Download as pdf or txt

You might also like

- iAL Economics Unit 4 Specimen Paper QPDocument24 pagesiAL Economics Unit 4 Specimen Paper QPSamuel KiruparajNo ratings yet

- ShowReport - 2023-03-29T092401.359Document1 pageShowReport - 2023-03-29T092401.359Moisés BoquinNo ratings yet

- RT Fact BookDocument115 pagesRT Fact BookenzoNo ratings yet

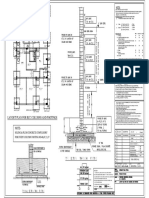

- Layout Plan For RCC Columns and FootingsDocument1 pageLayout Plan For RCC Columns and FootingsHusen GhoriNo ratings yet

- The Pandemic Punch: Ocbc Treasury ResearchDocument4 pagesThe Pandemic Punch: Ocbc Treasury ResearchenzoNo ratings yet

- Rashyu GuyinDocument1 pageRashyu GuyinChandra SegarNo ratings yet

- Mid-Year Investment Outlook For 2023Document14 pagesMid-Year Investment Outlook For 2023ShreyNo ratings yet

- Economic UpdateDocument2 pagesEconomic UpdatedoroteomatteoNo ratings yet

- BIMBSec - Economics - OPR at 4th MPC Meeting 2012 - 20120706Document3 pagesBIMBSec - Economics - OPR at 4th MPC Meeting 2012 - 20120706Bimb SecNo ratings yet

- ASEAN 5 FoxtrotDocument6 pagesASEAN 5 Foxtrotangelo duldulaoNo ratings yet

- Er 20121130 Bull A Us Rba Rates DecemberDocument3 pagesEr 20121130 Bull A Us Rba Rates DecemberBelinda WinkelmanNo ratings yet

- NICE 2014 Rating Update PhilippinesDocument9 pagesNICE 2014 Rating Update PhilippinesGMA News OnlineNo ratings yet

- Market Outlook - Structural Transformation UnderwayDocument27 pagesMarket Outlook - Structural Transformation Underwaysathiaseelans5356No ratings yet

- Er 20130415 Bull Phat DragonDocument3 pagesEr 20130415 Bull Phat DragonBelinda WinkelmanNo ratings yet

- GX Global Powers of Retailing 2022Document52 pagesGX Global Powers of Retailing 2022Ngoc Ngan LyNo ratings yet

- Phat Dragons (Westpac) Weekly Chronicle of The Chinese Economy 16.01.2013Document2 pagesPhat Dragons (Westpac) Weekly Chronicle of The Chinese Economy 16.01.2013leithvanonselenNo ratings yet

- PreBudgetExpectations2011-12 Anagram 180211Document18 pagesPreBudgetExpectations2011-12 Anagram 180211chaterji_aNo ratings yet

- GDP Growth at 5.5% For 1QFY2013Document5 pagesGDP Growth at 5.5% For 1QFY2013Angel BrokingNo ratings yet

- Chief Economists Outlook: Centre For The New Economy and SocietyDocument22 pagesChief Economists Outlook: Centre For The New Economy and SocietycantuscantusNo ratings yet

- Deutsche - 2023 OutlookDocument49 pagesDeutsche - 2023 OutlookEugene QuekNo ratings yet

- AllianzGI Rates Mid Year Outlook 2023 ENG 2023Document14 pagesAllianzGI Rates Mid Year Outlook 2023 ENG 2023Tú Vũ QuangNo ratings yet

- Pakistan Economic Realities PDFDocument3 pagesPakistan Economic Realities PDFsonia JavedNo ratings yet

- Insights Indonesia OutlookDocument15 pagesInsights Indonesia Outlookhanindita GuritnaNo ratings yet

- Exercises Forum Session 11 COMPLETEDDocument4 pagesExercises Forum Session 11 COMPLETEDAgustín Alberto RosalesNo ratings yet

- Weekly Bond Bulletin: Inflation AheadDocument3 pagesWeekly Bond Bulletin: Inflation Aheaddbr trackdNo ratings yet

- Er 20130311 Bull Phat DragonDocument2 pagesEr 20130311 Bull Phat DragonBelinda WinkelmanNo ratings yet

- Outlook 2022 UkDocument48 pagesOutlook 2022 Uk태민No ratings yet

- Empower June 2012Document68 pagesEmpower June 2012pravin963No ratings yet

- Atradius Regional Economic Outlook Asia March 2023 Ern230302Document8 pagesAtradius Regional Economic Outlook Asia March 2023 Ern230302lefebvreNo ratings yet

- C E S - C I W S: Urrent Conomic Cenario AN Ndia Eather The TormDocument5 pagesC E S - C I W S: Urrent Conomic Cenario AN Ndia Eather The TormAbhishek DattaNo ratings yet

- Vol 42Document43 pagesVol 42ANKIT_XXNo ratings yet

- Banking Operation AssignmentDocument7 pagesBanking Operation AssignmentMasela ChilibaNo ratings yet

- Ing Think Asia Philippines Economy Losing Steam Going Into 2021Document5 pagesIng Think Asia Philippines Economy Losing Steam Going Into 2021api-535558346No ratings yet

