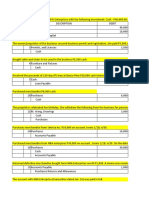

Divided by 65%: Fringe Benefit P14,400 Monetary Value P14,400

Divided by 65%: Fringe Benefit P14,400 Monetary Value P14,400

You might also like

- Qaisar Naveed Bank Statement 1 YearDocument20 pagesQaisar Naveed Bank Statement 1 Yearisrargondal786123100% (1)

- TAXDocument10 pagesTAXJeana Segumalian100% (3)

- Tax Compliance Survey QuestionnaireDocument4 pagesTax Compliance Survey QuestionnaireJennelyn Abella76% (21)

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- Taxation First Preboard 93 - QuestionnaireDocument16 pagesTaxation First Preboard 93 - QuestionnaireAmeroden AbdullahNo ratings yet

- TAX-06-FRINGE-BENEFITS-TAX (With Answers) WITHOUT TYPODocument8 pagesTAX-06-FRINGE-BENEFITS-TAX (With Answers) WITHOUT TYPOKendrew Sujide100% (1)

- Individual Income TaxDocument13 pagesIndividual Income TaxDaniel Dialino100% (1)

- 4 2020 UP BOC Taxation Law Reviewer PDFDocument263 pages4 2020 UP BOC Taxation Law Reviewer PDFRose Ann Lascuña90% (10)

- Midterm Examination With SolutionDocument2 pagesMidterm Examination With SolutionSeulgi Bear100% (1)

- Fringe Benefit Part 3Document24 pagesFringe Benefit Part 3kitkathyNo ratings yet

- Fringe Benefits and Fringe Benefit Tax ExercisesDocument3 pagesFringe Benefits and Fringe Benefit Tax Exercisesaj lopezNo ratings yet

- Resources Understanding ISO20022 NACHA Payments 2013Document121 pagesResources Understanding ISO20022 NACHA Payments 2013Rajendra PilludaNo ratings yet

- Fringe Benefit TAX: Mr. Mario M. Castro, Cpa, Mba Tax ConsultantDocument19 pagesFringe Benefit TAX: Mr. Mario M. Castro, Cpa, Mba Tax ConsultantKristine Aubrey AlvarezNo ratings yet

- Fringe Benefits 1Document13 pagesFringe Benefits 1Jessa Mae ZamudioNo ratings yet

- Average Quiz Set ADocument5 pagesAverage Quiz Set AMarvin AndresNo ratings yet

- Tax - 2nd Monthly Assessment - QuestionsDocument12 pagesTax - 2nd Monthly Assessment - QuestionsGRACELYN SOJORNo ratings yet

- Midterm Exam Principles of Taxation and Income TaxationDocument6 pagesMidterm Exam Principles of Taxation and Income TaxationKitagawa, Misia Sophia Jan B.No ratings yet

- Inge BenefitsDocument7 pagesInge BenefitsKarleen RazonabeNo ratings yet

- AFAR 1 Exams 2020Document7 pagesAFAR 1 Exams 2020RJ Kristine DaqueNo ratings yet

- Fringe Benefit - QuizDocument3 pagesFringe Benefit - QuizArlea AsenciNo ratings yet

- Fringe Benefit - QuizDocument3 pagesFringe Benefit - QuizArlea AsenciNo ratings yet

- Yellow - Not Sure, Green - CorrectDocument7 pagesYellow - Not Sure, Green - CorrectIsaiah John Domenic M. CantaneroNo ratings yet

- 2nd Quizzer 1st Sem SY 2020-2021 - AKDocument6 pages2nd Quizzer 1st Sem SY 2020-2021 - AKMitzi WamarNo ratings yet

- Fringe Benefit TaxDocument4 pagesFringe Benefit TaxKenneth Bryan Tegerero Tegio100% (1)

- Tax 1st Preboard A LUDocument9 pagesTax 1st Preboard A LUAnonymous 7HGskNNo ratings yet

- TAXDocument20 pagesTAXkate trishaNo ratings yet

- Theories: B. 2 and 3 OnlyDocument5 pagesTheories: B. 2 and 3 OnlyLucille Mae EndigaNo ratings yet

