Download as pdf or txt

You might also like

- Western Union Carding TutorialDocument5 pagesWestern Union Carding TutorialBass12100% (2)

- Chase E-Statement FebruaryDocument4 pagesChase E-Statement February76xzv4kk5vNo ratings yet

- CompleteFreedom-2517-03Apr2021 2021-04-08 at 8.15.26 AMDocument67 pagesCompleteFreedom-2517-03Apr2021 2021-04-08 at 8.15.26 AMSimerjeet SinghNo ratings yet

- Customer Relationship - Axis Bank DeepanshuDocument101 pagesCustomer Relationship - Axis Bank Deepanshudeepak Gupta100% (1)

- Hailey College of Banking and FinanceDocument18 pagesHailey College of Banking and Financesea waterNo ratings yet

- Bills Discounting: Dr. Sarbesh Mishra, Finance AreaDocument9 pagesBills Discounting: Dr. Sarbesh Mishra, Finance AreaDr Sarbesh MishraNo ratings yet

- Promissory Notes-Bills of Exchangeand ChequesDocument17 pagesPromissory Notes-Bills of Exchangeand Chequestheashu022No ratings yet

- Dealing With DebtDocument36 pagesDealing With DebtJanezNo ratings yet

- Origin of Banking: By: Dr. Swati GargDocument56 pagesOrigin of Banking: By: Dr. Swati GargSwati GargNo ratings yet

- Guide ON Transfer & Transmission of Shares and DebenturesDocument10 pagesGuide ON Transfer & Transmission of Shares and DebenturesM. Aqeel SaleemNo ratings yet

- Knowledge Bank - Advances Against DepositsDocument4 pagesKnowledge Bank - Advances Against DepositsKajeev KumarNo ratings yet

- Delegation of Authority - Involves The Concept of Looking at The Actual Authority orDocument4 pagesDelegation of Authority - Involves The Concept of Looking at The Actual Authority orCynthia Udeh-MartinNo ratings yet

- INISS Prospectus Jan-2024 V3Document42 pagesINISS Prospectus Jan-2024 V3lakshminivas Pingali100% (1)

- IIFL Securities POA Format KARVYDocument2 pagesIIFL Securities POA Format KARVYabhifake kkNo ratings yet

- Collection Agency LeterDocument2 pagesCollection Agency LeterTommyNo ratings yet

- After Judgement Guide To Getting Results ENDocument25 pagesAfter Judgement Guide To Getting Results ENTim GordashNo ratings yet

- Class 11 Accountancy NCERT Textbook Chapter 8 Bill of ExchangeDocument47 pagesClass 11 Accountancy NCERT Textbook Chapter 8 Bill of ExchangePathan KausarNo ratings yet

- Gaap and AuditDocument35 pagesGaap and AuditAayushi Arora100% (1)

- Part Vi:Trust Receipts LawDocument5 pagesPart Vi:Trust Receipts LawThrees SeeNo ratings yet

- To Study The Nationalize Plastic Money Payment Gateway SystemDocument39 pagesTo Study The Nationalize Plastic Money Payment Gateway SystemRajesh Singh100% (1)

- Bangladesh Electronic Funds Transfer Network (Beftn) : Presented By: Central BACH, Payment Service Department, (PSD)Document19 pagesBangladesh Electronic Funds Transfer Network (Beftn) : Presented By: Central BACH, Payment Service Department, (PSD)Tanvir MahmudNo ratings yet

- Right and Liabilities of Paying and Collecting BankersDocument3 pagesRight and Liabilities of Paying and Collecting BankersAtul KansalNo ratings yet

- E-Way Bill Step by StepDocument25 pagesE-Way Bill Step by Stepanon_226743984No ratings yet

- BankingDocument29 pagesBankingKenneth Wilson BavachanNo ratings yet

- Banking & Insurance Law SyllabusDocument3 pagesBanking & Insurance Law Syllabusriko avNo ratings yet

- Module 2 - Negotiable Instrument ActDocument62 pagesModule 2 - Negotiable Instrument ActVK GamerNo ratings yet

- Debt CollectionDocument4 pagesDebt CollectionLM RioNo ratings yet

- Digital SignatureDocument39 pagesDigital Signaturevijay anandNo ratings yet

- Affidavit For CourtDocument1 pageAffidavit For CourtWalter WhiteNo ratings yet

- Revisiting The Legal Tender CasesDocument52 pagesRevisiting The Legal Tender CasesA1 Hair BeautyNo ratings yet

- Seminar7 Group Discussion1cDocument55 pagesSeminar7 Group Discussion1cMytee TarasonNo ratings yet

- 4 - Negotiable Instrument Act PDFDocument48 pages4 - Negotiable Instrument Act PDFAmit royNo ratings yet

- Mitc Credit CardsDocument31 pagesMitc Credit Cardsguru jeeNo ratings yet

- Assignment On Insurance Policy On The Basis of Northern General Insurance Co. LTDDocument18 pagesAssignment On Insurance Policy On The Basis of Northern General Insurance Co. LTDBristir Majhe TumiNo ratings yet

