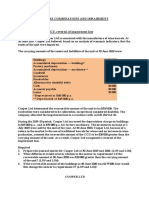

Issue of Share

Issue of Share

You might also like

- NDocument2 pagesNFreya EvangelineNo ratings yet

- Faculty of Business Management Fundamental of Finance (Fin 242)Document16 pagesFaculty of Business Management Fundamental of Finance (Fin 242)atiqah67% (3)

- CEL 1 TOA Answer Key 1Document12 pagesCEL 1 TOA Answer Key 1Joel Matthew MozarNo ratings yet

- NCERT Solutions For Class 12 Commerce Accountancy Chapter 1 - Accounting For Share CapitalDocument3 pagesNCERT Solutions For Class 12 Commerce Accountancy Chapter 1 - Accounting For Share CapitalDhanishtaNo ratings yet

- In The Books of A & B Co. LTD.: Journal Entries Date Sr. No. Particulars L.FDocument2 pagesIn The Books of A & B Co. LTD.: Journal Entries Date Sr. No. Particulars L.FIsha KatiyarNo ratings yet

- Corporate Accounting NotesDocument78 pagesCorporate Accounting NotesdivyanshuNo ratings yet

- Solution Ultimate Sample Paper 2Document7 pagesSolution Ultimate Sample Paper 2Nitin KumarNo ratings yet

- HA2032Document12 pagesHA2032Aayam SubediNo ratings yet

- Corporate AccountingDocument79 pagesCorporate Accountingakshrajput2005No ratings yet

- 637617309804853146SM Session10Document3 pages637617309804853146SM Session10kreshmith2No ratings yet

- Caa Assignment SolutionsDocument39 pagesCaa Assignment Solutionschikanesakshi2001No ratings yet

- C.S. Executive - Answers For CC Test Paper - IDocument7 pagesC.S. Executive - Answers For CC Test Paper - Isekhar_gantiNo ratings yet

- Recapulitation: Collaborating TechniqueDocument6 pagesRecapulitation: Collaborating TechniqueayeshaNo ratings yet

- Hsslive Xii Acc 3 Admission of A Partner KeyDocument8 pagesHsslive Xii Acc 3 Admission of A Partner KeyShinu ShinadNo ratings yet

- Issue of Share 2018Document2 pagesIssue of Share 2018Arpan CHATTERJEENo ratings yet

- Practical Guide To Issue, Forfeiture and Reissue of Shares: Topic I: Full SubscriptionDocument24 pagesPractical Guide To Issue, Forfeiture and Reissue of Shares: Topic I: Full SubscriptionGANDHI DHRUVINNo ratings yet

- Internal Reconstruction PQ SolDocument17 pagesInternal Reconstruction PQ SolKaran MokhaNo ratings yet

- Bv2018 Revised Conceptual FrameworkDocument18 pagesBv2018 Revised Conceptual FrameworkTeneswari RadhaNo ratings yet

- Answer Key - 1 TermDocument9 pagesAnswer Key - 1 TermsamayaksahuNo ratings yet

- E - Book - Dissolution of A Partnership Firm (Questions With Solutions) - Accountancy - Class 12th - Itika Ma'am - SohelDocument41 pagesE - Book - Dissolution of A Partnership Firm (Questions With Solutions) - Accountancy - Class 12th - Itika Ma'am - Sohelitika.chaudharyNo ratings yet

- Additional Illustrations 8Document16 pagesAdditional Illustrations 8Thulsi JayadevNo ratings yet

- Shares Issued at Premium & DiscountDocument13 pagesShares Issued at Premium & DiscountAwab HamidNo ratings yet

- Financial Accounting AssignentDocument8 pagesFinancial Accounting AssignentHitesh LodayaNo ratings yet

- CBSE Accountancy 12th Term 2 CH 3Document5 pagesCBSE Accountancy 12th Term 2 CH 3AadasNo ratings yet

