Student May Add To The List of Assumptions

Student May Add To The List of Assumptions

You might also like

- Original PDF Essential Communication by Ronald Adler PDFDocument41 pagesOriginal PDF Essential Communication by Ronald Adler PDFmary.burklow183100% (34)

- FIN 3512 Fall 2019 Quiz #1 9.18.2019 To UploadDocument3 pagesFIN 3512 Fall 2019 Quiz #1 9.18.2019 To UploadgNo ratings yet

- Primera Entrega Cultura y Economia Regional de EuropaDocument20 pagesPrimera Entrega Cultura y Economia Regional de EuropaAndrea Lara0% (1)

- Abbott Laboratories (Pakistan) Limited-1Document9 pagesAbbott Laboratories (Pakistan) Limited-1Shahrukh1994007No ratings yet

- Tutorial 2 QuestionsDocument4 pagesTutorial 2 Questionsguan junyanNo ratings yet

- Design of Air Conditioning and Ventilation System For A Multi Storey Office BuildingDocument5 pagesDesign of Air Conditioning and Ventilation System For A Multi Storey Office BuildingIppiNo ratings yet

- Folk Violin SongbookDocument19 pagesFolk Violin SongbookTyler Swinn100% (1)

- Abhilash N - BVDocument10 pagesAbhilash N - BVAbhilash NNo ratings yet

- Module 3 Chapter 15 DCF ModelDocument5 pagesModule 3 Chapter 15 DCF ModelAvinash GanesanNo ratings yet

- Symbiosis Law School, Pune: A F M I A - 1Document10 pagesSymbiosis Law School, Pune: A F M I A - 1pranjalNo ratings yet

- Symbiosis Law School, Pune: A F M I A - 1Document11 pagesSymbiosis Law School, Pune: A F M I A - 1pranjalNo ratings yet

- Kotak Mahindra Bank Limited Consolidated Financials FY18Document60 pagesKotak Mahindra Bank Limited Consolidated Financials FY18Kunal ObhraiNo ratings yet

- Calculation of Free Cashflow To The Firm: DCF Valuation (Amounts in Millions)Document1 pageCalculation of Free Cashflow To The Firm: DCF Valuation (Amounts in Millions)Prachi NavghareNo ratings yet

- LBO Assignment (AIM)Document20 pagesLBO Assignment (AIM)prachiNo ratings yet

- Year 2018 2019 2020: Task 1Document9 pagesYear 2018 2019 2020: Task 1Prateek ChandnaNo ratings yet

- Quarterly Update Q4FY20: Visaka Industries LTDDocument10 pagesQuarterly Update Q4FY20: Visaka Industries LTDsherwinmitraNo ratings yet

- FMO M5 Soln.sDocument16 pagesFMO M5 Soln.sVishwas ParakkaNo ratings yet

- Lucky CementDocument45 pagesLucky Cementaleema anjumNo ratings yet

- GR I Crew XV 2018 TcsDocument79 pagesGR I Crew XV 2018 TcsMUKESH KUMARNo ratings yet

- Financial Ratio Assessment 3 Template v2-1Document2 pagesFinancial Ratio Assessment 3 Template v2-1Rao waqarNo ratings yet

- Financial Analysis Template FinalDocument8 pagesFinancial Analysis Template FinalHarit keshruwalaNo ratings yet

- FFM - Assignment 3 Working SheetDocument4 pagesFFM - Assignment 3 Working SheetSubscribe PranksNo ratings yet

- Free Cash Flow Estimate (In INR CRS)Document2 pagesFree Cash Flow Estimate (In INR CRS)Kapil KhannaNo ratings yet

- Also Annual Report Gb2022 enDocument198 pagesAlso Annual Report Gb2022 enmihirbhojani603No ratings yet

- Q3FY21 Result Update Axis Bank: Towards End of Peak Credit Cost CycleDocument12 pagesQ3FY21 Result Update Axis Bank: Towards End of Peak Credit Cost CycleSAGAR VAZIRANINo ratings yet

- Dupont Analysis 3 FactorDocument7 pagesDupont Analysis 3 FactorVasavi MendaNo ratings yet

- UntitledDocument8 pagesUntitledPravin AmirthNo ratings yet

- FCFF Vs Fcfe StudentDocument5 pagesFCFF Vs Fcfe StudentKanchan GuptaNo ratings yet

