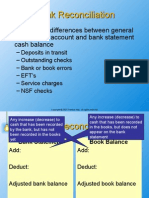

Bank Reconciliation Example

Bank Reconciliation Example

You might also like

- DLL Travel Services FIRST GradingDocument118 pagesDLL Travel Services FIRST GradingMary Cherill Umali75% (8)

- WBS Creation in PS ModuleDocument145 pagesWBS Creation in PS ModuleSDOT Ashta100% (1)

- Bank Reconciliation Bank ReconciliationDocument9 pagesBank Reconciliation Bank Reconciliationmustafa_33No ratings yet

- Supply Chain Management Project SYBBA IB (SAKSHI GOYAL 77) - 4Document44 pagesSupply Chain Management Project SYBBA IB (SAKSHI GOYAL 77) - 4Sakshi GoyalNo ratings yet

- Rekonsiliasi 2Document3 pagesRekonsiliasi 2ahmed aliNo ratings yet

- 05 Quiz 1 - ARG - ZarateDocument2 pages05 Quiz 1 - ARG - ZarateYvan ZarateNo ratings yet

- What Is A Bank Reconciliation?Document4 pagesWhat Is A Bank Reconciliation?Mustaeen DarNo ratings yet

- Project AccDocument6 pagesProject AccAgha TamourNo ratings yet

- What Is Bank Reconciliation?Document7 pagesWhat Is Bank Reconciliation?Yassi CurtisNo ratings yet

- What Is Bank Reconciliation?Document7 pagesWhat Is Bank Reconciliation?Yassi CurtisNo ratings yet

- What Is Bank Reconciliation?Document7 pagesWhat Is Bank Reconciliation?Yassi CurtisNo ratings yet

- Bank Reconciliation Statement: Mushtaq NadeemDocument4 pagesBank Reconciliation Statement: Mushtaq NadeemMalik SalmanNo ratings yet

- Bank RecolonizationDocument1 pageBank Recolonizationasma100% (1)

- Cash - CRDocument14 pagesCash - CRpingu patwhoNo ratings yet

- Control AccountingDocument7 pagesControl AccountingAmir RuplalNo ratings yet

- Bank Recon DiscussionDocument6 pagesBank Recon DiscussionKrigfordNo ratings yet

- Chapter 7 Exercises With SolutionDocument5 pagesChapter 7 Exercises With Solutionmohammad khataybehNo ratings yet

- Bank Reconciliation StatementDocument2 pagesBank Reconciliation StatementSelvi balanNo ratings yet

- Illustrative Problem On Adjusted Bank MethodDocument15 pagesIllustrative Problem On Adjusted Bank MethodRyDNo ratings yet

- Accounting For Cash and ReceivableDocument7 pagesAccounting For Cash and ReceivableAbrha GidayNo ratings yet

- Bank Recon GoldDocument2 pagesBank Recon Goldcrisjay ramosNo ratings yet

- Bank Reconciliation Statement-Problem Making: Cash Book (Depositors Book) Taka Pass Book (Bank's Book) TakaDocument13 pagesBank Reconciliation Statement-Problem Making: Cash Book (Depositors Book) Taka Pass Book (Bank's Book) TakaIván RañaNo ratings yet

- Practice Problem in Cash ReceivableDocument5 pagesPractice Problem in Cash ReceivableJernalynne AvellanaNo ratings yet

- Bank ReconciliationDocument6 pagesBank ReconciliationXienaNo ratings yet

- 10 BANK RECONCILIATIONS (Questions)Document22 pages10 BANK RECONCILIATIONS (Questions)Zeeshan BakaliNo ratings yet

- Homework Chapter 7Document12 pagesHomework Chapter 7Trung Kiên NguyễnNo ratings yet

- Gavarra-Marie Joy-Bsais-2b-Problem3-No.3Document2 pagesGavarra-Marie Joy-Bsais-2b-Problem3-No.3Nikki Jean Hona50% (2)

- 9.2 BRS HomeDocument3 pages9.2 BRS HomeaneesgillaniNo ratings yet

- Debit Relevant Expense A/c Credit Debit Credit Debit Bank Charges Account CreditDocument27 pagesDebit Relevant Expense A/c Credit Debit Credit Debit Bank Charges Account CreditAsif AslamNo ratings yet

