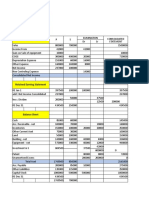

Class 3 - 28th March 2021

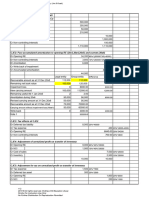

Class 3 - 28th March 2021

You might also like

- Advanced Financial Accounting: Solutions ManualDocument89 pagesAdvanced Financial Accounting: Solutions ManualThùy Ngân100% (2)

- Questions For IFRS HighlightedDocument28 pagesQuestions For IFRS HighlightedWowee Cruz100% (1)

- Advanced Financial Accounting 11th Edition Christensen Test Bank DownloadDocument56 pagesAdvanced Financial Accounting 11th Edition Christensen Test Bank DownloadHeatherRobertstwopa100% (40)

- Consolidation Question Solution PDFDocument3 pagesConsolidation Question Solution PDFjoannejose2011100% (2)

- AFAR TestbankDocument56 pagesAFAR TestbankDrama SubsNo ratings yet

- Group Reporting S4Document31 pagesGroup Reporting S4rajesh1978.nair2381100% (2)

- RIL Excel Sheet FRADocument56 pagesRIL Excel Sheet FRAAditi AgrawalNo ratings yet

- WAMUNIMA. Financial Accounting 2 Assignment.Document8 pagesWAMUNIMA. Financial Accounting 2 Assignment.simpitorussellNo ratings yet

- Net Income 38000 Non Cash ItemsDocument8 pagesNet Income 38000 Non Cash ItemsHuu LuatNo ratings yet

- BusCom Practice SetsDocument20 pagesBusCom Practice SetsShaz NagaNo ratings yet

- Tut 11 Self SolutionDocument4 pagesTut 11 Self SolutionDuwaine BramwellNo ratings yet

- Dispenser of California - Rahul - MattaDocument9 pagesDispenser of California - Rahul - MattaHarsh MaheshwariNo ratings yet

- Chapter 5Document5 pagesChapter 5bonfaceNo ratings yet

- MaDocument6 pagesMaAashayNo ratings yet

- 14 Marks AnswersDocument42 pages14 Marks Answerskuvira LodhaNo ratings yet

- FA With AdjustmentsDocument14 pagesFA With AdjustmentsHarshini AkilandanNo ratings yet

- Module 6 Business Income Exercise SolutionsDocument13 pagesModule 6 Business Income Exercise SolutionshodaNo ratings yet

- Pomsky GroupDocument18 pagesPomsky GroupEduskill Learning CentreNo ratings yet

- Fund Flow StatementDocument41 pagesFund Flow StatementMahima SinghNo ratings yet

- Dargent Co. AnswerDocument4 pagesDargent Co. AnswerAbishek GuptaNo ratings yet

- Midterm Test 2Document7 pagesMidterm Test 2bangannguyen2020No ratings yet

- SKD 4Document6 pagesSKD 4DiryanNo ratings yet

- Exercises On DividendsDocument16 pagesExercises On DividendsGrace RoqueNo ratings yet

- FM Assignment1Document6 pagesFM Assignment1Rishi Kumar SainiNo ratings yet

- Akl - Agung Prabowo - 02 - 5-3Document3 pagesAkl - Agung Prabowo - 02 - 5-3Agung PrabowoNo ratings yet

- Cash Flow QN 3Document4 pagesCash Flow QN 3Takudzwa LanceNo ratings yet

- Alpha Manufacturing Ltd. (AML) - Cash Flow: Nrti Poa-Quiz 2 Time: 40 MinutesDocument4 pagesAlpha Manufacturing Ltd. (AML) - Cash Flow: Nrti Poa-Quiz 2 Time: 40 MinutesDeepak KumarNo ratings yet

- Jawaban P5-1Document3 pagesJawaban P5-1Nadillah LeicaNo ratings yet

- Holding Company Class Note 1Document6 pagesHolding Company Class Note 1sahir112001No ratings yet

- Zahra Calista LAB AKLDocument24 pagesZahra Calista LAB AKLzahra calista armansyahNo ratings yet

- Business ValuationDocument6 pagesBusiness ValuationlenoraNo ratings yet

- Questions For Unit 4 RevisionDocument3 pagesQuestions For Unit 4 RevisionDimple PatelNo ratings yet

