Download as pdf or txt

You might also like

- PDFDocument732 pagesPDFMahmud Eljaarani90% (10)

- Assignment 2Document5 pagesAssignment 2Rohith DuvasiNo ratings yet

- Icelandic LanguageDocument28 pagesIcelandic LanguageMinamiCho100% (1)

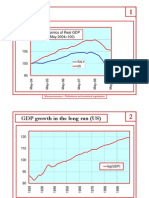

- The Crisis: Dynamics of Real GDP (May 2004 100)Document34 pagesThe Crisis: Dynamics of Real GDP (May 2004 100)Muhammad NaeemNo ratings yet

- Claims Triangle - R: Submitted by Ishan BandyopadhyayDocument23 pagesClaims Triangle - R: Submitted by Ishan BandyopadhyayAgni BanerjeeNo ratings yet

- Macro Chap1Document32 pagesMacro Chap1alemu ayeneNo ratings yet

- U Patnaik What Lies Behind The Food Crisis in India and The Global SouthDocument26 pagesU Patnaik What Lies Behind The Food Crisis in India and The Global SouthAnqur1984No ratings yet

- Assignment 2Document10 pagesAssignment 2Youssef AbdelhamidNo ratings yet

- Value Creation of Leveraged Buyouts in The United KingdomDocument34 pagesValue Creation of Leveraged Buyouts in The United KingdomCanlor LopesNo ratings yet

- 1 10 PDFDocument2 pages1 10 PDFhout rothanaNo ratings yet

- 1 Laws of Exponents and Algebraic ExpressionsDocument7 pages1 Laws of Exponents and Algebraic ExpressionsJanelle Dawn TanNo ratings yet

- 2011 - UOL - Monetary EconsDocument15 pages2011 - UOL - Monetary EconsAaron ChiaNo ratings yet

- Solution Manual For Precalculus With Limits 3rd EditionDocument36 pagesSolution Manual For Precalculus With Limits 3rd Editionhornpike.accidie6aot2o100% (56)

- Digitalisation On EconomyDocument20 pagesDigitalisation On EconomyMacsim BogdanNo ratings yet

- Network Theory: Instructions To CandidatesDocument3 pagesNetwork Theory: Instructions To CandidatesYadav BrandNo ratings yet

- Normal Distribution: Statistics and Probability Topic #4Document18 pagesNormal Distribution: Statistics and Probability Topic #4Diama, Hazel Anne B. 11-STEM 9No ratings yet

- Four Step Model Trip DistributionDocument25 pagesFour Step Model Trip DistributionLeBron JamesNo ratings yet

- SV-C33-AD and ASDocument16 pagesSV-C33-AD and ASphươngNo ratings yet

- CRIC - Economic Environment of Business-Lecture 1Document15 pagesCRIC - Economic Environment of Business-Lecture 1Jaz AzNo ratings yet

- Fajar Maulana Asl J - 057Document201 pagesFajar Maulana Asl J - 057MUHAMAD RISKYNo ratings yet

- Feature Selection For ClusteringDocument12 pagesFeature Selection For ClusteringLimonyNo ratings yet

- Tutorial Work Time Series Analysis Assignment 3 SolutionsDocument8 pagesTutorial Work Time Series Analysis Assignment 3 SolutionsMaritaNadyahNo ratings yet

- Continuous Beam AnalysisDocument20 pagesContinuous Beam AnalysisvnkatNo ratings yet

- Joe Robinson Fireflies Version 2Document8 pagesJoe Robinson Fireflies Version 2Edoardo TursiNo ratings yet

- Factor Analysis For Data Reduction Shahaida P Asst - ProfDocument15 pagesFactor Analysis For Data Reduction Shahaida P Asst - ProframanatenaliNo ratings yet

- ALGEBRA - PROBLEMS Examples and SolutionsDocument14 pagesALGEBRA - PROBLEMS Examples and Solutionssubash bandaruNo ratings yet

- So Why Do We Use Indices in Mathematics?: Working With Indices Gives Us A Quick Way To Simplify Complicated NumbersDocument7 pagesSo Why Do We Use Indices in Mathematics?: Working With Indices Gives Us A Quick Way To Simplify Complicated NumbersTavish AppadooNo ratings yet

- Jadual Susut Voltan (Single Core Cable) (TABLE 4D1B) : Lampiran IVDocument1 pageJadual Susut Voltan (Single Core Cable) (TABLE 4D1B) : Lampiran IVzfn2rqvqgqNo ratings yet

- Surveillance: Information For ActionDocument41 pagesSurveillance: Information For ActionDr. Zirwa AsimNo ratings yet

- Analysing Spatio-Temporal Regression Data: A Case Study in Forest HealthDocument43 pagesAnalysing Spatio-Temporal Regression Data: A Case Study in Forest HealthHoàng Thanh TùngNo ratings yet