- Chapter 1: Investment Recommendation: How We Have Derived The Summed Up ValueDocument4 pagesChapter 1: Investment Recommendation: How We Have Derived The Summed Up ValueMd. Mehedi HasanNo ratings yet

- Akash 5yr PidiliteDocument9 pagesAkash 5yr PidiliteAkash Didharia100% (1)

- BIOCON Ratio AnalysisDocument3 pagesBIOCON Ratio AnalysisVinuNo ratings yet

- TVS Motors Live Project Final 2Document39 pagesTVS Motors Live Project Final 2ritususmitakarNo ratings yet

- Earnings Presentation: Bse Code: 524558 - Nse Symbol: Neulandlab - Bloomberg: Nll:In - Reuters: Neul - NsDocument34 pagesEarnings Presentation: Bse Code: 524558 - Nse Symbol: Neulandlab - Bloomberg: Nll:In - Reuters: Neul - Nssunil.dasarath jadhavNo ratings yet

- Business Finance ProjectDocument9 pagesBusiness Finance Projectmuhammad muzzammilNo ratings yet

- Review: Ten Year (Standalone)Document10 pagesReview: Ten Year (Standalone)maruthi631No ratings yet

- Presentation H1 2022Document43 pagesPresentation H1 2022Tran Thi ThuongNo ratings yet

- Microsoft Investment AnalysisDocument4 pagesMicrosoft Investment AnalysisdkrauzaNo ratings yet

- 2022 10 20 PH S CNVRGDocument7 pages2022 10 20 PH S CNVRGValiente RandzNo ratings yet

- IndusInd BankDocument9 pagesIndusInd BankSrinivas NandikantiNo ratings yet

- Financial Modelling Mid Term: Do Not Hard Code Any Solution Hard Coded Solution Will Not Be Awarded Any MarksDocument7 pagesFinancial Modelling Mid Term: Do Not Hard Code Any Solution Hard Coded Solution Will Not Be Awarded Any MarksSAMBUDDHA ROYNo ratings yet

- We Have Taken 10-Year Government Bond Rate (G) FCF × (1 + G) ÷ (R - G) TV / (1 + R)Document3 pagesWe Have Taken 10-Year Government Bond Rate (G) FCF × (1 + G) ÷ (R - G) TV / (1 + R)mayankNo ratings yet

- Finance KT-5: ValuationDocument15 pagesFinance KT-5: ValuationABHIJEET BHUNIA MBA 2021-23 (Delhi)No ratings yet

- BHEL Valuation of CompanyDocument23 pagesBHEL Valuation of CompanyVishalNo ratings yet

- Bhavak Dixit (PGFC2113) PI Industries PVT - LTDDocument45 pagesBhavak Dixit (PGFC2113) PI Industries PVT - LTDdixitBhavak DixitNo ratings yet

- Sample URC-FS Projection Corp-PlanDocument7 pagesSample URC-FS Projection Corp-PlanrcdcaviteNo ratings yet

- Maryam Ehsan Assignment 3 1747140 Q # 01Document2 pagesMaryam Ehsan Assignment 3 1747140 Q # 01Maryam EhsanNo ratings yet

- Particulars (INR in Crores) FY2015A FY2016A FY2017A FY2018ADocument6 pagesParticulars (INR in Crores) FY2015A FY2016A FY2017A FY2018AHamzah HakeemNo ratings yet

- Onsite Day Care ValuationDocument2 pagesOnsite Day Care Valuationjindalmanoj06No ratings yet

- The Discounted Free Cash Flow Model For A Complete BusinessDocument5 pagesThe Discounted Free Cash Flow Model For A Complete BusinessSanket DubeyNo ratings yet

- Valuation of Tata Power, Based On Prof. Aswath Damodaran: DCF Base Year 1 2 3 AssumptionsDocument6 pagesValuation of Tata Power, Based On Prof. Aswath Damodaran: DCF Base Year 1 2 3 Assumptionspriyal batraNo ratings yet

- Deliverable #1 - Fiat Chrysler and VolkswagenDocument4 pagesDeliverable #1 - Fiat Chrysler and VolkswagenSavitaNo ratings yet