- Non-Current Assets: Hnda 3 Year - 2 Semester 2016 Advanced Financial Reporting Model AnswersDocument8 pagesNon-Current Assets: Hnda 3 Year - 2 Semester 2016 Advanced Financial Reporting Model Answersrwl s.r.lNo ratings yet

- Cash Flow StatementDocument4 pagesCash Flow StatementNarayan DhunganaNo ratings yet

- Mand CHODocument7 pagesMand CHOMichael BaguyoNo ratings yet

- Comparison of Old and New Tax Regime 04042023Document3 pagesComparison of Old and New Tax Regime 04042023VenkateshNo ratings yet

- On January 1, Year 4, Grant Corporation BoughtDocument4 pagesOn January 1, Year 4, Grant Corporation BoughtJalaj GuptaNo ratings yet

- Problem Solving - Statement of Cash FlowDocument7 pagesProblem Solving - Statement of Cash FlowHossain AlmasNo ratings yet

- FM 2019 SolutionsDocument6 pagesFM 2019 Solutionsaditikotere92No ratings yet

- Cash Flow ProblemsDocument9 pagesCash Flow ProblemsSharu BsNo ratings yet

- Assignment 9Document10 pagesAssignment 9Jerickho JNo ratings yet

- Business Income Revision SheetsDocument79 pagesBusiness Income Revision Sheets123nishandhakall.dNo ratings yet

- Business Plan of Event Management: Submitted To: Miss Gurpreet KaurDocument21 pagesBusiness Plan of Event Management: Submitted To: Miss Gurpreet KaurPrashantNo ratings yet

- Acct6005 Company Accounting: Assessment 2 Case StudyDocument8 pagesAcct6005 Company Accounting: Assessment 2 Case StudyRuhan SinghNo ratings yet

- BTAXREV ACT 184 Week 3 Income Taxation - Tax ReturnsDocument21 pagesBTAXREV ACT 184 Week 3 Income Taxation - Tax ReturnsgatotkaNo ratings yet

- Binaluyo 2022 Chap 1 MCDocument16 pagesBinaluyo 2022 Chap 1 MCWere dooomedNo ratings yet

- Chapter 16 - Teacher's Manual - Aa Part 2Document18 pagesChapter 16 - Teacher's Manual - Aa Part 2IsyongNo ratings yet

- FAR - Financial Liabilities - Debt RestructuringDocument9 pagesFAR - Financial Liabilities - Debt Restructuringmarlout.saritaNo ratings yet

- Prodigal Co. 000$ W Nci Statement of Profit & Loss & Comprihensive IncomeDocument2 pagesProdigal Co. 000$ W Nci Statement of Profit & Loss & Comprihensive IncomeMuhammad MahmoodNo ratings yet

- P6.25 - Chapter 6Document5 pagesP6.25 - Chapter 6Dang PhuongNo ratings yet

- Consolidated FS - QUIZ PART 3Document4 pagesConsolidated FS - QUIZ PART 3Christine Jane Ramos100% (1)

- Lape - ACP312 - ULOa - Let's Analyze Week6Document3 pagesLape - ACP312 - ULOa - Let's Analyze Week6Bryle Jay LapeNo ratings yet

- Cash Flow 05 With Answers Just Give SolutionsDocument21 pagesCash Flow 05 With Answers Just Give SolutionsEdi wow WowNo ratings yet

- Accounting 15 Investment SolutionsDocument18 pagesAccounting 15 Investment Solutionskhyla Marie NooraNo ratings yet

- Cash and Credit ManagementDocument11 pagesCash and Credit Managementaoishic2025No ratings yet

- Key UNIT II B SubsequentDocument6 pagesKey UNIT II B SubsequentDaisy TañoteNo ratings yet

- AC - IntAcctg-C Prelims Solutions Sol, Janesene NDocument36 pagesAC - IntAcctg-C Prelims Solutions Sol, Janesene NJanesene SolNo ratings yet

- Module 2 Capital Budgeting Handout For LMS 2020Document11 pagesModule 2 Capital Budgeting Handout For LMS 2020sandeshNo ratings yet

- Jurnal: 2. Pengakuan Realisasi Home Office Branch OfficeDocument2 pagesJurnal: 2. Pengakuan Realisasi Home Office Branch OfficefaldyNo ratings yet

- Interim Financial Reporting and Operating Segment Discussion Problems and Answer KeyDocument4 pagesInterim Financial Reporting and Operating Segment Discussion Problems and Answer Keyprincess QNo ratings yet