- Monetary Policy Statement October 2020Document2 pagesMonetary Policy Statement October 2020African Centre for Media ExcellenceNo ratings yet

- The GIC Weekly: Delta DynamicsDocument14 pagesThe GIC Weekly: Delta DynamicsIgor MartinsNo ratings yet

- C O M P A N Y P R O F I L E: Achal Gupta Managing Director & Chief Executive OfficerDocument61 pagesC O M P A N Y P R O F I L E: Achal Gupta Managing Director & Chief Executive OfficervipinkathpalNo ratings yet

- GBP Vemo Summary 2024 VanguardDocument5 pagesGBP Vemo Summary 2024 VanguardMalika YunusovaNo ratings yet

- Newsflash: Malaysia's Economy Grew at The Quickest Pace Since 2010Document2 pagesNewsflash: Malaysia's Economy Grew at The Quickest Pace Since 2010James WarrenNo ratings yet

- Monetary Policy Statement: State Bank of PakistanDocument42 pagesMonetary Policy Statement: State Bank of PakistanScorpian MouniehNo ratings yet

- Monthly Equity Strategy September 2021Document6 pagesMonthly Equity Strategy September 2021Gaurav PatelNo ratings yet

- er20130130BullPhatDragon PDFDocument2 pageser20130130BullPhatDragon PDFBelinda WinkelmanNo ratings yet

- 2023 AsiaDocument8 pages2023 AsiaJuan LaredoNo ratings yet

- SJBMS 23B312 321 RDocument10 pagesSJBMS 23B312 321 RTaimoor ArifNo ratings yet

- RBIPolicy CRISIL 170912Document4 pagesRBIPolicy CRISIL 170912Meenakshi MittalNo ratings yet

- The GIC Weekly: Change in Rates or Rates of Change?Document14 pagesThe GIC Weekly: Change in Rates or Rates of Change?Dylan AdrianNo ratings yet

- MI WP YearAhead2023 PDFDocument13 pagesMI WP YearAhead2023 PDFJNo ratings yet

- 2021-09-07-CS Opportunities During The No-Interest PhaseDocument10 pages2021-09-07-CS Opportunities During The No-Interest PhaseIsaac SamsonNo ratings yet

- Another Roaring '20s For The USDocument55 pagesAnother Roaring '20s For The USeldime06No ratings yet

- Impact of Debt Sustanability On Nigerian Economic DevelopmentDocument18 pagesImpact of Debt Sustanability On Nigerian Economic DevelopmentCentral Asian StudiesNo ratings yet

- Emr2023 en BookDocument105 pagesEmr2023 en BookNazhan ZharifNo ratings yet

- State Street Global Advisors Global Market Outlook 2022Document29 pagesState Street Global Advisors Global Market Outlook 2022Email Sampah KucipNo ratings yet

- Macro Economic Impact Apr08Document16 pagesMacro Economic Impact Apr08shekhar somaNo ratings yet

- Rba StatementDocument4 pagesRba StatementUneth CityNo ratings yet

- Vol 41Document45 pagesVol 41ANKIT_XXNo ratings yet

- FFADOSep11.Direct SentDocument3 pagesFFADOSep11.Direct SentQionghui FengNo ratings yet

- 2019macro Outlook PDFDocument71 pages2019macro Outlook PDFAdiKangdraNo ratings yet

- UOB Global Economics & Markets Research 2021Document1 pageUOB Global Economics & Markets Research 2021Freddy Daniel NababanNo ratings yet

- er20130213BullAusConsumerSentiment PDFDocument2 pageser20130213BullAusConsumerSentiment PDFAmanda MooreNo ratings yet

- Mba 324 Diokno On The Economic Growth of The CountryDocument3 pagesMba 324 Diokno On The Economic Growth of The CountryMark Joseph SoreNo ratings yet

- Case Study On NDB and DFCCDocument34 pagesCase Study On NDB and DFCCRantharu AttanayakeNo ratings yet

- GDP Growth 1QFY2014Document5 pagesGDP Growth 1QFY2014Angel BrokingNo ratings yet

- CMO BofA 10-02-2023 AdaDocument8 pagesCMO BofA 10-02-2023 AdaAlejandroNo ratings yet

- Banking in Africa: financing transformation amid uncertaintyFrom EverandBanking in Africa: financing transformation amid uncertaintyNo ratings yet

- Ocbc Treasury Research: Key ThemesDocument12 pagesOcbc Treasury Research: Key ThemesenzoNo ratings yet

- The Pandemic Punch: Ocbc Treasury ResearchDocument4 pagesThe Pandemic Punch: Ocbc Treasury ResearchenzoNo ratings yet

- Back Inside Again: Ocbc Treasury ResearchDocument2 pagesBack Inside Again: Ocbc Treasury ResearchenzoNo ratings yet

- Dearer Dinner: Ocbc Treasury ResearchDocument2 pagesDearer Dinner: Ocbc Treasury ResearchenzoNo ratings yet

