Sol. Man. - Chapter 9 - Income Taxes - 2021

Sol. Man. - Chapter 9 - Income Taxes - 2021

You might also like

- Week 2 Quiz Answers - Explanations PDFDocument6 pagesWeek 2 Quiz Answers - Explanations PDFanar82% (11)

- R2R Interview QuestionsDocument26 pagesR2R Interview Questions18Sandhya Thapliyal100% (10)

- Lecture Notes Lectures 1 9 Advanced Financial AccountingDocument22 pagesLecture Notes Lectures 1 9 Advanced Financial Accountingsir sahb100% (1)

- ACCOUNTING 3B HomeworkDocument11 pagesACCOUNTING 3B HomeworkRheu Reyes75% (4)

- Income Taxes: Problem 1: True or FalseDocument17 pagesIncome Taxes: Problem 1: True or FalseJean Mira AribalNo ratings yet

- Sol. Man. Chapter 9 Income Taxes 2021Document18 pagesSol. Man. Chapter 9 Income Taxes 2021Kim HanbinNo ratings yet

- Answers Chapter 9 Income TaxesDocument17 pagesAnswers Chapter 9 Income TaxesJeannamy PanizalesNo ratings yet

- Sol. Man. - Chapter 9 Income TaxesDocument15 pagesSol. Man. - Chapter 9 Income TaxesMiguel Amihan100% (1)

- Intacc2 Assignment 6.1 AnswersDocument6 pagesIntacc2 Assignment 6.1 AnswersMingNo ratings yet

- Problems Accouting For Deferred Taxes Webinar ReoDocument7 pagesProblems Accouting For Deferred Taxes Webinar ReocrookshanksNo ratings yet

- Toaz - Info 89bf91d5 1612761367237 PRDocument7 pagesToaz - Info 89bf91d5 1612761367237 PRAEHYUN YENVYNo ratings yet

- ABC Co. Started Its OperationsDocument1 pageABC Co. Started Its OperationsQueen ValleNo ratings yet

- Tutorial 12 (Answer)Document6 pagesTutorial 12 (Answer)Vidya IntaniNo ratings yet

- Gross Reportable Compensation Income 285,000Document3 pagesGross Reportable Compensation Income 285,000WenjunNo ratings yet

- 06 Taxation - Deferred s22Document38 pages06 Taxation - Deferred s22Odzulaho DemanaNo ratings yet

- TAÑOTE Daisy AEC7 MEPIIDocument9 pagesTAÑOTE Daisy AEC7 MEPIIDaisy TañoteNo ratings yet

- Class Activities (Millan, 2019) : Requirements: A. How Much Is The Income Tax Expense For 2003? SolutionDocument6 pagesClass Activities (Millan, 2019) : Requirements: A. How Much Is The Income Tax Expense For 2003? SolutionPrincess TaizeNo ratings yet

- Taxation Final Pre-Board - SolutionsDocument14 pagesTaxation Final Pre-Board - SolutionsMischievous MaeNo ratings yet

- Accounting For Income TaxDocument3 pagesAccounting For Income TaxDaniel Kahn GillamacNo ratings yet

- 06 Taxation - Deferred s20 Final-1Document44 pages06 Taxation - Deferred s20 Final-150902849No ratings yet

- BÀI TẬP NHÓM-IAS12-P11.2-11.3Document5 pagesBÀI TẬP NHÓM-IAS12-P11.2-11.3Kiều OanhNo ratings yet

- LAGRIMAS, Sarah Nicole S. - Income Taxes 2Document4 pagesLAGRIMAS, Sarah Nicole S. - Income Taxes 2saturdaysunbaeNo ratings yet

- CPA Review School of The Philippines Manila First Pre-Board Solutions TaxationDocument8 pagesCPA Review School of The Philippines Manila First Pre-Board Solutions TaxationLive LoveNo ratings yet

- T8 Tutorial SolutionsDocument4 pagesT8 Tutorial SolutionsAnathi AnathiNo ratings yet

