Download as pdf or txt

You might also like

- COA Resolution 2012-014 Guidelines On Conduct of Team Building ActivityDocument10 pagesCOA Resolution 2012-014 Guidelines On Conduct of Team Building Activitynelggkram86% (7)

- Manual On Barangay Financial Management PDFDocument288 pagesManual On Barangay Financial Management PDFAcu Z Marcus97% (31)

- Aom No. 05 - (One Time Cleansing of Ppe)Document8 pagesAom No. 05 - (One Time Cleansing of Ppe)Ragnar Lothbrok100% (8)

- AAA Solution Pack - Final 2Document146 pagesAAA Solution Pack - Final 2Kumaravel Nadar100% (1)

- Documentary Requirements For Common Government TransactionsDocument74 pagesDocumentary Requirements For Common Government TransactionsChristine Meralpes100% (9)

- COA Circular Relief From AccountabilityDocument4 pagesCOA Circular Relief From AccountabilityPrime Antonio Ramos85% (13)

- Local Government Supply and Property ManagementDocument1 pageLocal Government Supply and Property ManagementShinji50% (4)

- The PPSAS and The Revised Chart of AccountsDocument98 pagesThe PPSAS and The Revised Chart of AccountsDaniel Salmorin87% (15)

- Sample Aom - Procurement of Meals and SnacksDocument8 pagesSample Aom - Procurement of Meals and Snacksjaymark camacho75% (4)

- Relief From Accountability Sample Letter of StudentDocument8 pagesRelief From Accountability Sample Letter of StudentShiela ShieshielaNo ratings yet

- Request For Relief of AccountabilityDocument1 pageRequest For Relief of AccountabilityRussel Saracho88% (8)

- Enhanced eNGASDocument116 pagesEnhanced eNGASJo AnnNo ratings yet

- Reviewer ICLTE 202Document4 pagesReviewer ICLTE 202Angelica Aquino Gasmen100% (6)

- Process Flow On Disposal of Government PropertiesDocument3 pagesProcess Flow On Disposal of Government PropertiesEzpi LM75% (8)

- Revised Chart of Accounts For LGUsDocument98 pagesRevised Chart of Accounts For LGUsMara Reyes100% (9)

- DOF-BLGF Local Treasury Operations Manual (LTOM)Document609 pagesDOF-BLGF Local Treasury Operations Manual (LTOM)Carlo P. Caguimbal100% (21)

- BCLTE Results June 2023Document27 pagesBCLTE Results June 2023TOPNOTCHER PhilippinesNo ratings yet

- Printable LTOM BOOK 1Document210 pagesPrintable LTOM BOOK 1perrygrace07100% (1)

- AOM No. 19 002 Burgos NHS Reimbursements Final With SignatureDocument6 pagesAOM No. 19 002 Burgos NHS Reimbursements Final With SignatureJhoanna Marie Manuel-Abel100% (1)

- Engas Implementation Rollout555Document60 pagesEngas Implementation Rollout555Romy Wacas100% (2)

- COA DECISION NO. 2008-126: Facts of The CaseDocument2 pagesCOA DECISION NO. 2008-126: Facts of The CaseFe M. NguddoNo ratings yet

- Chapter 15 Problems, International Economics by SalvatoreDocument6 pagesChapter 15 Problems, International Economics by SalvatoreBùi Hà LinhNo ratings yet

- The Philippine Public Sector Accounting StandardsDocument8 pagesThe Philippine Public Sector Accounting StandardsRichel Armayan100% (1)

- NGAS Manual For Local Government UnitsDocument29 pagesNGAS Manual For Local Government UnitsChiyobels100% (6)

- Government Accounting Manual For NGAsDocument83 pagesGovernment Accounting Manual For NGAsAyan Vico100% (2)

- CH 2.0-PLAN THE CASH EXAMINATIONDocument12 pagesCH 2.0-PLAN THE CASH EXAMINATIONBon Carlo Medina MelocotonNo ratings yet

- Implementing The Computerized Government Accounting System:: Philippine ExperienceDocument60 pagesImplementing The Computerized Government Accounting System:: Philippine ExperienceEar Tan100% (2)

- New Government Accounting System in The PhilippinesDocument5 pagesNew Government Accounting System in The PhilippinesCristalNo ratings yet

- Manual On Barangay Financial Management 1Document270 pagesManual On Barangay Financial Management 1Reynen Mendoza100% (1)

- Ngas Volume 2Document6 pagesNgas Volume 2Carlota Nicolas Villaroman100% (1)

- AOM Sample (Brgy.)Document4 pagesAOM Sample (Brgy.)Russel Saracho100% (2)

- Office of The Municipal Mayor: Republic of The Philippines Province of Isabela Municipality of GamuDocument3 pagesOffice of The Municipal Mayor: Republic of The Philippines Province of Isabela Municipality of GamuEduard Ferrer100% (1)