- Bluedart Express: Strategic Investments Continue To Weigh On MarginsDocument9 pagesBluedart Express: Strategic Investments Continue To Weigh On MarginsYash AgarwalNo ratings yet

- Inputs From Income Statement:: Total RevenueDocument6 pagesInputs From Income Statement:: Total RevenuecarminatNo ratings yet

- Smic - DCF & Computations - de Asis - Gomez - TriviñoDocument47 pagesSmic - DCF & Computations - de Asis - Gomez - TriviñoDiana De AsisNo ratings yet

- Smic - DCF - de Asis - Gomez - TriviñoDocument36 pagesSmic - DCF - de Asis - Gomez - TriviñoDiana De AsisNo ratings yet

- Parag Q2 FY19 EdelDocument9 pagesParag Q2 FY19 EdelRohan AdlakhaNo ratings yet

- Financial Modeling CMDocument3 pagesFinancial Modeling CMAreeba Aslam100% (1)

- 2024 05 03 PH e RrhiDocument9 pages2024 05 03 PH e Rrhiphilnabank1217No ratings yet

- 28feb - DCF Worksheets - Pt3 - AGELDocument18 pages28feb - DCF Worksheets - Pt3 - AGELsrishtirungta2000No ratings yet

- Vertical & Horizontal AnalysisDocument11 pagesVertical & Horizontal Analysisstd25732No ratings yet

- ValuationDocument18 pagesValuationsanket patilNo ratings yet

- DCF AnalysisDocument7 pagesDCF AnalysisRiazul Islam TuhinNo ratings yet

- Kuhne NagelDocument133 pagesKuhne NagelKakoNo ratings yet

- To the Moon Investing: Visually Mapping Your Winning Stock Market PortfolioFrom EverandTo the Moon Investing: Visually Mapping Your Winning Stock Market PortfolioNo ratings yet

- Abhilash N - FIMDocument6 pagesAbhilash N - FIMAbhilash NNo ratings yet

- Fixed Income Markets - Assignment: Symbiosis School of Banking and Finance (SSBF)Document10 pagesFixed Income Markets - Assignment: Symbiosis School of Banking and Finance (SSBF)Abhilash NNo ratings yet

- Abhilash N - BVDocument10 pagesAbhilash N - BVAbhilash NNo ratings yet

- Companies - FormationDocument7 pagesCompanies - FormationAbhilash NNo ratings yet

- Sarsam2010 PDFDocument9 pagesSarsam2010 PDFlookNo ratings yet

- Canadian Jeweller January / February 2011 IssueDocument84 pagesCanadian Jeweller January / February 2011 IssuerivegaucheNo ratings yet

- Navasakam Grievance Application: Family DetailsDocument2 pagesNavasakam Grievance Application: Family DetailsmANOHARNo ratings yet

- Car Radio Frame AndroidDocument23 pagesCar Radio Frame AndroidSopheak NGORNo ratings yet

- My 100 Colour Pencil PortraitsDocument102 pagesMy 100 Colour Pencil PortraitsAnonymous 5u2Cvl100% (2)

- Factoring HandoutDocument2 pagesFactoring HandoutJordan SenkoNo ratings yet

- Corporate Nvidia in BriefDocument2 pagesCorporate Nvidia in BriefakesplwebsiteNo ratings yet

- Bills Discounting Agreement South Indian Bank PDFDocument7 pagesBills Discounting Agreement South Indian Bank PDFbaba ramdevNo ratings yet

- Power Electronic Unit For Field-Mounting (Contrac) EBN853, EBN861Document44 pagesPower Electronic Unit For Field-Mounting (Contrac) EBN853, EBN861Sad LiveNo ratings yet

- Residence Time Distribution For Chemical ReactorsDocument71 pagesResidence Time Distribution For Chemical ReactorsJuan Carlos Serrano MedranoNo ratings yet

- Audio 4 - 1 Travelling 1Document15 pagesAudio 4 - 1 Travelling 1Farewell03311No ratings yet

- Case Studies in Strategy (Catalogue III)Document130 pagesCase Studies in Strategy (Catalogue III)TahseenRanaNo ratings yet

- Aquagen: Recombination System For Stationary BatteriesDocument2 pagesAquagen: Recombination System For Stationary BatteriestaahaNo ratings yet