- Ia Forcadela Part IIIDocument5 pagesIa Forcadela Part IIIMary Joanne forcadelaNo ratings yet

- Answers - Chapter 5 Vol 2Document5 pagesAnswers - Chapter 5 Vol 2jamfloxNo ratings yet

- Income TaxesDocument3 pagesIncome TaxesCENTENO, JOAN R.No ratings yet

- 2019 IntAcc Vol 3 CH 4 AnswersDocument9 pages2019 IntAcc Vol 3 CH 4 AnswersRizalito SisonNo ratings yet

- IA2 Employee BenefitDocument4 pagesIA2 Employee BenefitCJ RianoNo ratings yet

- PRIA FAR - 014 Income Taxes (PAS 12) Notes and SolutionDocument7 pagesPRIA FAR - 014 Income Taxes (PAS 12) Notes and SolutionEnrique Hills RiveraNo ratings yet

- Finacc 6 A3 1Document4 pagesFinacc 6 A3 1200617No ratings yet

- Output Tax 396,000Document2 pagesOutput Tax 396,000almira garciaNo ratings yet

- R2. TAX ML Solution CMA January 2022 ExaminationDocument6 pagesR2. TAX ML Solution CMA January 2022 ExaminationPavel DhakaNo ratings yet

- Chapter 2 AssignmentDocument8 pagesChapter 2 AssignmentRoss John JimenezNo ratings yet

- Taxation 1-Midterms Exam-Reynancia, Maria Beatrice N.Document4 pagesTaxation 1-Midterms Exam-Reynancia, Maria Beatrice N.Beatrice ReynanciaNo ratings yet

- Financial Accounting 3A Assignment 2Document10 pagesFinancial Accounting 3A Assignment 2Mikaeel MohamedNo ratings yet

- Pricilla AssignmentDocument3 pagesPricilla AssignmentjasonnumahnalkelNo ratings yet

- Solvay Adv Acc Exercises Case 3 Deferred - Taxes IAS 12 - SolutionDocument9 pagesSolvay Adv Acc Exercises Case 3 Deferred - Taxes IAS 12 - SolutionlolaNo ratings yet

- ACT150 Assignment DIMAAMPAODocument4 pagesACT150 Assignment DIMAAMPAOJeromeNo ratings yet

- Tidak Boleh Diakui Sama Sekali: Dicatat Sebagai Deferred TaxDocument7 pagesTidak Boleh Diakui Sama Sekali: Dicatat Sebagai Deferred TaxAlfatih 1453No ratings yet

- Income Taxation - Chapter 2 - Individual TaxpayersDocument5 pagesIncome Taxation - Chapter 2 - Individual TaxpayerscurlybambiNo ratings yet

- Income Taxation Mcqs&ProblemsDocument14 pagesIncome Taxation Mcqs&ProblemsJayrald LacabaNo ratings yet

- Solution Lecture 4 Part 2: Financial Statement With Adjustments Question 1 (A) AdjustmentsDocument7 pagesSolution Lecture 4 Part 2: Financial Statement With Adjustments Question 1 (A) AdjustmentsIsyraf Hatim Mohd TamizamNo ratings yet

- Interim Financial Reporting: Problem 45-1: True or FalseDocument9 pagesInterim Financial Reporting: Problem 45-1: True or FalseAudrey AganNo ratings yet

- Interim Financial Reporting: Problem 45-1: True or FalseDocument9 pagesInterim Financial Reporting: Problem 45-1: True or FalseAudrey AganNo ratings yet

- Assignment E & L Env 4 BusiDocument9 pagesAssignment E & L Env 4 BusiSyed Hamza RasheedNo ratings yet

- Tax 8 9 12Document5 pagesTax 8 9 12Maix19No ratings yet

- Orca Share Media1540033147945Document17 pagesOrca Share Media1540033147945Melady Sison CequeñaNo ratings yet

- Insurance Expense Allocated To The Quarter: SolutionDocument4 pagesInsurance Expense Allocated To The Quarter: Solutionasdfghjkl zxcvbnmNo ratings yet