- ACCTG W09 Chapter 8Document15 pagesACCTG W09 Chapter 8kayla tsoiNo ratings yet

- Bank Reconciliation: Mrs. Rosalie Rosales-Makil, Cpa, LPT, MbaDocument18 pagesBank Reconciliation: Mrs. Rosalie Rosales-Makil, Cpa, LPT, MbaPSHNo ratings yet

- ACGA 504/ HCGA 507 General Accounting - Part 2Document17 pagesACGA 504/ HCGA 507 General Accounting - Part 2Eliza BethNo ratings yet

- Bank Reconciliation StatementDocument7 pagesBank Reconciliation StatementAhmed DeoNo ratings yet

- Uas Pengakun 2Document4 pagesUas Pengakun 2Givania RahmadhaniNo ratings yet

- Principles of Financial Accounting: Chapter 7 - Fraud, Internal Controls, & CashDocument12 pagesPrinciples of Financial Accounting: Chapter 7 - Fraud, Internal Controls, & CashAli Zain Parhar100% (2)

- What Is Bank Reconciliation.Document11 pagesWhat Is Bank Reconciliation.Sabrena FennaNo ratings yet

- Bank Reconciliation Statement - Process - Format - ExampleDocument5 pagesBank Reconciliation Statement - Process - Format - ExampleCykee100% (1)

- Actg14 Activity Group4Document2 pagesActg14 Activity Group4anneNo ratings yet

- BA3 M KIT Chapter 16Document4 pagesBA3 M KIT Chapter 16Nivneth PeirisNo ratings yet

- Bank Reconciliation & Proof of CashDocument25 pagesBank Reconciliation & Proof of CashTanya MaxNo ratings yet

- Module 6 P2 Internal Control - BSA & BSMADocument14 pagesModule 6 P2 Internal Control - BSA & BSMAramosmikay0222No ratings yet

- 5 D35 J1 XIzyh 2 HN 4 C OI59 N PVLG ISz 8 e Re CG TOm UTGbm WHWD WYhthrce 0Document14 pages5 D35 J1 XIzyh 2 HN 4 C OI59 N PVLG ISz 8 e Re CG TOm UTGbm WHWD WYhthrce 0ramosmikay0222No ratings yet

- Module 6 Part 2 Internal ControlDocument15 pagesModule 6 Part 2 Internal ControlKRISTINA CASSANDRA CUEVASNo ratings yet

- Bank Reconciliation Statement PreparationDocument5 pagesBank Reconciliation Statement PreparationsteveNo ratings yet

- Bank Reconciliation Statement: Strictly ConfidentialDocument3 pagesBank Reconciliation Statement: Strictly Confidentialnegussie biruNo ratings yet

- Reviewer in Accounting - xlsx-3Document59 pagesReviewer in Accounting - xlsx-3Franchesca CortezNo ratings yet

- ABM FABM2 Q2 Wk3 LAS3Document11 pagesABM FABM2 Q2 Wk3 LAS3ayaNo ratings yet

- UntitledDocument6 pagesUntitledÂn LyNo ratings yet

- Bank Reconciliations Credit Memo PDF FormatDocument8 pagesBank Reconciliations Credit Memo PDF FormatGeorge MockNo ratings yet

- 2 BRSDocument20 pages2 BRSasadimohammadsameerNo ratings yet

- Bài-tập-bank-reconciliation MLDocument6 pagesBài-tập-bank-reconciliation MLMai Lâm LêNo ratings yet

- Simulation 1 - Financial Accounting - March 4Document4 pagesSimulation 1 - Financial Accounting - March 4Ednalyn PascualNo ratings yet

- F.A.B.M PortfolioDocument28 pagesF.A.B.M PortfolioLjoy Vlog SurvivedNo ratings yet

- Illustration 8-5 Bank Reconciliation FormatDocument7 pagesIllustration 8-5 Bank Reconciliation FormatAbrar ShaikhNo ratings yet

- A. Bank To Book MethodDocument5 pagesA. Bank To Book MethodDiane MagnayeNo ratings yet

- June Bank ReconciliationDocument1 pageJune Bank ReconciliationSteven SandersonNo ratings yet

- MG T 101 Short Notes Lectures 2345Document29 pagesMG T 101 Short Notes Lectures 2345Abdul wadoodNo ratings yet