- 3jun24 - Intercompany Transaction - EquipmentDocument16 pages3jun24 - Intercompany Transaction - Equipmentsisilia rachelNo ratings yet

- Balance Sheet Liabilities 2004 2005 Capital 120000 150000 Sundry Creditors 37000 25000 Bills Payable 15000 17000 P&L A/c 60000 69000 232000 261000Document17 pagesBalance Sheet Liabilities 2004 2005 Capital 120000 150000 Sundry Creditors 37000 25000 Bills Payable 15000 17000 P&L A/c 60000 69000 232000 261000kumaranil_1983No ratings yet

- LAB 4 Capital Budgeting 2024Document3 pagesLAB 4 Capital Budgeting 2024asthapatel.akpNo ratings yet

- Finding Balance 2016: Benchmarking the Performance of State-Owned Enterprise in Island CountriesFrom EverandFinding Balance 2016: Benchmarking the Performance of State-Owned Enterprise in Island CountriesNo ratings yet

- PPT5-Allocation and Depreciation of Differences Between Implied and Book ValuesDocument51 pagesPPT5-Allocation and Depreciation of Differences Between Implied and Book ValuesRifdah SaphiraNo ratings yet

- F1 QandAarticle December2012Document15 pagesF1 QandAarticle December2012ZHANG EmilyNo ratings yet

- Test Bank For Fundamentals of Advanced Accounting 7th Edition by HoyleDocument61 pagesTest Bank For Fundamentals of Advanced Accounting 7th Edition by Hoylezacharyjacobsgsoictjazw100% (34)

- Cta ConsoDocument356 pagesCta ConsoPANASHE MARTIN MASANGUDZANo ratings yet

- Christensen 12e Chap01 2019Document70 pagesChristensen 12e Chap01 2019Ibnu WibowoNo ratings yet

- Reporting Intercorporate Interests: Douglas CloudDocument98 pagesReporting Intercorporate Interests: Douglas CloudRendra Arief Hidayat.No ratings yet

- Chapter 17 Consolidated FS - Part 1Document29 pagesChapter 17 Consolidated FS - Part 1Erwin Labayog Medina100% (1)

- Solution Chapter 18Document61 pagesSolution Chapter 18xxxxxxxxx100% (3)

- Corporation Notes Title IV-XVDocument19 pagesCorporation Notes Title IV-XVSharn Linzi Buan MontañoNo ratings yet

- IAS 31 Interest in Joint VentureDocument5 pagesIAS 31 Interest in Joint Venturemasanun0% (1)

- Sem V Amalgamation - & - AbsorptionDocument3 pagesSem V Amalgamation - & - AbsorptionAnita SoniNo ratings yet

- Amalgamation PDFDocument9 pagesAmalgamation PDFPravesh SharmaNo ratings yet

- Chapter 5 SolutionsDocument21 pagesChapter 5 SolutionsIzu EvansNo ratings yet

- Full Download Fundamentals of Advanced Accounting 7th Edition Hoyle Solutions ManualDocument35 pagesFull Download Fundamentals of Advanced Accounting 7th Edition Hoyle Solutions Manualbaobabproceed.1lzgi1100% (32)

- Siemens Limited Annual Report 2013Document95 pagesSiemens Limited Annual Report 2013Akshay UkeyNo ratings yet

- Advanced Accounting SyllabusDocument4 pagesAdvanced Accounting Syllabusizza zahratunnisaNo ratings yet

- Chapter 17Document19 pagesChapter 17Christian Blanza LlevaNo ratings yet

- Rayhan Dewangga Saputra - Tugas AKL TM 4Document6 pagesRayhan Dewangga Saputra - Tugas AKL TM 4Rayhan Dewangga SaputraNo ratings yet

- CA Final - Financial Reporting Vol. 1Document905 pagesCA Final - Financial Reporting Vol. 1Gs Shiksha100% (6)

- Joint Arrangement HandoutDocument5 pagesJoint Arrangement HandoutClyde SaulNo ratings yet

- Advance Accounting Chapter 3 NotesDocument4 pagesAdvance Accounting Chapter 3 NotesUmema SiddiquiNo ratings yet

- AS - NotesDocument27 pagesAS - NotesRaksha ShettyNo ratings yet

- ECC6 Report ListsDocument12 pagesECC6 Report Listsdienda1No ratings yet

- 676254Document89 pages676254Shofiana IfadaNo ratings yet

- Income Tax Act, 1961Document13 pagesIncome Tax Act, 1961Sanketh_Surey_6489No ratings yet

