Download as pdf or txt

You might also like

- UAPL Invoice PDFDocument1 pageUAPL Invoice PDFasim_kaleemNo ratings yet

- VN Insurance Market Research and Competitor Analysis 2020 PDFDocument47 pagesVN Insurance Market Research and Competitor Analysis 2020 PDFHoàng NM LêNo ratings yet

- Vietnam Consumer Report 2019Document88 pagesVietnam Consumer Report 2019Eric PhanNo ratings yet

- Senate SAFE Banking ActDocument30 pagesSenate SAFE Banking ActMarijuana MomentNo ratings yet

- Auditing The Financing/Investing Process: Cash and InvestmentsDocument22 pagesAuditing The Financing/Investing Process: Cash and InvestmentsasmaNo ratings yet

- IE CGC Money-and-Trust SPAIN 2020Document16 pagesIE CGC Money-and-Trust SPAIN 2020Humanidades DigitalesNo ratings yet

- IE CGC Money-and-Trust GERMANY 2020Document16 pagesIE CGC Money-and-Trust GERMANY 2020Humanidades DigitalesNo ratings yet

- Policy Note: PN 2104: Labour Market Dynamics in Bangladesh: Impact of The COVID-19Document10 pagesPolicy Note: PN 2104: Labour Market Dynamics in Bangladesh: Impact of The COVID-19Sanjida AhmedNo ratings yet

- Class 6Document75 pagesClass 6Христина ЯблоньNo ratings yet

- IBON - Budget 2010 (Notes) 0909-17Document42 pagesIBON - Budget 2010 (Notes) 0909-17mobilemauiNo ratings yet

- Banking & Insurance OverviewDocument28 pagesBanking & Insurance OverviewbharatNo ratings yet

- Balanz Capital 232 Province of Mendoza. Ongoing Solid Fiscal Consolidation EffortDocument6 pagesBalanz Capital 232 Province of Mendoza. Ongoing Solid Fiscal Consolidation EffortGabriel ConteNo ratings yet

- CDN Century UWindsor-2010!03!18Document42 pagesCDN Century UWindsor-2010!03!18RPCIncNo ratings yet

- Pop Dev Review Material Vol. 1 2023Document71 pagesPop Dev Review Material Vol. 1 2023Arlyn AyagNo ratings yet

- Economic Outlook Presentation To Senate - 05!26!2020Document19 pagesEconomic Outlook Presentation To Senate - 05!26!2020Russ LatinoNo ratings yet

- Budgets of The Economy of PakistanDocument33 pagesBudgets of The Economy of Pakistanhaseeb zainNo ratings yet

- How Does Aid Support Womens Economic Empowerment 2021Document7 pagesHow Does Aid Support Womens Economic Empowerment 2021Glaiza Veluz-SulitNo ratings yet

- Valuations Amidst The COVID-19 Pandemic & Significant Economic UncertaintiesDocument19 pagesValuations Amidst The COVID-19 Pandemic & Significant Economic Uncertaintiesikhan809No ratings yet

- Onthly Utlook: U.S. Overview International OverviewDocument6 pagesOnthly Utlook: U.S. Overview International OverviewInternational Business TimesNo ratings yet

- Chile's Public Finances in The Context of The Pandemic July 2021Document24 pagesChile's Public Finances in The Context of The Pandemic July 2021Ian Carrasco TufinoNo ratings yet

- Morocco-EU Trade Relations: January 2009Document17 pagesMorocco-EU Trade Relations: January 2009Pablo QuintanaNo ratings yet

- Jobless GrowthDocument13 pagesJobless GrowthApurva JhaNo ratings yet

- Analysis of Chile.Document23 pagesAnalysis of Chile.Estefanía Cardona UsmaNo ratings yet

- FY 19 Budget Overview 3818Document83 pagesFY 19 Budget Overview 3818Chris SwamNo ratings yet

- Brazil Vs Costa RicaDocument10 pagesBrazil Vs Costa RicaChaiNo ratings yet

- Applied Assignment Joseph - 031031Document4 pagesApplied Assignment Joseph - 031031Joseph OkpaNo ratings yet