- Marking Scheme: PRE - BOARD-2 (2023 - 2024)Document11 pagesMarking Scheme: PRE - BOARD-2 (2023 - 2024)Kaustav DasNo ratings yet

- Journal Entries Date Particulars L.F. Debit Amount Rs Credit Amount RsDocument2 pagesJournal Entries Date Particulars L.F. Debit Amount Rs Credit Amount RsRadhey EnterprisesNo ratings yet

- Business Combination Answers (Manav)Document58 pagesBusiness Combination Answers (Manav)Harshit ChauhanNo ratings yet

- Corporate AccountingDocument25 pagesCorporate Accountingrakshithaparimala100No ratings yet

- Pe2 Acc Nov05Document19 pagesPe2 Acc Nov05api-3825774No ratings yet

- Conversion or Sale of Partnership Firm Into Limited CompanyDocument24 pagesConversion or Sale of Partnership Firm Into Limited CompanyMadhav TailorNo ratings yet

- XII ACCOUNTANCY SET-2 Marking Scheme Ist Pre Board 2023-24-1Document9 pagesXII ACCOUNTANCY SET-2 Marking Scheme Ist Pre Board 2023-24-1Riddhima Murarka50% (2)

- Calls in AdvanceDocument14 pagesCalls in AdvanceShruti GoswamiNo ratings yet

- Class Work Chp. 8Document13 pagesClass Work Chp. 8Isha KatiyarNo ratings yet

- 70584bos010622 Foundation P1aDocument10 pages70584bos010622 Foundation P1aAdityaNo ratings yet

- Recapulitation: Collaborating TechniqueDocument5 pagesRecapulitation: Collaborating TechniqueayeshaNo ratings yet

- Cbse cl12 Ead Accountancy Answers To Sample Paper 6Document15 pagesCbse cl12 Ead Accountancy Answers To Sample Paper 6amaankhan828768No ratings yet

- Bhaskar AssignmentDocument2 pagesBhaskar Assignment2009silmshady6709No ratings yet

- Accounting For Share Capital (9 Questions - 3 Solved and 6 Unsolved)Document5 pagesAccounting For Share Capital (9 Questions - 3 Solved and 6 Unsolved)yuvraj gosain100% (2)

- Double Entry Book Keeping Ts Grewal Vol. I 2019 For Class 12 Commerce Accountancy Chapter 5 - Admission of A PartnerDocument1 pageDouble Entry Book Keeping Ts Grewal Vol. I 2019 For Class 12 Commerce Accountancy Chapter 5 - Admission of A PartnerTishaNo ratings yet

- Double Entry Book Keeping Ts Grewal Vol. I 2019 For Class 12 Commerce Accountancy Chapter 5 - Admission of A Partner 2Document1 pageDouble Entry Book Keeping Ts Grewal Vol. I 2019 For Class 12 Commerce Accountancy Chapter 5 - Admission of A Partner 2TishaNo ratings yet

- Suspense AccountsDocument5 pagesSuspense Accountsr233684qNo ratings yet

- CA Foundation Accounting SolutionsDocument117 pagesCA Foundation Accounting SolutionsAkash AjayNo ratings yet

- Solution For SharesDocument10 pagesSolution For SharesMohammad Tariq AnsariNo ratings yet

- Recapulitation: Collaborating TechniqueDocument3 pagesRecapulitation: Collaborating TechniqueayeshaNo ratings yet

- P18Document23 pagesP18aleeshaNo ratings yet

- Lecture 11-Forfeiture of SharesDocument12 pagesLecture 11-Forfeiture of SharesAwab HamidNo ratings yet

- Aidcom Financial Accounting AnalysisDocument17 pagesAidcom Financial Accounting AnalysisAjmal K HussainNo ratings yet

- RKG Class 11 Accounts Mock 1 SolDocument14 pagesRKG Class 11 Accounts Mock 1 SolSangket MukherjeeNo ratings yet

- Class Work Chp. 8Document12 pagesClass Work Chp. 8Isha KatiyarNo ratings yet

- TYBAF UnderwritingDocument49 pagesTYBAF UnderwritingJaimin VasaniNo ratings yet