- Interim Financial Reporting: Problem 45-1: True or FalseDocument7 pagesInterim Financial Reporting: Problem 45-1: True or FalseMarjorieNo ratings yet

- Interim Financial Reporting: Problem 45-1: True or FalseDocument7 pagesInterim Financial Reporting: Problem 45-1: True or FalseXyverbel Ocampo RegNo ratings yet

- Interim Financial ReportingDocument7 pagesInterim Financial ReportingRey Joyce AbuelNo ratings yet

- TAX Final Preboard Examination - Solutions PDFDocument15 pagesTAX Final Preboard Examination - Solutions PDF813 cafeNo ratings yet

- TAX ANSWER-R4Tanyag KeyDocument5 pagesTAX ANSWER-R4Tanyag KeyCheska JaplosNo ratings yet

- Sol. Man. - Chapter 9 - Interim Financial ReportingDocument6 pagesSol. Man. - Chapter 9 - Interim Financial ReportingAEDRIAN LEE DERECHONo ratings yet

- Solution NIngDocument3 pagesSolution NIngfahim tusarNo ratings yet

- Less: Cost of Goods Sold: Capital ExpenditureDocument3 pagesLess: Cost of Goods Sold: Capital Expenditurefahim tusarNo ratings yet

- Bai Tap - IAS 12 - Tu LuanDocument14 pagesBai Tap - IAS 12 - Tu LuanTrần Nguyễn Tuệ MinhNo ratings yet

- Case Study 1Document7 pagesCase Study 1Trisha Mae Mendoza MacalinoNo ratings yet

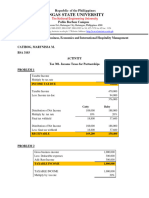

- Catibog, Marynissa M. - Activity On Income Taxes For PartnershipsDocument2 pagesCatibog, Marynissa M. - Activity On Income Taxes For PartnershipsMarynissa CatibogNo ratings yet

- Income Tax AccountingDocument3 pagesIncome Tax Accountinghae1234No ratings yet

- AFA IIP.L III SolutionJune 2016Document4 pagesAFA IIP.L III SolutionJune 2016HossainNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Accounting ReviewersDocument44 pagesAccounting ReviewersPortgas D. AceNo ratings yet

- Bookkeeping To Trial Balance 10Document15 pagesBookkeeping To Trial Balance 10elelwaniNo ratings yet

- Pak Suzuki Motors Financial Analysis With Interpretation PDFDocument30 pagesPak Suzuki Motors Financial Analysis With Interpretation PDFNazir AnsariNo ratings yet

- XII - Accy. QP - Revision-15.2.14Document6 pagesXII - Accy. QP - Revision-15.2.14devipreethiNo ratings yet

- ACCO 20063 Homework 4 Review of Accounting CycleDocument3 pagesACCO 20063 Homework 4 Review of Accounting CycleVincent Luigil Alcera100% (1)

- Accrual and ProvisionDocument66 pagesAccrual and ProvisionVeronica Bailey100% (1)

- Session 5-6: Accounting Records: Instructor Dr. Jagan Kumar SurDocument48 pagesSession 5-6: Accounting Records: Instructor Dr. Jagan Kumar SurBabusona SahaNo ratings yet

- CH 05Document72 pagesCH 05Chang Chan ChongNo ratings yet

- What Is 'Earnest Money': Definition and ExplanationDocument4 pagesWhat Is 'Earnest Money': Definition and ExplanationJaisurya SharmaNo ratings yet

- Cambridge International Examinations Cambridge International General Certificate of Secondary EducationDocument20 pagesCambridge International Examinations Cambridge International General Certificate of Secondary EducationAung Zaw HtweNo ratings yet

- Balaji Telefilms LTD: Key Financial IndicatorsDocument4 pagesBalaji Telefilms LTD: Key Financial IndicatorsGagandeep KaurNo ratings yet