- GAM For NGAs Volume IIDocument4 pagesGAM For NGAs Volume IIMariann Jane Gan71% (14)

- GAM For NGAs Volume IDocument60 pagesGAM For NGAs Volume IPhrexilyn PajarilloNo ratings yet

- The New Government Accounting System ManualDocument37 pagesThe New Government Accounting System ManualJane Delos Santos100% (11)

- ICLTE-A.1-Data Analytics - Investment Programming and FRMDocument31 pagesICLTE-A.1-Data Analytics - Investment Programming and FRMNash A. Dugasan100% (1)

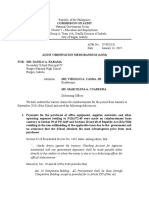

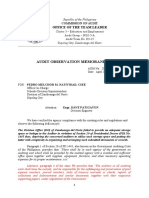

- Audit Observation Memorandum: Office of The Team LeaderDocument3 pagesAudit Observation Memorandum: Office of The Team Leaderrussel1435No ratings yet

- COA Resolution # 2021-010 Dtd. May 18, 2021 Updated Guidelines On The Appraisal, Disposal and Derecognition of Obsolete, Damaged and Junk Inventories and Unserviceable PropertyDocument13 pagesCOA Resolution # 2021-010 Dtd. May 18, 2021 Updated Guidelines On The Appraisal, Disposal and Derecognition of Obsolete, Damaged and Junk Inventories and Unserviceable PropertyRjae Baloyo100% (3)

- A.4A Registry of Semi Expendable Property Issued LVDocument8 pagesA.4A Registry of Semi Expendable Property Issued LVjaypee raguroNo ratings yet

- Local Public Financial Management Tools For ESREDocument54 pagesLocal Public Financial Management Tools For ESRERandy Sioson100% (1)

- Reviewer-Government AccountingDocument5 pagesReviewer-Government AccountingNicale JeenNo ratings yet

- COA - R2017-021 - Amended To Installment Settlement of ND PDFDocument3 pagesCOA - R2017-021 - Amended To Installment Settlement of ND PDFMelissa G. Aston - Balmediano100% (2)

- Certificate of Availability of Funds (CAF)Document1 pageCertificate of Availability of Funds (CAF)Al Simbajon100% (3)

- Book 1: Updated Local Treasury Operations Manual (Ltom)Document87 pagesBook 1: Updated Local Treasury Operations Manual (Ltom)Gian Bayaras100% (1)

- 4.registry of Semi-Expendable Property IssuedDocument1 page4.registry of Semi-Expendable Property IssuedAlgie ReñonNo ratings yet

- Responsibility, Accountability and Liability Over Government Funds and PropertyDocument15 pagesResponsibility, Accountability and Liability Over Government Funds and Propertylinette causingNo ratings yet

- SEF Joint CircularDocument3 pagesSEF Joint CircularReihannah Paguital-MagnoNo ratings yet

- PPSAS and The Revised Chart of AccountsDocument51 pagesPPSAS and The Revised Chart of Accountsmile100% (4)

- Bclte FormDocument3 pagesBclte Formjune florezNo ratings yet

- CamiguinProv2018 Audit ReportDocument159 pagesCamiguinProv2018 Audit ReporthazelNo ratings yet

- AOM NO. 01-Unserviceable PPEDocument3 pagesAOM NO. 01-Unserviceable PPERagnar LothbrokNo ratings yet

- Local Budget ProcessDocument3 pagesLocal Budget ProcessLoreen Tonett100% (1)

- Invoice Receipt For Property Form GF 30 A 2Document1 pageInvoice Receipt For Property Form GF 30 A 2Rexis ReginanNo ratings yet

- The PPSAS and The Revised Chart of Accounts: Tools To Enhance Accountability and Transparency in Financial ReportingDocument98 pagesThe PPSAS and The Revised Chart of Accounts: Tools To Enhance Accountability and Transparency in Financial ReportingJhopel Casagnap EmanNo ratings yet

- Statement of Relatives FormDocument1 pageStatement of Relatives FormMary Lenjelly Mandia OsinsaoNo ratings yet

- Seminar On Property and Supply Management SystemDocument7 pagesSeminar On Property and Supply Management SystemCire Etneilav75% (4)

- New Government Accounting System: Manual On The For Local Government UnitsDocument5 pagesNew Government Accounting System: Manual On The For Local Government UnitsMARILOU TANAELNo ratings yet

- Manual On The New Government Accounting System For National Government AgenciesDocument6 pagesManual On The New Government Accounting System For National Government AgenciesDerick AlmoNo ratings yet

- 05-Table of ContentsDocument5 pages05-Table of ContentsOdessa MendozaNo ratings yet