Download as xlsx, pdf, or txt

You might also like

- Advanced Financial Accounting: Solutions ManualDocument89 pagesAdvanced Financial Accounting: Solutions ManualThùy Ngân100% (2)

- Questions For IFRS HighlightedDocument28 pagesQuestions For IFRS HighlightedWowee Cruz100% (1)

- Advanced Financial Accounting 11th Edition Christensen Test Bank DownloadDocument56 pagesAdvanced Financial Accounting 11th Edition Christensen Test Bank DownloadHeatherRobertstwopa100% (40)

- Consolidation Question Solution PDFDocument3 pagesConsolidation Question Solution PDFjoannejose2011100% (2)

- AFAR TestbankDocument56 pagesAFAR TestbankDrama SubsNo ratings yet

- Group Reporting S4Document31 pagesGroup Reporting S4rajesh1978.nair2381100% (2)

- RIL Excel Sheet FRADocument56 pagesRIL Excel Sheet FRAAditi AgrawalNo ratings yet

- WAMUNIMA. Financial Accounting 2 Assignment.Document8 pagesWAMUNIMA. Financial Accounting 2 Assignment.simpitorussellNo ratings yet

- Net Income 38000 Non Cash ItemsDocument8 pagesNet Income 38000 Non Cash ItemsHuu LuatNo ratings yet

- BusCom Practice SetsDocument20 pagesBusCom Practice SetsShaz NagaNo ratings yet

- Tut 11 Self SolutionDocument4 pagesTut 11 Self SolutionDuwaine BramwellNo ratings yet

- Dispenser of California - Rahul - MattaDocument9 pagesDispenser of California - Rahul - MattaHarsh MaheshwariNo ratings yet

- Chapter 5Document5 pagesChapter 5bonfaceNo ratings yet

- MaDocument6 pagesMaAashayNo ratings yet

- 14 Marks AnswersDocument42 pages14 Marks Answerskuvira LodhaNo ratings yet

- FA With AdjustmentsDocument14 pagesFA With AdjustmentsHarshini AkilandanNo ratings yet

- Module 6 Business Income Exercise SolutionsDocument13 pagesModule 6 Business Income Exercise SolutionshodaNo ratings yet

- Pomsky GroupDocument18 pagesPomsky GroupEduskill Learning CentreNo ratings yet

- Fund Flow StatementDocument41 pagesFund Flow StatementMahima SinghNo ratings yet

- Dargent Co. AnswerDocument4 pagesDargent Co. AnswerAbishek GuptaNo ratings yet

- Midterm Test 2Document7 pagesMidterm Test 2bangannguyen2020No ratings yet

- SKD 4Document6 pagesSKD 4DiryanNo ratings yet

- Exercises On DividendsDocument16 pagesExercises On DividendsGrace RoqueNo ratings yet

- FM Assignment1Document6 pagesFM Assignment1Rishi Kumar SainiNo ratings yet

- Akl - Agung Prabowo - 02 - 5-3Document3 pagesAkl - Agung Prabowo - 02 - 5-3Agung PrabowoNo ratings yet

- Cash Flow QN 3Document4 pagesCash Flow QN 3Takudzwa LanceNo ratings yet

- Alpha Manufacturing Ltd. (AML) - Cash Flow: Nrti Poa-Quiz 2 Time: 40 MinutesDocument4 pagesAlpha Manufacturing Ltd. (AML) - Cash Flow: Nrti Poa-Quiz 2 Time: 40 MinutesDeepak KumarNo ratings yet

- Jawaban P5-1Document3 pagesJawaban P5-1Nadillah LeicaNo ratings yet

- Holding Company Class Note 1Document6 pagesHolding Company Class Note 1sahir112001No ratings yet

- Zahra Calista LAB AKLDocument24 pagesZahra Calista LAB AKLzahra calista armansyahNo ratings yet

- Business ValuationDocument6 pagesBusiness ValuationlenoraNo ratings yet

- Questions For Unit 4 RevisionDocument3 pagesQuestions For Unit 4 RevisionDimple PatelNo ratings yet

- Non-Current Assets: Hnda 3 Year - 2 Semester 2016 Advanced Financial Reporting Model AnswersDocument8 pagesNon-Current Assets: Hnda 3 Year - 2 Semester 2016 Advanced Financial Reporting Model Answersrwl s.r.lNo ratings yet