- Invoice 203265: GN Code: 3923.2100 - SwedenDocument2 pagesInvoice 203265: GN Code: 3923.2100 - SwedenArturo RiveroNo ratings yet

- Beam-Column-Design-SBC-306-2007-by KoushikDocument37 pagesBeam-Column-Design-SBC-306-2007-by KoushikSuperkineticNo ratings yet

- VIR - Reform in TelecommunicationsDocument10 pagesVIR - Reform in TelecommunicationsNgu HoangNo ratings yet

- USB TO RS232 Cable For Windows 2000 User's ManualDocument7 pagesUSB TO RS232 Cable For Windows 2000 User's ManualOsvaldo Loyde AlvaradoNo ratings yet

- Digital Control Systems (Elective) : Suggested ReadingDocument1 pageDigital Control Systems (Elective) : Suggested ReadingBebo DiaNo ratings yet

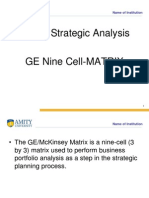

- GE - Nine CellDocument12 pagesGE - Nine CellNikita SangalNo ratings yet

- 014 - 030 Single Reduction Worm IntroductionDocument17 pages014 - 030 Single Reduction Worm IntroductionAlejandro MartinezNo ratings yet

- 3500 Most Common Chinese CharactersDocument2 pages3500 Most Common Chinese CharactersSub 2 PewdsNo ratings yet

- Applied Physics On Spectros PDFDocument71 pagesApplied Physics On Spectros PDFKaskus FourusNo ratings yet

- Sma Negeri 1 Kotabaru: I. Answer The Following Question!Document6 pagesSma Negeri 1 Kotabaru: I. Answer The Following Question!Dian MardhikaNo ratings yet

- Jargeous - Product - Catalog Ver 1220 Compressed PDFDocument16 pagesJargeous - Product - Catalog Ver 1220 Compressed PDFFirdaus YahyaNo ratings yet

- Fybaf Sem 2 Business Law1 Sample Question BankDocument21 pagesFybaf Sem 2 Business Law1 Sample Question BankDeepa BhatiaNo ratings yet

- Final Sample Report of Maruti Car CompanyDocument69 pagesFinal Sample Report of Maruti Car Companyofficial vrNo ratings yet

Download as xlsx, pdf, or txt

You might also like

- Original PDF Essential Communication by Ronald Adler PDFDocument41 pagesOriginal PDF Essential Communication by Ronald Adler PDFmary.burklow183100% (34)

- FIN 3512 Fall 2019 Quiz #1 9.18.2019 To UploadDocument3 pagesFIN 3512 Fall 2019 Quiz #1 9.18.2019 To UploadgNo ratings yet

- Primera Entrega Cultura y Economia Regional de EuropaDocument20 pagesPrimera Entrega Cultura y Economia Regional de EuropaAndrea Lara0% (1)

- Abbott Laboratories (Pakistan) Limited-1Document9 pagesAbbott Laboratories (Pakistan) Limited-1Shahrukh1994007No ratings yet

- Tutorial 2 QuestionsDocument4 pagesTutorial 2 Questionsguan junyanNo ratings yet

- Design of Air Conditioning and Ventilation System For A Multi Storey Office BuildingDocument5 pagesDesign of Air Conditioning and Ventilation System For A Multi Storey Office BuildingIppiNo ratings yet

- Folk Violin SongbookDocument19 pagesFolk Violin SongbookTyler Swinn100% (1)

- Abhilash N - BVDocument10 pagesAbhilash N - BVAbhilash NNo ratings yet

- Module 3 Chapter 15 DCF ModelDocument5 pagesModule 3 Chapter 15 DCF ModelAvinash GanesanNo ratings yet

- Symbiosis Law School, Pune: A F M I A - 1Document10 pagesSymbiosis Law School, Pune: A F M I A - 1pranjalNo ratings yet

- Symbiosis Law School, Pune: A F M I A - 1Document11 pagesSymbiosis Law School, Pune: A F M I A - 1pranjalNo ratings yet

- Kotak Mahindra Bank Limited Consolidated Financials FY18Document60 pagesKotak Mahindra Bank Limited Consolidated Financials FY18Kunal ObhraiNo ratings yet