- JHM 1Qtr21 Financial Report (Amendment)Document13 pagesJHM 1Qtr21 Financial Report (Amendment)Ooi Gim SengNo ratings yet

- Chap 4Document7 pagesChap 4hcw49539No ratings yet

- Intermediate Accounting 19Th Edition Stice Solutions Manual Full Chapter PDFDocument66 pagesIntermediate Accounting 19Th Edition Stice Solutions Manual Full Chapter PDFDebraWhitecxgn100% (11)

- Financial and Managerial Accounting PDFDocument1 pageFinancial and Managerial Accounting PDFcons theNo ratings yet

- Bwel 2021Document48 pagesBwel 2021ashwinsecfilingsNo ratings yet

- Mini Case - Chapter 14Document8 pagesMini Case - Chapter 14Jennifer Johnson100% (1)

- University of The Cordilleras College of Accountancy Quiz On Partnership Formation 1Document6 pagesUniversity of The Cordilleras College of Accountancy Quiz On Partnership Formation 1Ian Ranilopa100% (1)

- Performed 5000 Worth of Service For A Customer On Account: AccrualDocument10 pagesPerformed 5000 Worth of Service For A Customer On Account: AccrualShin Shan JeonNo ratings yet

- Accounting Principles Chapter 4 SolutionDocument154 pagesAccounting Principles Chapter 4 SolutionMaldin JeremiaNo ratings yet

- PartnershipDocument10 pagesPartnershipJasmine Marie Ng Cheong50% (2)

- Worksheet 1Document4 pagesWorksheet 1mahistudyaccNo ratings yet

- Activity 2Document5 pagesActivity 2danica dimaculanganNo ratings yet

- Q3 Oikonomikes Katastaseis enDocument91 pagesQ3 Oikonomikes Katastaseis enVenture ConsultancyNo ratings yet

- Final Exam Autumn 2011 v1Document38 pagesFinal Exam Autumn 2011 v1peter kongNo ratings yet

- Case 36 J.C. Penney CompanyFileDocument4 pagesCase 36 J.C. Penney CompanyFileKanoknad KalaphakdeeNo ratings yet

Download as docx, pdf, or txt

You might also like

- Week 2 Quiz Answers - Explanations PDFDocument6 pagesWeek 2 Quiz Answers - Explanations PDFanar82% (11)

- R2R Interview QuestionsDocument26 pagesR2R Interview Questions18Sandhya Thapliyal100% (10)

- Lecture Notes Lectures 1 9 Advanced Financial AccountingDocument22 pagesLecture Notes Lectures 1 9 Advanced Financial Accountingsir sahb100% (1)

- ACCOUNTING 3B HomeworkDocument11 pagesACCOUNTING 3B HomeworkRheu Reyes75% (4)

- Income Taxes: Problem 1: True or FalseDocument17 pagesIncome Taxes: Problem 1: True or FalseJean Mira AribalNo ratings yet

- Sol. Man. Chapter 9 Income Taxes 2021Document18 pagesSol. Man. Chapter 9 Income Taxes 2021Kim HanbinNo ratings yet

- Answers Chapter 9 Income TaxesDocument17 pagesAnswers Chapter 9 Income TaxesJeannamy PanizalesNo ratings yet

- Sol. Man. - Chapter 9 Income TaxesDocument15 pagesSol. Man. - Chapter 9 Income TaxesMiguel Amihan100% (1)

- Intacc2 Assignment 6.1 AnswersDocument6 pagesIntacc2 Assignment 6.1 AnswersMingNo ratings yet

- Problems Accouting For Deferred Taxes Webinar ReoDocument7 pagesProblems Accouting For Deferred Taxes Webinar ReocrookshanksNo ratings yet

- Toaz - Info 89bf91d5 1612761367237 PRDocument7 pagesToaz - Info 89bf91d5 1612761367237 PRAEHYUN YENVYNo ratings yet

- ABC Co. Started Its OperationsDocument1 pageABC Co. Started Its OperationsQueen ValleNo ratings yet

