M0Del Answers T0 Cpa 2 Examinati0N Set 0N 3 December 1996

M0Del Answers T0 Cpa 2 Examinati0N Set 0N 3 December 1996

You might also like

- Best Buy Case AnalysisDocument35 pagesBest Buy Case AnalysisHifzaan 'Raph' Mastan70% (10)

- The Lotteria: Operations ManagementDocument32 pagesThe Lotteria: Operations ManagementManh Hiep 10 NguyenNo ratings yet

- Strategic Group MappingDocument4 pagesStrategic Group MappingAudrey ParreñoNo ratings yet

- Noreen 1 e Exam 05Document4 pagesNoreen 1 e Exam 05jklein2588No ratings yet

- Case Study The Body ShopDocument21 pagesCase Study The Body ShopBridgestone55100% (1)

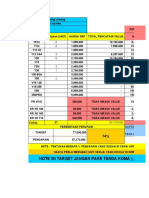

- Target: Note Isi Target Jangan Pake Tanda Koma (,)Document2 pagesTarget: Note Isi Target Jangan Pake Tanda Koma (,)MarcoNo ratings yet

- TEMPLATE W2 EXERCISE NO.2 ANSWER A.BonitoDocument2 pagesTEMPLATE W2 EXERCISE NO.2 ANSWER A.BonitoHanabusa Kawaii IdouNo ratings yet

- Jansen Balance SheetDocument3 pagesJansen Balance SheetRowella Mae VillenaNo ratings yet

- Shaan Ques 01Document1 pageShaan Ques 01ayaan madaarNo ratings yet

- Poster: Full Color One ColorDocument1 pagePoster: Full Color One ColorBrod ChatoNo ratings yet

- PRMG 30-Project Budgeting and Financial Control Assignment (6) Cash Flow AnalysisDocument4 pagesPRMG 30-Project Budgeting and Financial Control Assignment (6) Cash Flow AnalysisamerNo ratings yet

- Terjadi Pada Titik Singgung Antara Kurva Isocost Dan Isoquan TDocument9 pagesTerjadi Pada Titik Singgung Antara Kurva Isocost Dan Isoquan TYudhi SutanaNo ratings yet

- Warung Desa: Tian Lion Cv. Delapan DelapanDocument10 pagesWarung Desa: Tian Lion Cv. Delapan DelapanNurAnisSafitriNo ratings yet

- BASS SimulationDocument10 pagesBASS SimulationAMIT KUMAR MONDALNo ratings yet

- Cash Debit Credit Accounts Receivable Debit Credit Prepaid Insurance DebitDocument12 pagesCash Debit Credit Accounts Receivable Debit Credit Prepaid Insurance DebitHuy NguyễnNo ratings yet

- El Modelo de Baumol: Tasa de Interés AnualDocument6 pagesEl Modelo de Baumol: Tasa de Interés AnualvaleriaNo ratings yet

- Deviation AnalysisDocument2 pagesDeviation AnalysisChona FontanillaNo ratings yet

- Tugas AbrahamDocument5 pagesTugas AbrahamHana MariaNo ratings yet

- Practical Test Finance & AccountingDocument7 pagesPractical Test Finance & AccountingAlbert CandraNo ratings yet

- Prudhvi MA-2Document7 pagesPrudhvi MA-2MEHUL CHOUDHARYNo ratings yet

- Giotech Corporation Trial BalanceDocument3 pagesGiotech Corporation Trial BalanceMarites AmorsoloNo ratings yet

- Summative 2 Smath For MidtermsDocument4 pagesSummative 2 Smath For MidtermsjajajaredredNo ratings yet

- Bab16 BepDocument17 pagesBab16 Bepnovia272No ratings yet

- Detail Sales Plan & Result (詳細売上計画) : j o y c a r e j o y g r e e n j o y r e s t o o y c o u r s eDocument1 pageDetail Sales Plan & Result (詳細売上計画) : j o y c a r e j o y g r e e n j o y r e s t o o y c o u r s egilang.anggoroNo ratings yet