- CA Inter Accounts A MTP 1 Nov 2022Document13 pagesCA Inter Accounts A MTP 1 Nov 2022smartshivenduNo ratings yet

- 104 ReviewDocument4 pages104 ReviewalanNo ratings yet

- Introduction To Financial Accounting: Suggested Answers Foundation Examinations - Spring 2011Document5 pagesIntroduction To Financial Accounting: Suggested Answers Foundation Examinations - Spring 2011adnanNo ratings yet

- Ts Grewal Class 12 Accountancy Chapter 7 PDFDocument11 pagesTs Grewal Class 12 Accountancy Chapter 7 PDFmonikaNo ratings yet

- 12 Accountancy Notes CH07 Company Accounts Issue of Shares 01Document20 pages12 Accountancy Notes CH07 Company Accounts Issue of Shares 01zainab.xf77No ratings yet

- CFN 9305 Accounts Suggested Answers PDFDocument4 pagesCFN 9305 Accounts Suggested Answers PDFDivya PunjabiNo ratings yet

- Corporation Part 1Document9 pagesCorporation Part 11701791No ratings yet

- Class Work Journal EntryDocument16 pagesClass Work Journal EntryRishabh ChawlaNo ratings yet

- QUESTION PAPER 36195 (Solution)Document17 pagesQUESTION PAPER 36195 (Solution)Faizu KhamNo ratings yet

- Sample Paper-1 (Target Term - 2) Answers: Book Recommended - Ultimate Book of Accountancy Class 12Document8 pagesSample Paper-1 (Target Term - 2) Answers: Book Recommended - Ultimate Book of Accountancy Class 12Beena ShibuNo ratings yet

- Mgt402 Assigenment Result Fall2009Document5 pagesMgt402 Assigenment Result Fall2009maqsoom471No ratings yet

- Getting a Job in Hedge Funds: An Inside Look at How Funds HireFrom EverandGetting a Job in Hedge Funds: An Inside Look at How Funds HireRating: 2 out of 5 stars2/5 (1)

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Solutions 2021 MockExamDocument15 pagesSolutions 2021 MockExamdayeyoutai779No ratings yet

- Accounting Problem Book 2011 PDFDocument103 pagesAccounting Problem Book 2011 PDFViệt Đức Lê67% (3)

- Accounting 1 - Module 4Document12 pagesAccounting 1 - Module 4LuisitoNo ratings yet

- Teknosa 4 QengDocument15 pagesTeknosa 4 QengFaIIen0nENo ratings yet

- AST Chapter 3 MCPDocument20 pagesAST Chapter 3 MCPElleNo ratings yet

- Anatomi Kepala Dan Wajah: by FadhilDocument8 pagesAnatomi Kepala Dan Wajah: by FadhilFadhilNo ratings yet

- Sessions 8 - 9 - BS - SentDocument11 pagesSessions 8 - 9 - BS - SentAjay DesaleNo ratings yet

- Chapter 04 - (The Accounting Cycle. Accruals and Deferrals)Document41 pagesChapter 04 - (The Accounting Cycle. Accruals and Deferrals)Hafiz SherazNo ratings yet

- 74607bos60479 FND cp2 U2Document111 pages74607bos60479 FND cp2 U2adityatiwari122006No ratings yet

- Asynchronous Statement of Financial Position XYZ CompanyDocument5 pagesAsynchronous Statement of Financial Position XYZ CompanyDiana Fernandez MagnoNo ratings yet

- Samsung C&T AuditDocument104 pagesSamsung C&T AuditkevalNo ratings yet

- Preparing Financial StatementsDocument6 pagesPreparing Financial StatementsAUDITOR97No ratings yet

- Principles of Consolidated Financial StatementsDocument13 pagesPrinciples of Consolidated Financial StatementsADEYANJU AKEEM100% (1)

