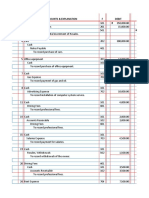

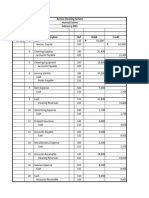

Accounting Assignment 10

Accounting Assignment 10

You might also like

- AHM13e - Chapter 01 - Key To EOC Problems and CasesDocument14 pagesAHM13e - Chapter 01 - Key To EOC Problems and CasesArunesh SN100% (1)

- Chapter 08Document26 pagesChapter 08Dan ChuaNo ratings yet

- Laurent e Answer KeyDocument4 pagesLaurent e Answer KeyZee Santisas86% (7)

- Tan, Vanessa Juventia Aurelia Dinata 2440031572 LG24-IBMDocument6 pagesTan, Vanessa Juventia Aurelia Dinata 2440031572 LG24-IBMvanessaNo ratings yet

- Case 33 PresentationDocument25 pagesCase 33 PresentationCh M Imran100% (2)

- Karima Sabilla Al HaqDocument2 pagesKarima Sabilla Al HaqNorazlina FitriahNo ratings yet

- Chap7 QuizDocument7 pagesChap7 QuizGracey DoyuganNo ratings yet

- Accounting 02182021Document4 pagesAccounting 02182021badNo ratings yet

- Nomor 1: Gain From Bargain Purchase $ - 9,000Document3 pagesNomor 1: Gain From Bargain Purchase $ - 9,000Sherlin KhuNo ratings yet

- Partnership FormationDocument5 pagesPartnership FormationIce Voltaire Buban GuiangNo ratings yet

- Pa 1Document4 pagesPa 1Aditya DzikirNo ratings yet

- Tugas Pertemuan 4Document6 pagesTugas Pertemuan 4Muhammad Musaid Rafii MaradityaNo ratings yet

- Assignment 1 Accounting Cycle For Service Business Part 2Document3 pagesAssignment 1 Accounting Cycle For Service Business Part 2Iya GarciaNo ratings yet

- Fabm Sample Exercises With Answer KeyDocument7 pagesFabm Sample Exercises With Answer KeySg Dimz100% (1)

- General JournalDocument5 pagesGeneral Journal૨εƒ XianNo ratings yet

- General JournalDocument5 pagesGeneral Journal૨εƒ XianNo ratings yet

- General JournalDocument5 pagesGeneral Journalmonicaaa melianaaaNo ratings yet

- Problem #1: Adjusting EntriesDocument5 pagesProblem #1: Adjusting EntriesShahzad AsifNo ratings yet

- Comp 2 Activity 5 SUPER FINAL1Document11 pagesComp 2 Activity 5 SUPER FINAL1Jhon Lester MagarsoNo ratings yet

- Accounting Question-With AnswerDocument5 pagesAccounting Question-With AnswerApanar OoNo ratings yet

- Class Project - November - HomeworkDocument13 pagesClass Project - November - HomeworkMarcoNo ratings yet

- Jurnal 1Document8 pagesJurnal 1William MangumbanNo ratings yet

- Module - WorksheetDocument2 pagesModule - WorksheetKae Abegail GarciaNo ratings yet

- Amaliya Quiz Tutor Finacc 1 Week 2Document8 pagesAmaliya Quiz Tutor Finacc 1 Week 2Amaliya MalikovaNo ratings yet

- Chintia Novrianti 3c Lat 12 RevDocument6 pagesChintia Novrianti 3c Lat 12 RevShintia NovriantiNo ratings yet

- Class Project - SolvedDocument8 pagesClass Project - SolvedMarcoNo ratings yet

- Lat 7 Knight&lesserDocument5 pagesLat 7 Knight&lesserNadratul Hasanah LubisNo ratings yet

- Exercises Chapter 2 Group 4Document8 pagesExercises Chapter 2 Group 4Phạm Ngọc Uyên NhiNo ratings yet

- DBM Corporation-Acco CycleDocument9 pagesDBM Corporation-Acco CycleJasmine ActaNo ratings yet