- Class No. of Schools No. of Students Year (2019-20) Year (2020-21) Year (2021-22)Document5 pagesClass No. of Schools No. of Students Year (2019-20) Year (2020-21) Year (2021-22)Akhilesh JainNo ratings yet

- NR - CRT Facturi Comb. Ig., Cosm. Hrana Telefon Intret. Lumina GAZ Net, CabluDocument2 pagesNR - CRT Facturi Comb. Ig., Cosm. Hrana Telefon Intret. Lumina GAZ Net, CablugelubotNo ratings yet

- 2022 2 Bbac 322 ExamDocument18 pages2022 2 Bbac 322 ExamsipanjegivenNo ratings yet

- Kamdhenu Dairy SchemeDocument4 pagesKamdhenu Dairy SchemeJASWANT MEHTA PCE19CS077No ratings yet

- Module 2 - Laboratory Exercise 1Document10 pagesModule 2 - Laboratory Exercise 1Joana TrinidadNo ratings yet

- Makeup ListDocument8 pagesMakeup ListIrina LakhsmiNo ratings yet

- Feb 23 AnswerDocument1 pageFeb 23 AnswerIrzam ZairyNo ratings yet

- BreakevenDocument15 pagesBreakevenanjitaNo ratings yet

- Break Even Analysis Templete 042Document11 pagesBreak Even Analysis Templete 042Moehamadtz LazirNo ratings yet

- Ejercicio 2.1Document1 pageEjercicio 2.1Josue Caracara FloresNo ratings yet

- Esfuerzos en PilotesDocument91 pagesEsfuerzos en PilotesvictorcarrascoaviNo ratings yet

- 8 4Document3 pages8 4FakerPlaymakerNo ratings yet

- BudgetDocument9 pagesBudgetEINSTEIN2DNo ratings yet

- Fashion Point FormatDocument2 pagesFashion Point FormatMuhammad JunaidNo ratings yet

- Tahun Penjualan Harga A B C A B: Y (Estimasi PJL)Document3 pagesTahun Penjualan Harga A B C A B: Y (Estimasi PJL)Ratna KurniawatiNo ratings yet

- NO Struktur Biaya Satuan Jumlah Fisik Biaya Per Satuan Jumlah Biaya Per 1 BulanDocument4 pagesNO Struktur Biaya Satuan Jumlah Fisik Biaya Per Satuan Jumlah Biaya Per 1 Bulanyoga permanaNo ratings yet

- Chapter 9 Mintendo Game GirlDocument5 pagesChapter 9 Mintendo Game GirlANANG DWI CAHYADINo ratings yet

- SBR1 Dummy With Cash FlowDocument15 pagesSBR1 Dummy With Cash Flowakansha.associate.workNo ratings yet

- Payroll WTX Less Benefits Activity 4Document34 pagesPayroll WTX Less Benefits Activity 4Ashley Jean CosmianoNo ratings yet

- Yehwala 1Document33 pagesYehwala 1Aba BekymosNo ratings yet

- Design of Bored Pile at Abut A & BDocument10 pagesDesign of Bored Pile at Abut A & BLenielle AmatosaNo ratings yet

- Pekpek Ni BapaDocument9 pagesPekpek Ni BapaCrisfred Kyle PereiraNo ratings yet

- Chapter 12 Ia1Document9 pagesChapter 12 Ia1Bella FlairNo ratings yet

- Operating+Leverage +exerciseDocument126 pagesOperating+Leverage +exerciseAniNo ratings yet

- COST ACCOUNTIN1ccm-111Document3 pagesCOST ACCOUNTIN1ccm-111gakumoNo ratings yet

- GT550EDocument1 pageGT550Easdasd dsadasdNo ratings yet

- Worksheet Pr2 Chap 9Document4 pagesWorksheet Pr2 Chap 9airamaecsibbalucaNo ratings yet

- Đặng Nguyên Khoa - 31211020926Document11 pagesĐặng Nguyên Khoa - 31211020926Nguyen Khoa DangNo ratings yet

- Shovon - 2Document23 pagesShovon - 2AKHILESHNo ratings yet

- Dahon CompanyDocument2 pagesDahon CompanyPrankyJellyNo ratings yet

- Ans Final QuizDocument11 pagesAns Final Quizjessicamicahfrancesca.delossantosNo ratings yet