- Power Situation in Lagos 2021Document10 pagesPower Situation in Lagos 2021simonNo ratings yet

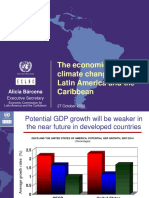

- The Economics of Climate Change in Latin America and The CaribbeanDocument23 pagesThe Economics of Climate Change in Latin America and The Caribbeanknowledge3736 jNo ratings yet

- Global Macro - Brazil Currency Crisi (12!01!09)Document2 pagesGlobal Macro - Brazil Currency Crisi (12!01!09)Vitor KHNo ratings yet

- CS-22-State of The WC Market-1Document26 pagesCS-22-State of The WC Market-1Stanley WangNo ratings yet

- Spanish Treasury Chart Pack: April 2022Document81 pagesSpanish Treasury Chart Pack: April 2022andres rebosoNo ratings yet

- Chicago City Treasurer: 2018 Q2 Earnings CallDocument29 pagesChicago City Treasurer: 2018 Q2 Earnings CallTreasurerSummersArchiveNo ratings yet

- Latam Investment Banking Review q1 2021Document18 pagesLatam Investment Banking Review q1 2021Fernando Cano WongNo ratings yet

- Chart PackDocument83 pagesChart PackDksndNo ratings yet

- Panama Research PaperDocument6 pagesPanama Research PaperSeanLejeeBajanNo ratings yet

- The Use of Financial Inclusion Data Country Case Study - MexicoDocument10 pagesThe Use of Financial Inclusion Data Country Case Study - Mexicosantiagous2No ratings yet

- Greenwood - Scharfstein - 2013 - The Growth of FinanceDocument26 pagesGreenwood - Scharfstein - 2013 - The Growth of FinanceBárbara AliagaNo ratings yet

- ch06Document8 pagesch06nepalman2023No ratings yet

- Headway (Academic Skills) : Sudaf MuhammadDocument2 pagesHeadway (Academic Skills) : Sudaf MuhammadSudaf MuhammadNo ratings yet

- Revenue Statistics Asia and Pacific PhilippinesDocument2 pagesRevenue Statistics Asia and Pacific Philippinesbry christianNo ratings yet

- WPS5316 (1) - Part-4Document7 pagesWPS5316 (1) - Part-4Enzo van der SluijsNo ratings yet

- AMERCO Finance Slides 2021Document24 pagesAMERCO Finance Slides 2021Daniel KwanNo ratings yet

- 2011 - UOL - Monetary EconsDocument15 pages2011 - UOL - Monetary EconsAaron ChiaNo ratings yet

- Highlights of Monitary Policy 2020Document15 pagesHighlights of Monitary Policy 2020Raushan KumarNo ratings yet

- Mohieldin - Industrial Policy in A Fast Changing World - February 2021Document48 pagesMohieldin - Industrial Policy in A Fast Changing World - February 2021AKNo ratings yet

- Customer Goods Guide PDFDocument40 pagesCustomer Goods Guide PDFmuthiaNo ratings yet

- Namibia Q3 GDP 2023Document10 pagesNamibia Q3 GDP 2023Enos McManni IVNo ratings yet

- Topics in International Macroeconomics Lecture 2: International Financial Crises and Regulation of Capital FlowsDocument42 pagesTopics in International Macroeconomics Lecture 2: International Financial Crises and Regulation of Capital FlowsKadirNo ratings yet

- Sesi 7. Trade and Investment in Practice - Verico - K - PDocument60 pagesSesi 7. Trade and Investment in Practice - Verico - K - PSlvi IlvniNo ratings yet

- The Sixty-Year Downward Trend of Economi PDFDocument20 pagesThe Sixty-Year Downward Trend of Economi PDFMarcus WilliamsNo ratings yet

- North South University: Economic Conditions of Bangladesh During 1972-2019Document16 pagesNorth South University: Economic Conditions of Bangladesh During 1972-2019Shoaib AhmedNo ratings yet

- Annual Report 202021Document128 pagesAnnual Report 202021AiswaryaNo ratings yet

- External Debt Development and Management: Presentations On IndiaDocument22 pagesExternal Debt Development and Management: Presentations On IndiaYasser KhanNo ratings yet

