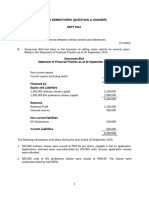

Balance Sheet As On 31/12/2016 (Balance Sheet After Reconstruction)

Balance Sheet As On 31/12/2016 (Balance Sheet After Reconstruction)

You might also like

- AP Receivables Quizzer507docDocument20 pagesAP Receivables Quizzer507docMa Yra YmataNo ratings yet

- Your Transunion Credit Report: Personal InformationDocument164 pagesYour Transunion Credit Report: Personal InformationRichard Griffin0% (1)

- Internal Reconstruction - HomeworkDocument25 pagesInternal Reconstruction - HomeworkYash ShewaleNo ratings yet

- Suggested Answer CAP II December 2016Document88 pagesSuggested Answer CAP II December 2016Nirmal ShresthaNo ratings yet

- Caa Assignment SolutionsDocument39 pagesCaa Assignment Solutionschikanesakshi2001No ratings yet

- Accountancy MSDocument11 pagesAccountancy MSmansoorbariNo ratings yet

- Accountancy-MS 23-24Document10 pagesAccountancy-MS 23-24Ashutosh SinghNo ratings yet

- Bv2018 Revised Conceptual FrameworkDocument18 pagesBv2018 Revised Conceptual FrameworkTeneswari RadhaNo ratings yet

- Internal ReconsrtuctionDocument33 pagesInternal ReconsrtuctionRenuNo ratings yet

- Marking SchemeDocument6 pagesMarking Schemeraghu monnappaNo ratings yet

- Accountancy 2023-24 MSDocument11 pagesAccountancy 2023-24 MSirfanoushad15No ratings yet

- Cbse cl12 Ead Accountancy Answers To Sample Paper 6Document15 pagesCbse cl12 Ead Accountancy Answers To Sample Paper 6amaankhan828768No ratings yet

- QUESTION PAPER 1 (Solution) : Q.1 A) Multiple Choice QuestionsDocument13 pagesQUESTION PAPER 1 (Solution) : Q.1 A) Multiple Choice QuestionsSiddharth VoraNo ratings yet

- Capital Reduction 2Document6 pagesCapital Reduction 2SANJIB SHARMANo ratings yet

- Pe2 Acc Nov05Document19 pagesPe2 Acc Nov05api-3825774No ratings yet

- Int Reconstruction 2019 Old-1Document14 pagesInt Reconstruction 2019 Old-1H122 Pallabi MukherjeeNo ratings yet

- Valuation of GoodwillDocument3 pagesValuation of GoodwillAhiaanNo ratings yet

- MS - Accountancy - 12-Practice Paper-1Document7 pagesMS - Accountancy - 12-Practice Paper-1Arun kumarNo ratings yet

- MS Xii Accountancy Set 1Document10 pagesMS Xii Accountancy Set 1arikoff07No ratings yet

- Marking Scheme Mock Test I 2023 24Document9 pagesMarking Scheme Mock Test I 2023 24HARSH CHAURASIYANo ratings yet

- QUESTION PAPER 36195 (Solution)Document17 pagesQUESTION PAPER 36195 (Solution)Faizu KhamNo ratings yet

- Internal ReconstructionDocument26 pagesInternal ReconstructionRajesh NangaliaNo ratings yet

- Answer Key 3Document8 pagesAnswer Key 3Hari prakarsh NimiNo ratings yet

- XII ACCOUNTANCY SET-2 Marking Scheme Ist Pre Board 2023-24-1Document9 pagesXII ACCOUNTANCY SET-2 Marking Scheme Ist Pre Board 2023-24-1Riddhima Murarka50% (2)

- Problem and Solutions: March, 2019Document2 pagesProblem and Solutions: March, 2019Pulkit SamratNo ratings yet

- 616806cf0cf2b988fbcdbd97 OriginalDocument20 pages616806cf0cf2b988fbcdbd97 OriginalTM GamingNo ratings yet

- CBSE Accountancy 12th Term 2 CH 3Document5 pagesCBSE Accountancy 12th Term 2 CH 3AadasNo ratings yet

- Corporate AccountingDocument93 pagesCorporate AccountingKalp JainNo ratings yet

