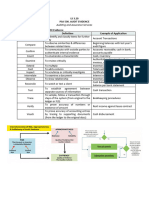

Gathering and Evaluating Audit Evidence: What Is An Audit Procedures?

Gathering and Evaluating Audit Evidence: What Is An Audit Procedures?

You might also like

- M Schemes 02Document3 pagesM Schemes 02Pathmanathan Nadeson22% (9)

- CIS ReportDocument10 pagesCIS ReportMarieNo ratings yet

- Chapter 4 SalosagcolDocument3 pagesChapter 4 SalosagcolElvie Abulencia-BagsicNo ratings yet

- Chapter 4 - Evidential Matter and Its DocumentationDocument14 pagesChapter 4 - Evidential Matter and Its DocumentationKristine WaliNo ratings yet

- At.3204 Nature and Type of Audit EvidenceDocument7 pagesAt.3204 Nature and Type of Audit EvidenceDenny June CraususNo ratings yet

- AT.3404 - Audit Evidence and DocumentationDocument6 pagesAT.3404 - Audit Evidence and DocumentationMonica GarciaNo ratings yet

- Audit Evidence and Audit Documentation Nature and Types Audit EvidenceDocument4 pagesAudit Evidence and Audit Documentation Nature and Types Audit EvidenceCattleyaNo ratings yet

- AT.3004-Nature and Type of Audit Evidence PDFDocument6 pagesAT.3004-Nature and Type of Audit Evidence PDFSean SanchezNo ratings yet

- Audit - Isa 500Document6 pagesAudit - Isa 500Imran AsgharNo ratings yet

- At.106.2 Audit Evidence Gathering My StudentsDocument7 pagesAt.106.2 Audit Evidence Gathering My StudentsLimuel NievoNo ratings yet

- Audit PrelimsDocument10 pagesAudit PrelimsMane NessyNo ratings yet

- Chapter 5 Audit Evidence and DocumentatiDocument54 pagesChapter 5 Audit Evidence and Documentatipadma adrianaNo ratings yet

- Audit Evidence AndTestingDocument15 pagesAudit Evidence AndTestingSigei LeonardNo ratings yet

- AA-Audit EvidenceDocument15 pagesAA-Audit EvidenceRafsan JazzNo ratings yet

- Audit Evidence ReviewerDocument9 pagesAudit Evidence ReviewerJames LopezNo ratings yet

- Audit Procedures: Learning OutcomesDocument5 pagesAudit Procedures: Learning OutcomesKimberly parciaNo ratings yet

- Audit Evidence and Auditing ProceduresDocument64 pagesAudit Evidence and Auditing ProceduresMAAN SHIN ANGNo ratings yet

- Substantive Test VsDocument2 pagesSubstantive Test VsPrincess TolentinoNo ratings yet

- Audit EvidenceDocument2 pagesAudit EvidenceShariful HoqueNo ratings yet

- Audit TechniqueDocument8 pagesAudit TechniqueAllin John FranciscoNo ratings yet

- AT 08 PSA Audit EvidenceDocument7 pagesAT 08 PSA Audit EvidencePrincess Mary Joy LadagaNo ratings yet

- Chapter 2 Audit EvidenceDocument13 pagesChapter 2 Audit EvidencelohitacademyNo ratings yet

- Chapter 12 Audit ProceduresDocument8 pagesChapter 12 Audit ProceduresRichard de LeonNo ratings yet

- Chapter 12 Audit Procedures - ppt179107590Document8 pagesChapter 12 Audit Procedures - ppt179107590Clar Aaron BautistaNo ratings yet

- B3 - Audit EvidenceDocument8 pagesB3 - Audit EvidenceFrank AlexanderNo ratings yet

- Chapter 4 Overview of Audit Process and Preliminary ActivitiesDocument2 pagesChapter 4 Overview of Audit Process and Preliminary ActivitiesNicole Anne Santiago SibuloNo ratings yet

- Unit 5: Audit EvidenceDocument10 pagesUnit 5: Audit EvidenceNigussie BerhanuNo ratings yet

- Audit EvidenceDocument6 pagesAudit Evidencenomanameer324No ratings yet

- Accumulating Audit Evidence GlossaryDocument2 pagesAccumulating Audit Evidence GlossaryGab RielNo ratings yet

- Chapter 5 Audit EvidenceDocument6 pagesChapter 5 Audit EvidencebiyaNo ratings yet

