Download as pdf or txt

You might also like

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeFrom EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeRating: 4 out of 5 stars4/5 (5820)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreFrom EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreRating: 4 out of 5 stars4/5 (1093)

- Never Split the Difference: Negotiating As If Your Life Depended On ItFrom EverandNever Split the Difference: Negotiating As If Your Life Depended On ItRating: 4.5 out of 5 stars4.5/5 (845)

- Grit: The Power of Passion and PerseveranceFrom EverandGrit: The Power of Passion and PerseveranceRating: 4 out of 5 stars4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceFrom EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceRating: 4 out of 5 stars4/5 (898)

- Shoe Dog: A Memoir by the Creator of NikeFrom EverandShoe Dog: A Memoir by the Creator of NikeRating: 4.5 out of 5 stars4.5/5 (540)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersFrom EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersRating: 4.5 out of 5 stars4.5/5 (349)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureFrom EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureRating: 4.5 out of 5 stars4.5/5 (474)

- Her Body and Other Parties: StoriesFrom EverandHer Body and Other Parties: StoriesRating: 4 out of 5 stars4/5 (822)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)From EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Rating: 4.5 out of 5 stars4.5/5 (122)

- The Emperor of All Maladies: A Biography of CancerFrom EverandThe Emperor of All Maladies: A Biography of CancerRating: 4.5 out of 5 stars4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingFrom EverandThe Little Book of Hygge: Danish Secrets to Happy LivingRating: 3.5 out of 5 stars3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyFrom EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyRating: 3.5 out of 5 stars3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)From EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Rating: 4 out of 5 stars4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaFrom EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaRating: 4.5 out of 5 stars4.5/5 (266)

- Team of Rivals: The Political Genius of Abraham LincolnFrom EverandTeam of Rivals: The Political Genius of Abraham LincolnRating: 4.5 out of 5 stars4.5/5 (234)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryFrom EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryRating: 3.5 out of 5 stars3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealFrom EverandOn Fire: The (Burning) Case for a Green New DealRating: 4 out of 5 stars4/5 (74)

- The Unwinding: An Inner History of the New AmericaFrom EverandThe Unwinding: An Inner History of the New AmericaRating: 4 out of 5 stars4/5 (45)

- A Guide To Food Selection, Preparation and PreservationDocument205 pagesA Guide To Food Selection, Preparation and Preservationdsissht83% (65)

- 3685-Article Text-6899-1-10-20210423Document9 pages3685-Article Text-6899-1-10-20210423K57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- Eps2004045org 9058920712 MulderDocument262 pagesEps2004045org 9058920712 MulderK57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- Vietnam Internet Resources 2013: Report OnDocument38 pagesVietnam Internet Resources 2013: Report OnK57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- The Effect of Sales Promotion and Knowledge On Impulsive Buying of Online Platform ConsumersDocument15 pagesThe Effect of Sales Promotion and Knowledge On Impulsive Buying of Online Platform ConsumersK57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- Impact of Sales Promotion On Consumer Impulse Purchases in Karachi, PakistanDocument32 pagesImpact of Sales Promotion On Consumer Impulse Purchases in Karachi, PakistanK57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- What If I Find It Cheaper Someplace ElseDocument18 pagesWhat If I Find It Cheaper Someplace ElseK57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- Study On Online Purchase Decisions On The Online Shopee Selling SiteDocument7 pagesStudy On Online Purchase Decisions On The Online Shopee Selling SiteK57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- The Consequences of Doing Nothing Inaction InertiaDocument11 pagesThe Consequences of Doing Nothing Inaction InertiaK57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- Market Pulse Q4 Report - Nielsen Viet Nam: Prepared by Nielsen Vietnam February 2017Document8 pagesMarket Pulse Q4 Report - Nielsen Viet Nam: Prepared by Nielsen Vietnam February 2017K57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- Nielsen Traditional Trade Report FINALDocument20 pagesNielsen Traditional Trade Report FINALK57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- EVBN Report Retail Final Report - CompressedDocument52 pagesEVBN Report Retail Final Report - CompressedK57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- Vietnam Retail Market and Comsumer TRENDS 2020Document27 pagesVietnam Retail Market and Comsumer TRENDS 2020K57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- Nielsen Market Pulse Q3 2017Document2 pagesNielsen Market Pulse Q3 2017K57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- Nielsen Market Pulse Q2 2018Document6 pagesNielsen Market Pulse Q2 2018K57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- Retail Foods Hanoi Vietnam 3-7-2017Document30 pagesRetail Foods Hanoi Vietnam 3-7-2017K57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- Nielsen Market Pulse Q3 2016Document8 pagesNielsen Market Pulse Q3 2016K57.CTTT BUI NGUYEN HUONG LYNo ratings yet