- Date Januar y Accounts Title Description P R Debts CreditDocument3 pagesDate Januar y Accounts Title Description P R Debts CreditMariel Samonte VillanuevaNo ratings yet

- WAC Service TheaterDocument48 pagesWAC Service TheaterJasmine ActaNo ratings yet

- HUM 121assignment 1Document6 pagesHUM 121assignment 1Nayeem HossainNo ratings yet

- Audit QuizDocument5 pagesAudit QuizCatherine Dela VegaNo ratings yet

- Answer To Sample Question 2Document3 pagesAnswer To Sample Question 2Farid AbbasovNo ratings yet

- Accouncting ProblemDocument3 pagesAccouncting ProblemShaneNo ratings yet

- Budget Driving Institute Prob 2&3Document94 pagesBudget Driving Institute Prob 2&3Ma Sophia Mikaela EreceNo ratings yet

- General Journal 1: Item Account Titles and Explanation Dr. CRDocument9 pagesGeneral Journal 1: Item Account Titles and Explanation Dr. CRJhoy AmoscoNo ratings yet

- ACR4.3 Cindy QaaniaDocument4 pagesACR4.3 Cindy QaaniaIndrian Sibi todingNo ratings yet

- Accounting Module 2 AnswerDocument5 pagesAccounting Module 2 AnswerMariel Mae MoralesNo ratings yet

- Boat BizDocument30 pagesBoat BizChernor Sulaiman BarrieNo ratings yet

- Sample ProblemDocument4 pagesSample ProblemENIDNo ratings yet

- Cho Cho's - SarayDocument6 pagesCho Cho's - SarayLaiza Cristella SarayNo ratings yet

- Bakhromov hw2 PDFDocument4 pagesBakhromov hw2 PDFRakhimjon BakhromovNo ratings yet

- Far Activity LavadoDocument14 pagesFar Activity LavadoPamela AbenirNo ratings yet

- Accounting Homework 2-12-2024 FINALDocument6 pagesAccounting Homework 2-12-2024 FINALsamiramellaneoNo ratings yet

- Cae 1Document4 pagesCae 1stonefiona6No ratings yet

- T Accounts Trial BalanceDocument7 pagesT Accounts Trial BalanceCamille Pasion100% (1)

- Accounting Cycle WorksheetDocument11 pagesAccounting Cycle Worksheettarikuabdisa0No ratings yet

- SEATWORK6Document6 pagesSEATWORK6dumpanonymouslyNo ratings yet

- Buenafe, Melanie Joy P. Sbac-3D: Journal EntryDocument7 pagesBuenafe, Melanie Joy P. Sbac-3D: Journal EntryMelanie BuenafeNo ratings yet

- Perilla Geriqjoedn 1Document20 pagesPerilla Geriqjoedn 1Geriq Joeden PerillaNo ratings yet

- General Journal Date DebitDocument17 pagesGeneral Journal Date DebitMickaella VergaraNo ratings yet

- CHP 2 Exam Preparation ProblemsDocument3 pagesCHP 2 Exam Preparation ProblemsShawn JohnstonNo ratings yet

- Module 3 Chapter 7Document8 pagesModule 3 Chapter 7Angelie Bocala CatalanNo ratings yet

- Accounting TaskDocument10 pagesAccounting TaskSamuel Amon OkumuNo ratings yet

- Applied Auditing-Prelim FinalDocument3 pagesApplied Auditing-Prelim FinalDominic E. BoticarioNo ratings yet

- Date Account Titles & Explanation Debit Credit: A. Prepare EntriesDocument4 pagesDate Account Titles & Explanation Debit Credit: A. Prepare Entriesyogi fetriansyahNo ratings yet

- Comp 2 Activity 5Document13 pagesComp 2 Activity 5Jhon Lester MagarsoNo ratings yet

- Module 3 - EA03Document30 pagesModule 3 - EA03Vaseline QtipsNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Corporation Issuance of Shares Illutsrative ProblemDocument15 pagesCorporation Issuance of Shares Illutsrative ProblemHoney MuliNo ratings yet

- Asset Liability Management: in BanksDocument44 pagesAsset Liability Management: in Bankssachin21singhNo ratings yet