- Ea - TaxDocument8 pagesEa - TaxKc SevillaNo ratings yet

- Tax Computations SampleDocument5 pagesTax Computations Samplelcsme tubodaccountsNo ratings yet

- Partnership Operations (Additional Sample Problems)Document5 pagesPartnership Operations (Additional Sample Problems)Pauline Anne LopezNo ratings yet

- Sample Problem Accounting Taxation 1Document4 pagesSample Problem Accounting Taxation 1carl patNo ratings yet

- Practical Accounting TwoDocument25 pagesPractical Accounting TwoJoseph SalidoNo ratings yet

- Income Taxation 1Document4 pagesIncome Taxation 1nicole bancoroNo ratings yet

- Instruction: Write The Letter of Your Choice On The Space Provided Before The NumberDocument4 pagesInstruction: Write The Letter of Your Choice On The Space Provided Before The NumberASDDD100% (2)

- FBT Sample ComputationsDocument3 pagesFBT Sample ComputationsLynn HermNo ratings yet

- Taxation Material 2Document7 pagesTaxation Material 2Shaira BugayongNo ratings yet

- Partnership OperationDocument3 pagesPartnership Operationbrmo.amatorio.uiNo ratings yet

- 8.6 Assignment - Regular Income Tax On CorporationsDocument3 pages8.6 Assignment - Regular Income Tax On CorporationsRoselyn LumbaoNo ratings yet

- Fat Deferred Income TaxDocument2 pagesFat Deferred Income Taxnicole bancoroNo ratings yet

- Practical Accounting TwoDocument48 pagesPractical Accounting TwoFerdinand FernandoNo ratings yet

- Test 1-Theory (1 PT Each) - Write Only The Letter Which Corresponds To Your Chosen AnswerDocument3 pagesTest 1-Theory (1 PT Each) - Write Only The Letter Which Corresponds To Your Chosen AnswerJazel Mae CelerinosNo ratings yet

- Taxation Review Final Income TaxDocument4 pagesTaxation Review Final Income TaxGendyBocoNo ratings yet

- Fringe Benefits, de Minimis Benefits, Filing of Income Tax ReturnDocument5 pagesFringe Benefits, de Minimis Benefits, Filing of Income Tax ReturndgdeguzmanNo ratings yet

- Tax On Individuals QuizDocument6 pagesTax On Individuals QuizJomarNo ratings yet

- GT1 IncotaxDocument10 pagesGT1 IncotaxAndree PereaNo ratings yet

- Chapter8 TaxationonindividualsDocument12 pagesChapter8 TaxationonindividualsChristine Joy Rapi MarsoNo ratings yet

- Tax Pre TestDocument4 pagesTax Pre TestSebastian GarciaNo ratings yet

- 18 - Illustrative Examples (Multiple Choice - Solutions)Document10 pages18 - Illustrative Examples (Multiple Choice - Solutions)Allan SantosNo ratings yet

- Final Income TaxationDocument7 pagesFinal Income TaxationJimmyChaoNo ratings yet

- Income Tax Finals Sample Questions Final ExamDocument19 pagesIncome Tax Finals Sample Questions Final ExamAnie P. Martinez0% (1)

- Income Tax For IndividualsDocument11 pagesIncome Tax For IndividualsJoel Christian Mascariña100% (1)

- For The Month.: Answer: The Total Allowable Deduction From Business Income of Lucky Corporation Is 258,923Document2 pagesFor The Month.: Answer: The Total Allowable Deduction From Business Income of Lucky Corporation Is 258,923Aleksa FelicianoNo ratings yet

- TAXN 2000 SECOND TERM EXAM SY22 23 QuestionnaireDocument15 pagesTAXN 2000 SECOND TERM EXAM SY22 23 QuestionnaireGrace Love Yzyry LuNo ratings yet

- Incotax GT1 PDFDocument3 pagesIncotax GT1 PDFSoahNo ratings yet

- Module 2 - Topic 3 (Notes Receivable)Document7 pagesModule 2 - Topic 3 (Notes Receivable)GRACE ANN BERGONIONo ratings yet

- Basic Principles of TaxationDocument18 pagesBasic Principles of TaxationAlexandra Nicole IsaacNo ratings yet

- Prefinal Exam Phil TaxDocument4 pagesPrefinal Exam Phil TaxDarren GreNo ratings yet