- Practice Paper Pre-Board Xii Acc 2023-24Document13 pagesPractice Paper Pre-Board Xii Acc 2023-24Pratiksha Suryavanshi100% (1)

- 19013comp Sugans Pe2 Accounting Cp8 5Document12 pages19013comp Sugans Pe2 Accounting Cp8 5Ubaidulla MachingalNo ratings yet

- CA Inter Accounts A MTP 1 Nov 2022Document13 pagesCA Inter Accounts A MTP 1 Nov 2022smartshivenduNo ratings yet

- C.S. Executive - Answers For CC Test Paper - IDocument7 pagesC.S. Executive - Answers For CC Test Paper - Isekhar_gantiNo ratings yet

- 17269pe2 Sugg June09 1 PDFDocument22 pages17269pe2 Sugg June09 1 PDFSahil GoyalNo ratings yet

- Internal Reconstruction - ProblemsDocument8 pagesInternal Reconstruction - ProblemsNaomi SaldanhaNo ratings yet

- Sept 2014 - 230716 - 233727Document22 pagesSept 2014 - 230716 - 233727mohddanialhanaffimustaffiNo ratings yet

- Accounting Redemption of Debentures 1642416359Document19 pagesAccounting Redemption of Debentures 1642416359Shashank SikarwarNo ratings yet

- Set - 1 Acc MS PB12023-24Document10 pagesSet - 1 Acc MS PB12023-24aamiralishiasbackup1No ratings yet

- 5.cpbe - Xii Accts - MSDocument18 pages5.cpbe - Xii Accts - MScommerce12onlineclassesNo ratings yet

- XII Acc SQP 1 (AP 23-24)Document11 pagesXII Acc SQP 1 (AP 23-24)Vaidehi BagraNo ratings yet

- June 2019 All Paper SuggestedDocument120 pagesJune 2019 All Paper SuggestedEdtech NepalNo ratings yet

- CBSE Sample Paper 2024 Class 12 Accountancy MSDocument11 pagesCBSE Sample Paper 2024 Class 12 Accountancy MSskhushbusahniNo ratings yet

- CR Assignemt Unit 3Document25 pagesCR Assignemt Unit 3Calida SoaresNo ratings yet

- Answer Key - 1 TermDocument9 pagesAnswer Key - 1 TermsamayaksahuNo ratings yet

- Final Accounts 1. As Per Schedule III of Companies Act 2013, Prepare Financial Statement For Gillette India PVT LTDDocument3 pagesFinal Accounts 1. As Per Schedule III of Companies Act 2013, Prepare Financial Statement For Gillette India PVT LTDermiasNo ratings yet

- 12 Accountancy Comp Delhi2017 1Document28 pages12 Accountancy Comp Delhi2017 1harshit agrawalNo ratings yet

- Adobe Scan Jan 30, 2023Document6 pagesAdobe Scan Jan 30, 2023Karan RajakNo ratings yet

- CBCS BCOM GENERAL Sem-5 COMMERCE DSE-5.2-A CORPORATE-ACCOUNTING-10988Document12 pagesCBCS BCOM GENERAL Sem-5 COMMERCE DSE-5.2-A CORPORATE-ACCOUNTING-10988Sayantan DebnathNo ratings yet

- Ratio Analysis Ex 1Document2 pagesRatio Analysis Ex 1dZOAVIT GamingNo ratings yet

- Accountancy - Additional Questions MARKING SCHEMEDocument15 pagesAccountancy - Additional Questions MARKING SCHEMEseema chadhaNo ratings yet

- Assignment 2 Bus ComDocument22 pagesAssignment 2 Bus ComFaithful FighterNo ratings yet

- Internal Reconstruction PQ SolDocument17 pagesInternal Reconstruction PQ SolKaran MokhaNo ratings yet

- Adv Acc - 3 CHDocument21 pagesAdv Acc - 3 CHhassan nassereddineNo ratings yet

- Set - 3 Acc MSDocument6 pagesSet - 3 Acc MSaamiralishiasbackup1No ratings yet

- 5 6084915055709651012Document8 pages5 6084915055709651012Ajit Yadav100% (1)

- Accountancy Term-2 MVP 2023-24Document7 pagesAccountancy Term-2 MVP 2023-24Cp GpNo ratings yet