- MANUAL On FINANCIAL MANAGEMENT of BARANGAY - 05-Table of ContentsDocument4 pagesMANUAL On FINANCIAL MANAGEMENT of BARANGAY - 05-Table of ContentsMACCO BABATNGONNo ratings yet

- BARANGAY MANUAL - 01-CoverDocument278 pagesBARANGAY MANUAL - 01-CoverMACCO BABATNGONNo ratings yet

- Manual On The New Government Accounting System For Local Government UnitsDocument12 pagesManual On The New Government Accounting System For Local Government UnitsCarlota Nicolas VillaromanNo ratings yet

- Insurance Code MCQDocument13 pagesInsurance Code MCQaldenamellNo ratings yet

- HOMEWORK 003 (HW003) Conceptual Framework & Accounting StandardsDocument4 pagesHOMEWORK 003 (HW003) Conceptual Framework & Accounting StandardsaltaNo ratings yet

- Budget PreparationDocument2 pagesBudget PreparationAAAAANo ratings yet

- Challan No. ITNS 281 : Assessment YearDocument1 pageChallan No. ITNS 281 : Assessment YearTpm UmasankarNo ratings yet

- Residual Method - Incoming & Outgoing Partial Payments Posting in SAPDocument6 pagesResidual Method - Incoming & Outgoing Partial Payments Posting in SAPrune 00No ratings yet

- PKG 29 KCPDocument1 pagePKG 29 KCPkarthikeyan PNo ratings yet

- 2021 Prelim P2 - Answer BookletDocument10 pages2021 Prelim P2 - Answer Bookletchayemba.cheNo ratings yet

- Cma UsaDocument2 pagesCma UsaADWAID RAJAN0% (1)

- Chapter 1: Introduction: 1.1: Profile and Performance of ICICI BankDocument33 pagesChapter 1: Introduction: 1.1: Profile and Performance of ICICI Banksonal mhatreNo ratings yet

- Welcome Letter 131706428Document3 pagesWelcome Letter 131706428rupesh.gunjan90823No ratings yet

- Faysal Bank Internship ReportDocument84 pagesFaysal Bank Internship Reportimran_greenplus100% (3)

- CUHK FINA4110 Assignment2Document5 pagesCUHK FINA4110 Assignment2MOON TVNo ratings yet

- Chapter 3 - Sources of CapitalDocument7 pagesChapter 3 - Sources of CapitalAnthony BalandoNo ratings yet

- MENGECO Group 6 - InterestDocument59 pagesMENGECO Group 6 - InterestEarl James RoqueNo ratings yet

- Digital SystemDocument71 pagesDigital SystemKing KelishNo ratings yet

- Sample Board Resolution - PartnershipDocument3 pagesSample Board Resolution - PartnershipmikeNo ratings yet

- IA Chapter-1-3Document7 pagesIA Chapter-1-3Christine Joyce EnriquezNo ratings yet

- Presentation of Islamic Banking of FinanceDocument18 pagesPresentation of Islamic Banking of FinanceZarlish Naseem RanaNo ratings yet

- Auto Debit Instruction For Nach/Dd: Cc/Branchops/Mandate Form/002Document2 pagesAuto Debit Instruction For Nach/Dd: Cc/Branchops/Mandate Form/002Dhruv SekhriNo ratings yet

- Yes Bank CrisisDocument21 pagesYes Bank CrisisAftab GhanchiNo ratings yet

- Tutorial 7 - Problem 7Document3 pagesTutorial 7 - Problem 7Joe DicksonNo ratings yet

- Finacle Commands - Finacle Wiki, Finacle Tutorial & Finacle Training For BankersDocument4 pagesFinacle Commands - Finacle Wiki, Finacle Tutorial & Finacle Training For BankersJayantNo ratings yet

- Problem 1-A Bank Reconciliation: Add/less: Book Errors P 900.00Document4 pagesProblem 1-A Bank Reconciliation: Add/less: Book Errors P 900.00Merry Kriss RiveraNo ratings yet

- GR12 Business Finance Module 3-4Document8 pagesGR12 Business Finance Module 3-4Jean Diane JoveloNo ratings yet

- Risk Aversion and Capital Allocation To Risky AssetsDocument16 pagesRisk Aversion and Capital Allocation To Risky Assets777priyankaNo ratings yet

- Intacc Cash and Cash EquivalentsDocument2 pagesIntacc Cash and Cash EquivalentsKristalen ArmandoNo ratings yet

- Master Template v1Document79 pagesMaster Template v1KiranNo ratings yet

- Anz Pensioner Advantage Statement: Welcome To Your Anz Account at A GlanceDocument12 pagesAnz Pensioner Advantage Statement: Welcome To Your Anz Account at A GlanceMohitNo ratings yet