Download as docx, pdf, or txt

You might also like

- MV3A - Incident DescriptionDocument3 pagesMV3A - Incident DescriptionSreekanth Reddy GoliNo ratings yet

- Ratio Analysis - 10 Questions ExerciseDocument10 pagesRatio Analysis - 10 Questions ExerciseSaralita NairNo ratings yet

- Chapter 2 - Income Statement QuestionsDocument3 pagesChapter 2 - Income Statement QuestionsMuntasir Ahmmed0% (1)

- Cost QB PDFDocument300 pagesCost QB PDFHuzaifa Muhammad80% (5)

- EPS Practice ProblemsDocument8 pagesEPS Practice ProblemsmikeNo ratings yet

- Ratio Analysis Notes and Practice Questions With SolutionsDocument23 pagesRatio Analysis Notes and Practice Questions With SolutionsAnkith Poojary71% (7)

- Chapter - 2 - Exercise & Problems ANSWERSDocument5 pagesChapter - 2 - Exercise & Problems ANSWERSFahad Mushtaq100% (2)

- Accounting Equation - Problems & SolutionsDocument25 pagesAccounting Equation - Problems & Solutionsgag9075% (4)

- Manufacturing Accounts NotesDocument9 pagesManufacturing Accounts NotesFarrukhsg100% (5)

- Principle of Accounting Notes PDFDocument22 pagesPrinciple of Accounting Notes PDFFahad Rizwan80% (5)

- Voucher System, Special Journals, and Subsidiary LedgersDocument9 pagesVoucher System, Special Journals, and Subsidiary LedgersCatherine Calero50% (2)

- 08-Rectification-Of-Errors Good OneDocument54 pages08-Rectification-Of-Errors Good OneAejaz MohamedNo ratings yet

- Trial Balance Problems and Solutions - Accountancy KnowledgeDocument8 pagesTrial Balance Problems and Solutions - Accountancy KnowledgeSanjay Godara100% (1)

- Exercise On Adjusting Entries Trial BalanceDocument5 pagesExercise On Adjusting Entries Trial Balancemarvin fajardo100% (1)

- Inventory Valuation-ProblemsDocument3 pagesInventory Valuation-ProblemsKaran100% (1)

- Trading Account & P&L Account QuestionsDocument2 pagesTrading Account & P&L Account QuestionsMrAlexander83% (12)

- Exercise - Accounting - Worksheet - Historia CompanyDocument15 pagesExercise - Accounting - Worksheet - Historia Companytristan ignatiusNo ratings yet

- Exercise 1 - Transaction AnalysisDocument2 pagesExercise 1 - Transaction AnalysistmhoangvnaNo ratings yet

- Accounting Income StatementDocument5 pagesAccounting Income Statementjane100% (1)

- 6 ProblemsDocument6 pages6 ProblemsAzelAnnAlibinNo ratings yet

- Problems On Cash Budget MBADocument3 pagesProblems On Cash Budget MBAsafwanhossain100% (1)

- Closing EntsDocument20 pagesClosing EntsEmma Ria100% (1)

- Problem 1:: Caf 1 Accounting EquationDocument7 pagesProblem 1:: Caf 1 Accounting EquationSerish ButtNo ratings yet

- Suspense Accounts and Error CorrectionDocument8 pagesSuspense Accounts and Error CorrectionAllzoommood100% (9)

- Statement of Financial Position - ANSWER KEYDocument3 pagesStatement of Financial Position - ANSWER KEYHennessy Shania Gallera Ardiente100% (2)

- Worksheet 2 Statement of Financial Position Question With SolutionDocument3 pagesWorksheet 2 Statement of Financial Position Question With SolutionNayaz EmamaulleeNo ratings yet

- Umer Solution 2Document21 pagesUmer Solution 2shoaiba1No ratings yet

- Corporate RestructuringDocument17 pagesCorporate RestructuringSantosh....No ratings yet

- Chapter 16 - Accounts From Incomplete Records-Single Entry SystemDocument27 pagesChapter 16 - Accounts From Incomplete Records-Single Entry SystemTru eduzoneNo ratings yet

- Assignment Questions For Financial StatementsDocument5 pagesAssignment Questions For Financial StatementsAejaz Mohamed100% (2)

- Examples of Trading and Profit and Loss Account and Balance SheetDocument5 pagesExamples of Trading and Profit and Loss Account and Balance SheetDada Lim100% (2)

- Kid - Questions and AnswerDocument4 pagesKid - Questions and AnswersurvivalofthepolyNo ratings yet

- Final Accounts - AdjustmentsDocument12 pagesFinal Accounts - AdjustmentsSarthak Gupta100% (2)

- CashFlowStatement AssignmentDocument15 pagesCashFlowStatement AssignmentAnanta Vishain0% (1)

- FAR MerchandisingDocument68 pagesFAR MerchandisingAira DavidNo ratings yet

- Chapter # 1: Accounting For Incomplete Records (Single Entry)Document24 pagesChapter # 1: Accounting For Incomplete Records (Single Entry)Umar Zahid100% (1)

