Download as docx, pdf, or txt

You might also like

- Wine IndustryDocument16 pagesWine IndustryHean Lee Kang50% (2)

- Adolph Coors in The Brewing IndustryDocument2 pagesAdolph Coors in The Brewing Industrysamadabbas00275% (4)

- Adolph Coors in The Brewing IndustryDocument12 pagesAdolph Coors in The Brewing Industryzchanna100% (3)

- Heineken Case StudyDocument31 pagesHeineken Case StudyNitesh-sa100% (2)

- Beer Industry 5 ForcesDocument4 pagesBeer Industry 5 ForcesmheeisnotabearNo ratings yet

- Mondavi Case StudyDocument3 pagesMondavi Case StudysroghenNo ratings yet

- Sample E - Response - Wine-Label PDFDocument3 pagesSample E - Response - Wine-Label PDFAaryan ShroffNo ratings yet

- Sandland Vineyards - DivB - Group 3Document5 pagesSandland Vineyards - DivB - Group 3Numair Shirqhi MohammedNo ratings yet

- Strongbow InternationalizationDocument22 pagesStrongbow InternationalizationXuân NguyễnNo ratings yet

- Group Case AnalysisDocument4 pagesGroup Case AnalysisHannah Jean86% (7)

- Mondavi Case StudyDocument5 pagesMondavi Case StudyAmol JavahireNo ratings yet

- Porter's Five ForcesDocument9 pagesPorter's Five Forcesmark alcantaraNo ratings yet

- Global Forces and The Western European Brewing IndustryDocument5 pagesGlobal Forces and The Western European Brewing IndustryHushnak AliNo ratings yet

- Store Wars: The Worldwide Battle for Mindspace and Shelfspace, Online and In-storeFrom EverandStore Wars: The Worldwide Battle for Mindspace and Shelfspace, Online and In-storeNo ratings yet

- Lla006 General Equipment ListsDocument28 pagesLla006 General Equipment ListsJon NicholNo ratings yet

- Assignment 1 (Porter's Industry Analysis) - Aayush ChoudharyDocument2 pagesAssignment 1 (Porter's Industry Analysis) - Aayush ChoudharyAayush ChoudharyNo ratings yet

- Case 2 - Lagunitas Brewing - RianaDocument3 pagesCase 2 - Lagunitas Brewing - RianaRiana RusdiantoNo ratings yet

- MondaviDocument3 pagesMondaviritu_wadhwa0079769No ratings yet

- Strategic Marketing Assignment: Kingfisher BeerDocument8 pagesStrategic Marketing Assignment: Kingfisher BeerSharthak Shankar Bhagat100% (1)

- Global Wine Industry Case StudyDocument10 pagesGlobal Wine Industry Case Studywasifq100% (1)

- Coors Industry 3Document9 pagesCoors Industry 3Thilina Rupasinghe100% (1)

- Wine IndustryDocument16 pagesWine IndustryTiberiu FalibogaNo ratings yet

- Porter 5Document4 pagesPorter 5'Sånjîdå KåBîr'No ratings yet

- Porter AnalysisDocument6 pagesPorter AnalysisSahil0111No ratings yet

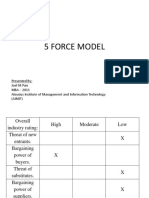

- 5 Force Model: Presented By: Joel M Pais MBA - 2011 Aloysius Institute of Management and Information Technology (Aimit)Document6 pages5 Force Model: Presented By: Joel M Pais MBA - 2011 Aloysius Institute of Management and Information Technology (Aimit)Sdsm 719No ratings yet

- Wine Industry Market PlanDocument14 pagesWine Industry Market PlanWashif AnwarNo ratings yet

- Beer Industry 5 Forces - NasoDocument4 pagesBeer Industry 5 Forces - NasoShi JieNo ratings yet

- Indian Wine Industry Analysis - FinalDocument4 pagesIndian Wine Industry Analysis - FinalShaifali DixitNo ratings yet