- Theory of Accounts - Cpa-ReviewerDocument10 pagesTheory of Accounts - Cpa-ReviewerHeart EspineliNo ratings yet

- REVTOA ReceivablesDocument5 pagesREVTOA ReceivablesJoanna Marie UrbienNo ratings yet

- Financial Ratio AnalysisDocument10 pagesFinancial Ratio AnalysisAnonymous ic2CDkFNo ratings yet

- TPL Annual Report 2013 2014Document66 pagesTPL Annual Report 2013 2014piraisudi013341No ratings yet

- DocxDocument9 pagesDocxReiah RongavillaNo ratings yet

- Ratio Reviewer 2Document15 pagesRatio Reviewer 2Edgar Lay60% (5)

- Mba Faaunit - IIDocument15 pagesMba Faaunit - IINaresh GuduruNo ratings yet

- Week 1 Topic Tutorial Solutions CB2100 - 1920ADocument6 pagesWeek 1 Topic Tutorial Solutions CB2100 - 1920ALily TsengNo ratings yet

- Topic 02 - Accounting EquationDocument22 pagesTopic 02 - Accounting EquationNorainah Abdul Gani0% (1)

- F1 - Financial OperationsDocument20 pagesF1 - Financial OperationsZHANG EmilyNo ratings yet

- Financial Ratios Topic (MFP 1) PDFDocument9 pagesFinancial Ratios Topic (MFP 1) PDFsrinivasa annamayyaNo ratings yet

- Financial Accounting and Reporting: IFRS - 2016 June QPDocument11 pagesFinancial Accounting and Reporting: IFRS - 2016 June QPMarchella LukitoNo ratings yet

- Discounted Cash Flow Analysis: CompanyDocument3 pagesDiscounted Cash Flow Analysis: Company/jncjdncjdnNo ratings yet

- 2022 ICTSI Balance Sheet Income Statement - pg.53Document1 page2022 ICTSI Balance Sheet Income Statement - pg.53loveartxoxo.commissionNo ratings yet

- Handouts 3 - CORPORATE LIQUIDATIONDocument7 pagesHandouts 3 - CORPORATE LIQUIDATIONcecille ramirezNo ratings yet

- FAC 1502 Tutorial Letter 101-2015 PDFDocument96 pagesFAC 1502 Tutorial Letter 101-2015 PDFVinny Hungwe0% (1)

- R12 Troubleshooting Misclassified Accounts in General Ledger (Doc ID 872162.1)Document10 pagesR12 Troubleshooting Misclassified Accounts in General Ledger (Doc ID 872162.1)obioraechezonaNo ratings yet

- Ethiopia International Public Sector Accounting Standards Latest UpdatesDocument8 pagesEthiopia International Public Sector Accounting Standards Latest UpdatesPhoenix Rising100% (1)

- 23 - Vol-1 - Issue-7 - Financial Statement Effect - WiproDocument20 pages23 - Vol-1 - Issue-7 - Financial Statement Effect - WiproKanav GuptaNo ratings yet

- Final Round - 1ST - QDocument6 pagesFinal Round - 1ST - QwivadaNo ratings yet

- Chapter Three: General Fund & Special Revenue Funds 3.1 General Fund IsDocument41 pagesChapter Three: General Fund & Special Revenue Funds 3.1 General Fund IsTamirat BashaaNo ratings yet

- Study Guide CH 12Document7 pagesStudy Guide CH 12Stephanie RobinsonNo ratings yet

- 1 Blank Model TemplateDocument28 pages1 Blank Model TemplateMasroor KhanNo ratings yet

- Assignment Intermediate Financial Accounting I - Rifky Mahendra - 1900012264.Document4 pagesAssignment Intermediate Financial Accounting I - Rifky Mahendra - 1900012264.Rahmat AlamsyahNo ratings yet

- Bsa 3101 - Accounting For Special Transactions Seatwork No. 2 InstructionsDocument2 pagesBsa 3101 - Accounting For Special Transactions Seatwork No. 2 InstructionsZihr EllerycNo ratings yet

- First Quarter Assessment in FABM2Document4 pagesFirst Quarter Assessment in FABM2Nhelben ManuelNo ratings yet