- Lesson 5: Bank Reconciliation What Is A Bank Reconciliation?Document9 pagesLesson 5: Bank Reconciliation What Is A Bank Reconciliation?Reymark TalaveraNo ratings yet

- FA2 Revision Questions 2Document9 pagesFA2 Revision Questions 2miss ainaNo ratings yet

- Cash and Cash Equivalents Solved ProblemsDocument25 pagesCash and Cash Equivalents Solved ProblemsddalgisznNo ratings yet

- Unit 8 Cash: Balance Per BankDocument5 pagesUnit 8 Cash: Balance Per BankAnonymous Fn7Ko5riKTNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- J.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineNo ratings yet

- 9 Core Elements of A Quality Management System: Ken CroucherDocument7 pages9 Core Elements of A Quality Management System: Ken CroucherTariq HashamiNo ratings yet

- Persuasive Speech OutlineDocument3 pagesPersuasive Speech OutlinehasanNo ratings yet

- Biocon India Case StudyDocument7 pagesBiocon India Case StudyAmit Jha100% (1)

- Nifty Reits and Invits Whitepaper For Dec 2023 - v1 (Final)Document9 pagesNifty Reits and Invits Whitepaper For Dec 2023 - v1 (Final)JackNo ratings yet

- Pakistan As A Tourist Destination & Tourism Industry in Pakistan-2011Document31 pagesPakistan As A Tourist Destination & Tourism Industry in Pakistan-2011tayyab_mir_488% (8)

- Cost Sheet ExercisesDocument2 pagesCost Sheet ExercisessivapriyakamatNo ratings yet

- RMK Akm 2-CH 21Document14 pagesRMK Akm 2-CH 21Rio Capitano0% (1)

- Istilah Akuntansi Dalam Bahasa InggrisDocument16 pagesIstilah Akuntansi Dalam Bahasa InggrisDhuny OctavianNo ratings yet

- Print - Udyam Registration Certificate 2Document4 pagesPrint - Udyam Registration Certificate 2DanishNo ratings yet

- Culture of The Container StoreDocument9 pagesCulture of The Container StoreSajib ChakrabortyNo ratings yet

- The Global Green Economy ReportDocument65 pagesThe Global Green Economy Reportlee jin huiNo ratings yet

- The Search For A Sound Business IdeaDocument46 pagesThe Search For A Sound Business IdeaMiguel JaralveNo ratings yet

- Chapter-10: Customer OrientationDocument16 pagesChapter-10: Customer Orientationtaranjeet singhNo ratings yet

- United Company For FoodDocument2 pagesUnited Company For FoodmshawkycnNo ratings yet

- Domestic Travel ReadingDocument3 pagesDomestic Travel ReadingBenian TuncelNo ratings yet

- Occupation of The Respondents: InterpretationDocument14 pagesOccupation of The Respondents: InterpretationArjun RajNo ratings yet

- Discussion DDocument2 pagesDiscussion DVarunNo ratings yet

- AFJ Annual 2022 FINAL PDFDocument104 pagesAFJ Annual 2022 FINAL PDFEdwin SinginiNo ratings yet

- Bridgeport CT Adopted Budget 2010-2011Document552 pagesBridgeport CT Adopted Budget 2010-2011BridgeportCTNo ratings yet

- Exploring Recent Long-Distance Passenger Travel Trends in EuropeDocument10 pagesExploring Recent Long-Distance Passenger Travel Trends in EuropeyrperdanaNo ratings yet

- BM2 Chapter 1Document23 pagesBM2 Chapter 1Lowela KasandraNo ratings yet

- FIN3403 Exam 4 PracticeDocument8 pagesFIN3403 Exam 4 Practicek10924No ratings yet

- Intraday: Trading With TheDocument4 pagesIntraday: Trading With Thepetefader100% (2)

- Icici BankDocument16 pagesIcici BankGulafsha AnsariNo ratings yet

- Lululemon Online CaseDocument7 pagesLululemon Online CaseEmil Hopkinson100% (1)

- Catherine Morris - Demystifying SustainabilityDocument34 pagesCatherine Morris - Demystifying SustainabilityshivalikaNo ratings yet

- ITASIA - 24.09.22 Itasia - Daily Sales Invoice & COD MonitoringDocument15 pagesITASIA - 24.09.22 Itasia - Daily Sales Invoice & COD MonitoringCharlene Martinez DeguzmanNo ratings yet