- SecuritisationDocument74 pagesSecuritisationrohitpatil699No ratings yet

- (B-4) Bills of Exchange ActDocument67 pages(B-4) Bills of Exchange ActJoy100% (1)

- Contracts Unit 5Document10 pagesContracts Unit 5Karina JacobNo ratings yet

- CHAPTER VII - Bank GuaranteesDocument12 pagesCHAPTER VII - Bank Guaranteespriya guptaNo ratings yet

- Negotiable Instruments: Commercial PaperDocument45 pagesNegotiable Instruments: Commercial PaperSimranNo ratings yet

- Complaint Against James McNeile and Andrew Duncan (May 16, 2016)Document5 pagesComplaint Against James McNeile and Andrew Duncan (May 16, 2016)Conflict GateNo ratings yet

- TenderDocument31 pagesTenderdurgesh pandharpureNo ratings yet

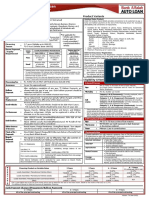

- Alfalah Auto Loan: Policy One PagerDocument1 pageAlfalah Auto Loan: Policy One PagerbilalasifNo ratings yet

- Re Residential Tenancies - See Public Crevier) : Baker V Canada (1999)Document41 pagesRe Residential Tenancies - See Public Crevier) : Baker V Canada (1999)Chamil JanithNo ratings yet

- No Notice SentDocument2 pagesNo Notice SentShannonNo ratings yet

- Acceptance May Be: 1. ActualDocument4 pagesAcceptance May Be: 1. Actualaquanesse21No ratings yet

- Off-Balance Sheet ActivitiesDocument21 pagesOff-Balance Sheet ActivitiesblahblahblueNo ratings yet

- 1 Current Affairs - 1Document133 pages1 Current Affairs - 1madihaNo ratings yet

- Accounts Code K - U - K - 275 PagesDocument277 pagesAccounts Code K - U - K - 275 PagesJayanti KumariNo ratings yet

- Asset Securitisation What Is SecuritisationDocument7 pagesAsset Securitisation What Is SecuritisationVaishali Jhaveri100% (1)

- How To Endorse A Check & What Check Endorsement Means Huntington BankDocument7 pagesHow To Endorse A Check & What Check Endorsement Means Huntington BankJuliana Geraldine Lozano NeiraNo ratings yet

- Form 1041-ES: Pager/XmlDocument7 pagesForm 1041-ES: Pager/XmlMario A. MckinleyNo ratings yet

- WWW - Pakassignment.Blo: Send Your Assignments and Projects To Be Displayed Here As Sample For Others atDocument52 pagesWWW - Pakassignment.Blo: Send Your Assignments and Projects To Be Displayed Here As Sample For Others atPakassignmentNo ratings yet

- Banking Correspondence ToolsDocument35 pagesBanking Correspondence Toolsmanjusha148825% (4)

- Bond Return and ValuationDocument19 pagesBond Return and Valuationoureducation.in100% (2)

- IZE V Experian - DOC 35 - Order On MTDDocument8 pagesIZE V Experian - DOC 35 - Order On MTDKenneth G. EadeNo ratings yet

- Financial Instrument ClassificationDocument43 pagesFinancial Instrument ClassificationShah KamalNo ratings yet

- Ds 10Document5 pagesDs 10Tan Dq100% (1)

- Negotiable Instruments Outline Hughes 2002Document26 pagesNegotiable Instruments Outline Hughes 2002zesrtyryytshrtNo ratings yet

- List of Consumer Reporting Companies: Consumer Financial Protection Bureau - 2021Document38 pagesList of Consumer Reporting Companies: Consumer Financial Protection Bureau - 2021P DiverNo ratings yet

- Asset Securitization and Direct AssignmentDocument3 pagesAsset Securitization and Direct AssignmentDivyanshu RajNo ratings yet

- Special Banking Laws JurisprudenceDocument108 pagesSpecial Banking Laws JurisprudenceJade Ligan EliabNo ratings yet

- Gmail - Experian Credit Report and Credit Score Through INDIALENDSDocument2 pagesGmail - Experian Credit Report and Credit Score Through INDIALENDSAshok PoddarNo ratings yet

- Banking Law Loans and AdvancesDocument35 pagesBanking Law Loans and AdvancesNisha SanoojNo ratings yet

- Ush - Docx. 12345 (1) 0Document82 pagesUsh - Docx. 12345 (1) 0Mohammad MAAZNo ratings yet

- 2 - 1862473 - Salary - Annexure - 6 - 5 - 2021 12 - 46 - 56 AMDocument1 page2 - 1862473 - Salary - Annexure - 6 - 5 - 2021 12 - 46 - 56 AMMohammad MAAZNo ratings yet

- Postpaid Bill 8197545758 BM2229I010262570Document4 pagesPostpaid Bill 8197545758 BM2229I010262570Mohammad MAAZNo ratings yet