- Notes PSA 500Document5 pagesNotes PSA 500Aang GrandeNo ratings yet

- 4 Audit Objectives, Audit Evidence & Staffing An AuditDocument30 pages4 Audit Objectives, Audit Evidence & Staffing An AuditSiham OsmanNo ratings yet

- Audit Evidence New SlidesDocument20 pagesAudit Evidence New SlidesAdeel AhmadNo ratings yet

- Evidence and Performance of Substantive TestingDocument49 pagesEvidence and Performance of Substantive Testing2019-202518No ratings yet

- PA503 Chapter 6 Audit EvidenceDocument6 pagesPA503 Chapter 6 Audit EvidenceAnonymous rJuerZMVNo ratings yet

- FINANCIAL AUDIT (Final Exam - Portions) : RelevanceDocument5 pagesFINANCIAL AUDIT (Final Exam - Portions) : RelevanceSoniea DianiNo ratings yet

- LS 3.20 - PSA 500 Audit EvidenceDocument3 pagesLS 3.20 - PSA 500 Audit EvidenceSkye LeeNo ratings yet

- Revision Week: Auditing and Assurance 2 21 Mar 2019Document56 pagesRevision Week: Auditing and Assurance 2 21 Mar 2019Fatimah AzzahraNo ratings yet

- Audit Evidence 2Document10 pagesAudit Evidence 2jackrobertodiraNo ratings yet

- Audit ProceduresDocument23 pagesAudit ProceduresJem BalanoNo ratings yet

- Evaluating The Design and Effectiveness of Internal ControlDocument34 pagesEvaluating The Design and Effectiveness of Internal ControlClene DoconteNo ratings yet

- AUD 1.4 Audit Objectives, Procedures, Evidence and Documentation - 2022Document11 pagesAUD 1.4 Audit Objectives, Procedures, Evidence and Documentation - 2022Aimee CuteNo ratings yet

- Chapter 3 General Types of Audit - PPT 123915218Document32 pagesChapter 3 General Types of Audit - PPT 123915218Clar Aaron Bautista100% (2)

- CH14Document8 pagesCH14Joyce Anne GarduqueNo ratings yet

- AU 9 Consideration of ICDocument11 pagesAU 9 Consideration of ICJb MejiaNo ratings yet

- ACCO 30043 Assignment No.5Document7 pagesACCO 30043 Assignment No.5RoseanneNo ratings yet

- AT 07 Audit EvidenceDocument6 pagesAT 07 Audit EvidenceRandy PaderesNo ratings yet

- AUDMOD1 Overview of Auditing and Pre-EngagemeDocument26 pagesAUDMOD1 Overview of Auditing and Pre-EngagemeJohn Archie AntonioNo ratings yet

- Chapter 3 Audit Objectives, Procedures, Evidence, and DocumentationDocument11 pagesChapter 3 Audit Objectives, Procedures, Evidence, and DocumentationSteffany RoqueNo ratings yet

- Audit Evidence and Documentation HandoutsDocument16 pagesAudit Evidence and Documentation Handoutsumar shahzadNo ratings yet

- Module 8 - Substantive Test of Details of AccountsDocument12 pagesModule 8 - Substantive Test of Details of AccountsMark Angelo BustosNo ratings yet

- CA. Saju Sreedhar.K, FCADocument22 pagesCA. Saju Sreedhar.K, FCASimon QuinnyNo ratings yet

- Pertemuan 11 Evidence HDocument17 pagesPertemuan 11 Evidence HAmin NasutionNo ratings yet

- Audit Evidence Procedures and DocumentationDocument46 pagesAudit Evidence Procedures and Documentationbobo kaNo ratings yet

- Chapter 5Document5 pagesChapter 5JakeSiglerNo ratings yet

- ISA Ou NIA 500 Dez 04 Paragrafo 15 e Seguinte Asserc SBJ DFDocument11 pagesISA Ou NIA 500 Dez 04 Paragrafo 15 e Seguinte Asserc SBJ DFeusebio macuacuaNo ratings yet

- Module 1 3 Audi313Document12 pagesModule 1 3 Audi313Katrina PaquizNo ratings yet

- ACAUD 3149 TOPIC 1 Overview of The Audit ProcessDocument2 pagesACAUD 3149 TOPIC 1 Overview of The Audit ProcessCazia Mei JoverNo ratings yet

- MODULE 10 - Evidence Gathering LECTUREDocument7 pagesMODULE 10 - Evidence Gathering LECTURERufina B VerdeNo ratings yet