- Interim 7 Consolidation AFAR1Document7 pagesInterim 7 Consolidation AFAR1Bea Tepace PototNo ratings yet

- Nasa Coursehero Exam NG FEUDocument9 pagesNasa Coursehero Exam NG FEUZedie Leigh VioletaNo ratings yet

- Module 5 Franchise Sales Assignments 2bac May 2023Document6 pagesModule 5 Franchise Sales Assignments 2bac May 2023Aaron OsmaNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Institute of Doctors Engineers and ScientistsDocument2 pagesInstitute of Doctors Engineers and ScientistsVINAY CHANDWANINo ratings yet

- Group 4 - Evolution of Taxation in The Philippines Estrada Arroyo PNOY and Duterte Administrations For Powerpoint VersionDocument3 pagesGroup 4 - Evolution of Taxation in The Philippines Estrada Arroyo PNOY and Duterte Administrations For Powerpoint VersionSairah Camille ArandiaNo ratings yet

- Thittayil Builders & Developers: Form GST Inv - 1Document2 pagesThittayil Builders & Developers: Form GST Inv - 1SujithNo ratings yet

- PP Requirements Dec 2011Document78 pagesPP Requirements Dec 2011Ab baNo ratings yet

- Departmental Interpretation and Practice Notes No. 24 (Revised)Document17 pagesDepartmental Interpretation and Practice Notes No. 24 (Revised)Difanny KooNo ratings yet

- Kangra Co-Operative BankDocument6 pagesKangra Co-Operative BankPallavi ThakurNo ratings yet

- Cespt Tijuana Online Payment TranslationDocument2 pagesCespt Tijuana Online Payment TranslationJessica DonahueNo ratings yet

- Iris - RuckusDocument1 pageIris - RuckusSwagBeast SKJJNo ratings yet

- G.R. No. 210836 Chevron Philippines Inc., Petitioner, Commissioner of Internal Revenue, RespondentDocument5 pagesG.R. No. 210836 Chevron Philippines Inc., Petitioner, Commissioner of Internal Revenue, Respondentavalavenia2abadNo ratings yet

- Amar Ujala Web Services PVT LTD: Tax InvoiceDocument1 pageAmar Ujala Web Services PVT LTD: Tax InvoiceShubhamNo ratings yet

- Flowchart Current (Replenishment of Petty Cash)Document2 pagesFlowchart Current (Replenishment of Petty Cash)April Rose Sobrevilla Dimpo100% (2)

- NotesDocument6 pagesNotesAsad MuhammadNo ratings yet

- LDNDocument2 pagesLDNShaharyar KhanNo ratings yet

- Lim Ban Long PayslipDocument3 pagesLim Ban Long PayslipDaniel GuanNo ratings yet

- LitecoinDocument4 pagesLitecoinReda El BdrNo ratings yet

- Master Domestic PDFDocument1 pageMaster Domestic PDFYudhis Panji HarmawanNo ratings yet

- New Home Broadband BrochureDocument1 pageNew Home Broadband BrochureVarun KanwarNo ratings yet

- Receipt Voucher: Jaipuria Institute of Management, LucknowDocument1 pageReceipt Voucher: Jaipuria Institute of Management, LucknowSanjeev Kumar Suman Student, Jaipuria LucknowNo ratings yet

- Customer Inquiry ReportDocument3 pagesCustomer Inquiry Reportharis_fikriNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument2 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceHunterNo ratings yet

- Journal Entries Module 1Document7 pagesJournal Entries Module 1Jervin Maon Velasco100% (1)

- Indiana Property Tax Benefits: (This Form Must Be Printed On Gold or Yellow Paper)Document2 pagesIndiana Property Tax Benefits: (This Form Must Be Printed On Gold or Yellow Paper)abramsdcNo ratings yet

- Goods & Services Tax (GST) - (One Nation One Tax)Document40 pagesGoods & Services Tax (GST) - (One Nation One Tax)sumukh0% (1)

- Apr 23Document1 pageApr 23Amit ShindeNo ratings yet

- Chapter 10 - With NotesDocument47 pagesChapter 10 - With NotesJackNo ratings yet

- Income Taxation Week 1Document19 pagesIncome Taxation Week 1Hannah Rae ChingNo ratings yet