- E Brochure Urban Cruiser MobileDocument12 pagesE Brochure Urban Cruiser MobileMohammad MAAZNo ratings yet

- NCP - Culture, Diversity and SocietyDocument2 pagesNCP - Culture, Diversity and SocietyMohammad MAAZNo ratings yet

- Monthly Statement: This Month's SummaryDocument4 pagesMonthly Statement: This Month's SummaryMohammad MAAZNo ratings yet

- Seshadripuram First Grade College: V Sem B.B.A. Elective List - 2020-21Document6 pagesSeshadripuram First Grade College: V Sem B.B.A. Elective List - 2020-21Mohammad MAAZNo ratings yet

- Methods of Estimating InventoryDocument46 pagesMethods of Estimating Inventoryone formanyNo ratings yet

- MB00046274 SS00000076Document1 pageMB00046274 SS00000076scribble_55No ratings yet

- Accounting Principles 12th Edition Weygandt Solutions ManualDocument16 pagesAccounting Principles 12th Edition Weygandt Solutions Manualmalabarhumane088100% (33)

- Slice Pay Case StudyDocument7 pagesSlice Pay Case StudyBhavya KariyanaNo ratings yet

- Larson17ce - PPT - V1 - Ch07 (2023 - 01 - 09 00 - 10 - 56 UTC)Document91 pagesLarson17ce - PPT - V1 - Ch07 (2023 - 01 - 09 00 - 10 - 56 UTC)rbasaiti1No ratings yet

- Error of CorrectionDocument8 pagesError of CorrectionTeo Yu XuanNo ratings yet

- BRS Ca FoundationDocument9 pagesBRS Ca FoundationJunaid Iqbal MastoiNo ratings yet

- Terms and Conditions For Cashback For Airtel Axis Bank Credit CardDocument5 pagesTerms and Conditions For Cashback For Airtel Axis Bank Credit CardVASTU INTACTNo ratings yet

- ForeclosureDocument3 pagesForeclosuremohammadafreed223No ratings yet

- Internet BillDocument4 pagesInternet BillKanchan Asnani0% (1)

- Camacop Stewardship Management: 1. The Local Church Is The Basic Ministry Unit of CAMACOP Administered by TheDocument4 pagesCamacop Stewardship Management: 1. The Local Church Is The Basic Ministry Unit of CAMACOP Administered by TheRIJANE MAE EMPLEONo ratings yet

- Premier Tariff ChargesDocument4 pagesPremier Tariff ChargesvergelNo ratings yet

- Accountancy Notes-Jayakumar SirDocument31 pagesAccountancy Notes-Jayakumar SirSouvik Aich100% (1)

- Tugas Auditing 1 Pertanyaan Dan Soal Diskusi No 14-30 Sampai 14-32 14-30 (Objective 14-5) You Have Been Asked by The Board of Trustees of A Local ChurchDocument4 pagesTugas Auditing 1 Pertanyaan Dan Soal Diskusi No 14-30 Sampai 14-32 14-30 (Objective 14-5) You Have Been Asked by The Board of Trustees of A Local ChurchHusnul KhatimahNo ratings yet

- Aadhaar Update FormDocument4 pagesAadhaar Update FormSumit MeghNo ratings yet

- Key Fact StatementDocument6 pagesKey Fact StatementChoudhary JaatNo ratings yet

- Special Exam-Prelims: Audit of Cash and Cash Equivalents Problem No. 1Document4 pagesSpecial Exam-Prelims: Audit of Cash and Cash Equivalents Problem No. 1Ma Yra YmataNo ratings yet

- Ocbc Business Card Activation Form UpdatedDocument2 pagesOcbc Business Card Activation Form UpdatedWong AngelinaNo ratings yet

- Cash and Accrual BasisDocument4 pagesCash and Accrual BasisBwwwiiiii100% (1)

- Banking 1Document69 pagesBanking 1Shaifali GargNo ratings yet

- Credit Card Approval PredictionDocument14 pagesCredit Card Approval PredictionAyush GuptaNo ratings yet

- ENBD - Infinite Credit Card Acquisition - EDM 2 2Document1 pageENBD - Infinite Credit Card Acquisition - EDM 2 2Syed SajidNo ratings yet

- Financial Management Documentary On Mang InasalDocument209 pagesFinancial Management Documentary On Mang InasalMarla Brigitte Galvan50% (2)

- American International University-Bangladesh (AIUB) Department of Computer Science Software Quality and Testing Fall 2021-2022Document4 pagesAmerican International University-Bangladesh (AIUB) Department of Computer Science Software Quality and Testing Fall 2021-2022Juairah RahmanNo ratings yet

- Internet Bill Format PDFDocument4 pagesInternet Bill Format PDFARUNNo ratings yet

- CP 1 Consolidated Foods DataDocument5 pagesCP 1 Consolidated Foods DataASHUTOSH BISWALNo ratings yet