- Test Your Knowledge - 7Document2 pagesTest Your Knowledge - 7narangdiya602No ratings yet

- CE On Quasi-ReorganizationDocument1 pageCE On Quasi-ReorganizationalyssaNo ratings yet

- Question Papers: SEM. - (JULY 2023)Document8 pagesQuestion Papers: SEM. - (JULY 2023)arpitgupta20050No ratings yet

- 6.XII Accountancy Marking SchemeDocument10 pages6.XII Accountancy Marking Schemecommerce12onlineclassesNo ratings yet

- Isc Mock 2Document14 pagesIsc Mock 2anshikajain3474No ratings yet

- 2023 24 Xii Pre Board 1 MsDocument13 pages2023 24 Xii Pre Board 1 MsacguptaclassesNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- The Accounting Process Involves in Recording: A)Document28 pagesThe Accounting Process Involves in Recording: A)Shubham Saurav SSNo ratings yet

- RMOE FormatDocument2 pagesRMOE FormatVivekanand VaradarajanNo ratings yet

- Z Transforms WorksheetsDocument4 pagesZ Transforms Worksheetspilas_nikolaNo ratings yet

- Chapter 3 - Bonds Payable Other ConceptsDocument29 pagesChapter 3 - Bonds Payable Other ConceptsJEFFERSON CUTENo ratings yet

- Case Laws On Personal & Corporate Guarantors Under IBCDocument6 pagesCase Laws On Personal & Corporate Guarantors Under IBClaxmiNo ratings yet

- Topic 4 AnnuityDocument22 pagesTopic 4 AnnuityNanteni GanesanNo ratings yet

- Debt Collector Disclosure StatementDocument8 pagesDebt Collector Disclosure StatementGreg WilderNo ratings yet

- ST FinancingDocument30 pagesST FinancingJeyavikinesh SelvakkuganNo ratings yet

- Foreclosing On Nothing, Dale WhitmanDocument51 pagesForeclosing On Nothing, Dale WhitmanMarie McDonnellNo ratings yet

- Credit Structuring Model - COMPLETEDDocument9 pagesCredit Structuring Model - COMPLETEDfisehaNo ratings yet

- SALPL AgreementDocument30 pagesSALPL AgreementVipul JainNo ratings yet

- Paper 3 1 1Document7 pagesPaper 3 1 1api-593075882No ratings yet

- Customer Education IRACDocument3 pagesCustomer Education IRACHridya SNo ratings yet

- Siva RDocument17 pagesSiva RsidvikventuresNo ratings yet

- Individual Facility AgreementDocument66 pagesIndividual Facility AgreementDY KIM (INKO)No ratings yet

- 1.6 Accounting EquationDocument8 pages1.6 Accounting EquationAbijit GudaNo ratings yet

- Wa0004.Document7 pagesWa0004.viphainhumNo ratings yet

- MULTIPLE CHOICES-answer KeyDocument7 pagesMULTIPLE CHOICES-answer KeyLiaNo ratings yet

- Chapter 1Document24 pagesChapter 1Jhopel Casagnap EmanNo ratings yet

- David MccormickDocument20 pagesDavid MccormickAnonymous vRG3cFNjANo ratings yet

- Portofilo Quality and Delinquency ManagementDocument15 pagesPortofilo Quality and Delinquency ManagementILDEFONSO DEL ROSARIONo ratings yet

- AST Partnership Liquidation Rob NotesDocument2 pagesAST Partnership Liquidation Rob NotesEvelyn LabhananNo ratings yet

- UST Golden Notes - Special Laws 2Document27 pagesUST Golden Notes - Special Laws 2Adalie Nageau100% (1)

- Portfolio Report Jan'23Document1 pagePortfolio Report Jan'23Dimple WaghelaNo ratings yet

- Assignment3 7QsDocument2 pagesAssignment3 7QsavirgNo ratings yet

- Story of A Security - CMLTI 2006-NC2Document6 pagesStory of A Security - CMLTI 2006-NC2the_akinitiNo ratings yet

- Acctg 4 Quiz 3 Debt Restructuring Payables 1Document11 pagesAcctg 4 Quiz 3 Debt Restructuring Payables 1Competente, Jhonna W.No ratings yet

- Akun Impor PT Surya SejahteraDocument4 pagesAkun Impor PT Surya SejahteraDiana FransiscaNo ratings yet