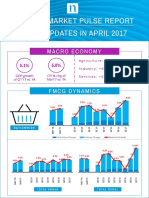

- Agriculture: +2.0% Industry: +4.2% Services: +6.5%: Unit Value Change Volume Change Nominal GrowthDocument2 pagesAgriculture: +2.0% Industry: +4.2% Services: +6.5%: Unit Value Change Volume Change Nominal GrowthK57.CTTT BUI NGUYEN HUONG LYNo ratings yet

- MATH 10 SummativeDocument6 pagesMATH 10 SummativeEmerita TrasesNo ratings yet

- NCMA121.HAs - RLE PHYSICAL ASSESSMENT ADULT PART 1Document3 pagesNCMA121.HAs - RLE PHYSICAL ASSESSMENT ADULT PART 1Rowena SamsonNo ratings yet

- Biosafety in The LaboratoryDocument1 pageBiosafety in The LaboratoryALFARO CHAT CARMINA ROSARIONo ratings yet

- PCL-R II Advanced PCL-R TrainingDocument113 pagesPCL-R II Advanced PCL-R TrainingDr. Anna C. Salter100% (1)

- A. LISTENING (50 Points) : Part 1: (10 PTS.)Document9 pagesA. LISTENING (50 Points) : Part 1: (10 PTS.)Dương LêNo ratings yet

- Icds N AayDocument8 pagesIcds N AayMeghan PaulNo ratings yet

- DLL 8 W6Document4 pagesDLL 8 W6Kristela Mae ColomaNo ratings yet

- Mase Student Planner 6Document25 pagesMase Student Planner 6api-242315971No ratings yet

- Chem Lab Safety IS.4209.1987Document25 pagesChem Lab Safety IS.4209.1987DEE TOTLVJANo ratings yet

- Learning Objectives DS: ScenarioDocument31 pagesLearning Objectives DS: ScenarioSeyna OfficialNo ratings yet

- Id AssignmentDocument4 pagesId AssignmentAmutuhaire JudithNo ratings yet

- Autism and Occupational Therapy: Optimizing FunctionDocument18 pagesAutism and Occupational Therapy: Optimizing Functiondrana1No ratings yet

- Advanced Rigging Principles - Student HandbookDocument204 pagesAdvanced Rigging Principles - Student HandbookChrisselda-ü AndalecioNo ratings yet

- How To Survive Christmas After LossDocument14 pagesHow To Survive Christmas After LossVenetta CoetzeeNo ratings yet

- The Contours of Positive Human HealthDocument29 pagesThe Contours of Positive Human HealthSalvadorNo ratings yet

- Tatalaksana Awal Koreksi Cairan Pada Kasus Syok - Dr. Rudy K, SP - PDDocument60 pagesTatalaksana Awal Koreksi Cairan Pada Kasus Syok - Dr. Rudy K, SP - PDmuhammad benyNo ratings yet

- What Is Bisexual - Google SearchDocument1 pageWhat Is Bisexual - Google SearchYe etNo ratings yet

- Food Answers Food Answers: 8aa/8 8aa/8Document6 pagesFood Answers Food Answers: 8aa/8 8aa/8Helen100% (1)

- DHRD - Handbook - 2017 - Chapter - 3 TRNG DevtDocument5 pagesDHRD - Handbook - 2017 - Chapter - 3 TRNG DevtLino MomonganNo ratings yet

- Why Do We Measure Coronary Artery Calcium Score?Document6 pagesWhy Do We Measure Coronary Artery Calcium Score?eugeniaNo ratings yet

- Dysfunctional FamiliesDocument2 pagesDysfunctional FamiliesJane JasaNo ratings yet

- Compounding Pharmacist Resume ExampleDocument1 pageCompounding Pharmacist Resume Exampleakanksha pisalNo ratings yet

- Lesson Plan in Science 10Document3 pagesLesson Plan in Science 10Phranxies Jean BlayaNo ratings yet

- PERFECT TENSES - More Practice + SolutionsDocument3 pagesPERFECT TENSES - More Practice + SolutionsEstherEscudero100% (1)

- Hospital Equipment. Research ReportDocument6 pagesHospital Equipment. Research ReportYazan Al JabariNo ratings yet

- Psu Genrel 2013 14 Misc Non Event UPPERFIXDocument1 pagePsu Genrel 2013 14 Misc Non Event UPPERFIXKayque RibeiroNo ratings yet

- Creatina FosfoquinasaDocument1 pageCreatina Fosfoquinasasusey tepaNo ratings yet

- A. B. C. D. E. F. G.: Crutch-WalkingDocument4 pagesA. B. C. D. E. F. G.: Crutch-WalkingGene BulaNo ratings yet

- Acitivity 4Document2 pagesAcitivity 4Elijah Mae MundocNo ratings yet