- Template Annual ReportDocument8 pagesTemplate Annual ReportMas Hamzah FansuriNo ratings yet

- Chapter 11 - Depreciation and DepletionDocument46 pagesChapter 11 - Depreciation and DepletionDawn Rei DangkiwNo ratings yet

- Bookkeeping and Payroll Accounting - Module 3Document8 pagesBookkeeping and Payroll Accounting - Module 3LuisitoNo ratings yet

- Salce Prelim Act102 E2Document8 pagesSalce Prelim Act102 E2Joshua P. SalceNo ratings yet

- UNIT-4 - Income-From-BusinessDocument114 pagesUNIT-4 - Income-From-BusinessGuinevereNo ratings yet

- Practical ExerciseDocument9 pagesPractical Exercisesharini subramaniamNo ratings yet

- Accounting For InventoriesDocument9 pagesAccounting For InventoriesPrince AngelNo ratings yet

- Chapter 10Document5 pagesChapter 10Xynith Nicole RamosNo ratings yet

- Accounting For Branches and Combined FSDocument112 pagesAccounting For Branches and Combined FSMuhammad Fahad100% (2)

- U4A5 PracExerciseDocument7 pagesU4A5 PracExerciseDrippy SnowflakeNo ratings yet

- Practice 8: Business Combinations and Impairment Exercise 7.12 Impairment Loss For A CGU, Reversal of Impairment LossDocument7 pagesPractice 8: Business Combinations and Impairment Exercise 7.12 Impairment Loss For A CGU, Reversal of Impairment LossJingwen YangNo ratings yet

- Sip Project of HDFC Bank Financial Statement Analysis.1 (1) @...Document62 pagesSip Project of HDFC Bank Financial Statement Analysis.1 (1) @...Rajendra KhaireNo ratings yet

- Sme Discussion TemplateDocument5 pagesSme Discussion TemplateLeahmae OlimbaNo ratings yet

- Analysis of Financial StatementsDocument16 pagesAnalysis of Financial StatementsAlok ThakurNo ratings yet

Download as pdf or txt

You might also like

- NDocument2 pagesNFreya EvangelineNo ratings yet

- Faculty of Business Management Fundamental of Finance (Fin 242)Document16 pagesFaculty of Business Management Fundamental of Finance (Fin 242)atiqah67% (3)

- CEL 1 TOA Answer Key 1Document12 pagesCEL 1 TOA Answer Key 1Joel Matthew MozarNo ratings yet

- NCERT Solutions For Class 12 Commerce Accountancy Chapter 1 - Accounting For Share CapitalDocument3 pagesNCERT Solutions For Class 12 Commerce Accountancy Chapter 1 - Accounting For Share CapitalDhanishtaNo ratings yet

- In The Books of A & B Co. LTD.: Journal Entries Date Sr. No. Particulars L.FDocument2 pagesIn The Books of A & B Co. LTD.: Journal Entries Date Sr. No. Particulars L.FIsha KatiyarNo ratings yet

- Corporate Accounting NotesDocument78 pagesCorporate Accounting NotesdivyanshuNo ratings yet

- Solution Ultimate Sample Paper 2Document7 pagesSolution Ultimate Sample Paper 2Nitin KumarNo ratings yet

- HA2032Document12 pagesHA2032Aayam SubediNo ratings yet

- Corporate AccountingDocument79 pagesCorporate Accountingakshrajput2005No ratings yet

- 637617309804853146SM Session10Document3 pages637617309804853146SM Session10kreshmith2No ratings yet

- Caa Assignment SolutionsDocument39 pagesCaa Assignment Solutionschikanesakshi2001No ratings yet

- C.S. Executive - Answers For CC Test Paper - IDocument7 pagesC.S. Executive - Answers For CC Test Paper - Isekhar_gantiNo ratings yet

- Recapulitation: Collaborating TechniqueDocument6 pagesRecapulitation: Collaborating TechniqueayeshaNo ratings yet