Download as docx, pdf, or txt

You might also like

- Qaisar Naveed Bank Statement 1 YearDocument20 pagesQaisar Naveed Bank Statement 1 Yearisrargondal786123100% (1)

- TAXDocument10 pagesTAXJeana Segumalian100% (3)

- Tax Compliance Survey QuestionnaireDocument4 pagesTax Compliance Survey QuestionnaireJennelyn Abella76% (21)

- CPA Review Notes 2019 - FAR (Financial Accounting and Reporting)From EverandCPA Review Notes 2019 - FAR (Financial Accounting and Reporting)Rating: 3.5 out of 5 stars3.5/5 (17)

- Taxation First Preboard 93 - QuestionnaireDocument16 pagesTaxation First Preboard 93 - QuestionnaireAmeroden AbdullahNo ratings yet

- TAX-06-FRINGE-BENEFITS-TAX (With Answers) WITHOUT TYPODocument8 pagesTAX-06-FRINGE-BENEFITS-TAX (With Answers) WITHOUT TYPOKendrew Sujide100% (1)

- Individual Income TaxDocument13 pagesIndividual Income TaxDaniel Dialino100% (1)

- 4 2020 UP BOC Taxation Law Reviewer PDFDocument263 pages4 2020 UP BOC Taxation Law Reviewer PDFRose Ann Lascuña90% (10)

- Midterm Examination With SolutionDocument2 pagesMidterm Examination With SolutionSeulgi Bear100% (1)

- Fringe Benefit Part 3Document24 pagesFringe Benefit Part 3kitkathyNo ratings yet

- Fringe Benefits and Fringe Benefit Tax ExercisesDocument3 pagesFringe Benefits and Fringe Benefit Tax Exercisesaj lopezNo ratings yet

- Resources Understanding ISO20022 NACHA Payments 2013Document121 pagesResources Understanding ISO20022 NACHA Payments 2013Rajendra PilludaNo ratings yet

- Fringe Benefit TAX: Mr. Mario M. Castro, Cpa, Mba Tax ConsultantDocument19 pagesFringe Benefit TAX: Mr. Mario M. Castro, Cpa, Mba Tax ConsultantKristine Aubrey AlvarezNo ratings yet

- Fringe Benefits 1Document13 pagesFringe Benefits 1Jessa Mae ZamudioNo ratings yet

- Average Quiz Set ADocument5 pagesAverage Quiz Set AMarvin AndresNo ratings yet

- Tax - 2nd Monthly Assessment - QuestionsDocument12 pagesTax - 2nd Monthly Assessment - QuestionsGRACELYN SOJORNo ratings yet

- Midterm Exam Principles of Taxation and Income TaxationDocument6 pagesMidterm Exam Principles of Taxation and Income TaxationKitagawa, Misia Sophia Jan B.No ratings yet

- Inge BenefitsDocument7 pagesInge BenefitsKarleen RazonabeNo ratings yet

- AFAR 1 Exams 2020Document7 pagesAFAR 1 Exams 2020RJ Kristine DaqueNo ratings yet

- Fringe Benefit - QuizDocument3 pagesFringe Benefit - QuizArlea AsenciNo ratings yet

- Fringe Benefit - QuizDocument3 pagesFringe Benefit - QuizArlea AsenciNo ratings yet

- Yellow - Not Sure, Green - CorrectDocument7 pagesYellow - Not Sure, Green - CorrectIsaiah John Domenic M. CantaneroNo ratings yet

- 2nd Quizzer 1st Sem SY 2020-2021 - AKDocument6 pages2nd Quizzer 1st Sem SY 2020-2021 - AKMitzi WamarNo ratings yet

- Fringe Benefit TaxDocument4 pagesFringe Benefit TaxKenneth Bryan Tegerero Tegio100% (1)

- Tax 1st Preboard A LUDocument9 pagesTax 1st Preboard A LUAnonymous 7HGskNNo ratings yet

- TAXDocument20 pagesTAXkate trishaNo ratings yet

- Theories: B. 2 and 3 OnlyDocument5 pagesTheories: B. 2 and 3 OnlyLucille Mae EndigaNo ratings yet

- Ea - TaxDocument8 pagesEa - TaxKc SevillaNo ratings yet

- Tax Computations SampleDocument5 pagesTax Computations Samplelcsme tubodaccountsNo ratings yet