Download as docx, pdf, or txt

You might also like

- AP Receivables Quizzer507docDocument20 pagesAP Receivables Quizzer507docMa Yra YmataNo ratings yet

- Your Transunion Credit Report: Personal InformationDocument164 pagesYour Transunion Credit Report: Personal InformationRichard Griffin0% (1)

- Internal Reconstruction - HomeworkDocument25 pagesInternal Reconstruction - HomeworkYash ShewaleNo ratings yet

- Suggested Answer CAP II December 2016Document88 pagesSuggested Answer CAP II December 2016Nirmal ShresthaNo ratings yet

- Caa Assignment SolutionsDocument39 pagesCaa Assignment Solutionschikanesakshi2001No ratings yet

- Accountancy MSDocument11 pagesAccountancy MSmansoorbariNo ratings yet

- Accountancy-MS 23-24Document10 pagesAccountancy-MS 23-24Ashutosh SinghNo ratings yet

- Bv2018 Revised Conceptual FrameworkDocument18 pagesBv2018 Revised Conceptual FrameworkTeneswari RadhaNo ratings yet

- Internal ReconsrtuctionDocument33 pagesInternal ReconsrtuctionRenuNo ratings yet

- Marking SchemeDocument6 pagesMarking Schemeraghu monnappaNo ratings yet

- Accountancy 2023-24 MSDocument11 pagesAccountancy 2023-24 MSirfanoushad15No ratings yet

- Cbse cl12 Ead Accountancy Answers To Sample Paper 6Document15 pagesCbse cl12 Ead Accountancy Answers To Sample Paper 6amaankhan828768No ratings yet

- QUESTION PAPER 1 (Solution) : Q.1 A) Multiple Choice QuestionsDocument13 pagesQUESTION PAPER 1 (Solution) : Q.1 A) Multiple Choice QuestionsSiddharth VoraNo ratings yet

- Capital Reduction 2Document6 pagesCapital Reduction 2SANJIB SHARMANo ratings yet

- Pe2 Acc Nov05Document19 pagesPe2 Acc Nov05api-3825774No ratings yet

- Int Reconstruction 2019 Old-1Document14 pagesInt Reconstruction 2019 Old-1H122 Pallabi MukherjeeNo ratings yet

- Valuation of GoodwillDocument3 pagesValuation of GoodwillAhiaanNo ratings yet

- MS - Accountancy - 12-Practice Paper-1Document7 pagesMS - Accountancy - 12-Practice Paper-1Arun kumarNo ratings yet

- MS Xii Accountancy Set 1Document10 pagesMS Xii Accountancy Set 1arikoff07No ratings yet

- Marking Scheme Mock Test I 2023 24Document9 pagesMarking Scheme Mock Test I 2023 24HARSH CHAURASIYANo ratings yet

- QUESTION PAPER 36195 (Solution)Document17 pagesQUESTION PAPER 36195 (Solution)Faizu KhamNo ratings yet

- Internal ReconstructionDocument26 pagesInternal ReconstructionRajesh NangaliaNo ratings yet

- Answer Key 3Document8 pagesAnswer Key 3Hari prakarsh NimiNo ratings yet

- XII ACCOUNTANCY SET-2 Marking Scheme Ist Pre Board 2023-24-1Document9 pagesXII ACCOUNTANCY SET-2 Marking Scheme Ist Pre Board 2023-24-1Riddhima Murarka50% (2)

- Problem and Solutions: March, 2019Document2 pagesProblem and Solutions: March, 2019Pulkit SamratNo ratings yet

- 616806cf0cf2b988fbcdbd97 OriginalDocument20 pages616806cf0cf2b988fbcdbd97 OriginalTM GamingNo ratings yet

- CBSE Accountancy 12th Term 2 CH 3Document5 pagesCBSE Accountancy 12th Term 2 CH 3AadasNo ratings yet

- Corporate AccountingDocument93 pagesCorporate AccountingKalp JainNo ratings yet

- Practice Paper Pre-Board Xii Acc 2023-24Document13 pagesPractice Paper Pre-Board Xii Acc 2023-24Pratiksha Suryavanshi100% (1)