- Chapter 1 Problem 5 To 7Document2 pagesChapter 1 Problem 5 To 7XienaNo ratings yet

Download as pdf or txt

You might also like

- AHM13e - Chapter 01 - Key To EOC Problems and CasesDocument14 pagesAHM13e - Chapter 01 - Key To EOC Problems and CasesArunesh SN100% (1)

- Chapter 08Document26 pagesChapter 08Dan ChuaNo ratings yet

- Laurent e Answer KeyDocument4 pagesLaurent e Answer KeyZee Santisas86% (7)

- Tan, Vanessa Juventia Aurelia Dinata 2440031572 LG24-IBMDocument6 pagesTan, Vanessa Juventia Aurelia Dinata 2440031572 LG24-IBMvanessaNo ratings yet

- Case 33 PresentationDocument25 pagesCase 33 PresentationCh M Imran100% (2)

- Karima Sabilla Al HaqDocument2 pagesKarima Sabilla Al HaqNorazlina FitriahNo ratings yet

- Chap7 QuizDocument7 pagesChap7 QuizGracey DoyuganNo ratings yet

- Accounting 02182021Document4 pagesAccounting 02182021badNo ratings yet

- Nomor 1: Gain From Bargain Purchase $ - 9,000Document3 pagesNomor 1: Gain From Bargain Purchase $ - 9,000Sherlin KhuNo ratings yet

- Partnership FormationDocument5 pagesPartnership FormationIce Voltaire Buban GuiangNo ratings yet

- Pa 1Document4 pagesPa 1Aditya DzikirNo ratings yet

- Tugas Pertemuan 4Document6 pagesTugas Pertemuan 4Muhammad Musaid Rafii MaradityaNo ratings yet

- Assignment 1 Accounting Cycle For Service Business Part 2Document3 pagesAssignment 1 Accounting Cycle For Service Business Part 2Iya GarciaNo ratings yet

- Fabm Sample Exercises With Answer KeyDocument7 pagesFabm Sample Exercises With Answer KeySg Dimz100% (1)

- General JournalDocument5 pagesGeneral Journal૨εƒ XianNo ratings yet

- General JournalDocument5 pagesGeneral Journal૨εƒ XianNo ratings yet

- General JournalDocument5 pagesGeneral Journalmonicaaa melianaaaNo ratings yet

- Problem #1: Adjusting EntriesDocument5 pagesProblem #1: Adjusting EntriesShahzad AsifNo ratings yet

- Comp 2 Activity 5 SUPER FINAL1Document11 pagesComp 2 Activity 5 SUPER FINAL1Jhon Lester MagarsoNo ratings yet

- Accounting Question-With AnswerDocument5 pagesAccounting Question-With AnswerApanar OoNo ratings yet

- Class Project - November - HomeworkDocument13 pagesClass Project - November - HomeworkMarcoNo ratings yet

- Jurnal 1Document8 pagesJurnal 1William MangumbanNo ratings yet

- Module - WorksheetDocument2 pagesModule - WorksheetKae Abegail GarciaNo ratings yet

- Amaliya Quiz Tutor Finacc 1 Week 2Document8 pagesAmaliya Quiz Tutor Finacc 1 Week 2Amaliya MalikovaNo ratings yet

- Chintia Novrianti 3c Lat 12 RevDocument6 pagesChintia Novrianti 3c Lat 12 RevShintia NovriantiNo ratings yet

- Class Project - SolvedDocument8 pagesClass Project - SolvedMarcoNo ratings yet

- Lat 7 Knight&lesserDocument5 pagesLat 7 Knight&lesserNadratul Hasanah LubisNo ratings yet

- Exercises Chapter 2 Group 4Document8 pagesExercises Chapter 2 Group 4Phạm Ngọc Uyên NhiNo ratings yet

- DBM Corporation-Acco CycleDocument9 pagesDBM Corporation-Acco CycleJasmine ActaNo ratings yet

- Date Januar y Accounts Title Description P R Debts CreditDocument3 pagesDate Januar y Accounts Title Description P R Debts CreditMariel Samonte VillanuevaNo ratings yet