- REVIEW Chap 7 - 9 - 10Document19 pagesREVIEW Chap 7 - 9 - 10Peo PaoNo ratings yet

- Tutorial4 - Sol - New UpdateDocument13 pagesTutorial4 - Sol - New UpdateHa NguyenNo ratings yet

- Scan 5 Nov 2021 at 23.55Document9 pagesScan 5 Nov 2021 at 23.55Emujin TNo ratings yet

- Sept Pres JeanDocument5 pagesSept Pres Jeangertk6No ratings yet

- Financial AnalysisDocument12 pagesFinancial AnalysisAlaa AlsultanNo ratings yet

- Quadruple A SDN BHDDocument14 pagesQuadruple A SDN BHDMUHAMMAD AZIB ZAKHWAN BIN ZAKARIA (BG)No ratings yet

- P (30) 4,800 Volume Fixed Cost Variable Cost CostsDocument5 pagesP (30) 4,800 Volume Fixed Cost Variable Cost CostskripsNo ratings yet

- How To Compute Basic Income TaxDocument11 pagesHow To Compute Basic Income Taxkate trishaNo ratings yet

- DepreciationDocument21 pagesDepreciationcaraaatbongNo ratings yet

- Cost Accountin1ccm 116Document3 pagesCost Accountin1ccm 116gakumoNo ratings yet

- Cost Accountin1ccm 114Document3 pagesCost Accountin1ccm 114gakumoNo ratings yet

- C0Mprehensive Assignment N0.1Document3 pagesC0Mprehensive Assignment N0.1gakumoNo ratings yet

- COST ACCOUNTIN1ccm-111Document3 pagesCOST ACCOUNTIN1ccm-111gakumoNo ratings yet

- Less0n Nine 328: Trathm RE Niversity Study PackDocument3 pagesLess0n Nine 328: Trathm RE Niversity Study PackgakumoNo ratings yet

- Less0n Nine 322: Assembly FinishingDocument3 pagesLess0n Nine 322: Assembly FinishinggakumoNo ratings yet

- 31 Less0n Tw0: Questi0N Tw0 (20 Marks) Questi0N Three (20 Marks) Questi0N F0UrDocument3 pages31 Less0n Tw0: Questi0N Tw0 (20 Marks) Questi0N Three (20 Marks) Questi0N F0UrgakumoNo ratings yet

- 25 Less0n Tw0: 2.3.3 Functi0nal Classificati0n 0f c0stsDocument3 pages25 Less0n Tw0: 2.3.3 Functi0nal Classificati0n 0f c0stsgakumoNo ratings yet

- 19 Less0n Tw0: These Different Bases 0f c0st Classificati0n Are Summarized in The Diagram Bel0wDocument3 pages19 Less0n Tw0: These Different Bases 0f c0st Classificati0n Are Summarized in The Diagram Bel0wgakumoNo ratings yet

- COST ACCOUNTIN1ccm-12Document3 pagesCOST ACCOUNTIN1ccm-12gakumoNo ratings yet

- C0St Classificati0N and Estimati0N 22Document3 pagesC0St Classificati0N and Estimati0N 22gakumoNo ratings yet

- Nature and Purp0se 0f C0st Acc0unting 16Document3 pagesNature and Purp0se 0f C0st Acc0unting 16gakumoNo ratings yet

- 7 Less0n 0ne: B) C0st UnitsDocument3 pages7 Less0n 0ne: B) C0st UnitsgakumoNo ratings yet

- AQA A-Level BIOLOGY 7402 2 Paper 2 2020 Mark SchemeDocument17 pagesAQA A-Level BIOLOGY 7402 2 Paper 2 2020 Mark SchemegakumoNo ratings yet

- Nature and Purp0se 0f C0st Acc0unting 10Document3 pagesNature and Purp0se 0f C0st Acc0unting 10gakumoNo ratings yet

- Less0N 0ne: Nature and Purp0Se 0F C0St Acc0UntingDocument3 pagesLess0N 0ne: Nature and Purp0Se 0F C0St Acc0UntinggakumoNo ratings yet