- Partnership Operations (Additional Sample Problems)Document5 pagesPartnership Operations (Additional Sample Problems)Pauline Anne LopezNo ratings yet

- Sample Problem Accounting Taxation 1Document4 pagesSample Problem Accounting Taxation 1carl patNo ratings yet

- Practical Accounting TwoDocument25 pagesPractical Accounting TwoJoseph SalidoNo ratings yet

- Income Taxation 1Document4 pagesIncome Taxation 1nicole bancoroNo ratings yet

- Instruction: Write The Letter of Your Choice On The Space Provided Before The NumberDocument4 pagesInstruction: Write The Letter of Your Choice On The Space Provided Before The NumberASDDD100% (2)

- FBT Sample ComputationsDocument3 pagesFBT Sample ComputationsLynn HermNo ratings yet

- Taxation Material 2Document7 pagesTaxation Material 2Shaira BugayongNo ratings yet

- Partnership OperationDocument3 pagesPartnership Operationbrmo.amatorio.uiNo ratings yet

- 8.6 Assignment - Regular Income Tax On CorporationsDocument3 pages8.6 Assignment - Regular Income Tax On CorporationsRoselyn LumbaoNo ratings yet

- Fat Deferred Income TaxDocument2 pagesFat Deferred Income Taxnicole bancoroNo ratings yet

- Practical Accounting TwoDocument48 pagesPractical Accounting TwoFerdinand FernandoNo ratings yet

- Test 1-Theory (1 PT Each) - Write Only The Letter Which Corresponds To Your Chosen AnswerDocument3 pagesTest 1-Theory (1 PT Each) - Write Only The Letter Which Corresponds To Your Chosen AnswerJazel Mae CelerinosNo ratings yet

- Taxation Review Final Income TaxDocument4 pagesTaxation Review Final Income TaxGendyBocoNo ratings yet

- Fringe Benefits, de Minimis Benefits, Filing of Income Tax ReturnDocument5 pagesFringe Benefits, de Minimis Benefits, Filing of Income Tax ReturndgdeguzmanNo ratings yet

- Tax On Individuals QuizDocument6 pagesTax On Individuals QuizJomarNo ratings yet

- GT1 IncotaxDocument10 pagesGT1 IncotaxAndree PereaNo ratings yet

- Chapter8 TaxationonindividualsDocument12 pagesChapter8 TaxationonindividualsChristine Joy Rapi MarsoNo ratings yet

- Tax Pre TestDocument4 pagesTax Pre TestSebastian GarciaNo ratings yet

- 18 - Illustrative Examples (Multiple Choice - Solutions)Document10 pages18 - Illustrative Examples (Multiple Choice - Solutions)Allan SantosNo ratings yet

- Final Income TaxationDocument7 pagesFinal Income TaxationJimmyChaoNo ratings yet

- Income Tax Finals Sample Questions Final ExamDocument19 pagesIncome Tax Finals Sample Questions Final ExamAnie P. Martinez0% (1)

- Income Tax For IndividualsDocument11 pagesIncome Tax For IndividualsJoel Christian Mascariña100% (1)

- For The Month.: Answer: The Total Allowable Deduction From Business Income of Lucky Corporation Is 258,923Document2 pagesFor The Month.: Answer: The Total Allowable Deduction From Business Income of Lucky Corporation Is 258,923Aleksa FelicianoNo ratings yet

- TAXN 2000 SECOND TERM EXAM SY22 23 QuestionnaireDocument15 pagesTAXN 2000 SECOND TERM EXAM SY22 23 QuestionnaireGrace Love Yzyry LuNo ratings yet

- Incotax GT1 PDFDocument3 pagesIncotax GT1 PDFSoahNo ratings yet

- Module 2 - Topic 3 (Notes Receivable)Document7 pagesModule 2 - Topic 3 (Notes Receivable)GRACE ANN BERGONIONo ratings yet

- Basic Principles of TaxationDocument18 pagesBasic Principles of TaxationAlexandra Nicole IsaacNo ratings yet

- Prefinal Exam Phil TaxDocument4 pagesPrefinal Exam Phil TaxDarren GreNo ratings yet