- Tutorial 12 (Answer)Document6 pagesTutorial 12 (Answer)Vidya IntaniNo ratings yet

- Gross Reportable Compensation Income 285,000Document3 pagesGross Reportable Compensation Income 285,000WenjunNo ratings yet

- 06 Taxation - Deferred s22Document38 pages06 Taxation - Deferred s22Odzulaho DemanaNo ratings yet

- TAÑOTE Daisy AEC7 MEPIIDocument9 pagesTAÑOTE Daisy AEC7 MEPIIDaisy TañoteNo ratings yet

- Class Activities (Millan, 2019) : Requirements: A. How Much Is The Income Tax Expense For 2003? SolutionDocument6 pagesClass Activities (Millan, 2019) : Requirements: A. How Much Is The Income Tax Expense For 2003? SolutionPrincess TaizeNo ratings yet

- Taxation Final Pre-Board - SolutionsDocument14 pagesTaxation Final Pre-Board - SolutionsMischievous MaeNo ratings yet

- Accounting For Income TaxDocument3 pagesAccounting For Income TaxDaniel Kahn GillamacNo ratings yet

- 06 Taxation - Deferred s20 Final-1Document44 pages06 Taxation - Deferred s20 Final-150902849No ratings yet

- BÀI TẬP NHÓM-IAS12-P11.2-11.3Document5 pagesBÀI TẬP NHÓM-IAS12-P11.2-11.3Kiều OanhNo ratings yet

- LAGRIMAS, Sarah Nicole S. - Income Taxes 2Document4 pagesLAGRIMAS, Sarah Nicole S. - Income Taxes 2saturdaysunbaeNo ratings yet

- CPA Review School of The Philippines Manila First Pre-Board Solutions TaxationDocument8 pagesCPA Review School of The Philippines Manila First Pre-Board Solutions TaxationLive LoveNo ratings yet

- T8 Tutorial SolutionsDocument4 pagesT8 Tutorial SolutionsAnathi AnathiNo ratings yet

- Ia Forcadela Part IIIDocument5 pagesIa Forcadela Part IIIMary Joanne forcadelaNo ratings yet

- Answers - Chapter 5 Vol 2Document5 pagesAnswers - Chapter 5 Vol 2jamfloxNo ratings yet

- Income TaxesDocument3 pagesIncome TaxesCENTENO, JOAN R.No ratings yet

- 2019 IntAcc Vol 3 CH 4 AnswersDocument9 pages2019 IntAcc Vol 3 CH 4 AnswersRizalito SisonNo ratings yet

- IA2 Employee BenefitDocument4 pagesIA2 Employee BenefitCJ RianoNo ratings yet

- PRIA FAR - 014 Income Taxes (PAS 12) Notes and SolutionDocument7 pagesPRIA FAR - 014 Income Taxes (PAS 12) Notes and SolutionEnrique Hills RiveraNo ratings yet

- Finacc 6 A3 1Document4 pagesFinacc 6 A3 1200617No ratings yet

- Output Tax 396,000Document2 pagesOutput Tax 396,000almira garciaNo ratings yet

- R2. TAX ML Solution CMA January 2022 ExaminationDocument6 pagesR2. TAX ML Solution CMA January 2022 ExaminationPavel DhakaNo ratings yet

- Chapter 2 AssignmentDocument8 pagesChapter 2 AssignmentRoss John JimenezNo ratings yet

- Taxation 1-Midterms Exam-Reynancia, Maria Beatrice N.Document4 pagesTaxation 1-Midterms Exam-Reynancia, Maria Beatrice N.Beatrice ReynanciaNo ratings yet

- Financial Accounting 3A Assignment 2Document10 pagesFinancial Accounting 3A Assignment 2Mikaeel MohamedNo ratings yet

- Pricilla AssignmentDocument3 pagesPricilla AssignmentjasonnumahnalkelNo ratings yet