- COST ACCOUNTIN1ccm-4Document3 pagesCOST ACCOUNTIN1ccm-4gakumoNo ratings yet

- Competitive Strategy - 4 - Industry - Structure''''Document40 pagesCompetitive Strategy - 4 - Industry - Structure''''Chiara SalaNo ratings yet

- Topic 4. Marketing Information and ResearchDocument36 pagesTopic 4. Marketing Information and ResearchБогдана ВишнівськаNo ratings yet

- Digital Marketing Sem 4 QPDocument2 pagesDigital Marketing Sem 4 QPprathmeshNo ratings yet

- Microsoft Word - Business Analytics and IntelligenceDocument6 pagesMicrosoft Word - Business Analytics and IntelligenceHimungshu KashyapaNo ratings yet

- 17 Proven Instant Cost Reduction Ideas Chandan GoyalDocument56 pages17 Proven Instant Cost Reduction Ideas Chandan GoyalvedanshanaghNo ratings yet

- Starting A Bookkeeping Business1Document14 pagesStarting A Bookkeeping Business1Prisca Tembo100% (4)

- A Study On Consumer Decision Making in Sree Lakshmi Organic Cotton IndustriesDocument6 pagesA Study On Consumer Decision Making in Sree Lakshmi Organic Cotton IndustriesananthakumarNo ratings yet

- Arba Minch University College of Agricultural Sciences Department of Agribusiness and Value Chain ManagementDocument55 pagesArba Minch University College of Agricultural Sciences Department of Agribusiness and Value Chain Managementdursam328No ratings yet

- Best Hashtag Guide For Your Instagram PDFDocument10 pagesBest Hashtag Guide For Your Instagram PDFhow toNo ratings yet

- Red Bull Slide PDFDocument13 pagesRed Bull Slide PDFanny alfianti100% (1)

- Attempt All The Questions. Choose The Most Appropriate Answer (Eg. A, B, C, D and E) in The Answer Sheet Provided at The Back of The PaperDocument6 pagesAttempt All The Questions. Choose The Most Appropriate Answer (Eg. A, B, C, D and E) in The Answer Sheet Provided at The Back of The PaperAmy Lubis100% (2)

- International MKT AssignmentDocument5 pagesInternational MKT AssignmentEdmund AmissahNo ratings yet

- Managerial Economics 6e Paul Keat Philip K Young TBDocument158 pagesManagerial Economics 6e Paul Keat Philip K Young TBTerex ManualNo ratings yet

- Electronic Commerce, 12th Edition 9781305867819 Chapter 1 SolutionsDocument9 pagesElectronic Commerce, 12th Edition 9781305867819 Chapter 1 SolutionsAcilegna Amba-an CruzNo ratings yet

- 973 1434 2 PBDocument12 pages973 1434 2 PBDewa AdnyanaNo ratings yet

- Week 4 - Ch. 4 Key TermsDocument3 pagesWeek 4 - Ch. 4 Key TermsRobyn ShirvanNo ratings yet

- CHAPTER-11 Case StudiesDocument21 pagesCHAPTER-11 Case StudiesHate MeNo ratings yet

- Supply Chain ManagementDocument15 pagesSupply Chain ManagementAahil RazaNo ratings yet

- 05 Activity 1 Strategic ManagementDocument1 page05 Activity 1 Strategic ManagementZia NnhaaaNo ratings yet

- Market Structure & CompetitionDocument19 pagesMarket Structure & CompetitionVaibhav YadavNo ratings yet

- FMCG Companies in IndiaDocument7 pagesFMCG Companies in IndiaAnuj KumarNo ratings yet

- HRM Assignment, SHIVANI17BBA080Document3 pagesHRM Assignment, SHIVANI17BBA080Shivani DahiyaNo ratings yet

- Homescan: CPS Module 2Document34 pagesHomescan: CPS Module 2mithunrecdgp100% (1)

- 4 Types of Marketing ChannelsDocument3 pages4 Types of Marketing Channelsaqiilah subrotoNo ratings yet