- Auditevidence 160112060200Document36 pagesAuditevidence 160112060200MahediNo ratings yet

- The Art and Science of Auditing: Principles, Practices, and InsightsFrom EverandThe Art and Science of Auditing: Principles, Practices, and InsightsNo ratings yet

- Detecting Unseen Malicious VBA Macros With NLPTechniquesDocument9 pagesDetecting Unseen Malicious VBA Macros With NLPTechniquesPrakash ChandraNo ratings yet

- HP LaserJet Managed MFP E72425-E72430 - CPMDDocument526 pagesHP LaserJet Managed MFP E72425-E72430 - CPMDDaniel GarciaNo ratings yet

- Instruction Manual: HF TransceiverDocument88 pagesInstruction Manual: HF TransceiverRahadianNo ratings yet

- Moxon Sat AntDocument4 pagesMoxon Sat AntMaureen PegusNo ratings yet

- 50 Most Pervasive Workhorse Words (YouTube)Document1 page50 Most Pervasive Workhorse Words (YouTube)rohit.jarupla100% (1)

- RTN 29.2023 - 2023 Annual AG Show - 2023 April 27 To April 29Document2 pagesRTN 29.2023 - 2023 Annual AG Show - 2023 April 27 To April 29Anonymous UpWci5No ratings yet

- Nicky Aulia Nissa: Resume ObjectiveDocument1 pageNicky Aulia Nissa: Resume ObjectiveNicky Aulia NissaNo ratings yet

- Visible ThinkingDocument4 pagesVisible ThinkinginterianobersabeNo ratings yet

- Industrial Training ReportDocument6 pagesIndustrial Training Reportmayank guptaNo ratings yet

- HZ 01Cpr: Material Safety Data SheetDocument6 pagesHZ 01Cpr: Material Safety Data SheetFakhreddine BousninaNo ratings yet

- Comparative and Superlative AdjectivesDocument5 pagesComparative and Superlative AdjectivesYoussef BrsNo ratings yet

- Chapter 6Document24 pagesChapter 6گل میوہNo ratings yet

- MC Practicals 2Document12 pagesMC Practicals 2Adi AdnanNo ratings yet

- Trends in Food Science & Technology: SciencedirectDocument13 pagesTrends in Food Science & Technology: SciencedirectIlija MileticNo ratings yet

- 如何写一个简短的开场白Document6 pages如何写一个简短的开场白afmojdevnNo ratings yet

- Task Force ProposalDocument8 pagesTask Force ProposalForkLogNo ratings yet

- Assignment - 6 SolutionsDocument7 pagesAssignment - 6 SolutionsGopal Iswarpur Ghosh100% (1)

- One Love Executive Business Plan 4Document62 pagesOne Love Executive Business Plan 4Rocio CarrascalNo ratings yet

- Module 1 (Etymology, Nature and Importance of Communication)Document10 pagesModule 1 (Etymology, Nature and Importance of Communication)jk lavaNo ratings yet

- Pontryagin's Maximum PrincipleDocument21 pagesPontryagin's Maximum PrincipleAhmed TalbiNo ratings yet

- Hindalco ReportDocument42 pagesHindalco ReportAman RoyNo ratings yet

- UPNMG Press Statement-Unemployed Nurses and MidwivesDocument1 pageUPNMG Press Statement-Unemployed Nurses and MidwivesClavia NyaabaNo ratings yet

- ATR72 Freighter VersionDocument6 pagesATR72 Freighter Versiontomay777No ratings yet

- Collection Development and Acquisition in ASIAN ACADEMIC LIBRARIES: Some Current IssuesDocument8 pagesCollection Development and Acquisition in ASIAN ACADEMIC LIBRARIES: Some Current IssuesKrish ViliranNo ratings yet

- Take Away Material SYFC - September 2022Document11 pagesTake Away Material SYFC - September 2022Akun TumbalNo ratings yet

- SR Designworks: Head OfficeDocument15 pagesSR Designworks: Head Officeihameed4100% (1)

- 5S (Methodology) : 5S Is The Name of A Workplace Organization Methodology That Uses A List of FiveDocument3 pages5S (Methodology) : 5S Is The Name of A Workplace Organization Methodology That Uses A List of FiveRoberto DiyNo ratings yet

- HARVARD Referencing Made EasyDocument1 pageHARVARD Referencing Made EasyMediaMassageNo ratings yet