- Going Above and Beyond: To Deliver Value To The WorldDocument11 pagesGoing Above and Beyond: To Deliver Value To The WorldenzoNo ratings yet

- Alba Discloses Its Financial Results For The First Quarter of 2020Document3 pagesAlba Discloses Its Financial Results For The First Quarter of 2020enzoNo ratings yet

- Alba Discloses Its Financial Results For The Third Quarter and Nine-Months of 2020Document4 pagesAlba Discloses Its Financial Results For The Third Quarter and Nine-Months of 2020enzoNo ratings yet

- Revenues & Earnings: All Figures in US$ MillionDocument4 pagesRevenues & Earnings: All Figures in US$ MillionenzoNo ratings yet

- CAT 2 July 2022 SOLUTIONSDocument4 pagesCAT 2 July 2022 SOLUTIONSSandra YebyoNo ratings yet

- This Study Resource WasDocument4 pagesThis Study Resource WasSauban AhmedNo ratings yet

- Conceptual Framework For Financial ReportingDocument1 pageConceptual Framework For Financial Reportingsadegh.ab1380No ratings yet

- Flat Sale in EnglishDocument7 pagesFlat Sale in EnglishDeep HiraniNo ratings yet

- Legal Realism: An LPE Reading List and Introduction: EIL Uxbury Atterns of Merican Urisprudence MER IST EVDocument12 pagesLegal Realism: An LPE Reading List and Introduction: EIL Uxbury Atterns of Merican Urisprudence MER IST EVTWINKLE MAE EGAYNo ratings yet

- Portable Toilet Hire Business PlanDocument5 pagesPortable Toilet Hire Business PlanafwnpberyfodflNo ratings yet

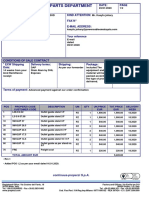

- Parts Catalog PDF 2216 Cd101Document588 pagesParts Catalog PDF 2216 Cd101Diego RodriguezNo ratings yet

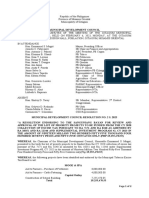

- MDC Resolution 02-2023 Excise Tax Ver 2Document2 pagesMDC Resolution 02-2023 Excise Tax Ver 2Enp Titus Velez100% (1)

- Important Safety NoticeDocument22 pagesImportant Safety NoticeDennis CanasNo ratings yet

- LACROIX v. CANADA (1954) 4 D.L.R. 470: Presented byDocument3 pagesLACROIX v. CANADA (1954) 4 D.L.R. 470: Presented byLina KhalidaNo ratings yet

- Spink Auction World Vanknotes 23231Document188 pagesSpink Auction World Vanknotes 23231Nikola KukrikaNo ratings yet

- 2023-2024 Fix B PTS KELAS 12Document8 pages2023-2024 Fix B PTS KELAS 12milatrikanti80No ratings yet

- Strategy and Business Decision Making (University of Greenwich)Document32 pagesStrategy and Business Decision Making (University of Greenwich)sdrakopoulos323No ratings yet

- Competitor Reviews and Swot Analysis of HykonDocument19 pagesCompetitor Reviews and Swot Analysis of HykonTina chackoNo ratings yet

- Exit Guide From ProperziDocument2 pagesExit Guide From Properzimuhammad kasyfuNo ratings yet

- Data Entry QuestionsDocument9 pagesData Entry QuestionsJackson MafumboNo ratings yet

- Lapto Bill HPDocument1 pageLapto Bill HPNehal SinghNo ratings yet

- Your Energy Statement: BalanceDocument4 pagesYour Energy Statement: BalancePawelNo ratings yet

- Correlation and Regression Correlation: Correlation Between 2 Variables X and Y Indicates Whether They Are Related To EachDocument18 pagesCorrelation and Regression Correlation: Correlation Between 2 Variables X and Y Indicates Whether They Are Related To EachAravind ShekharNo ratings yet

- Does Foreign Aid Help To Achieve Economic Stability - Essay For CSSDocument7 pagesDoes Foreign Aid Help To Achieve Economic Stability - Essay For CSSIhsaan gulzarNo ratings yet

- Ventura, Marymickaellar Chapter6 (2,3,4,20,21)Document2 pagesVentura, Marymickaellar Chapter6 (2,3,4,20,21)Mary VenturaNo ratings yet

- SV-520/550 Instruction ManualDocument32 pagesSV-520/550 Instruction ManualLe DuNo ratings yet

- Nonlinear Relationships: Y X X X X EYXDocument23 pagesNonlinear Relationships: Y X X X X EYXEmmanuella EmefeNo ratings yet

- ECON 222-C SyllabusDocument7 pagesECON 222-C SyllabusAlexis R. CamargoNo ratings yet

- HS20001 Economics ES 2016Document2 pagesHS20001 Economics ES 2016Vivek MarwadeNo ratings yet

- TM Iatf 16949Document2 pagesTM Iatf 16949storymaple94No ratings yet

- MCQs Chapters 156 - The Monetary PolicyDocument40 pagesMCQs Chapters 156 - The Monetary PolicyLộc TrầnNo ratings yet