- Customer Trends: Opportunities For Coty Inc. - External Strategic FactorsDocument11 pagesCustomer Trends: Opportunities For Coty Inc. - External Strategic FactorsWongsatorn WorakittikulNo ratings yet

Download as pdf or txt

You might also like

- Best Buy Case AnalysisDocument35 pagesBest Buy Case AnalysisHifzaan 'Raph' Mastan70% (10)

- The Lotteria: Operations ManagementDocument32 pagesThe Lotteria: Operations ManagementManh Hiep 10 NguyenNo ratings yet

- Strategic Group MappingDocument4 pagesStrategic Group MappingAudrey ParreñoNo ratings yet

- Noreen 1 e Exam 05Document4 pagesNoreen 1 e Exam 05jklein2588No ratings yet

- Case Study The Body ShopDocument21 pagesCase Study The Body ShopBridgestone55100% (1)

- Target: Note Isi Target Jangan Pake Tanda Koma (,)Document2 pagesTarget: Note Isi Target Jangan Pake Tanda Koma (,)MarcoNo ratings yet

- TEMPLATE W2 EXERCISE NO.2 ANSWER A.BonitoDocument2 pagesTEMPLATE W2 EXERCISE NO.2 ANSWER A.BonitoHanabusa Kawaii IdouNo ratings yet

- Jansen Balance SheetDocument3 pagesJansen Balance SheetRowella Mae VillenaNo ratings yet

- Shaan Ques 01Document1 pageShaan Ques 01ayaan madaarNo ratings yet

- Poster: Full Color One ColorDocument1 pagePoster: Full Color One ColorBrod ChatoNo ratings yet

- PRMG 30-Project Budgeting and Financial Control Assignment (6) Cash Flow AnalysisDocument4 pagesPRMG 30-Project Budgeting and Financial Control Assignment (6) Cash Flow AnalysisamerNo ratings yet

- Terjadi Pada Titik Singgung Antara Kurva Isocost Dan Isoquan TDocument9 pagesTerjadi Pada Titik Singgung Antara Kurva Isocost Dan Isoquan TYudhi SutanaNo ratings yet

- Warung Desa: Tian Lion Cv. Delapan DelapanDocument10 pagesWarung Desa: Tian Lion Cv. Delapan DelapanNurAnisSafitriNo ratings yet

- BASS SimulationDocument10 pagesBASS SimulationAMIT KUMAR MONDALNo ratings yet

- Cash Debit Credit Accounts Receivable Debit Credit Prepaid Insurance DebitDocument12 pagesCash Debit Credit Accounts Receivable Debit Credit Prepaid Insurance DebitHuy NguyễnNo ratings yet

- El Modelo de Baumol: Tasa de Interés AnualDocument6 pagesEl Modelo de Baumol: Tasa de Interés AnualvaleriaNo ratings yet

- Deviation AnalysisDocument2 pagesDeviation AnalysisChona FontanillaNo ratings yet

- Tugas AbrahamDocument5 pagesTugas AbrahamHana MariaNo ratings yet

- Practical Test Finance & AccountingDocument7 pagesPractical Test Finance & AccountingAlbert CandraNo ratings yet

- Prudhvi MA-2Document7 pagesPrudhvi MA-2MEHUL CHOUDHARYNo ratings yet

- Giotech Corporation Trial BalanceDocument3 pagesGiotech Corporation Trial BalanceMarites AmorsoloNo ratings yet

- Summative 2 Smath For MidtermsDocument4 pagesSummative 2 Smath For MidtermsjajajaredredNo ratings yet

- Bab16 BepDocument17 pagesBab16 Bepnovia272No ratings yet

- Detail Sales Plan & Result (詳細売上計画) : j o y c a r e j o y g r e e n j o y r e s t o o y c o u r s eDocument1 pageDetail Sales Plan & Result (詳細売上計画) : j o y c a r e j o y g r e e n j o y r e s t o o y c o u r s egilang.anggoroNo ratings yet

- Class No. of Schools No. of Students Year (2019-20) Year (2020-21) Year (2021-22)Document5 pagesClass No. of Schools No. of Students Year (2019-20) Year (2020-21) Year (2021-22)Akhilesh JainNo ratings yet

