Download as pdf or txt

You might also like

- FRRF-ICB Assignment 3-QP-2023.v1Document7 pagesFRRF-ICB Assignment 3-QP-2023.v1Audrey KhwinanaNo ratings yet

- SuccessFactors Employee Central Practice QuestionsDocument11 pagesSuccessFactors Employee Central Practice Questionsrekha89757% (7)

- For Hino: Tics Pump Electrical Part Resistance Value ListDocument35 pagesFor Hino: Tics Pump Electrical Part Resistance Value Listfersky90% (10)

- Finance Act 2020 - ACCA GlobalDocument62 pagesFinance Act 2020 - ACCA GlobalhfdghdhNo ratings yet

- Chargeable Lifetime Transfers - Calculation of Tax: Basic PrinciplesDocument8 pagesChargeable Lifetime Transfers - Calculation of Tax: Basic PrinciplesAlellie Khay JordanNo ratings yet

- Finance Act 2020 - ACCA GlobalDocument65 pagesFinance Act 2020 - ACCA GlobalRaza AliNo ratings yet

- Finance Act 2021 - ACCA GlobalDocument56 pagesFinance Act 2021 - ACCA GlobalhfdghdhNo ratings yet

- Assignment 3 1Document6 pagesAssignment 3 1Siying GuNo ratings yet

- Advanced Accounting 763554577Document151 pagesAdvanced Accounting 763554577premium info2222No ratings yet

- CGT 1Document25 pagesCGT 1Donald HollistNo ratings yet

- Income Tax Calculation Worksheet: Ellucian Higher Education Systems India Private Limited Ascent PayrollDocument2 pagesIncome Tax Calculation Worksheet: Ellucian Higher Education Systems India Private Limited Ascent PayrollShiva098No ratings yet

- Notice of Assessment 2021 03 22 15 36 05 837221Document4 pagesNotice of Assessment 2021 03 22 15 36 05 837221Joseph HudsonNo ratings yet

- CMPC 131 AnswerDocument5 pagesCMPC 131 AnswerKharen ValdezNo ratings yet

- f6 ANSDocument14 pagesf6 ANSSarad KharelNo ratings yet

- CBSE Class 12 Accountancy Accounting For Not For Profit Organisation WorksheetDocument6 pagesCBSE Class 12 Accountancy Accounting For Not For Profit Organisation WorksheetJas Singh DevganNo ratings yet

- Speaker Kotek Business Tax ProposalDocument11 pagesSpeaker Kotek Business Tax ProposalMatthew KishNo ratings yet

- Solution Adv. Accounting Test-2 CH-3Document13 pagesSolution Adv. Accounting Test-2 CH-3NITIN JAINNo ratings yet

- Bafacr4X Non-Financial Liabilities: Problem 4.1Document7 pagesBafacr4X Non-Financial Liabilities: Problem 4.1Aga Mathew MayugaNo ratings yet

- Atxuk Sample Marjun 2019 ADocument10 pagesAtxuk Sample Marjun 2019 AAdam KhanNo ratings yet

- Annual Results PresentationDocument25 pagesAnnual Results PresentationManik VermaNo ratings yet

- Soln PT2 Acc XII (Session 2023-24)Document14 pagesSoln PT2 Acc XII (Session 2023-24)Vaidehi BagraNo ratings yet

- Solutions To Exercises P Class2-2022Document7 pagesSolutions To Exercises P Class2-2022Angel MéndezNo ratings yet

- Basics LTD - MemoDocument3 pagesBasics LTD - Memoewriteandread.businessNo ratings yet

- Tax Rates 2019/20: Precise. Proven. PerformanceDocument4 pagesTax Rates 2019/20: Precise. Proven. PerformanceIssa BoyNo ratings yet

- (CBCS) Commerce Paper: 4.5 A - Innovations in Accounting: Note: Answer As Per Internal ChoiceDocument4 pages(CBCS) Commerce Paper: 4.5 A - Innovations in Accounting: Note: Answer As Per Internal ChoiceSanaullah M SultanpurNo ratings yet

- LFPE5800 November 2018 MEMODocument37 pagesLFPE5800 November 2018 MEMOSibongiseniNo ratings yet