- 19013comp Sugans Pe2 Accounting Cp8 5Document12 pages19013comp Sugans Pe2 Accounting Cp8 5Ubaidulla MachingalNo ratings yet

- CA Inter Accounts A MTP 1 Nov 2022Document13 pagesCA Inter Accounts A MTP 1 Nov 2022smartshivenduNo ratings yet

- C.S. Executive - Answers For CC Test Paper - IDocument7 pagesC.S. Executive - Answers For CC Test Paper - Isekhar_gantiNo ratings yet

- 17269pe2 Sugg June09 1 PDFDocument22 pages17269pe2 Sugg June09 1 PDFSahil GoyalNo ratings yet

- Internal Reconstruction - ProblemsDocument8 pagesInternal Reconstruction - ProblemsNaomi SaldanhaNo ratings yet

- Sept 2014 - 230716 - 233727Document22 pagesSept 2014 - 230716 - 233727mohddanialhanaffimustaffiNo ratings yet

- Accounting Redemption of Debentures 1642416359Document19 pagesAccounting Redemption of Debentures 1642416359Shashank SikarwarNo ratings yet

- Set - 1 Acc MS PB12023-24Document10 pagesSet - 1 Acc MS PB12023-24aamiralishiasbackup1No ratings yet

- 5.cpbe - Xii Accts - MSDocument18 pages5.cpbe - Xii Accts - MScommerce12onlineclassesNo ratings yet

- XII Acc SQP 1 (AP 23-24)Document11 pagesXII Acc SQP 1 (AP 23-24)Vaidehi BagraNo ratings yet

- June 2019 All Paper SuggestedDocument120 pagesJune 2019 All Paper SuggestedEdtech NepalNo ratings yet

- CBSE Sample Paper 2024 Class 12 Accountancy MSDocument11 pagesCBSE Sample Paper 2024 Class 12 Accountancy MSskhushbusahniNo ratings yet

- CR Assignemt Unit 3Document25 pagesCR Assignemt Unit 3Calida SoaresNo ratings yet

- Answer Key - 1 TermDocument9 pagesAnswer Key - 1 TermsamayaksahuNo ratings yet

- Final Accounts 1. As Per Schedule III of Companies Act 2013, Prepare Financial Statement For Gillette India PVT LTDDocument3 pagesFinal Accounts 1. As Per Schedule III of Companies Act 2013, Prepare Financial Statement For Gillette India PVT LTDermiasNo ratings yet

- 12 Accountancy Comp Delhi2017 1Document28 pages12 Accountancy Comp Delhi2017 1harshit agrawalNo ratings yet

- Adobe Scan Jan 30, 2023Document6 pagesAdobe Scan Jan 30, 2023Karan RajakNo ratings yet

- CBCS BCOM GENERAL Sem-5 COMMERCE DSE-5.2-A CORPORATE-ACCOUNTING-10988Document12 pagesCBCS BCOM GENERAL Sem-5 COMMERCE DSE-5.2-A CORPORATE-ACCOUNTING-10988Sayantan DebnathNo ratings yet

- Ratio Analysis Ex 1Document2 pagesRatio Analysis Ex 1dZOAVIT GamingNo ratings yet

- Accountancy - Additional Questions MARKING SCHEMEDocument15 pagesAccountancy - Additional Questions MARKING SCHEMEseema chadhaNo ratings yet

- Assignment 2 Bus ComDocument22 pagesAssignment 2 Bus ComFaithful FighterNo ratings yet

- Internal Reconstruction PQ SolDocument17 pagesInternal Reconstruction PQ SolKaran MokhaNo ratings yet

- Adv Acc - 3 CHDocument21 pagesAdv Acc - 3 CHhassan nassereddineNo ratings yet

- Set - 3 Acc MSDocument6 pagesSet - 3 Acc MSaamiralishiasbackup1No ratings yet

- 5 6084915055709651012Document8 pages5 6084915055709651012Ajit Yadav100% (1)

- Accountancy Term-2 MVP 2023-24Document7 pagesAccountancy Term-2 MVP 2023-24Cp GpNo ratings yet

- Test Your Knowledge - 7Document2 pagesTest Your Knowledge - 7narangdiya602No ratings yet

- CE On Quasi-ReorganizationDocument1 pageCE On Quasi-ReorganizationalyssaNo ratings yet