- Calculation of Free Cashflow To The Firm: DCF Valuation (Amounts in Millions)Document1 pageCalculation of Free Cashflow To The Firm: DCF Valuation (Amounts in Millions)Prachi NavghareNo ratings yet

- LBO Assignment (AIM)Document20 pagesLBO Assignment (AIM)prachiNo ratings yet

- Year 2018 2019 2020: Task 1Document9 pagesYear 2018 2019 2020: Task 1Prateek ChandnaNo ratings yet

- Quarterly Update Q4FY20: Visaka Industries LTDDocument10 pagesQuarterly Update Q4FY20: Visaka Industries LTDsherwinmitraNo ratings yet

- FMO M5 Soln.sDocument16 pagesFMO M5 Soln.sVishwas ParakkaNo ratings yet

- Lucky CementDocument45 pagesLucky Cementaleema anjumNo ratings yet

- GR I Crew XV 2018 TcsDocument79 pagesGR I Crew XV 2018 TcsMUKESH KUMARNo ratings yet

- Financial Ratio Assessment 3 Template v2-1Document2 pagesFinancial Ratio Assessment 3 Template v2-1Rao waqarNo ratings yet

- Financial Analysis Template FinalDocument8 pagesFinancial Analysis Template FinalHarit keshruwalaNo ratings yet

- FFM - Assignment 3 Working SheetDocument4 pagesFFM - Assignment 3 Working SheetSubscribe PranksNo ratings yet

- Free Cash Flow Estimate (In INR CRS)Document2 pagesFree Cash Flow Estimate (In INR CRS)Kapil KhannaNo ratings yet

- Also Annual Report Gb2022 enDocument198 pagesAlso Annual Report Gb2022 enmihirbhojani603No ratings yet

- Q3FY21 Result Update Axis Bank: Towards End of Peak Credit Cost CycleDocument12 pagesQ3FY21 Result Update Axis Bank: Towards End of Peak Credit Cost CycleSAGAR VAZIRANINo ratings yet

- Dupont Analysis 3 FactorDocument7 pagesDupont Analysis 3 FactorVasavi MendaNo ratings yet

- UntitledDocument8 pagesUntitledPravin AmirthNo ratings yet

- FCFF Vs Fcfe StudentDocument5 pagesFCFF Vs Fcfe StudentKanchan GuptaNo ratings yet

- Chapter 1: Investment Recommendation: How We Have Derived The Summed Up ValueDocument4 pagesChapter 1: Investment Recommendation: How We Have Derived The Summed Up ValueMd. Mehedi HasanNo ratings yet

- Akash 5yr PidiliteDocument9 pagesAkash 5yr PidiliteAkash Didharia100% (1)

- BIOCON Ratio AnalysisDocument3 pagesBIOCON Ratio AnalysisVinuNo ratings yet

- TVS Motors Live Project Final 2Document39 pagesTVS Motors Live Project Final 2ritususmitakarNo ratings yet

- Earnings Presentation: Bse Code: 524558 - Nse Symbol: Neulandlab - Bloomberg: Nll:In - Reuters: Neul - NsDocument34 pagesEarnings Presentation: Bse Code: 524558 - Nse Symbol: Neulandlab - Bloomberg: Nll:In - Reuters: Neul - Nssunil.dasarath jadhavNo ratings yet

- Business Finance ProjectDocument9 pagesBusiness Finance Projectmuhammad muzzammilNo ratings yet

- Review: Ten Year (Standalone)Document10 pagesReview: Ten Year (Standalone)maruthi631No ratings yet

- Presentation H1 2022Document43 pagesPresentation H1 2022Tran Thi ThuongNo ratings yet

- Microsoft Investment AnalysisDocument4 pagesMicrosoft Investment AnalysisdkrauzaNo ratings yet

- 2022 10 20 PH S CNVRGDocument7 pages2022 10 20 PH S CNVRGValiente RandzNo ratings yet

- IndusInd BankDocument9 pagesIndusInd BankSrinivas NandikantiNo ratings yet

- Financial Modelling Mid Term: Do Not Hard Code Any Solution Hard Coded Solution Will Not Be Awarded Any MarksDocument7 pagesFinancial Modelling Mid Term: Do Not Hard Code Any Solution Hard Coded Solution Will Not Be Awarded Any MarksSAMBUDDHA ROYNo ratings yet