- Notice of Reassessment 2021 05 31 09 31 59 847068Document4 pagesNotice of Reassessment 2021 05 31 09 31 59 847068api-676582318No ratings yet

- Inheritance Tax, Part 1Document22 pagesInheritance Tax, Part 1hfdghdhNo ratings yet

- Thq002-Inst. Sales PDFDocument2 pagesThq002-Inst. Sales PDFAndrea AtendidoNo ratings yet

- Notice of Assessment 2020 04 09 13 13 51 21033Document4 pagesNotice of Assessment 2020 04 09 13 13 51 21033Burning LightNo ratings yet

- 2-Budget Preparation UpdatedJDADocument81 pages2-Budget Preparation UpdatedJDAJamy Vab MontesNo ratings yet

- 92 08 DeductionsDocument18 pages92 08 DeductionsNikkoNo ratings yet

- Financial Reporting Paper 2.1Document26 pagesFinancial Reporting Paper 2.1Gen AbulkhairNo ratings yet

- Question Number 1: REP LimitedDocument10 pagesQuestion Number 1: REP LimitedJalees Ul HassanNo ratings yet

- Model Solution: Page 1 of 6Document6 pagesModel Solution: Page 1 of 6ShuvonathNo ratings yet

- Remote Desktop Redirected PrinterDocument1 pageRemote Desktop Redirected Printeramit chavariaNo ratings yet

- Amended Tax Credit Certificate 2022: 9371000KA Pps NoDocument2 pagesAmended Tax Credit Certificate 2022: 9371000KA Pps NoJose ArevaloNo ratings yet

- Sem-1 14 BCOM GENERAL CC-1.1CG FINANCIAL-ACCOUNTING-I-1348 PDFDocument11 pagesSem-1 14 BCOM GENERAL CC-1.1CG FINANCIAL-ACCOUNTING-I-1348 PDFJude VascoNo ratings yet

- Ru Advanced Accounting ExerciseDocument1 pageRu Advanced Accounting Exerciseprince matamboNo ratings yet

- Set 3Document14 pagesSet 3Prakshi KansalNo ratings yet

- LCCI Level 4 Certificate in Financial Accounting VQR Resource Booklet ASE20101 April 2019Document12 pagesLCCI Level 4 Certificate in Financial Accounting VQR Resource Booklet ASE20101 April 2019Musthari KhanNo ratings yet

- 2nd Quizzer 1st Sem SY 2020-2021 - AKDocument6 pages2nd Quizzer 1st Sem SY 2020-2021 - AKMitzi WamarNo ratings yet

- Tugas Pertemuan 11Document4 pagesTugas Pertemuan 11Hana NadhifaNo ratings yet

- Warranty Liability Empleo Robles SolManDocument2 pagesWarranty Liability Empleo Robles SolManJohanna Raissa CapadaNo ratings yet

- ACCOUNTANCY SOLUTION PROJECT On FSDocument15 pagesACCOUNTANCY SOLUTION PROJECT On FSRiyasat khanNo ratings yet

- Q3.2 Boampong. Shortworkings Rec. & Edem AccountDocument2 pagesQ3.2 Boampong. Shortworkings Rec. & Edem AccountPrince AntwiNo ratings yet

- DeanDocument16 pagesDeanJames De TorresNo ratings yet

- HeheDocument8 pagesHeheCunanan, Malakhai JeuNo ratings yet

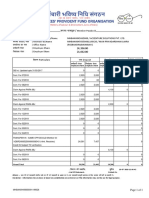

- PF FormDocument1 pagePF FormLalit SharmaNo ratings yet

- MPACC512 Advanced Fin Reporting Answer Bank 2022Document44 pagesMPACC512 Advanced Fin Reporting Answer Bank 2022Tawanda Tatenda HerbertNo ratings yet

- FAR - March-April-2021Document8 pagesFAR - March-April-2021Towhidul IslamNo ratings yet

- Esd #2Document10 pagesEsd #2FarzanNo ratings yet

- TAX PLANNING & COMPLIANCE - ND-2022 - Suggested - AnswersDocument9 pagesTAX PLANNING & COMPLIANCE - ND-2022 - Suggested - AnswersMohammad FaridNo ratings yet