- Solvay Adv Acc Exercises Case 3 Deferred - Taxes IAS 12 - SolutionDocument9 pagesSolvay Adv Acc Exercises Case 3 Deferred - Taxes IAS 12 - SolutionlolaNo ratings yet

- ACT150 Assignment DIMAAMPAODocument4 pagesACT150 Assignment DIMAAMPAOJeromeNo ratings yet

- Tidak Boleh Diakui Sama Sekali: Dicatat Sebagai Deferred TaxDocument7 pagesTidak Boleh Diakui Sama Sekali: Dicatat Sebagai Deferred TaxAlfatih 1453No ratings yet

- Income Taxation - Chapter 2 - Individual TaxpayersDocument5 pagesIncome Taxation - Chapter 2 - Individual TaxpayerscurlybambiNo ratings yet

- Income Taxation Mcqs&ProblemsDocument14 pagesIncome Taxation Mcqs&ProblemsJayrald LacabaNo ratings yet

- Solution Lecture 4 Part 2: Financial Statement With Adjustments Question 1 (A) AdjustmentsDocument7 pagesSolution Lecture 4 Part 2: Financial Statement With Adjustments Question 1 (A) AdjustmentsIsyraf Hatim Mohd TamizamNo ratings yet

- Interim Financial Reporting: Problem 45-1: True or FalseDocument9 pagesInterim Financial Reporting: Problem 45-1: True or FalseAudrey AganNo ratings yet

- Interim Financial Reporting: Problem 45-1: True or FalseDocument9 pagesInterim Financial Reporting: Problem 45-1: True or FalseAudrey AganNo ratings yet

- Assignment E & L Env 4 BusiDocument9 pagesAssignment E & L Env 4 BusiSyed Hamza RasheedNo ratings yet

- Tax 8 9 12Document5 pagesTax 8 9 12Maix19No ratings yet

- Orca Share Media1540033147945Document17 pagesOrca Share Media1540033147945Melady Sison CequeñaNo ratings yet

- Insurance Expense Allocated To The Quarter: SolutionDocument4 pagesInsurance Expense Allocated To The Quarter: Solutionasdfghjkl zxcvbnmNo ratings yet

- Interim Financial Reporting: Problem 45-1: True or FalseDocument7 pagesInterim Financial Reporting: Problem 45-1: True or FalseMarjorieNo ratings yet

- Interim Financial Reporting: Problem 45-1: True or FalseDocument7 pagesInterim Financial Reporting: Problem 45-1: True or FalseXyverbel Ocampo RegNo ratings yet

- Interim Financial ReportingDocument7 pagesInterim Financial ReportingRey Joyce AbuelNo ratings yet

- TAX Final Preboard Examination - Solutions PDFDocument15 pagesTAX Final Preboard Examination - Solutions PDF813 cafeNo ratings yet

- TAX ANSWER-R4Tanyag KeyDocument5 pagesTAX ANSWER-R4Tanyag KeyCheska JaplosNo ratings yet

- Sol. Man. - Chapter 9 - Interim Financial ReportingDocument6 pagesSol. Man. - Chapter 9 - Interim Financial ReportingAEDRIAN LEE DERECHONo ratings yet

- Solution NIngDocument3 pagesSolution NIngfahim tusarNo ratings yet

- Less: Cost of Goods Sold: Capital ExpenditureDocument3 pagesLess: Cost of Goods Sold: Capital Expenditurefahim tusarNo ratings yet

- Bai Tap - IAS 12 - Tu LuanDocument14 pagesBai Tap - IAS 12 - Tu LuanTrần Nguyễn Tuệ MinhNo ratings yet

- Case Study 1Document7 pagesCase Study 1Trisha Mae Mendoza MacalinoNo ratings yet

- Catibog, Marynissa M. - Activity On Income Taxes For PartnershipsDocument2 pagesCatibog, Marynissa M. - Activity On Income Taxes For PartnershipsMarynissa CatibogNo ratings yet