- Yash Thakur 2100 or AssignmentDocument3 pagesYash Thakur 2100 or AssignmentYash ThakurNo ratings yet

- CE383 Direct Stiffness Method Examples 1Document35 pagesCE383 Direct Stiffness Method Examples 1yılmaz çepniNo ratings yet

- 21 Macro Economic Shocks and Their EffectsDocument14 pages21 Macro Economic Shocks and Their Effectssaywhat133No ratings yet

- DHL ReportDocument21 pagesDHL Reporttarun606No ratings yet

- CE 411 - Lecture 5Document14 pagesCE 411 - Lecture 5Israel PopeNo ratings yet

- Escalas Mayores Con BemolesDocument1 pageEscalas Mayores Con BemolesRicardo Dioses Gonzales-PolarNo ratings yet

- Basic and Applied Mathematics: SolutionDocument9 pagesBasic and Applied Mathematics: Solutionkefyalew TNo ratings yet

- Arch GarchDocument34 pagesArch GarchRishika JainNo ratings yet

- Chapter-2: Problem-11: Observed % of Observations Expected % of ObservationsDocument1 pageChapter-2: Problem-11: Observed % of Observations Expected % of ObservationsHarshal ShindeNo ratings yet

- Bba 3 Semester Examination Jan.2014 Subject - Operation Research Subject Code: MSL-205Document1 pageBba 3 Semester Examination Jan.2014 Subject - Operation Research Subject Code: MSL-205Pritee SinghNo ratings yet

- 13-Quine McCluskey MethodDocument43 pages13-Quine McCluskey Methodkambala dhanush100% (1)

- Pareto Chart - Zam EMQM5103 - Project Quality ManagementDocument20 pagesPareto Chart - Zam EMQM5103 - Project Quality ManagementIzam MuhammadNo ratings yet

- Preprint Asinari JCP 2008b PDFDocument30 pagesPreprint Asinari JCP 2008b PDFMücahitYıldızNo ratings yet

- A Markov-Switching Vector Equilibrium Correction Model of The Uk Labour MarketDocument22 pagesA Markov-Switching Vector Equilibrium Correction Model of The Uk Labour Marketgogayin869No ratings yet

- Lecture Note 1 - Introduction To Time SeriesDocument13 pagesLecture Note 1 - Introduction To Time SeriesWilians SantosNo ratings yet

- Project Report: Structural DynamicsDocument24 pagesProject Report: Structural DynamicsatifaNo ratings yet

- Time-Series Analysis (Cont.)Document20 pagesTime-Series Analysis (Cont.)snoozermanNo ratings yet

- ECON 3023 CH 13Document22 pagesECON 3023 CH 13Rafina AzizNo ratings yet

- Beam 3Document20 pagesBeam 3MARIO MARCELONo ratings yet

- Time SeriousDocument10 pagesTime SeriousZubair AnwarNo ratings yet

- Beam 3Document20 pagesBeam 3MARIO MARCELONo ratings yet

- Assignment 2Document7 pagesAssignment 2Ibrahim KhaledNo ratings yet

- SBBSBDocument25 pagesSBBSBHelloNo ratings yet

- ECO452 October 2019Document3 pagesECO452 October 2019leonwankwo1No ratings yet

- Data For LabsDocument17 pagesData For LabsDarkoNo ratings yet

- Chapter 5&6Document9 pagesChapter 5&6Bhebz Erin MaeNo ratings yet

- Civ-306 Estructuras Hiperestaticas: Ejercicio #1 Proyecto I Univ.:Fajardo Mamani WilverDocument28 pagesCiv-306 Estructuras Hiperestaticas: Ejercicio #1 Proyecto I Univ.:Fajardo Mamani WilverWifama Fajardo MamaniNo ratings yet

- Assignment 1 TaskDocument3 pagesAssignment 1 Taskginevra.disalvoNo ratings yet

- Foundations of Modern Macroeconomics Third Edition: Chapter 7: A Closer Look at The Labour MarketDocument69 pagesFoundations of Modern Macroeconomics Third Edition: Chapter 7: A Closer Look at The Labour Marketarmagg1245No ratings yet

- Multidimensional Operations: PJ01 PR99 B 04Document50 pagesMultidimensional Operations: PJ01 PR99 B 04pepe_3059No ratings yet

- Introduction To Business Statistics 6th Edition Weiers Solutions ManualDocument25 pagesIntroduction To Business Statistics 6th Edition Weiers Solutions ManualMatthewRosarioksdf100% (48)

- Ebouk Monetary Economics 03Document4 pagesEbouk Monetary Economics 03koraNo ratings yet