- We Have Taken 10-Year Government Bond Rate (G) FCF × (1 + G) ÷ (R - G) TV / (1 + R)Document3 pagesWe Have Taken 10-Year Government Bond Rate (G) FCF × (1 + G) ÷ (R - G) TV / (1 + R)mayankNo ratings yet

- Finance KT-5: ValuationDocument15 pagesFinance KT-5: ValuationABHIJEET BHUNIA MBA 2021-23 (Delhi)No ratings yet

- BHEL Valuation of CompanyDocument23 pagesBHEL Valuation of CompanyVishalNo ratings yet

- Bhavak Dixit (PGFC2113) PI Industries PVT - LTDDocument45 pagesBhavak Dixit (PGFC2113) PI Industries PVT - LTDdixitBhavak DixitNo ratings yet

- Sample URC-FS Projection Corp-PlanDocument7 pagesSample URC-FS Projection Corp-PlanrcdcaviteNo ratings yet

- Maryam Ehsan Assignment 3 1747140 Q # 01Document2 pagesMaryam Ehsan Assignment 3 1747140 Q # 01Maryam EhsanNo ratings yet

- Particulars (INR in Crores) FY2015A FY2016A FY2017A FY2018ADocument6 pagesParticulars (INR in Crores) FY2015A FY2016A FY2017A FY2018AHamzah HakeemNo ratings yet

- Onsite Day Care ValuationDocument2 pagesOnsite Day Care Valuationjindalmanoj06No ratings yet

- The Discounted Free Cash Flow Model For A Complete BusinessDocument5 pagesThe Discounted Free Cash Flow Model For A Complete BusinessSanket DubeyNo ratings yet

- Valuation of Tata Power, Based On Prof. Aswath Damodaran: DCF Base Year 1 2 3 AssumptionsDocument6 pagesValuation of Tata Power, Based On Prof. Aswath Damodaran: DCF Base Year 1 2 3 Assumptionspriyal batraNo ratings yet

- Deliverable #1 - Fiat Chrysler and VolkswagenDocument4 pagesDeliverable #1 - Fiat Chrysler and VolkswagenSavitaNo ratings yet

- Bluedart Express: Strategic Investments Continue To Weigh On MarginsDocument9 pagesBluedart Express: Strategic Investments Continue To Weigh On MarginsYash AgarwalNo ratings yet

- Inputs From Income Statement:: Total RevenueDocument6 pagesInputs From Income Statement:: Total RevenuecarminatNo ratings yet

- Smic - DCF & Computations - de Asis - Gomez - TriviñoDocument47 pagesSmic - DCF & Computations - de Asis - Gomez - TriviñoDiana De AsisNo ratings yet

- Smic - DCF - de Asis - Gomez - TriviñoDocument36 pagesSmic - DCF - de Asis - Gomez - TriviñoDiana De AsisNo ratings yet

- Parag Q2 FY19 EdelDocument9 pagesParag Q2 FY19 EdelRohan AdlakhaNo ratings yet

- Financial Modeling CMDocument3 pagesFinancial Modeling CMAreeba Aslam100% (1)

- 2024 05 03 PH e RrhiDocument9 pages2024 05 03 PH e Rrhiphilnabank1217No ratings yet

- 28feb - DCF Worksheets - Pt3 - AGELDocument18 pages28feb - DCF Worksheets - Pt3 - AGELsrishtirungta2000No ratings yet

- Vertical & Horizontal AnalysisDocument11 pagesVertical & Horizontal Analysisstd25732No ratings yet

- ValuationDocument18 pagesValuationsanket patilNo ratings yet

- DCF AnalysisDocument7 pagesDCF AnalysisRiazul Islam TuhinNo ratings yet

- Kuhne NagelDocument133 pagesKuhne NagelKakoNo ratings yet

- To the Moon Investing: Visually Mapping Your Winning Stock Market PortfolioFrom EverandTo the Moon Investing: Visually Mapping Your Winning Stock Market PortfolioNo ratings yet

- Abhilash N - FIMDocument6 pagesAbhilash N - FIMAbhilash NNo ratings yet

- Fixed Income Markets - Assignment: Symbiosis School of Banking and Finance (SSBF)Document10 pagesFixed Income Markets - Assignment: Symbiosis School of Banking and Finance (SSBF)Abhilash NNo ratings yet