- Question Papers: SEM. - (JULY 2023)Document8 pagesQuestion Papers: SEM. - (JULY 2023)arpitgupta20050No ratings yet

- 6.XII Accountancy Marking SchemeDocument10 pages6.XII Accountancy Marking Schemecommerce12onlineclassesNo ratings yet

- Isc Mock 2Document14 pagesIsc Mock 2anshikajain3474No ratings yet

- 2023 24 Xii Pre Board 1 MsDocument13 pages2023 24 Xii Pre Board 1 MsacguptaclassesNo ratings yet

- Visual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsFrom EverandVisual Financial Accounting for You: Greatly Modified Chess Positions as Financial and Accounting ConceptsNo ratings yet

- The Accounting Process Involves in Recording: A)Document28 pagesThe Accounting Process Involves in Recording: A)Shubham Saurav SSNo ratings yet

- RMOE FormatDocument2 pagesRMOE FormatVivekanand VaradarajanNo ratings yet

- Z Transforms WorksheetsDocument4 pagesZ Transforms Worksheetspilas_nikolaNo ratings yet

- Chapter 3 - Bonds Payable Other ConceptsDocument29 pagesChapter 3 - Bonds Payable Other ConceptsJEFFERSON CUTENo ratings yet

- Case Laws On Personal & Corporate Guarantors Under IBCDocument6 pagesCase Laws On Personal & Corporate Guarantors Under IBClaxmiNo ratings yet

- Topic 4 AnnuityDocument22 pagesTopic 4 AnnuityNanteni GanesanNo ratings yet

- Debt Collector Disclosure StatementDocument8 pagesDebt Collector Disclosure StatementGreg WilderNo ratings yet

- ST FinancingDocument30 pagesST FinancingJeyavikinesh SelvakkuganNo ratings yet

- Foreclosing On Nothing, Dale WhitmanDocument51 pagesForeclosing On Nothing, Dale WhitmanMarie McDonnellNo ratings yet

- Credit Structuring Model - COMPLETEDDocument9 pagesCredit Structuring Model - COMPLETEDfisehaNo ratings yet

- SALPL AgreementDocument30 pagesSALPL AgreementVipul JainNo ratings yet

- Paper 3 1 1Document7 pagesPaper 3 1 1api-593075882No ratings yet

- Customer Education IRACDocument3 pagesCustomer Education IRACHridya SNo ratings yet

- Siva RDocument17 pagesSiva RsidvikventuresNo ratings yet

- Individual Facility AgreementDocument66 pagesIndividual Facility AgreementDY KIM (INKO)No ratings yet

- 1.6 Accounting EquationDocument8 pages1.6 Accounting EquationAbijit GudaNo ratings yet

- Wa0004.Document7 pagesWa0004.viphainhumNo ratings yet

- MULTIPLE CHOICES-answer KeyDocument7 pagesMULTIPLE CHOICES-answer KeyLiaNo ratings yet

- Chapter 1Document24 pagesChapter 1Jhopel Casagnap EmanNo ratings yet

- David MccormickDocument20 pagesDavid MccormickAnonymous vRG3cFNjANo ratings yet

- Portofilo Quality and Delinquency ManagementDocument15 pagesPortofilo Quality and Delinquency ManagementILDEFONSO DEL ROSARIONo ratings yet

- AST Partnership Liquidation Rob NotesDocument2 pagesAST Partnership Liquidation Rob NotesEvelyn LabhananNo ratings yet

- UST Golden Notes - Special Laws 2Document27 pagesUST Golden Notes - Special Laws 2Adalie Nageau100% (1)

- Portfolio Report Jan'23Document1 pagePortfolio Report Jan'23Dimple WaghelaNo ratings yet

- Assignment3 7QsDocument2 pagesAssignment3 7QsavirgNo ratings yet

- Story of A Security - CMLTI 2006-NC2Document6 pagesStory of A Security - CMLTI 2006-NC2the_akinitiNo ratings yet

- Acctg 4 Quiz 3 Debt Restructuring Payables 1Document11 pagesAcctg 4 Quiz 3 Debt Restructuring Payables 1Competente, Jhonna W.No ratings yet

- Akun Impor PT Surya SejahteraDocument4 pagesAkun Impor PT Surya SejahteraDiana FransiscaNo ratings yet