- Ebouk Monetary Economics 05Document2 pagesEbouk Monetary Economics 05koraNo ratings yet

- 6.3 Political and Monetary UnionDocument2 pages6.3 Political and Monetary UnionkoraNo ratings yet

- Figure 2 Annual CPI Inflation Rates.: UK TheDocument2 pagesFigure 2 Annual CPI Inflation Rates.: UK ThekoraNo ratings yet

- Ebouk Monetary Economics 10Document2 pagesEbouk Monetary Economics 10koraNo ratings yet

- Ebouk Monetary Economics 08Document2 pagesEbouk Monetary Economics 08koraNo ratings yet

- Ebouk Monetary Economics 05Document2 pagesEbouk Monetary Economics 05koraNo ratings yet

- Ebouk Monetary Economics 03Document2 pagesEbouk Monetary Economics 03koraNo ratings yet

- Magnetic Effects Class 10Document6 pagesMagnetic Effects Class 10Lokesh VaswaniNo ratings yet

- Design of Elastomeric BearingsDocument6 pagesDesign of Elastomeric BearingsHarshitha GaneshNo ratings yet

- Turning Process, Defects, EquipmentDocument7 pagesTurning Process, Defects, Equipmentvinaybaba100% (1)

- CCCC CCC CDocument9 pagesCCCC CCC CGhulamMustafa76No ratings yet

- IMPULSEP3 Series 2 AdvancedDocument84 pagesIMPULSEP3 Series 2 Advancedjeevan sankarNo ratings yet

- How To Create A Text Portrait Effect in Photoshop PDFDocument13 pagesHow To Create A Text Portrait Effect in Photoshop PDFkimberlyNo ratings yet

- Transmisor TRA ComecoDocument1 pageTransmisor TRA ComecoCorina FraszczakNo ratings yet

- High Performance Lubricant For Bikes 100% Synthetic - Ester: Type of UseDocument1 pageHigh Performance Lubricant For Bikes 100% Synthetic - Ester: Type of UseDouimni AyoubNo ratings yet

- PCCP Construction MethodologyDocument26 pagesPCCP Construction MethodologyRolly Marc G. Sotelo50% (2)

- 2 Operations On PolynomialsDocument5 pages2 Operations On Polynomialsapi-304499560No ratings yet

- The Rise of "Blockchain": Bibliometric Analysis of Blockchain StudyDocument43 pagesThe Rise of "Blockchain": Bibliometric Analysis of Blockchain StudyJimNo ratings yet

- 327, BC A101 05 Oa As BSDocument9 pages327, BC A101 05 Oa As BSMiguel AngelNo ratings yet

- MC 12 PDFDocument5 pagesMC 12 PDFtobi10No ratings yet

- IV B.Tech. I Semester Supplementary Examinations July 2021: Code: 7G574Document5 pagesIV B.Tech. I Semester Supplementary Examinations July 2021: Code: 7G574battle backbenchersNo ratings yet

- Understanding Calculation ScriptsDocument17 pagesUnderstanding Calculation ScriptsKrishna TilakNo ratings yet

- Explosion Protection Theory and Practice - Phoenix ContactDocument40 pagesExplosion Protection Theory and Practice - Phoenix Contactcuongphan123No ratings yet

- Leica Hds 6100 Brochure UsDocument4 pagesLeica Hds 6100 Brochure UsBlake WhiteNo ratings yet

- Transformer Oil AnalysisDocument1 pageTransformer Oil Analysisalvin meNo ratings yet

- Atomic Orbital WorksheetsDocument6 pagesAtomic Orbital WorksheetsMarnieKanarek0% (1)

- Dips PDFDocument2 pagesDips PDFRaghvendra ShrivastavaNo ratings yet

- Ncert 11 Physics 2Document181 pagesNcert 11 Physics 2shivaraj pNo ratings yet

- Oracle VM Manager (3.0.1) Installation: On Suse Linux Enterprise Server 11 Sp1 (X86 - 64)Document20 pagesOracle VM Manager (3.0.1) Installation: On Suse Linux Enterprise Server 11 Sp1 (X86 - 64)Tolulope AbiodunNo ratings yet

- Chapter Five Network Items SpecificationDocument37 pagesChapter Five Network Items SpecificationPro NebyuNo ratings yet

- BCA Sheet Manitou RepairDocument71 pagesBCA Sheet Manitou Repairbumatio lati100% (1)

- HDG Kla Gard enDocument2 pagesHDG Kla Gard enVictor ManuelNo ratings yet

- Design Via Root LocusDocument53 pagesDesign Via Root LocusAhmed ShareefNo ratings yet

- Klawiatura Dell KB216Document1 pageKlawiatura Dell KB216Diogo Borges OliveiraNo ratings yet