee BenefitDocument32 pagesEmployee BenefitnatiNo ratings yet

- FR17 - Employee Benefits (Stud) .Document45 pagesFR17 - Employee Benefits (Stud) .duong duongNo ratings yet

- Educ 207 - FINANCIAL ASPECTS IN EDUCATIONAL PLANNING v2Document7 pagesEduc 207 - FINANCIAL ASPECTS IN EDUCATIONAL PLANNING v2DARLING REMOLAR100% (1)

- Edu 2013 10 Ret Plan Exam Case Kuk671xDocument20 pagesEdu 2013 10 Ret Plan Exam Case Kuk671xjusttestitNo ratings yet

- APPENDIXDocument16 pagesAPPENDIXNishaNo ratings yet

- Leave Enhancement PolicyDocument2 pagesLeave Enhancement PolicymtnazeerNo ratings yet

- Lyubaaa 082624Document3 pagesLyubaaa 082624omarikibwanaNo ratings yet

- Far TheoriesDocument4 pagesFar Theoriesfrancis dungcaNo ratings yet

- Course Materials-IA3-Week 1-M. ManayaoDocument17 pagesCourse Materials-IA3-Week 1-M. ManayaoMitchie FaustinoNo ratings yet

- IAS 19 Employee Benefits (2021)Document6 pagesIAS 19 Employee Benefits (2021)Tawanda Tatenda Herbert100% (1)

- Employee BenefitsDocument9 pagesEmployee BenefitstinydmpNo ratings yet

- RUIZ, Jevilyn Mary ASSIGNMENT 003-2021Document12 pagesRUIZ, Jevilyn Mary ASSIGNMENT 003-2021Jevi RuiizNo ratings yet

- Maximizing Your Wealth: A Comprehensive Guide to Understanding Gross and Net SalaryFrom EverandMaximizing Your Wealth: A Comprehensive Guide to Understanding Gross and Net SalaryNo ratings yet

- 1040 Exam Prep Module III: Items Excluded from Gross IncomeFrom Everand1040 Exam Prep Module III: Items Excluded from Gross IncomeRating: 1 out of 5 stars1/5 (1)

- Healthcare Staffing Payroll and Billing Process GuideFrom EverandHealthcare Staffing Payroll and Billing Process GuideNo ratings yet

- Budgeting: The Free Ultimate Guide to Passive Income Streams (How to Ensure Business Budgeting Works for You Instead of Against You)From EverandBudgeting: The Free Ultimate Guide to Passive Income Streams (How to Ensure Business Budgeting Works for You Instead of Against You)No ratings yet

- Accountingtools: Balance Sheet DefinitionDocument5 pagesAccountingtools: Balance Sheet DefinitionHosty PuffNo ratings yet

- Accounting Reports - Balance Sheet1Document2 pagesAccounting Reports - Balance Sheet1Hosty PuffNo ratings yet

- Workers' Compensation Insurance Requirements For Employers: Colorado Department of Labor and EmploymentDocument2 pagesWorkers' Compensation Insurance Requirements For Employers: Colorado Department of Labor and EmploymentHosty PuffNo ratings yet

- Deducting Meals While Traveling and Per Diem AllowancesDocument3 pagesDeducting Meals While Traveling and Per Diem AllowancesHosty PuffNo ratings yet

- Business Deductions For Rent and Lease Payments: AmortizedDocument6 pagesBusiness Deductions For Rent and Lease Payments: AmortizedHosty PuffNo ratings yet

- Napthpajakri Tender 1 - PCD-575Document42 pagesNapthpajakri Tender 1 - PCD-575JamjamNo ratings yet

- Cs6201 Digital Principles and System Design: Unit IDocument19 pagesCs6201 Digital Principles and System Design: Unit IUttam NeelapureddyNo ratings yet

- 3 San Miguel Corp V Heirs of InguitoDocument21 pages3 San Miguel Corp V Heirs of InguitokwonpenguinNo ratings yet

- The Magnacarta For Public School Teachers v.1Document70 pagesThe Magnacarta For Public School Teachers v.1France BejosaNo ratings yet

- Occupational TherapyDocument11 pagesOccupational TherapyYingVuong100% (1)

- Etchells Tuning SequenceDocument2 pagesEtchells Tuning SequencegsolomonsNo ratings yet

- Weed Control Using GoatsDocument24 pagesWeed Control Using Goatsstormbaby100% (1)

- 11 BishopDocument37 pages11 BishopaniseclassNo ratings yet

- Stereo Isomerism - (Eng)Document32 pagesStereo Isomerism - (Eng)Atharva WatekarNo ratings yet

- Sotto Vs TevesDocument4 pagesSotto Vs TevesLittle GirlblueNo ratings yet

- Fine Art - September 2022Document15 pagesFine Art - September 2022ArtdataNo ratings yet

- Art of Prolonging LifeDocument83 pagesArt of Prolonging LifePaulo SilvaNo ratings yet

- Document 5Document1 pageDocument 5Joycie CalluengNo ratings yet

- Hongkong and Shanghai Banking Corporation (HSBC) : International Money TransfersDocument3 pagesHongkong and Shanghai Banking Corporation (HSBC) : International Money TransfersThenmozhi ThambiduraiNo ratings yet

- 7.EE.B4b Inequalities Symbolize & Solve 10QDocument4 pages7.EE.B4b Inequalities Symbolize & Solve 10Qicka83No ratings yet

- Refugees and AssylumDocument18 pagesRefugees and AssylumCherry Ann Bawagan Astudillo-BalonggayNo ratings yet

- Portrait AssignmentDocument1 pagePortrait Assignmentapi-240963149No ratings yet

- Percentages PracticeDocument8 pagesPercentages PracticeChikanma OkoisorNo ratings yet

- ĐÁP ÁN ĐỀ THI THỬ SỐ 09 (2019-2020)Document6 pagesĐÁP ÁN ĐỀ THI THỬ SỐ 09 (2019-2020)Changg100% (1)

- Fluid Mechanics Lectures NotesDocument16 pagesFluid Mechanics Lectures NotesFady KamilNo ratings yet

- Ucsp Q1M2 PDFDocument20 pagesUcsp Q1M2 PDFElvin Santiago100% (7)

- Cash ReceiptDocument6 pagesCash ReceiptYed777andiNo ratings yet

- Ausensi (2020) A New Resultative Construction in SpanishDocument29 pagesAusensi (2020) A New Resultative Construction in SpanishcfmaNo ratings yet

- Schools Pan IndiaDocument6,699 pagesSchools Pan Indiadeva nesanNo ratings yet

- Contempor Ary Philippine Arts From The Regions: Rose-Anne B. Magsino, LPTDocument21 pagesContempor Ary Philippine Arts From The Regions: Rose-Anne B. Magsino, LPTLara NicoleNo ratings yet