- Hsslive Xii Acc 3 Admission of A Partner KeyDocument8 pagesHsslive Xii Acc 3 Admission of A Partner KeyShinu ShinadNo ratings yet

- Issue of Share 2018Document2 pagesIssue of Share 2018Arpan CHATTERJEENo ratings yet

- Practical Guide To Issue, Forfeiture and Reissue of Shares: Topic I: Full SubscriptionDocument24 pagesPractical Guide To Issue, Forfeiture and Reissue of Shares: Topic I: Full SubscriptionGANDHI DHRUVINNo ratings yet

- Internal Reconstruction PQ SolDocument17 pagesInternal Reconstruction PQ SolKaran MokhaNo ratings yet

- Bv2018 Revised Conceptual FrameworkDocument18 pagesBv2018 Revised Conceptual FrameworkTeneswari RadhaNo ratings yet

- Answer Key - 1 TermDocument9 pagesAnswer Key - 1 TermsamayaksahuNo ratings yet

- E - Book - Dissolution of A Partnership Firm (Questions With Solutions) - Accountancy - Class 12th - Itika Ma'am - SohelDocument41 pagesE - Book - Dissolution of A Partnership Firm (Questions With Solutions) - Accountancy - Class 12th - Itika Ma'am - Sohelitika.chaudharyNo ratings yet

- Additional Illustrations 8Document16 pagesAdditional Illustrations 8Thulsi JayadevNo ratings yet

- Shares Issued at Premium & DiscountDocument13 pagesShares Issued at Premium & DiscountAwab HamidNo ratings yet

- Financial Accounting AssignentDocument8 pagesFinancial Accounting AssignentHitesh LodayaNo ratings yet

- CBSE Accountancy 12th Term 2 CH 3Document5 pagesCBSE Accountancy 12th Term 2 CH 3AadasNo ratings yet

- Marking Scheme: PRE - BOARD-2 (2023 - 2024)Document11 pagesMarking Scheme: PRE - BOARD-2 (2023 - 2024)Kaustav DasNo ratings yet

- Journal Entries Date Particulars L.F. Debit Amount Rs Credit Amount RsDocument2 pagesJournal Entries Date Particulars L.F. Debit Amount Rs Credit Amount RsRadhey EnterprisesNo ratings yet

- Business Combination Answers (Manav)Document58 pagesBusiness Combination Answers (Manav)Harshit ChauhanNo ratings yet

- Corporate AccountingDocument25 pagesCorporate Accountingrakshithaparimala100No ratings yet

- Pe2 Acc Nov05Document19 pagesPe2 Acc Nov05api-3825774No ratings yet

- Conversion or Sale of Partnership Firm Into Limited CompanyDocument24 pagesConversion or Sale of Partnership Firm Into Limited CompanyMadhav TailorNo ratings yet

- XII ACCOUNTANCY SET-2 Marking Scheme Ist Pre Board 2023-24-1Document9 pagesXII ACCOUNTANCY SET-2 Marking Scheme Ist Pre Board 2023-24-1Riddhima Murarka50% (2)

- Calls in AdvanceDocument14 pagesCalls in AdvanceShruti GoswamiNo ratings yet

- Class Work Chp. 8Document13 pagesClass Work Chp. 8Isha KatiyarNo ratings yet

- 70584bos010622 Foundation P1aDocument10 pages70584bos010622 Foundation P1aAdityaNo ratings yet

- Recapulitation: Collaborating TechniqueDocument5 pagesRecapulitation: Collaborating TechniqueayeshaNo ratings yet

- Cbse cl12 Ead Accountancy Answers To Sample Paper 6Document15 pagesCbse cl12 Ead Accountancy Answers To Sample Paper 6amaankhan828768No ratings yet

- Bhaskar AssignmentDocument2 pagesBhaskar Assignment2009silmshady6709No ratings yet

- Accounting For Share Capital (9 Questions - 3 Solved and 6 Unsolved)Document5 pagesAccounting For Share Capital (9 Questions - 3 Solved and 6 Unsolved)yuvraj gosain100% (2)