- Product 043 UMDocument31 pagesProduct 043 UMPankaj MauryaNo ratings yet

Download as pdf or txt

You might also like

- M Schemes 02Document3 pagesM Schemes 02Pathmanathan Nadeson22% (9)

- CIS ReportDocument10 pagesCIS ReportMarieNo ratings yet

- Chapter 4 SalosagcolDocument3 pagesChapter 4 SalosagcolElvie Abulencia-BagsicNo ratings yet

- Chapter 4 - Evidential Matter and Its DocumentationDocument14 pagesChapter 4 - Evidential Matter and Its DocumentationKristine WaliNo ratings yet

- At.3204 Nature and Type of Audit EvidenceDocument7 pagesAt.3204 Nature and Type of Audit EvidenceDenny June CraususNo ratings yet

- AT.3404 - Audit Evidence and DocumentationDocument6 pagesAT.3404 - Audit Evidence and DocumentationMonica GarciaNo ratings yet

- Audit Evidence and Audit Documentation Nature and Types Audit EvidenceDocument4 pagesAudit Evidence and Audit Documentation Nature and Types Audit EvidenceCattleyaNo ratings yet

- AT.3004-Nature and Type of Audit Evidence PDFDocument6 pagesAT.3004-Nature and Type of Audit Evidence PDFSean SanchezNo ratings yet

- Audit - Isa 500Document6 pagesAudit - Isa 500Imran AsgharNo ratings yet

- At.106.2 Audit Evidence Gathering My StudentsDocument7 pagesAt.106.2 Audit Evidence Gathering My StudentsLimuel NievoNo ratings yet

- Audit PrelimsDocument10 pagesAudit PrelimsMane NessyNo ratings yet

- Chapter 5 Audit Evidence and DocumentatiDocument54 pagesChapter 5 Audit Evidence and Documentatipadma adrianaNo ratings yet

- Audit Evidence AndTestingDocument15 pagesAudit Evidence AndTestingSigei LeonardNo ratings yet

- AA-Audit EvidenceDocument15 pagesAA-Audit EvidenceRafsan JazzNo ratings yet

- Audit Evidence ReviewerDocument9 pagesAudit Evidence ReviewerJames LopezNo ratings yet

- Audit Procedures: Learning OutcomesDocument5 pagesAudit Procedures: Learning OutcomesKimberly parciaNo ratings yet

- Audit Evidence and Auditing ProceduresDocument64 pagesAudit Evidence and Auditing ProceduresMAAN SHIN ANGNo ratings yet

- Substantive Test VsDocument2 pagesSubstantive Test VsPrincess TolentinoNo ratings yet

- Audit EvidenceDocument2 pagesAudit EvidenceShariful HoqueNo ratings yet

- Audit TechniqueDocument8 pagesAudit TechniqueAllin John FranciscoNo ratings yet

- AT 08 PSA Audit EvidenceDocument7 pagesAT 08 PSA Audit EvidencePrincess Mary Joy LadagaNo ratings yet

- Chapter 2 Audit EvidenceDocument13 pagesChapter 2 Audit EvidencelohitacademyNo ratings yet

- Chapter 12 Audit ProceduresDocument8 pagesChapter 12 Audit ProceduresRichard de LeonNo ratings yet

- Chapter 12 Audit Procedures - ppt179107590Document8 pagesChapter 12 Audit Procedures - ppt179107590Clar Aaron BautistaNo ratings yet

- B3 - Audit EvidenceDocument8 pagesB3 - Audit EvidenceFrank AlexanderNo ratings yet

- Chapter 4 Overview of Audit Process and Preliminary ActivitiesDocument2 pagesChapter 4 Overview of Audit Process and Preliminary ActivitiesNicole Anne Santiago SibuloNo ratings yet

- Unit 5: Audit EvidenceDocument10 pagesUnit 5: Audit EvidenceNigussie BerhanuNo ratings yet

- Audit EvidenceDocument6 pagesAudit Evidencenomanameer324No ratings yet

- Accumulating Audit Evidence GlossaryDocument2 pagesAccumulating Audit Evidence GlossaryGab RielNo ratings yet

- Chapter 5 Audit EvidenceDocument6 pagesChapter 5 Audit EvidencebiyaNo ratings yet

- Notes PSA 500Document5 pagesNotes PSA 500Aang GrandeNo ratings yet

- 4 Audit Objectives, Audit Evidence & Staffing An AuditDocument30 pages4 Audit Objectives, Audit Evidence & Staffing An AuditSiham OsmanNo ratings yet