- Paper - 4: Taxation Section A: Income Tax Law: © The Institute of Chartered Accountants of IndiaDocument27 pagesPaper - 4: Taxation Section A: Income Tax Law: © The Institute of Chartered Accountants of IndiaHarineNo ratings yet

- Govtdomdebt Oct2019Document7 pagesGovtdomdebt Oct2019shamma.aminNo ratings yet

- Adobe Scan 20-Apr-2024Document3 pagesAdobe Scan 20-Apr-2024kanishkaaryan96No ratings yet

- MPAC523 WIP A 2020Document8 pagesMPAC523 WIP A 2020Tawanda Tatenda HerbertNo ratings yet

- Midterm Problem - DocmDocument2 pagesMidterm Problem - Docmpippen venegasNo ratings yet

- Question 7 - Financial-Reporting-Nov-2020 - Kingdom & Paradise-Question 1Document6 pagesQuestion 7 - Financial-Reporting-Nov-2020 - Kingdom & Paradise-Question 1Laud ListowellNo ratings yet

- 2020 DT Notes RevisionDocument7 pages2020 DT Notes RevisionTsekeNo ratings yet

- TDS & TCSDocument11 pagesTDS & TCSKartikNo ratings yet

- A Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionFrom EverandA Comparative Analysis of Tax Administration in Asia and the Pacific: Fifth EditionNo ratings yet

- Taxable ValueDocument1 pageTaxable ValuehfdghdhNo ratings yet

- Scope of ChargeDocument1 pageScope of ChargehfdghdhNo ratings yet

- Claim For Personal Reliefs Under Joint Assessment: Example 5Document1 pageClaim For Personal Reliefs Under Joint Assessment: Example 5hfdghdhNo ratings yet

- Tax Rates: Key Features Sales Tax Service TaxDocument1 pageTax Rates: Key Features Sales Tax Service TaxhfdghdhNo ratings yet

- There Is No Such Thing As 'SST'Document1 pageThere Is No Such Thing As 'SST'hfdghdhNo ratings yet

- Related Links: Taxable PeriodDocument1 pageRelated Links: Taxable PeriodhfdghdhNo ratings yet

- Joint and Separate Assessment: MenuDocument11 pagesJoint and Separate Assessment: MenuhfdghdhNo ratings yet

- Entitlement To Tax Rebates Under Joint Assessment: Example 10Document1 pageEntitlement To Tax Rebates Under Joint Assessment: Example 10hfdghdhNo ratings yet

- Conditions For Electing For Joint Assessment: Example 2Document1 pageConditions For Electing For Joint Assessment: Example 2hfdghdhNo ratings yet

- Tax Implications of Financial Arrangements For Motor Vehicles - ACCA GlobalDocument8 pagesTax Implications of Financial Arrangements For Motor Vehicles - ACCA GlobalhfdghdhNo ratings yet

- Cash Donations To City Council (DBKL) 1,500: Example 6Document1 pageCash Donations To City Council (DBKL) 1,500: Example 6hfdghdhNo ratings yet

- Option 1: Purchase OutrightDocument1 pageOption 1: Purchase OutrighthfdghdhNo ratings yet

- The Pitfalls of Interest Deduction Claims by Corporate Taxpayers - ACCA GlobalDocument9 pagesThe Pitfalls of Interest Deduction Claims by Corporate Taxpayers - ACCA GlobalhfdghdhNo ratings yet

- The Pitfalls of Interest Deduction Claims by Individual Taxpayers - ACCA Qualification - Students - ACCA GlobalDocument12 pagesThe Pitfalls of Interest Deduction Claims by Individual Taxpayers - ACCA Qualification - Students - ACCA GlobalhfdghdhNo ratings yet

- 03-15-2016 ECF 305 USA V JON RITZHEIMER - Response To Motion by USA As To Jon Ritzheimer Re Motion For Release From CustodyDocument12 pages03-15-2016 ECF 305 USA V JON RITZHEIMER - Response To Motion by USA As To Jon Ritzheimer Re Motion For Release From CustodyJack RyanNo ratings yet