- Double Entry Book Keeping Ts Grewal Vol. I 2019 For Class 12 Commerce Accountancy Chapter 5 - Admission of A PartnerDocument1 pageDouble Entry Book Keeping Ts Grewal Vol. I 2019 For Class 12 Commerce Accountancy Chapter 5 - Admission of A PartnerTishaNo ratings yet

- Double Entry Book Keeping Ts Grewal Vol. I 2019 For Class 12 Commerce Accountancy Chapter 5 - Admission of A Partner 2Document1 pageDouble Entry Book Keeping Ts Grewal Vol. I 2019 For Class 12 Commerce Accountancy Chapter 5 - Admission of A Partner 2TishaNo ratings yet

- Suspense AccountsDocument5 pagesSuspense Accountsr233684qNo ratings yet

- CA Foundation Accounting SolutionsDocument117 pagesCA Foundation Accounting SolutionsAkash AjayNo ratings yet

- Solution For SharesDocument10 pagesSolution For SharesMohammad Tariq AnsariNo ratings yet

- Recapulitation: Collaborating TechniqueDocument3 pagesRecapulitation: Collaborating TechniqueayeshaNo ratings yet

- P18Document23 pagesP18aleeshaNo ratings yet

- Lecture 11-Forfeiture of SharesDocument12 pagesLecture 11-Forfeiture of SharesAwab HamidNo ratings yet

- Aidcom Financial Accounting AnalysisDocument17 pagesAidcom Financial Accounting AnalysisAjmal K HussainNo ratings yet

- RKG Class 11 Accounts Mock 1 SolDocument14 pagesRKG Class 11 Accounts Mock 1 SolSangket MukherjeeNo ratings yet

- Class Work Chp. 8Document12 pagesClass Work Chp. 8Isha KatiyarNo ratings yet

- TYBAF UnderwritingDocument49 pagesTYBAF UnderwritingJaimin VasaniNo ratings yet

- CA Inter Accounts A MTP 1 Nov 2022Document13 pagesCA Inter Accounts A MTP 1 Nov 2022smartshivenduNo ratings yet

- 104 ReviewDocument4 pages104 ReviewalanNo ratings yet

- Introduction To Financial Accounting: Suggested Answers Foundation Examinations - Spring 2011Document5 pagesIntroduction To Financial Accounting: Suggested Answers Foundation Examinations - Spring 2011adnanNo ratings yet

- Ts Grewal Class 12 Accountancy Chapter 7 PDFDocument11 pagesTs Grewal Class 12 Accountancy Chapter 7 PDFmonikaNo ratings yet

- 12 Accountancy Notes CH07 Company Accounts Issue of Shares 01Document20 pages12 Accountancy Notes CH07 Company Accounts Issue of Shares 01zainab.xf77No ratings yet

- CFN 9305 Accounts Suggested Answers PDFDocument4 pagesCFN 9305 Accounts Suggested Answers PDFDivya PunjabiNo ratings yet

- Corporation Part 1Document9 pagesCorporation Part 11701791No ratings yet

- Class Work Journal EntryDocument16 pagesClass Work Journal EntryRishabh ChawlaNo ratings yet

- QUESTION PAPER 36195 (Solution)Document17 pagesQUESTION PAPER 36195 (Solution)Faizu KhamNo ratings yet

- Sample Paper-1 (Target Term - 2) Answers: Book Recommended - Ultimate Book of Accountancy Class 12Document8 pagesSample Paper-1 (Target Term - 2) Answers: Book Recommended - Ultimate Book of Accountancy Class 12Beena ShibuNo ratings yet

- Mgt402 Assigenment Result Fall2009Document5 pagesMgt402 Assigenment Result Fall2009maqsoom471No ratings yet

- Getting a Job in Hedge Funds: An Inside Look at How Funds HireFrom EverandGetting a Job in Hedge Funds: An Inside Look at How Funds HireRating: 2 out of 5 stars2/5 (1)