- WAC Service TheaterDocument48 pagesWAC Service TheaterJasmine ActaNo ratings yet

- HUM 121assignment 1Document6 pagesHUM 121assignment 1Nayeem HossainNo ratings yet

- Audit QuizDocument5 pagesAudit QuizCatherine Dela VegaNo ratings yet

- Answer To Sample Question 2Document3 pagesAnswer To Sample Question 2Farid AbbasovNo ratings yet

- Accouncting ProblemDocument3 pagesAccouncting ProblemShaneNo ratings yet

- Budget Driving Institute Prob 2&3Document94 pagesBudget Driving Institute Prob 2&3Ma Sophia Mikaela EreceNo ratings yet

- General Journal 1: Item Account Titles and Explanation Dr. CRDocument9 pagesGeneral Journal 1: Item Account Titles and Explanation Dr. CRJhoy AmoscoNo ratings yet

- ACR4.3 Cindy QaaniaDocument4 pagesACR4.3 Cindy QaaniaIndrian Sibi todingNo ratings yet

- Accounting Module 2 AnswerDocument5 pagesAccounting Module 2 AnswerMariel Mae MoralesNo ratings yet

- Boat BizDocument30 pagesBoat BizChernor Sulaiman BarrieNo ratings yet

- Sample ProblemDocument4 pagesSample ProblemENIDNo ratings yet

- Cho Cho's - SarayDocument6 pagesCho Cho's - SarayLaiza Cristella SarayNo ratings yet

- Bakhromov hw2 PDFDocument4 pagesBakhromov hw2 PDFRakhimjon BakhromovNo ratings yet

- Far Activity LavadoDocument14 pagesFar Activity LavadoPamela AbenirNo ratings yet

- Accounting Homework 2-12-2024 FINALDocument6 pagesAccounting Homework 2-12-2024 FINALsamiramellaneoNo ratings yet

- Cae 1Document4 pagesCae 1stonefiona6No ratings yet

- T Accounts Trial BalanceDocument7 pagesT Accounts Trial BalanceCamille Pasion100% (1)

- Accounting Cycle WorksheetDocument11 pagesAccounting Cycle Worksheettarikuabdisa0No ratings yet

- SEATWORK6Document6 pagesSEATWORK6dumpanonymouslyNo ratings yet

- Buenafe, Melanie Joy P. Sbac-3D: Journal EntryDocument7 pagesBuenafe, Melanie Joy P. Sbac-3D: Journal EntryMelanie BuenafeNo ratings yet

- Perilla Geriqjoedn 1Document20 pagesPerilla Geriqjoedn 1Geriq Joeden PerillaNo ratings yet

- General Journal Date DebitDocument17 pagesGeneral Journal Date DebitMickaella VergaraNo ratings yet

- CHP 2 Exam Preparation ProblemsDocument3 pagesCHP 2 Exam Preparation ProblemsShawn JohnstonNo ratings yet

- Module 3 Chapter 7Document8 pagesModule 3 Chapter 7Angelie Bocala CatalanNo ratings yet

- Accounting TaskDocument10 pagesAccounting TaskSamuel Amon OkumuNo ratings yet

- Applied Auditing-Prelim FinalDocument3 pagesApplied Auditing-Prelim FinalDominic E. BoticarioNo ratings yet

- Date Account Titles & Explanation Debit Credit: A. Prepare EntriesDocument4 pagesDate Account Titles & Explanation Debit Credit: A. Prepare Entriesyogi fetriansyahNo ratings yet

- Comp 2 Activity 5Document13 pagesComp 2 Activity 5Jhon Lester MagarsoNo ratings yet

- Module 3 - EA03Document30 pagesModule 3 - EA03Vaseline QtipsNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Corporation Issuance of Shares Illutsrative ProblemDocument15 pagesCorporation Issuance of Shares Illutsrative ProblemHoney MuliNo ratings yet

- Asset Liability Management: in BanksDocument44 pagesAsset Liability Management: in Bankssachin21singhNo ratings yet

- Theory of Accounts - Cpa-ReviewerDocument10 pagesTheory of Accounts - Cpa-ReviewerHeart EspineliNo ratings yet