- Abhilash N - BVDocument10 pagesAbhilash N - BVAbhilash NNo ratings yet

- Companies - FormationDocument7 pagesCompanies - FormationAbhilash NNo ratings yet

- Sarsam2010 PDFDocument9 pagesSarsam2010 PDFlookNo ratings yet

- Canadian Jeweller January / February 2011 IssueDocument84 pagesCanadian Jeweller January / February 2011 IssuerivegaucheNo ratings yet

- Navasakam Grievance Application: Family DetailsDocument2 pagesNavasakam Grievance Application: Family DetailsmANOHARNo ratings yet

- Car Radio Frame AndroidDocument23 pagesCar Radio Frame AndroidSopheak NGORNo ratings yet

- My 100 Colour Pencil PortraitsDocument102 pagesMy 100 Colour Pencil PortraitsAnonymous 5u2Cvl100% (2)

- Factoring HandoutDocument2 pagesFactoring HandoutJordan SenkoNo ratings yet

- Corporate Nvidia in BriefDocument2 pagesCorporate Nvidia in BriefakesplwebsiteNo ratings yet

- Bills Discounting Agreement South Indian Bank PDFDocument7 pagesBills Discounting Agreement South Indian Bank PDFbaba ramdevNo ratings yet

- Power Electronic Unit For Field-Mounting (Contrac) EBN853, EBN861Document44 pagesPower Electronic Unit For Field-Mounting (Contrac) EBN853, EBN861Sad LiveNo ratings yet

- Residence Time Distribution For Chemical ReactorsDocument71 pagesResidence Time Distribution For Chemical ReactorsJuan Carlos Serrano MedranoNo ratings yet

- Audio 4 - 1 Travelling 1Document15 pagesAudio 4 - 1 Travelling 1Farewell03311No ratings yet

- Case Studies in Strategy (Catalogue III)Document130 pagesCase Studies in Strategy (Catalogue III)TahseenRanaNo ratings yet

- Aquagen: Recombination System For Stationary BatteriesDocument2 pagesAquagen: Recombination System For Stationary BatteriestaahaNo ratings yet

- Invoice 203265: GN Code: 3923.2100 - SwedenDocument2 pagesInvoice 203265: GN Code: 3923.2100 - SwedenArturo RiveroNo ratings yet

- Beam-Column-Design-SBC-306-2007-by KoushikDocument37 pagesBeam-Column-Design-SBC-306-2007-by KoushikSuperkineticNo ratings yet

- VIR - Reform in TelecommunicationsDocument10 pagesVIR - Reform in TelecommunicationsNgu HoangNo ratings yet

- USB TO RS232 Cable For Windows 2000 User's ManualDocument7 pagesUSB TO RS232 Cable For Windows 2000 User's ManualOsvaldo Loyde AlvaradoNo ratings yet

- Digital Control Systems (Elective) : Suggested ReadingDocument1 pageDigital Control Systems (Elective) : Suggested ReadingBebo DiaNo ratings yet

- GE - Nine CellDocument12 pagesGE - Nine CellNikita SangalNo ratings yet

- 014 - 030 Single Reduction Worm IntroductionDocument17 pages014 - 030 Single Reduction Worm IntroductionAlejandro MartinezNo ratings yet

- 3500 Most Common Chinese CharactersDocument2 pages3500 Most Common Chinese CharactersSub 2 PewdsNo ratings yet

- Applied Physics On Spectros PDFDocument71 pagesApplied Physics On Spectros PDFKaskus FourusNo ratings yet

- Sma Negeri 1 Kotabaru: I. Answer The Following Question!Document6 pagesSma Negeri 1 Kotabaru: I. Answer The Following Question!Dian MardhikaNo ratings yet

- Jargeous - Product - Catalog Ver 1220 Compressed PDFDocument16 pagesJargeous - Product - Catalog Ver 1220 Compressed PDFFirdaus YahyaNo ratings yet

- Fybaf Sem 2 Business Law1 Sample Question BankDocument21 pagesFybaf Sem 2 Business Law1 Sample Question BankDeepa BhatiaNo ratings yet

- Final Sample Report of Maruti Car CompanyDocument69 pagesFinal Sample Report of Maruti Car Companyofficial vrNo ratings yet