- Correction of Errors (With Answers) : Step 1 Show CorrectionsDocument34 pagesCorrection of Errors (With Answers) : Step 1 Show Correctionsanga100% (1)

- FA Work BookDocument59 pagesFA Work BookUnais AhmedNo ratings yet

- Cost Sheet QuestionsDocument7 pagesCost Sheet QuestionsGurpreet Singh100% (1)

- Books of Original Entry and Ledgers (II) : Short QuestionsDocument16 pagesBooks of Original Entry and Ledgers (II) : Short QuestionsangaNo ratings yet

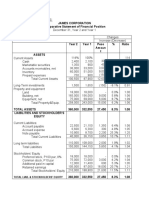

- Horizontal Analysis:: James Corporation Comparative Statement of Financial PositionDocument7 pagesHorizontal Analysis:: James Corporation Comparative Statement of Financial PositionJohn Francis IdananNo ratings yet

- Functional BudgetsDocument12 pagesFunctional Budgetsarjun sachdev100% (1)

- Problem 2-2: J.L. Gregory CompanyDocument5 pagesProblem 2-2: J.L. Gregory CompanyKAPIL MBA 2021-23 (Delhi)No ratings yet

- Exercises - Trial Balance and Final Accounts - PracticeDocument23 pagesExercises - Trial Balance and Final Accounts - PracticeDilfaraz Kalawat79% (38)

- Journal, Ledger, Subsidiary Books and Trial BalanceDocument16 pagesJournal, Ledger, Subsidiary Books and Trial Balancetmenterprise cbeNo ratings yet

- Trial Balance and Final Accounts ProblemsDocument6 pagesTrial Balance and Final Accounts Problemsbhanu.chandu100% (1)

- Assignment of Depreciation PDFDocument50 pagesAssignment of Depreciation PDFMuhammad Arslan0% (2)

- Problem 9-1: Net IncomeDocument16 pagesProblem 9-1: Net IncomeHerlyn Juvelle SevillaNo ratings yet

- IAS 2 Summary-MergedDocument19 pagesIAS 2 Summary-MergedShameel IrshadNo ratings yet

- Depreciation O Level NotesDocument5 pagesDepreciation O Level NotesBijoy SalahuddinNo ratings yet

- Financial Statements 24 Questions AnswersDocument6 pagesFinancial Statements 24 Questions AnswersGideon Turner100% (2)

- Level 12 Text Update June 20211Document110 pagesLevel 12 Text Update June 20211Swe Zin Thet100% (2)

- Numerical On Journal + Ledger + Trial BalanceDocument1 pageNumerical On Journal + Ledger + Trial BalanceyogeshNo ratings yet

- Chapter - 03 Final Accounts With AdjustmentsDocument114 pagesChapter - 03 Final Accounts With AdjustmentsAuthor Jyoti Prakash rath100% (1)

- Basic Journal Entry's2Document8 pagesBasic Journal Entry's2Venkatesh Babu100% (2)

- Bank Reconciliation QuestionsDocument14 pagesBank Reconciliation Questionsanga100% (1)

- ACC 557 Week 1 Chapter 1Document11 pagesACC 557 Week 1 Chapter 1acurashah100% (2)

- Basket Wonders' Balance Sheet (Asset Side)Document32 pagesBasket Wonders' Balance Sheet (Asset Side)OSAMA0% (1)

- Problem Set 1 SolutionsDocument15 pagesProblem Set 1 SolutionsCosta Andrea67% (3)

- Comprehensive ProblemDocument11 pagesComprehensive Problemapi-295660192No ratings yet

- 3rd Sem Finance True and False PDFDocument14 pages3rd Sem Finance True and False PDFMausam GhimireNo ratings yet

- Fundamentals of Accounting Notes 1Document18 pagesFundamentals of Accounting Notes 1deo omach67% (3)

- Intermediate: AccountingDocument76 pagesIntermediate: AccountingDieu NguyenNo ratings yet

- 104 CourseInfo Spring2019Document4 pages104 CourseInfo Spring2019mikeNo ratings yet

- 1 - Accounting Cycle Overview Practice ProblemsDocument5 pages1 - Accounting Cycle Overview Practice ProblemsmikeNo ratings yet

- Acct 2101 Fall 2019 SyllabusDocument8 pagesAcct 2101 Fall 2019 SyllabusmikeNo ratings yet

- JEdwards MGT202 Syllabus SP19 MWDocument5 pagesJEdwards MGT202 Syllabus SP19 MWmikeNo ratings yet

- 17 Merger Consequences b4 ClassDocument40 pages17 Merger Consequences b4 ClassmikeNo ratings yet

- Revenue Practice ProblemsDocument9 pagesRevenue Practice ProblemsmikeNo ratings yet

- Profitability Practice ProblemsDocument5 pagesProfitability Practice ProblemsmikeNo ratings yet

- Financial Accounting: Tools For Business Decision Making: Reporting and Analyzing ReceivablesDocument60 pagesFinancial Accounting: Tools For Business Decision Making: Reporting and Analyzing ReceivablesmikeNo ratings yet