- REVTOA ReceivablesDocument5 pagesREVTOA ReceivablesJoanna Marie UrbienNo ratings yet

- Financial Ratio AnalysisDocument10 pagesFinancial Ratio AnalysisAnonymous ic2CDkFNo ratings yet

- TPL Annual Report 2013 2014Document66 pagesTPL Annual Report 2013 2014piraisudi013341No ratings yet

- DocxDocument9 pagesDocxReiah RongavillaNo ratings yet

- Ratio Reviewer 2Document15 pagesRatio Reviewer 2Edgar Lay60% (5)

- Mba Faaunit - IIDocument15 pagesMba Faaunit - IINaresh GuduruNo ratings yet

- Week 1 Topic Tutorial Solutions CB2100 - 1920ADocument6 pagesWeek 1 Topic Tutorial Solutions CB2100 - 1920ALily TsengNo ratings yet

- Topic 02 - Accounting EquationDocument22 pagesTopic 02 - Accounting EquationNorainah Abdul Gani0% (1)

- F1 - Financial OperationsDocument20 pagesF1 - Financial OperationsZHANG EmilyNo ratings yet

- Financial Ratios Topic (MFP 1) PDFDocument9 pagesFinancial Ratios Topic (MFP 1) PDFsrinivasa annamayyaNo ratings yet

- Financial Accounting and Reporting: IFRS - 2016 June QPDocument11 pagesFinancial Accounting and Reporting: IFRS - 2016 June QPMarchella LukitoNo ratings yet

- Discounted Cash Flow Analysis: CompanyDocument3 pagesDiscounted Cash Flow Analysis: Company/jncjdncjdnNo ratings yet

- 2022 ICTSI Balance Sheet Income Statement - pg.53Document1 page2022 ICTSI Balance Sheet Income Statement - pg.53loveartxoxo.commissionNo ratings yet

- Handouts 3 - CORPORATE LIQUIDATIONDocument7 pagesHandouts 3 - CORPORATE LIQUIDATIONcecille ramirezNo ratings yet

- FAC 1502 Tutorial Letter 101-2015 PDFDocument96 pagesFAC 1502 Tutorial Letter 101-2015 PDFVinny Hungwe0% (1)

- R12 Troubleshooting Misclassified Accounts in General Ledger (Doc ID 872162.1)Document10 pagesR12 Troubleshooting Misclassified Accounts in General Ledger (Doc ID 872162.1)obioraechezonaNo ratings yet

- Ethiopia International Public Sector Accounting Standards Latest UpdatesDocument8 pagesEthiopia International Public Sector Accounting Standards Latest UpdatesPhoenix Rising100% (1)

- 23 - Vol-1 - Issue-7 - Financial Statement Effect - WiproDocument20 pages23 - Vol-1 - Issue-7 - Financial Statement Effect - WiproKanav GuptaNo ratings yet

- Final Round - 1ST - QDocument6 pagesFinal Round - 1ST - QwivadaNo ratings yet

- Chapter Three: General Fund & Special Revenue Funds 3.1 General Fund IsDocument41 pagesChapter Three: General Fund & Special Revenue Funds 3.1 General Fund IsTamirat BashaaNo ratings yet

- Study Guide CH 12Document7 pagesStudy Guide CH 12Stephanie RobinsonNo ratings yet

- 1 Blank Model TemplateDocument28 pages1 Blank Model TemplateMasroor KhanNo ratings yet

- Assignment Intermediate Financial Accounting I - Rifky Mahendra - 1900012264.Document4 pagesAssignment Intermediate Financial Accounting I - Rifky Mahendra - 1900012264.Rahmat AlamsyahNo ratings yet

- Bsa 3101 - Accounting For Special Transactions Seatwork No. 2 InstructionsDocument2 pagesBsa 3101 - Accounting For Special Transactions Seatwork No. 2 InstructionsZihr EllerycNo ratings yet

- First Quarter Assessment in FABM2Document4 pagesFirst Quarter Assessment in FABM2Nhelben ManuelNo ratings yet

- Chapter 1 Problem 5 To 7Document2 pagesChapter 1 Problem 5 To 7XienaNo ratings yet