- Interim 7 Consolidation AFAR1Document7 pagesInterim 7 Consolidation AFAR1Bea Tepace PototNo ratings yet

- Nasa Coursehero Exam NG FEUDocument9 pagesNasa Coursehero Exam NG FEUZedie Leigh VioletaNo ratings yet

- Module 5 Franchise Sales Assignments 2bac May 2023Document6 pagesModule 5 Franchise Sales Assignments 2bac May 2023Aaron OsmaNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Institute of Doctors Engineers and ScientistsDocument2 pagesInstitute of Doctors Engineers and ScientistsVINAY CHANDWANINo ratings yet

- Group 4 - Evolution of Taxation in The Philippines Estrada Arroyo PNOY and Duterte Administrations For Powerpoint VersionDocument3 pagesGroup 4 - Evolution of Taxation in The Philippines Estrada Arroyo PNOY and Duterte Administrations For Powerpoint VersionSairah Camille ArandiaNo ratings yet

- Thittayil Builders & Developers: Form GST Inv - 1Document2 pagesThittayil Builders & Developers: Form GST Inv - 1SujithNo ratings yet

- PP Requirements Dec 2011Document78 pagesPP Requirements Dec 2011Ab baNo ratings yet

- Departmental Interpretation and Practice Notes No. 24 (Revised)Document17 pagesDepartmental Interpretation and Practice Notes No. 24 (Revised)Difanny KooNo ratings yet

- Kangra Co-Operative BankDocument6 pagesKangra Co-Operative BankPallavi ThakurNo ratings yet

- Cespt Tijuana Online Payment TranslationDocument2 pagesCespt Tijuana Online Payment TranslationJessica DonahueNo ratings yet

- Iris - RuckusDocument1 pageIris - RuckusSwagBeast SKJJNo ratings yet

- G.R. No. 210836 Chevron Philippines Inc., Petitioner, Commissioner of Internal Revenue, RespondentDocument5 pagesG.R. No. 210836 Chevron Philippines Inc., Petitioner, Commissioner of Internal Revenue, Respondentavalavenia2abadNo ratings yet

- Amar Ujala Web Services PVT LTD: Tax InvoiceDocument1 pageAmar Ujala Web Services PVT LTD: Tax InvoiceShubhamNo ratings yet

- Flowchart Current (Replenishment of Petty Cash)Document2 pagesFlowchart Current (Replenishment of Petty Cash)April Rose Sobrevilla Dimpo100% (2)

- NotesDocument6 pagesNotesAsad MuhammadNo ratings yet

- LDNDocument2 pagesLDNShaharyar KhanNo ratings yet

- Lim Ban Long PayslipDocument3 pagesLim Ban Long PayslipDaniel GuanNo ratings yet

- LitecoinDocument4 pagesLitecoinReda El BdrNo ratings yet

- Master Domestic PDFDocument1 pageMaster Domestic PDFYudhis Panji HarmawanNo ratings yet

- New Home Broadband BrochureDocument1 pageNew Home Broadband BrochureVarun KanwarNo ratings yet

- Receipt Voucher: Jaipuria Institute of Management, LucknowDocument1 pageReceipt Voucher: Jaipuria Institute of Management, LucknowSanjeev Kumar Suman Student, Jaipuria LucknowNo ratings yet

- Customer Inquiry ReportDocument3 pagesCustomer Inquiry Reportharis_fikriNo ratings yet

- Statement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocument2 pagesStatement of Account: Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceHunterNo ratings yet

- Journal Entries Module 1Document7 pagesJournal Entries Module 1Jervin Maon Velasco100% (1)

- Indiana Property Tax Benefits: (This Form Must Be Printed On Gold or Yellow Paper)Document2 pagesIndiana Property Tax Benefits: (This Form Must Be Printed On Gold or Yellow Paper)abramsdcNo ratings yet

- Goods & Services Tax (GST) - (One Nation One Tax)Document40 pagesGoods & Services Tax (GST) - (One Nation One Tax)sumukh0% (1)

- Apr 23Document1 pageApr 23Amit ShindeNo ratings yet

- Chapter 10 - With NotesDocument47 pagesChapter 10 - With NotesJackNo ratings yet

- Income Taxation Week 1Document19 pagesIncome Taxation Week 1Hannah Rae ChingNo ratings yet