- Reactivation After Covid19Document21 pagesReactivation After Covid19euro.rep7117No ratings yet

- Monetary Policy During The Past 30 Years With Lessons For The Next 30 Years CATOFall2013Document13 pagesMonetary Policy During The Past 30 Years With Lessons For The Next 30 Years CATOFall2013Satish VirasNo ratings yet

- Annual Letter 2016Document25 pagesAnnual Letter 2016Incandescent CapitalNo ratings yet

- Bridged Network Whitepaper ENDocument27 pagesBridged Network Whitepaper ENTriadi Akbar WijayaNo ratings yet

- Class 7Document64 pagesClass 7Христина ЯблоньNo ratings yet

- For Student 15Document15 pagesFor Student 15sunil kumarNo ratings yet

- Q1 2020-21 Fact Sheet PDFDocument27 pagesQ1 2020-21 Fact Sheet PDFJose CANo ratings yet

- Impact of Covid-19 On Banking in IndiaDocument19 pagesImpact of Covid-19 On Banking in IndiaAakash MalhotraNo ratings yet

- 2020 - An - Inflection - Point - in - Global - Corporate - TaxDocument12 pages2020 - An - Inflection - Point - in - Global - Corporate - Taxds2084No ratings yet

- Morocco's Jobs Landscape: Identifying Constraints to an Inclusive Labor MarketFrom EverandMorocco's Jobs Landscape: Identifying Constraints to an Inclusive Labor MarketNo ratings yet

- Apocalypse NowDocument145 pagesApocalypse NowAkshay SrivastavaNo ratings yet

- Common Sense: Senso Comune, in The Notebooks, Is That Accumulation of Taken-For - GrantedDocument16 pagesCommon Sense: Senso Comune, in The Notebooks, Is That Accumulation of Taken-For - GrantedHumanidades DigitalesNo ratings yet

- Molotch, Harvey - The City As A Growth Machine Toward A Political Economy of PlaceDocument24 pagesMolotch, Harvey - The City As A Growth Machine Toward A Political Economy of PlaceHumanidades DigitalesNo ratings yet

- Bitcoin SimmelDocument14 pagesBitcoin SimmelHumanidades DigitalesNo ratings yet

- Till-Peters From Blockchain Technology To Global Health EquityDocument7 pagesTill-Peters From Blockchain Technology To Global Health EquityHumanidades DigitalesNo ratings yet

- Heynen - HHintern - Space As Receptor, Instrument or Stage Interaction Between Spatial and Social ConstellationsDocument18 pagesHeynen - HHintern - Space As Receptor, Instrument or Stage Interaction Between Spatial and Social ConstellationsHumanidades DigitalesNo ratings yet

- IE CGC Money-and-Trust GERMANY 2020Document16 pagesIE CGC Money-and-Trust GERMANY 2020Humanidades DigitalesNo ratings yet

- Position Paper German Banks Say: The Economy Needs A Programmable Digital Euro!Document19 pagesPosition Paper German Banks Say: The Economy Needs A Programmable Digital Euro!Humanidades DigitalesNo ratings yet

- Llewellyn - Digital-Money-Readiness IndexDocument40 pagesLlewellyn - Digital-Money-Readiness IndexHumanidades DigitalesNo ratings yet

- IE CGC Money-and-Trust SPAIN 2020Document16 pagesIE CGC Money-and-Trust SPAIN 2020Humanidades DigitalesNo ratings yet

- IE CGC Money and Trust Argentina 2020Document17 pagesIE CGC Money and Trust Argentina 2020Humanidades DigitalesNo ratings yet

- Bell Assassination PoliticsDocument31 pagesBell Assassination PoliticsHumanidades DigitalesNo ratings yet

- BIS-CPSS Electronic MoneyDocument112 pagesBIS-CPSS Electronic MoneyHumanidades DigitalesNo ratings yet

- UK Money Markets CodeDocument44 pagesUK Money Markets CodeHumanidades DigitalesNo ratings yet