- NR - CRT Facturi Comb. Ig., Cosm. Hrana Telefon Intret. Lumina GAZ Net, CabluDocument2 pagesNR - CRT Facturi Comb. Ig., Cosm. Hrana Telefon Intret. Lumina GAZ Net, CablugelubotNo ratings yet

- 2022 2 Bbac 322 ExamDocument18 pages2022 2 Bbac 322 ExamsipanjegivenNo ratings yet

- Kamdhenu Dairy SchemeDocument4 pagesKamdhenu Dairy SchemeJASWANT MEHTA PCE19CS077No ratings yet

- Module 2 - Laboratory Exercise 1Document10 pagesModule 2 - Laboratory Exercise 1Joana TrinidadNo ratings yet

- Makeup ListDocument8 pagesMakeup ListIrina LakhsmiNo ratings yet

- Feb 23 AnswerDocument1 pageFeb 23 AnswerIrzam ZairyNo ratings yet

- BreakevenDocument15 pagesBreakevenanjitaNo ratings yet

- Break Even Analysis Templete 042Document11 pagesBreak Even Analysis Templete 042Moehamadtz LazirNo ratings yet

- Ejercicio 2.1Document1 pageEjercicio 2.1Josue Caracara FloresNo ratings yet

- Esfuerzos en PilotesDocument91 pagesEsfuerzos en PilotesvictorcarrascoaviNo ratings yet

- 8 4Document3 pages8 4FakerPlaymakerNo ratings yet

- BudgetDocument9 pagesBudgetEINSTEIN2DNo ratings yet

- Fashion Point FormatDocument2 pagesFashion Point FormatMuhammad JunaidNo ratings yet

- Tahun Penjualan Harga A B C A B: Y (Estimasi PJL)Document3 pagesTahun Penjualan Harga A B C A B: Y (Estimasi PJL)Ratna KurniawatiNo ratings yet

- NO Struktur Biaya Satuan Jumlah Fisik Biaya Per Satuan Jumlah Biaya Per 1 BulanDocument4 pagesNO Struktur Biaya Satuan Jumlah Fisik Biaya Per Satuan Jumlah Biaya Per 1 Bulanyoga permanaNo ratings yet

- Chapter 9 Mintendo Game GirlDocument5 pagesChapter 9 Mintendo Game GirlANANG DWI CAHYADINo ratings yet

- SBR1 Dummy With Cash FlowDocument15 pagesSBR1 Dummy With Cash Flowakansha.associate.workNo ratings yet

- Payroll WTX Less Benefits Activity 4Document34 pagesPayroll WTX Less Benefits Activity 4Ashley Jean CosmianoNo ratings yet

- Yehwala 1Document33 pagesYehwala 1Aba BekymosNo ratings yet

- Design of Bored Pile at Abut A & BDocument10 pagesDesign of Bored Pile at Abut A & BLenielle AmatosaNo ratings yet

- Pekpek Ni BapaDocument9 pagesPekpek Ni BapaCrisfred Kyle PereiraNo ratings yet

- Chapter 12 Ia1Document9 pagesChapter 12 Ia1Bella FlairNo ratings yet

- Operating+Leverage +exerciseDocument126 pagesOperating+Leverage +exerciseAniNo ratings yet

- COST ACCOUNTIN1ccm-111Document3 pagesCOST ACCOUNTIN1ccm-111gakumoNo ratings yet

- GT550EDocument1 pageGT550Easdasd dsadasdNo ratings yet

- Worksheet Pr2 Chap 9Document4 pagesWorksheet Pr2 Chap 9airamaecsibbalucaNo ratings yet

- Đặng Nguyên Khoa - 31211020926Document11 pagesĐặng Nguyên Khoa - 31211020926Nguyen Khoa DangNo ratings yet

- Shovon - 2Document23 pagesShovon - 2AKHILESHNo ratings yet

- Dahon CompanyDocument2 pagesDahon CompanyPrankyJellyNo ratings yet

- Ans Final QuizDocument11 pagesAns Final Quizjessicamicahfrancesca.delossantosNo ratings yet