- Exam 1A (1) Chem GTDocument5 pagesExam 1A (1) Chem GTmikeNo ratings yet

- Tangible Practice ProblemsDocument11 pagesTangible Practice ProblemsmikeNo ratings yet

- Inventory Practice ProblemsDocument14 pagesInventory Practice ProblemsmikeNo ratings yet

- Investment Practice ProblemsDocument14 pagesInvestment Practice ProblemsmikeNo ratings yet

- Taxes Practice ProblemsDocument10 pagesTaxes Practice ProblemsmikeNo ratings yet

- Debt Practice ProblemsDocument11 pagesDebt Practice ProblemsmikeNo ratings yet

- Intentional Injuries: SuicideDocument10 pagesIntentional Injuries: SuicideJaze CelosNo ratings yet

- RealEstate SingaporeDocument2 pagesRealEstate SingaporeKyaw Kyaw AungNo ratings yet

- 1 PETER-review QuestionsDocument2 pages1 PETER-review QuestionsJoanna CortesNo ratings yet

- Outline of Topics Taxation Law Review IvDocument6 pagesOutline of Topics Taxation Law Review IvervingabralagbonNo ratings yet

- Power Up MocoDocument7 pagesPower Up MocoParents' Coalition of Montgomery County, MarylandNo ratings yet

- Blank Lease ApplicationDocument4 pagesBlank Lease ApplicationNema GhNo ratings yet

- G.R. No. L-39598Document15 pagesG.R. No. L-39598Heloise yooNo ratings yet

- Dr. Bacchiocchi, The Sabbath, and The Writings of Paul - Kerry WynneDocument19 pagesDr. Bacchiocchi, The Sabbath, and The Writings of Paul - Kerry WynneRubem_CLNo ratings yet

- 323 Ta Aerosil200 PDFDocument2 pages323 Ta Aerosil200 PDFelektron2010No ratings yet

- Correlli Barnett - The American ConservativeDocument3 pagesCorrelli Barnett - The American ConservativeAlexNo ratings yet

- Mary Es Mi Amor: Leo Dan Prof. Alvaro BarriosDocument2 pagesMary Es Mi Amor: Leo Dan Prof. Alvaro BarriosAlvaroBarriosSalasNo ratings yet

- Tafseer Mariful Quran Sura 109 Al Kafirun English Translation PDFDocument6 pagesTafseer Mariful Quran Sura 109 Al Kafirun English Translation PDFamaanking8bpNo ratings yet

- Ye Dharmā HetuprabhavaDocument3 pagesYe Dharmā HetuprabhavaProkhor PetrovNo ratings yet

- Problem Solving: A: Purchasing 20% Capital Which of The Following Statements Is Correct?Document6 pagesProblem Solving: A: Purchasing 20% Capital Which of The Following Statements Is Correct?Actg SolmanNo ratings yet

- Law of Evidence - Important Question (2018-2022)Document8 pagesLaw of Evidence - Important Question (2018-2022)stevin.john538No ratings yet

- In Sunny SpainDocument3 pagesIn Sunny SpainAnonymous ht2L8xP100% (1)

- People vs. LovedioroDocument16 pagesPeople vs. LovedioroChristopher Julian ArellanoNo ratings yet

- Andhra Pradesh Grama - Ward SachivalayamDocument1 pageAndhra Pradesh Grama - Ward SachivalayamVenkatesh TatikondaNo ratings yet

- Milanowski, Todd v. SpeedplayDocument6 pagesMilanowski, Todd v. SpeedplayPriorSmartNo ratings yet

- Labor Standards Case Digests - Nina Beleen CastilloDocument18 pagesLabor Standards Case Digests - Nina Beleen CastilloNina CastilloNo ratings yet

- Weimer, D.L. Vining, A.R. Policy Analysis Concepts & Practice in Policy Analysis Concepts (274-279)Document8 pagesWeimer, D.L. Vining, A.R. Policy Analysis Concepts & Practice in Policy Analysis Concepts (274-279)HM KNo ratings yet

- Investment AlternativesDocument19 pagesInvestment AlternativesJagrityTalwarNo ratings yet

- Arce Vs Capital InsuranceDocument1 pageArce Vs Capital InsurancePam Otic-ReyesNo ratings yet

- SECURITY or PHYSICAL SECURITY or RISK ASSESSMENTDocument3 pagesSECURITY or PHYSICAL SECURITY or RISK ASSESSMENTapi-1216271390% (1)

- Chemical Checkpoints: Department of Occupational Safety and HealthDocument13 pagesChemical Checkpoints: Department of Occupational Safety and HealthpsssNo ratings yet

- Simple Harmonic MotionDocument40 pagesSimple Harmonic MotionHarshNo ratings yet

- Easy Education Loan DetailsDocument3 pagesEasy Education Loan Detailsayusht7iNo ratings yet

- Agenda 21 Roll Back ManualDocument12 pagesAgenda 21 Roll Back ManualAnna MorkeskiNo ratings yet