- Equity Valuation: Models from Leading Investment BanksFrom EverandEquity Valuation: Models from Leading Investment BanksJan ViebigNo ratings yet

- Solutions 2021 MockExamDocument15 pagesSolutions 2021 MockExamdayeyoutai779No ratings yet

- Accounting Problem Book 2011 PDFDocument103 pagesAccounting Problem Book 2011 PDFViệt Đức Lê67% (3)

- Accounting 1 - Module 4Document12 pagesAccounting 1 - Module 4LuisitoNo ratings yet

- Teknosa 4 QengDocument15 pagesTeknosa 4 QengFaIIen0nENo ratings yet

- AST Chapter 3 MCPDocument20 pagesAST Chapter 3 MCPElleNo ratings yet

- Anatomi Kepala Dan Wajah: by FadhilDocument8 pagesAnatomi Kepala Dan Wajah: by FadhilFadhilNo ratings yet

- Sessions 8 - 9 - BS - SentDocument11 pagesSessions 8 - 9 - BS - SentAjay DesaleNo ratings yet

- Chapter 04 - (The Accounting Cycle. Accruals and Deferrals)Document41 pagesChapter 04 - (The Accounting Cycle. Accruals and Deferrals)Hafiz SherazNo ratings yet

- 74607bos60479 FND cp2 U2Document111 pages74607bos60479 FND cp2 U2adityatiwari122006No ratings yet

- Asynchronous Statement of Financial Position XYZ CompanyDocument5 pagesAsynchronous Statement of Financial Position XYZ CompanyDiana Fernandez MagnoNo ratings yet

- Samsung C&T AuditDocument104 pagesSamsung C&T AuditkevalNo ratings yet

- Preparing Financial StatementsDocument6 pagesPreparing Financial StatementsAUDITOR97No ratings yet

- Principles of Consolidated Financial StatementsDocument13 pagesPrinciples of Consolidated Financial StatementsADEYANJU AKEEM100% (1)

- Template Annual ReportDocument8 pagesTemplate Annual ReportMas Hamzah FansuriNo ratings yet

- Chapter 11 - Depreciation and DepletionDocument46 pagesChapter 11 - Depreciation and DepletionDawn Rei DangkiwNo ratings yet

- Bookkeeping and Payroll Accounting - Module 3Document8 pagesBookkeeping and Payroll Accounting - Module 3LuisitoNo ratings yet

- Salce Prelim Act102 E2Document8 pagesSalce Prelim Act102 E2Joshua P. SalceNo ratings yet

- UNIT-4 - Income-From-BusinessDocument114 pagesUNIT-4 - Income-From-BusinessGuinevereNo ratings yet

- Practical ExerciseDocument9 pagesPractical Exercisesharini subramaniamNo ratings yet

- Accounting For InventoriesDocument9 pagesAccounting For InventoriesPrince AngelNo ratings yet

- Chapter 10Document5 pagesChapter 10Xynith Nicole RamosNo ratings yet

- Accounting For Branches and Combined FSDocument112 pagesAccounting For Branches and Combined FSMuhammad Fahad100% (2)

- U4A5 PracExerciseDocument7 pagesU4A5 PracExerciseDrippy SnowflakeNo ratings yet

- Practice 8: Business Combinations and Impairment Exercise 7.12 Impairment Loss For A CGU, Reversal of Impairment LossDocument7 pagesPractice 8: Business Combinations and Impairment Exercise 7.12 Impairment Loss For A CGU, Reversal of Impairment LossJingwen YangNo ratings yet

- Sip Project of HDFC Bank Financial Statement Analysis.1 (1) @...Document62 pagesSip Project of HDFC Bank Financial Statement Analysis.1 (1) @...Rajendra KhaireNo ratings yet

- Sme Discussion TemplateDocument5 pagesSme Discussion TemplateLeahmae OlimbaNo ratings yet

- Analysis of Financial StatementsDocument16 pagesAnalysis of Financial StatementsAlok ThakurNo ratings yet