- Audit Evidence New SlidesDocument20 pagesAudit Evidence New SlidesAdeel AhmadNo ratings yet

- Evidence and Performance of Substantive TestingDocument49 pagesEvidence and Performance of Substantive Testing2019-202518No ratings yet

- PA503 Chapter 6 Audit EvidenceDocument6 pagesPA503 Chapter 6 Audit EvidenceAnonymous rJuerZMVNo ratings yet

- FINANCIAL AUDIT (Final Exam - Portions) : RelevanceDocument5 pagesFINANCIAL AUDIT (Final Exam - Portions) : RelevanceSoniea DianiNo ratings yet

- LS 3.20 - PSA 500 Audit EvidenceDocument3 pagesLS 3.20 - PSA 500 Audit EvidenceSkye LeeNo ratings yet

- Revision Week: Auditing and Assurance 2 21 Mar 2019Document56 pagesRevision Week: Auditing and Assurance 2 21 Mar 2019Fatimah AzzahraNo ratings yet

- Audit Evidence 2Document10 pagesAudit Evidence 2jackrobertodiraNo ratings yet

- Audit ProceduresDocument23 pagesAudit ProceduresJem BalanoNo ratings yet

- Evaluating The Design and Effectiveness of Internal ControlDocument34 pagesEvaluating The Design and Effectiveness of Internal ControlClene DoconteNo ratings yet

- AUD 1.4 Audit Objectives, Procedures, Evidence and Documentation - 2022Document11 pagesAUD 1.4 Audit Objectives, Procedures, Evidence and Documentation - 2022Aimee CuteNo ratings yet

- Chapter 3 General Types of Audit - PPT 123915218Document32 pagesChapter 3 General Types of Audit - PPT 123915218Clar Aaron Bautista100% (2)

- CH14Document8 pagesCH14Joyce Anne GarduqueNo ratings yet

- AU 9 Consideration of ICDocument11 pagesAU 9 Consideration of ICJb MejiaNo ratings yet

- ACCO 30043 Assignment No.5Document7 pagesACCO 30043 Assignment No.5RoseanneNo ratings yet

- AT 07 Audit EvidenceDocument6 pagesAT 07 Audit EvidenceRandy PaderesNo ratings yet

- AUDMOD1 Overview of Auditing and Pre-EngagemeDocument26 pagesAUDMOD1 Overview of Auditing and Pre-EngagemeJohn Archie AntonioNo ratings yet

- Chapter 3 Audit Objectives, Procedures, Evidence, and DocumentationDocument11 pagesChapter 3 Audit Objectives, Procedures, Evidence, and DocumentationSteffany RoqueNo ratings yet

- Audit Evidence and Documentation HandoutsDocument16 pagesAudit Evidence and Documentation Handoutsumar shahzadNo ratings yet

- Module 8 - Substantive Test of Details of AccountsDocument12 pagesModule 8 - Substantive Test of Details of AccountsMark Angelo BustosNo ratings yet

- CA. Saju Sreedhar.K, FCADocument22 pagesCA. Saju Sreedhar.K, FCASimon QuinnyNo ratings yet

- Pertemuan 11 Evidence HDocument17 pagesPertemuan 11 Evidence HAmin NasutionNo ratings yet

- Audit Evidence Procedures and DocumentationDocument46 pagesAudit Evidence Procedures and Documentationbobo kaNo ratings yet

- Chapter 5Document5 pagesChapter 5JakeSiglerNo ratings yet

- ISA Ou NIA 500 Dez 04 Paragrafo 15 e Seguinte Asserc SBJ DFDocument11 pagesISA Ou NIA 500 Dez 04 Paragrafo 15 e Seguinte Asserc SBJ DFeusebio macuacuaNo ratings yet

- Module 1 3 Audi313Document12 pagesModule 1 3 Audi313Katrina PaquizNo ratings yet

- ACAUD 3149 TOPIC 1 Overview of The Audit ProcessDocument2 pagesACAUD 3149 TOPIC 1 Overview of The Audit ProcessCazia Mei JoverNo ratings yet

- MODULE 10 - Evidence Gathering LECTUREDocument7 pagesMODULE 10 - Evidence Gathering LECTURERufina B VerdeNo ratings yet

- Auditevidence 160112060200Document36 pagesAuditevidence 160112060200MahediNo ratings yet