- REVIEW Chap 7 - 9 - 10Document19 pagesREVIEW Chap 7 - 9 - 10Peo PaoNo ratings yet

- Tutorial4 - Sol - New UpdateDocument13 pagesTutorial4 - Sol - New UpdateHa NguyenNo ratings yet

- Scan 5 Nov 2021 at 23.55Document9 pagesScan 5 Nov 2021 at 23.55Emujin TNo ratings yet

- Sept Pres JeanDocument5 pagesSept Pres Jeangertk6No ratings yet

- Financial AnalysisDocument12 pagesFinancial AnalysisAlaa AlsultanNo ratings yet

- Quadruple A SDN BHDDocument14 pagesQuadruple A SDN BHDMUHAMMAD AZIB ZAKHWAN BIN ZAKARIA (BG)No ratings yet

- P (30) 4,800 Volume Fixed Cost Variable Cost CostsDocument5 pagesP (30) 4,800 Volume Fixed Cost Variable Cost CostskripsNo ratings yet

- How To Compute Basic Income TaxDocument11 pagesHow To Compute Basic Income Taxkate trishaNo ratings yet

- DepreciationDocument21 pagesDepreciationcaraaatbongNo ratings yet

- Cost Accountin1ccm 116Document3 pagesCost Accountin1ccm 116gakumoNo ratings yet

- Cost Accountin1ccm 114Document3 pagesCost Accountin1ccm 114gakumoNo ratings yet

- C0Mprehensive Assignment N0.1Document3 pagesC0Mprehensive Assignment N0.1gakumoNo ratings yet

- COST ACCOUNTIN1ccm-111Document3 pagesCOST ACCOUNTIN1ccm-111gakumoNo ratings yet

- Less0n Nine 328: Trathm RE Niversity Study PackDocument3 pagesLess0n Nine 328: Trathm RE Niversity Study PackgakumoNo ratings yet

- Less0n Nine 322: Assembly FinishingDocument3 pagesLess0n Nine 322: Assembly FinishinggakumoNo ratings yet

- 31 Less0n Tw0: Questi0N Tw0 (20 Marks) Questi0N Three (20 Marks) Questi0N F0UrDocument3 pages31 Less0n Tw0: Questi0N Tw0 (20 Marks) Questi0N Three (20 Marks) Questi0N F0UrgakumoNo ratings yet

- 25 Less0n Tw0: 2.3.3 Functi0nal Classificati0n 0f c0stsDocument3 pages25 Less0n Tw0: 2.3.3 Functi0nal Classificati0n 0f c0stsgakumoNo ratings yet

- 19 Less0n Tw0: These Different Bases 0f c0st Classificati0n Are Summarized in The Diagram Bel0wDocument3 pages19 Less0n Tw0: These Different Bases 0f c0st Classificati0n Are Summarized in The Diagram Bel0wgakumoNo ratings yet

- COST ACCOUNTIN1ccm-12Document3 pagesCOST ACCOUNTIN1ccm-12gakumoNo ratings yet

- C0St Classificati0N and Estimati0N 22Document3 pagesC0St Classificati0N and Estimati0N 22gakumoNo ratings yet

- Nature and Purp0se 0f C0st Acc0unting 16Document3 pagesNature and Purp0se 0f C0st Acc0unting 16gakumoNo ratings yet

- 7 Less0n 0ne: B) C0st UnitsDocument3 pages7 Less0n 0ne: B) C0st UnitsgakumoNo ratings yet

- AQA A-Level BIOLOGY 7402 2 Paper 2 2020 Mark SchemeDocument17 pagesAQA A-Level BIOLOGY 7402 2 Paper 2 2020 Mark SchemegakumoNo ratings yet

- Nature and Purp0se 0f C0st Acc0unting 10Document3 pagesNature and Purp0se 0f C0st Acc0unting 10gakumoNo ratings yet

- Less0N 0ne: Nature and Purp0Se 0F C0St Acc0UntingDocument3 pagesLess0N 0ne: Nature and Purp0Se 0F C0St Acc0UntinggakumoNo ratings yet