- US Beer Market - Group 2 FinalDocument11 pagesUS Beer Market - Group 2 FinalFrancisco Trigueiros100% (1)

- The Book and The Authors: Prof Renee Mauborgne Prof Chan KimDocument18 pagesThe Book and The Authors: Prof Renee Mauborgne Prof Chan KimKarthik GowdaNo ratings yet

- Case Study BREWERYDocument4 pagesCase Study BREWERYCharlotte Lemaire0% (1)

- Poters Five ForcesDocument4 pagesPoters Five ForcesSanam AdvaniNo ratings yet

- Mide TermDocument2 pagesMide Termmichalis72No ratings yet

- Adolph Coors (1) Group 1Document8 pagesAdolph Coors (1) Group 1HaroonNasirNo ratings yet

- Strongbow InternationalizationDocument22 pagesStrongbow InternationalizationXuân NguyễnNo ratings yet

- Competition in The Craft Beer Industry in 2016Document5 pagesCompetition in The Craft Beer Industry in 2016Keka SamNo ratings yet

- Minimum Efficient Scale of Production-Has Steadily Increased. This Resulted To A RadicalDocument3 pagesMinimum Efficient Scale of Production-Has Steadily Increased. This Resulted To A RadicalLuhenNo ratings yet

- Crafting Winning Strategies in A Mature Market: The US Wine Industry in 2001Document12 pagesCrafting Winning Strategies in A Mature Market: The US Wine Industry in 2001Devika NarulaNo ratings yet

- Micro Analysis of Soft-Drink Industry 2008Document5 pagesMicro Analysis of Soft-Drink Industry 2008Tom Jacob100% (1)

- Beer Co Wine Market CaseDocument12 pagesBeer Co Wine Market Caseafeubo ioafsNo ratings yet

- Lagunitas CaseDocument10 pagesLagunitas CaseAntoine SionNo ratings yet

- Fair Trade GroundsforcomplaintDocument12 pagesFair Trade GroundsforcomplaintRyan HayesNo ratings yet

- Minimum Efficient Scale of Production Has Steadily Increased. This Resulted To A RadicalDocument2 pagesMinimum Efficient Scale of Production Has Steadily Increased. This Resulted To A RadicalJoicy ToppoNo ratings yet

- 2011 Performing A Competitor Analysis For Wine in DenmarkDocument5 pages2011 Performing A Competitor Analysis For Wine in DenmarkNovia LieNo ratings yet

- Session 2 - ClassDocument54 pagesSession 2 - ClassSrijan SharmaNo ratings yet

- KingfisherDocument8 pagesKingfisherRaunak GuptaNo ratings yet

- To The CustomersDocument31 pagesTo The CustomersSaranyaelangovan MargaretNo ratings yet

- The Global Alcohol Industry: Daniel O'Leary - 1469525Document16 pagesThe Global Alcohol Industry: Daniel O'Leary - 1469525doleary1109No ratings yet

- DiageoDocument31 pagesDiageoVarun AmritwarNo ratings yet

- The United States Beer IndustryDocument2 pagesThe United States Beer IndustryMarfie SwanNo ratings yet

- Part 2Document5 pagesPart 2vi viNo ratings yet

- Microbrewery Industry Analysis ScanningDocument5 pagesMicrobrewery Industry Analysis ScanningYayaakshi ShokeenNo ratings yet

- IAA - Potato Chips - ML, DQ, TCDocument15 pagesIAA - Potato Chips - ML, DQ, TCAnjali TvmNo ratings yet

- Case 3Document2 pagesCase 3lorinetixierNo ratings yet

- Carrefour Final PresentationDocument52 pagesCarrefour Final PresentationImteeaz Goolamhossen100% (2)

- Part I: Analysis of Case 5Document10 pagesPart I: Analysis of Case 5Pedro SoldadoNo ratings yet