- The Art and Science of Auditing: Principles, Practices, and InsightsFrom EverandThe Art and Science of Auditing: Principles, Practices, and InsightsNo ratings yet

- Detecting Unseen Malicious VBA Macros With NLPTechniquesDocument9 pagesDetecting Unseen Malicious VBA Macros With NLPTechniquesPrakash ChandraNo ratings yet

- HP LaserJet Managed MFP E72425-E72430 - CPMDDocument526 pagesHP LaserJet Managed MFP E72425-E72430 - CPMDDaniel GarciaNo ratings yet

- Instruction Manual: HF TransceiverDocument88 pagesInstruction Manual: HF TransceiverRahadianNo ratings yet

- Moxon Sat AntDocument4 pagesMoxon Sat AntMaureen PegusNo ratings yet

- 50 Most Pervasive Workhorse Words (YouTube)Document1 page50 Most Pervasive Workhorse Words (YouTube)rohit.jarupla100% (1)

- RTN 29.2023 - 2023 Annual AG Show - 2023 April 27 To April 29Document2 pagesRTN 29.2023 - 2023 Annual AG Show - 2023 April 27 To April 29Anonymous UpWci5No ratings yet

- Nicky Aulia Nissa: Resume ObjectiveDocument1 pageNicky Aulia Nissa: Resume ObjectiveNicky Aulia NissaNo ratings yet

- Visible ThinkingDocument4 pagesVisible ThinkinginterianobersabeNo ratings yet

- Industrial Training ReportDocument6 pagesIndustrial Training Reportmayank guptaNo ratings yet

- HZ 01Cpr: Material Safety Data SheetDocument6 pagesHZ 01Cpr: Material Safety Data SheetFakhreddine BousninaNo ratings yet

- Comparative and Superlative AdjectivesDocument5 pagesComparative and Superlative AdjectivesYoussef BrsNo ratings yet

- Chapter 6Document24 pagesChapter 6گل میوہNo ratings yet

- MC Practicals 2Document12 pagesMC Practicals 2Adi AdnanNo ratings yet

- Trends in Food Science & Technology: SciencedirectDocument13 pagesTrends in Food Science & Technology: SciencedirectIlija MileticNo ratings yet

- 如何写一个简短的开场白Document6 pages如何写一个简短的开场白afmojdevnNo ratings yet

- Task Force ProposalDocument8 pagesTask Force ProposalForkLogNo ratings yet

- Assignment - 6 SolutionsDocument7 pagesAssignment - 6 SolutionsGopal Iswarpur Ghosh100% (1)

- One Love Executive Business Plan 4Document62 pagesOne Love Executive Business Plan 4Rocio CarrascalNo ratings yet

- Module 1 (Etymology, Nature and Importance of Communication)Document10 pagesModule 1 (Etymology, Nature and Importance of Communication)jk lavaNo ratings yet

- Pontryagin's Maximum PrincipleDocument21 pagesPontryagin's Maximum PrincipleAhmed TalbiNo ratings yet

- Hindalco ReportDocument42 pagesHindalco ReportAman RoyNo ratings yet

- UPNMG Press Statement-Unemployed Nurses and MidwivesDocument1 pageUPNMG Press Statement-Unemployed Nurses and MidwivesClavia NyaabaNo ratings yet

- ATR72 Freighter VersionDocument6 pagesATR72 Freighter Versiontomay777No ratings yet

- Collection Development and Acquisition in ASIAN ACADEMIC LIBRARIES: Some Current IssuesDocument8 pagesCollection Development and Acquisition in ASIAN ACADEMIC LIBRARIES: Some Current IssuesKrish ViliranNo ratings yet

- Take Away Material SYFC - September 2022Document11 pagesTake Away Material SYFC - September 2022Akun TumbalNo ratings yet

- SR Designworks: Head OfficeDocument15 pagesSR Designworks: Head Officeihameed4100% (1)

- 5S (Methodology) : 5S Is The Name of A Workplace Organization Methodology That Uses A List of FiveDocument3 pages5S (Methodology) : 5S Is The Name of A Workplace Organization Methodology That Uses A List of FiveRoberto DiyNo ratings yet

- HARVARD Referencing Made EasyDocument1 pageHARVARD Referencing Made EasyMediaMassageNo ratings yet

- Product 043 UMDocument31 pagesProduct 043 UMPankaj MauryaNo ratings yet