- 547f68fde4b029305d9c1f1c Twolsey5 1417636145991 ConsumermathafinalexamstudyguideDocument12 pages547f68fde4b029305d9c1f1c Twolsey5 1417636145991 Consumermathafinalexamstudyguidewoodlandsoup70% (1)

- "A COMPARATIVE STUDY ON INVESTMENT BANKING INDIA by Pradeep Jariwal For More Topics Call 8233116967Document93 pages"A COMPARATIVE STUDY ON INVESTMENT BANKING INDIA by Pradeep Jariwal For More Topics Call 8233116967Pradeep N Sheetal0% (1)

- Nan Mudhalvan Content Full PDFDocument15 pagesNan Mudhalvan Content Full PDFSwethaNo ratings yet

- Agrani Bank Limited: Wasa Corp. Branch4786Document2 pagesAgrani Bank Limited: Wasa Corp. Branch4786farjana khatun0% (1)

- NetbankDocument3 pagesNetbankjambroo100% (1)

- Sbi Homeloan ProjectDocument63 pagesSbi Homeloan Projectrncreation &photoghraphyNo ratings yet

- Account Statement - Mar 31, 2021Document7 pagesAccount Statement - Mar 31, 2021Clifton WilsonNo ratings yet

- AbhiiiiiiDocument17 pagesAbhiiiiiigpolytechnicmauNo ratings yet

- Banking Awareness Hand Book by Er. G C Nayak PDFDocument86 pagesBanking Awareness Hand Book by Er. G C Nayak PDFTapas Kumar NandiNo ratings yet

- Crystal Microfinance ProjectDocument18 pagesCrystal Microfinance ProjectShashi Kanth Sahni100% (2)

- MPU 3482 Personal Finance Management Individual Assignment 1Document9 pagesMPU 3482 Personal Finance Management Individual Assignment 1PoogensNo ratings yet

- Loan Calculator With Extra PaymentsDocument2,415 pagesLoan Calculator With Extra PaymentsRst BruneiNo ratings yet

- In The Event of Coming Up With Edition of Principles & Practices of BANKING We Have Made Following Changes in The Edition BookDocument21 pagesIn The Event of Coming Up With Edition of Principles & Practices of BANKING We Have Made Following Changes in The Edition BookdhirajNo ratings yet

- EMS Project On SARBDocument2 pagesEMS Project On SARBMichael-John ReelerNo ratings yet

- Í N Zcè Yalung Ma - Âluzâââââââ C Ç4) $83, Î Mrs. Ma. Luz Cura YalungDocument7 pagesÍ N Zcè Yalung Ma - Âluzâââââââ C Ç4) $83, Î Mrs. Ma. Luz Cura YalungKevin YalungNo ratings yet

- Mpesa Data KenyaDocument18 pagesMpesa Data KenyaagweyoNo ratings yet

- 2nd Quiz Simple InterestDocument6 pages2nd Quiz Simple InterestVanessaNo ratings yet

- Real Estate Principles Real Estate: An Introduction To The ProfessionDocument13 pagesReal Estate Principles Real Estate: An Introduction To The Professiondenden007No ratings yet

- Deutsche Bank Ag - 2023 02 21Document6 pagesDeutsche Bank Ag - 2023 02 21Nuria PuenteNo ratings yet

- Final ProjectDocument42 pagesFinal ProjectAnonymous g7uPednINo ratings yet

- Kibor RatesDocument282 pagesKibor Ratesbhimani1981100% (3)

- CA CPT Fundamentals of Accounting PPT Bills of Exchange and Promissory Notes Part 1Document21 pagesCA CPT Fundamentals of Accounting PPT Bills of Exchange and Promissory Notes Part 1Palani Muthusamy100% (1)

- Project Development and Land Development in BangladeshDocument11 pagesProject Development and Land Development in BangladeshShahriar AzadNo ratings yet

- Blank Sample LedgerDocument4 pagesBlank Sample LedgerABDUL FAHEEMNo ratings yet

- Ibs Lahad Datu 1 31/12/23Document4 pagesIbs Lahad Datu 1 31/12/23fidatulsyafikahsamsualam12No ratings yet

- Credit FunctionDocument19 pagesCredit FunctionPrincess Di BaykingNo ratings yet