- Cash Flow StatementDocument4 pagesCash Flow StatementNarayan DhunganaNo ratings yet

- Mand CHODocument7 pagesMand CHOMichael BaguyoNo ratings yet

- Comparison of Old and New Tax Regime 04042023Document3 pagesComparison of Old and New Tax Regime 04042023VenkateshNo ratings yet

- On January 1, Year 4, Grant Corporation BoughtDocument4 pagesOn January 1, Year 4, Grant Corporation BoughtJalaj GuptaNo ratings yet

- Problem Solving - Statement of Cash FlowDocument7 pagesProblem Solving - Statement of Cash FlowHossain AlmasNo ratings yet

- FM 2019 SolutionsDocument6 pagesFM 2019 Solutionsaditikotere92No ratings yet

- Cash Flow ProblemsDocument9 pagesCash Flow ProblemsSharu BsNo ratings yet

- Assignment 9Document10 pagesAssignment 9Jerickho JNo ratings yet

- Business Income Revision SheetsDocument79 pagesBusiness Income Revision Sheets123nishandhakall.dNo ratings yet

- Business Plan of Event Management: Submitted To: Miss Gurpreet KaurDocument21 pagesBusiness Plan of Event Management: Submitted To: Miss Gurpreet KaurPrashantNo ratings yet

- Acct6005 Company Accounting: Assessment 2 Case StudyDocument8 pagesAcct6005 Company Accounting: Assessment 2 Case StudyRuhan SinghNo ratings yet

- BTAXREV ACT 184 Week 3 Income Taxation - Tax ReturnsDocument21 pagesBTAXREV ACT 184 Week 3 Income Taxation - Tax ReturnsgatotkaNo ratings yet

- Binaluyo 2022 Chap 1 MCDocument16 pagesBinaluyo 2022 Chap 1 MCWere dooomedNo ratings yet

- Chapter 16 - Teacher's Manual - Aa Part 2Document18 pagesChapter 16 - Teacher's Manual - Aa Part 2IsyongNo ratings yet

- FAR - Financial Liabilities - Debt RestructuringDocument9 pagesFAR - Financial Liabilities - Debt Restructuringmarlout.saritaNo ratings yet

- Prodigal Co. 000$ W Nci Statement of Profit & Loss & Comprihensive IncomeDocument2 pagesProdigal Co. 000$ W Nci Statement of Profit & Loss & Comprihensive IncomeMuhammad MahmoodNo ratings yet

- P6.25 - Chapter 6Document5 pagesP6.25 - Chapter 6Dang PhuongNo ratings yet

- Consolidated FS - QUIZ PART 3Document4 pagesConsolidated FS - QUIZ PART 3Christine Jane Ramos100% (1)

- Lape - ACP312 - ULOa - Let's Analyze Week6Document3 pagesLape - ACP312 - ULOa - Let's Analyze Week6Bryle Jay LapeNo ratings yet

- Cash Flow 05 With Answers Just Give SolutionsDocument21 pagesCash Flow 05 With Answers Just Give SolutionsEdi wow WowNo ratings yet

- Accounting 15 Investment SolutionsDocument18 pagesAccounting 15 Investment Solutionskhyla Marie NooraNo ratings yet

- Cash and Credit ManagementDocument11 pagesCash and Credit Managementaoishic2025No ratings yet

- Key UNIT II B SubsequentDocument6 pagesKey UNIT II B SubsequentDaisy TañoteNo ratings yet

- AC - IntAcctg-C Prelims Solutions Sol, Janesene NDocument36 pagesAC - IntAcctg-C Prelims Solutions Sol, Janesene NJanesene SolNo ratings yet

- Module 2 Capital Budgeting Handout For LMS 2020Document11 pagesModule 2 Capital Budgeting Handout For LMS 2020sandeshNo ratings yet

- Jurnal: 2. Pengakuan Realisasi Home Office Branch OfficeDocument2 pagesJurnal: 2. Pengakuan Realisasi Home Office Branch OfficefaldyNo ratings yet

- Interim Financial Reporting and Operating Segment Discussion Problems and Answer KeyDocument4 pagesInterim Financial Reporting and Operating Segment Discussion Problems and Answer Keyprincess QNo ratings yet

- 3jun24 - Intercompany Transaction - EquipmentDocument16 pages3jun24 - Intercompany Transaction - Equipmentsisilia rachelNo ratings yet