- 2 French StratDocument12 pages2 French StratNedved NedvedNo ratings yet

- Trading Up (Review and Analysis of Silverstein and Fiske's Book)From EverandTrading Up (Review and Analysis of Silverstein and Fiske's Book)No ratings yet

- Solar Powered Agro Industrial Project of Cassava Based Bioethanol Processing UnitFrom EverandSolar Powered Agro Industrial Project of Cassava Based Bioethanol Processing UnitNo ratings yet

- Sugar Consumption in MalaysiaDocument14 pagesSugar Consumption in MalaysiaShi Yen50% (2)

- Internship ReportDocument99 pagesInternship ReportShubham TyagiNo ratings yet

- Literary Analysis Cathedral Final DraftDocument5 pagesLiterary Analysis Cathedral Final Draftapi-457013524No ratings yet

- 1Document2 pages1chantal desireeNo ratings yet

- 38 Foods That Contain Almost Zero CaloriesDocument6 pages38 Foods That Contain Almost Zero CaloriesMS GAMERZNo ratings yet

- Tipulo Packages (NEW)Document6 pagesTipulo Packages (NEW)Wilfredo PineroNo ratings yet

- SpecDocument23 pagesSpecZuhaib NasirNo ratings yet

- DISTILLERIA WASHINGTON V CADocument2 pagesDISTILLERIA WASHINGTON V CAJake Castañeda100% (1)

- The Bah Bar Opening and Closing Check ListsDocument4 pagesThe Bah Bar Opening and Closing Check ListsbarmanagerNo ratings yet

- Teabag Process TestDocument5 pagesTeabag Process TestJonny LizardiNo ratings yet

- Research Paper? PDFDocument15 pagesResearch Paper? PDFChriscia Myle Rosales GegantoNo ratings yet

- PDF 20221016 202706 0000Document53 pagesPDF 20221016 202706 0000CA Manoj Kumar SabatNo ratings yet

- Chapter 1beverage Service IndustryDocument14 pagesChapter 1beverage Service IndustryZyNo ratings yet

- Alcoholic Beverage Eg MRDocument8 pagesAlcoholic Beverage Eg MRPSYCHO RockstarNo ratings yet

- Baqueta2019 JFS SensorialDocument10 pagesBaqueta2019 JFS SensorialTanChantreaNo ratings yet

- The Lighthouse BistroDocument3 pagesThe Lighthouse Bistroapi-359496549No ratings yet

- Grand Casino Hotel & Resort Catering MenuDocument22 pagesGrand Casino Hotel & Resort Catering MenunokiarishNo ratings yet

- Hydration MattersDocument2 pagesHydration Mattersknoxacademy100% (1)

- The Ability of Yeast To Ferment Different Sugars: Fermentation Lab ReportDocument5 pagesThe Ability of Yeast To Ferment Different Sugars: Fermentation Lab ReportIan MullenNo ratings yet

- Final Demo Semi DetailedDocument2 pagesFinal Demo Semi DetailedMocha FrappuccinoNo ratings yet

- Mead Hall CommunityDocument15 pagesMead Hall CommunityClyde RexNo ratings yet

- HalEeb MArKeTiNgDocument65 pagesHalEeb MArKeTiNglovelove50500% (1)

- Group 1 Chapter 1-4 ABM ADocument24 pagesGroup 1 Chapter 1-4 ABM AAlissa MayNo ratings yet

- How Does Drinking Coffee Everyday Affect Your BodyDocument6 pagesHow Does Drinking Coffee Everyday Affect Your BodyShanza qureshiNo ratings yet

- Ek0230 Seadxb y 47CDocument2 pagesEk0230 Seadxb y 47CAdinarayana RaoNo ratings yet

- An Overview of CocaDocument14 pagesAn Overview of CocaantorNo ratings yet

- Paul Manning, Waters, June 2008Document95 pagesPaul Manning, Waters, June 2008nana_kipianiNo ratings yet

- Workbook 9&10Document27 pagesWorkbook 9&10Andrea PrietoNo ratings yet