- CURVESDocument30 pagesCURVESPHULARAM PEGUNo ratings yet

- Guasch-Espasa Brill 2015 PDFDocument21 pagesGuasch-Espasa Brill 2015 PDFERIKA VIVIANA MOLINA BALAGUERANo ratings yet

- Daughtrey v. Fresno City Police Department, Et Al. - Document No. 4Document1 pageDaughtrey v. Fresno City Police Department, Et Al. - Document No. 4Justia.comNo ratings yet

- Modification and Characterization of PolypropyleneDocument7 pagesModification and Characterization of PolypropyleneSaba MalikNo ratings yet

- Lab ManualDocument14 pagesLab Manualhak creationNo ratings yet

- A VFP-SQL Server Application From The BeginingDocument38 pagesA VFP-SQL Server Application From The Beginingmohsin.computers3076No ratings yet

- Lesson 10Document19 pagesLesson 10AnilNo ratings yet

- 2009-11-05Document20 pages2009-11-05The University Daily KansanNo ratings yet

- IP Rating ChartDocument5 pagesIP Rating Charthemant kumarNo ratings yet

- Saidu Teaching Hospital / Saidu Medical College, Saidu Sharif SwatDocument5 pagesSaidu Teaching Hospital / Saidu Medical College, Saidu Sharif SwatZeeshan KhanNo ratings yet

- Mitsubishi 3000gt 1997 Wiring DiagramsDocument58 pagesMitsubishi 3000gt 1997 Wiring DiagramsThanh LiemNo ratings yet

- Kalimat Simple Present Tense Aktif Kalimat Simple Past Tense AktifDocument2 pagesKalimat Simple Present Tense Aktif Kalimat Simple Past Tense AktifRestu PamujiNo ratings yet

- Cs607 Midterm Solved Mcqs by JunaidDocument49 pagesCs607 Midterm Solved Mcqs by JunaidZainab Tatheer100% (1)

- PS: Patient Safety and Risk ManagementDocument5 pagesPS: Patient Safety and Risk Managementnoor88No ratings yet

- Weather ChangesDocument34 pagesWeather ChangesEmina PodicNo ratings yet

- 1672298032245-ICE CE-29 - RevisionDocument86 pages1672298032245-ICE CE-29 - RevisionSoumyaranjan NayakNo ratings yet

- TOT Water For Pharmaceutical Use - Part 1Document132 pagesTOT Water For Pharmaceutical Use - Part 1Delly AnakAfternoonyesterdays0% (1)

- Reviewer in Pa 108Document14 pagesReviewer in Pa 108Madelyn OrfinadaNo ratings yet

- Application Form AWKUM-NewDocument6 pagesApplication Form AWKUM-Newfazal ghaniNo ratings yet

- ISO 2597-2 - 2019 - Iron Ores Determination of Total Iron Content - Part 2 Titrimetric Methods After Titanium (III) Chloride ReductionDocument20 pagesISO 2597-2 - 2019 - Iron Ores Determination of Total Iron Content - Part 2 Titrimetric Methods After Titanium (III) Chloride ReductionMetal deptNo ratings yet

- Physics Education Thesis TopicsDocument4 pagesPhysics Education Thesis TopicsPaperWriterServicesCanada100% (2)

- Purpose - Device - Ravana - OSHODocument2 pagesPurpose - Device - Ravana - OSHOChitter SinghNo ratings yet

- CCBoot Manual - Server SettingsDocument89 pagesCCBoot Manual - Server SettingsHasnan IbrahimNo ratings yet

- BIO Genetics Eukaryote TranscriptionDocument23 pagesBIO Genetics Eukaryote TranscriptionAnonymous SVy8sOsvJDNo ratings yet

- Passive VoiceDocument2 pagesPassive Voicenguyen hong phuong63% (19)

- Oodp Project 1Document14 pagesOodp Project 1dikshaNo ratings yet

- Effects of Handling On Animals Welfare During TranDocument54 pagesEffects of Handling On Animals Welfare During TranNikhilesh WaniNo ratings yet