- Income Tax AccountingDocument3 pagesIncome Tax Accountinghae1234No ratings yet

- AFA IIP.L III SolutionJune 2016Document4 pagesAFA IIP.L III SolutionJune 2016HossainNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Accounting ReviewersDocument44 pagesAccounting ReviewersPortgas D. AceNo ratings yet

- Bookkeeping To Trial Balance 10Document15 pagesBookkeeping To Trial Balance 10elelwaniNo ratings yet

- Pak Suzuki Motors Financial Analysis With Interpretation PDFDocument30 pagesPak Suzuki Motors Financial Analysis With Interpretation PDFNazir AnsariNo ratings yet

- XII - Accy. QP - Revision-15.2.14Document6 pagesXII - Accy. QP - Revision-15.2.14devipreethiNo ratings yet

- ACCO 20063 Homework 4 Review of Accounting CycleDocument3 pagesACCO 20063 Homework 4 Review of Accounting CycleVincent Luigil Alcera100% (1)

- Accrual and ProvisionDocument66 pagesAccrual and ProvisionVeronica Bailey100% (1)

- Session 5-6: Accounting Records: Instructor Dr. Jagan Kumar SurDocument48 pagesSession 5-6: Accounting Records: Instructor Dr. Jagan Kumar SurBabusona SahaNo ratings yet

- CH 05Document72 pagesCH 05Chang Chan ChongNo ratings yet

- What Is 'Earnest Money': Definition and ExplanationDocument4 pagesWhat Is 'Earnest Money': Definition and ExplanationJaisurya SharmaNo ratings yet

- Cambridge International Examinations Cambridge International General Certificate of Secondary EducationDocument20 pagesCambridge International Examinations Cambridge International General Certificate of Secondary EducationAung Zaw HtweNo ratings yet

- Balaji Telefilms LTD: Key Financial IndicatorsDocument4 pagesBalaji Telefilms LTD: Key Financial IndicatorsGagandeep KaurNo ratings yet

- JHM 1Qtr21 Financial Report (Amendment)Document13 pagesJHM 1Qtr21 Financial Report (Amendment)Ooi Gim SengNo ratings yet

- Chap 4Document7 pagesChap 4hcw49539No ratings yet

- Intermediate Accounting 19Th Edition Stice Solutions Manual Full Chapter PDFDocument66 pagesIntermediate Accounting 19Th Edition Stice Solutions Manual Full Chapter PDFDebraWhitecxgn100% (11)

- Financial and Managerial Accounting PDFDocument1 pageFinancial and Managerial Accounting PDFcons theNo ratings yet

- Bwel 2021Document48 pagesBwel 2021ashwinsecfilingsNo ratings yet

- Mini Case - Chapter 14Document8 pagesMini Case - Chapter 14Jennifer Johnson100% (1)

- University of The Cordilleras College of Accountancy Quiz On Partnership Formation 1Document6 pagesUniversity of The Cordilleras College of Accountancy Quiz On Partnership Formation 1Ian Ranilopa100% (1)

- Performed 5000 Worth of Service For A Customer On Account: AccrualDocument10 pagesPerformed 5000 Worth of Service For A Customer On Account: AccrualShin Shan JeonNo ratings yet

- Accounting Principles Chapter 4 SolutionDocument154 pagesAccounting Principles Chapter 4 SolutionMaldin JeremiaNo ratings yet

- PartnershipDocument10 pagesPartnershipJasmine Marie Ng Cheong50% (2)

- Worksheet 1Document4 pagesWorksheet 1mahistudyaccNo ratings yet

- Activity 2Document5 pagesActivity 2danica dimaculanganNo ratings yet

- Q3 Oikonomikes Katastaseis enDocument91 pagesQ3 Oikonomikes Katastaseis enVenture ConsultancyNo ratings yet

- Final Exam Autumn 2011 v1Document38 pagesFinal Exam Autumn 2011 v1peter kongNo ratings yet

- Case 36 J.C. Penney CompanyFileDocument4 pagesCase 36 J.C. Penney CompanyFileKanoknad KalaphakdeeNo ratings yet