- Balance Sheet Liabilities 2004 2005 Capital 120000 150000 Sundry Creditors 37000 25000 Bills Payable 15000 17000 P&L A/c 60000 69000 232000 261000Document17 pagesBalance Sheet Liabilities 2004 2005 Capital 120000 150000 Sundry Creditors 37000 25000 Bills Payable 15000 17000 P&L A/c 60000 69000 232000 261000kumaranil_1983No ratings yet

- LAB 4 Capital Budgeting 2024Document3 pagesLAB 4 Capital Budgeting 2024asthapatel.akpNo ratings yet

- Finding Balance 2016: Benchmarking the Performance of State-Owned Enterprise in Island CountriesFrom EverandFinding Balance 2016: Benchmarking the Performance of State-Owned Enterprise in Island CountriesNo ratings yet

- PPT5-Allocation and Depreciation of Differences Between Implied and Book ValuesDocument51 pagesPPT5-Allocation and Depreciation of Differences Between Implied and Book ValuesRifdah SaphiraNo ratings yet

- F1 QandAarticle December2012Document15 pagesF1 QandAarticle December2012ZHANG EmilyNo ratings yet

- Test Bank For Fundamentals of Advanced Accounting 7th Edition by HoyleDocument61 pagesTest Bank For Fundamentals of Advanced Accounting 7th Edition by Hoylezacharyjacobsgsoictjazw100% (34)

- Cta ConsoDocument356 pagesCta ConsoPANASHE MARTIN MASANGUDZANo ratings yet

- Christensen 12e Chap01 2019Document70 pagesChristensen 12e Chap01 2019Ibnu WibowoNo ratings yet

- Reporting Intercorporate Interests: Douglas CloudDocument98 pagesReporting Intercorporate Interests: Douglas CloudRendra Arief Hidayat.No ratings yet

- Chapter 17 Consolidated FS - Part 1Document29 pagesChapter 17 Consolidated FS - Part 1Erwin Labayog Medina100% (1)

- Solution Chapter 18Document61 pagesSolution Chapter 18xxxxxxxxx100% (3)

- Corporation Notes Title IV-XVDocument19 pagesCorporation Notes Title IV-XVSharn Linzi Buan MontañoNo ratings yet

- IAS 31 Interest in Joint VentureDocument5 pagesIAS 31 Interest in Joint Venturemasanun0% (1)

- Sem V Amalgamation - & - AbsorptionDocument3 pagesSem V Amalgamation - & - AbsorptionAnita SoniNo ratings yet

- Amalgamation PDFDocument9 pagesAmalgamation PDFPravesh SharmaNo ratings yet

- Chapter 5 SolutionsDocument21 pagesChapter 5 SolutionsIzu EvansNo ratings yet

- Full Download Fundamentals of Advanced Accounting 7th Edition Hoyle Solutions ManualDocument35 pagesFull Download Fundamentals of Advanced Accounting 7th Edition Hoyle Solutions Manualbaobabproceed.1lzgi1100% (32)

- Siemens Limited Annual Report 2013Document95 pagesSiemens Limited Annual Report 2013Akshay UkeyNo ratings yet

- Advanced Accounting SyllabusDocument4 pagesAdvanced Accounting Syllabusizza zahratunnisaNo ratings yet

- Chapter 17Document19 pagesChapter 17Christian Blanza LlevaNo ratings yet

- Rayhan Dewangga Saputra - Tugas AKL TM 4Document6 pagesRayhan Dewangga Saputra - Tugas AKL TM 4Rayhan Dewangga SaputraNo ratings yet

- CA Final - Financial Reporting Vol. 1Document905 pagesCA Final - Financial Reporting Vol. 1Gs Shiksha100% (6)

- Joint Arrangement HandoutDocument5 pagesJoint Arrangement HandoutClyde SaulNo ratings yet

- Advance Accounting Chapter 3 NotesDocument4 pagesAdvance Accounting Chapter 3 NotesUmema SiddiquiNo ratings yet

- AS - NotesDocument27 pagesAS - NotesRaksha ShettyNo ratings yet

- ECC6 Report ListsDocument12 pagesECC6 Report Listsdienda1No ratings yet

- 676254Document89 pages676254Shofiana IfadaNo ratings yet

- Income Tax Act, 1961Document13 pagesIncome Tax Act, 1961Sanketh_Surey_6489No ratings yet