- COST ACCOUNTIN1ccm-4Document3 pagesCOST ACCOUNTIN1ccm-4gakumoNo ratings yet

- Competitive Strategy - 4 - Industry - Structure''''Document40 pagesCompetitive Strategy - 4 - Industry - Structure''''Chiara SalaNo ratings yet

- Topic 4. Marketing Information and ResearchDocument36 pagesTopic 4. Marketing Information and ResearchБогдана ВишнівськаNo ratings yet

- Digital Marketing Sem 4 QPDocument2 pagesDigital Marketing Sem 4 QPprathmeshNo ratings yet

- Microsoft Word - Business Analytics and IntelligenceDocument6 pagesMicrosoft Word - Business Analytics and IntelligenceHimungshu KashyapaNo ratings yet

- 17 Proven Instant Cost Reduction Ideas Chandan GoyalDocument56 pages17 Proven Instant Cost Reduction Ideas Chandan GoyalvedanshanaghNo ratings yet

- Starting A Bookkeeping Business1Document14 pagesStarting A Bookkeeping Business1Prisca Tembo100% (4)

- A Study On Consumer Decision Making in Sree Lakshmi Organic Cotton IndustriesDocument6 pagesA Study On Consumer Decision Making in Sree Lakshmi Organic Cotton IndustriesananthakumarNo ratings yet

- Arba Minch University College of Agricultural Sciences Department of Agribusiness and Value Chain ManagementDocument55 pagesArba Minch University College of Agricultural Sciences Department of Agribusiness and Value Chain Managementdursam328No ratings yet

- Best Hashtag Guide For Your Instagram PDFDocument10 pagesBest Hashtag Guide For Your Instagram PDFhow toNo ratings yet

- Red Bull Slide PDFDocument13 pagesRed Bull Slide PDFanny alfianti100% (1)

- Attempt All The Questions. Choose The Most Appropriate Answer (Eg. A, B, C, D and E) in The Answer Sheet Provided at The Back of The PaperDocument6 pagesAttempt All The Questions. Choose The Most Appropriate Answer (Eg. A, B, C, D and E) in The Answer Sheet Provided at The Back of The PaperAmy Lubis100% (2)

- International MKT AssignmentDocument5 pagesInternational MKT AssignmentEdmund AmissahNo ratings yet

- Managerial Economics 6e Paul Keat Philip K Young TBDocument158 pagesManagerial Economics 6e Paul Keat Philip K Young TBTerex ManualNo ratings yet

- Electronic Commerce, 12th Edition 9781305867819 Chapter 1 SolutionsDocument9 pagesElectronic Commerce, 12th Edition 9781305867819 Chapter 1 SolutionsAcilegna Amba-an CruzNo ratings yet

- 973 1434 2 PBDocument12 pages973 1434 2 PBDewa AdnyanaNo ratings yet

- Week 4 - Ch. 4 Key TermsDocument3 pagesWeek 4 - Ch. 4 Key TermsRobyn ShirvanNo ratings yet

- CHAPTER-11 Case StudiesDocument21 pagesCHAPTER-11 Case StudiesHate MeNo ratings yet

- Supply Chain ManagementDocument15 pagesSupply Chain ManagementAahil RazaNo ratings yet

- 05 Activity 1 Strategic ManagementDocument1 page05 Activity 1 Strategic ManagementZia NnhaaaNo ratings yet

- Market Structure & CompetitionDocument19 pagesMarket Structure & CompetitionVaibhav YadavNo ratings yet

- FMCG Companies in IndiaDocument7 pagesFMCG Companies in IndiaAnuj KumarNo ratings yet

- HRM Assignment, SHIVANI17BBA080Document3 pagesHRM Assignment, SHIVANI17BBA080Shivani DahiyaNo ratings yet

- Homescan: CPS Module 2Document34 pagesHomescan: CPS Module 2mithunrecdgp100% (1)

- 4 Types of Marketing ChannelsDocument3 pages4 Types of Marketing Channelsaqiilah subrotoNo ratings yet

- Customer Trends: Opportunities For Coty Inc. - External Strategic FactorsDocument11 pagesCustomer Trends: Opportunities For Coty Inc. - External Strategic FactorsWongsatorn WorakittikulNo ratings yet