Download as docx, pdf, or txt

You might also like

- DLL Travel Services FIRST GradingDocument118 pagesDLL Travel Services FIRST GradingMary Cherill Umali75% (8)

- WBS Creation in PS ModuleDocument145 pagesWBS Creation in PS ModuleSDOT Ashta100% (1)

- Bank Reconciliation Bank ReconciliationDocument9 pagesBank Reconciliation Bank Reconciliationmustafa_33No ratings yet

- Supply Chain Management Project SYBBA IB (SAKSHI GOYAL 77) - 4Document44 pagesSupply Chain Management Project SYBBA IB (SAKSHI GOYAL 77) - 4Sakshi GoyalNo ratings yet

- Rekonsiliasi 2Document3 pagesRekonsiliasi 2ahmed aliNo ratings yet

- 05 Quiz 1 - ARG - ZarateDocument2 pages05 Quiz 1 - ARG - ZarateYvan ZarateNo ratings yet

- What Is A Bank Reconciliation?Document4 pagesWhat Is A Bank Reconciliation?Mustaeen DarNo ratings yet

- Project AccDocument6 pagesProject AccAgha TamourNo ratings yet

- What Is Bank Reconciliation?Document7 pagesWhat Is Bank Reconciliation?Yassi CurtisNo ratings yet

- What Is Bank Reconciliation?Document7 pagesWhat Is Bank Reconciliation?Yassi CurtisNo ratings yet

- What Is Bank Reconciliation?Document7 pagesWhat Is Bank Reconciliation?Yassi CurtisNo ratings yet

- Bank Reconciliation Statement: Mushtaq NadeemDocument4 pagesBank Reconciliation Statement: Mushtaq NadeemMalik SalmanNo ratings yet

- Bank RecolonizationDocument1 pageBank Recolonizationasma100% (1)

- Cash - CRDocument14 pagesCash - CRpingu patwhoNo ratings yet

- Control AccountingDocument7 pagesControl AccountingAmir RuplalNo ratings yet

- Bank Recon DiscussionDocument6 pagesBank Recon DiscussionKrigfordNo ratings yet

- Chapter 7 Exercises With SolutionDocument5 pagesChapter 7 Exercises With Solutionmohammad khataybehNo ratings yet

- Bank Reconciliation StatementDocument2 pagesBank Reconciliation StatementSelvi balanNo ratings yet

- Illustrative Problem On Adjusted Bank MethodDocument15 pagesIllustrative Problem On Adjusted Bank MethodRyDNo ratings yet

- Accounting For Cash and ReceivableDocument7 pagesAccounting For Cash and ReceivableAbrha GidayNo ratings yet

- Bank Recon GoldDocument2 pagesBank Recon Goldcrisjay ramosNo ratings yet

- Bank Reconciliation Statement-Problem Making: Cash Book (Depositors Book) Taka Pass Book (Bank's Book) TakaDocument13 pagesBank Reconciliation Statement-Problem Making: Cash Book (Depositors Book) Taka Pass Book (Bank's Book) TakaIván RañaNo ratings yet

- Practice Problem in Cash ReceivableDocument5 pagesPractice Problem in Cash ReceivableJernalynne AvellanaNo ratings yet

- Bank ReconciliationDocument6 pagesBank ReconciliationXienaNo ratings yet

- 10 BANK RECONCILIATIONS (Questions)Document22 pages10 BANK RECONCILIATIONS (Questions)Zeeshan BakaliNo ratings yet

- Homework Chapter 7Document12 pagesHomework Chapter 7Trung Kiên NguyễnNo ratings yet

- Gavarra-Marie Joy-Bsais-2b-Problem3-No.3Document2 pagesGavarra-Marie Joy-Bsais-2b-Problem3-No.3Nikki Jean Hona50% (2)

- 9.2 BRS HomeDocument3 pages9.2 BRS HomeaneesgillaniNo ratings yet

- Debit Relevant Expense A/c Credit Debit Credit Debit Bank Charges Account CreditDocument27 pagesDebit Relevant Expense A/c Credit Debit Credit Debit Bank Charges Account CreditAsif AslamNo ratings yet

- ACCTG W09 Chapter 8Document15 pagesACCTG W09 Chapter 8kayla tsoiNo ratings yet

- Bank Reconciliation: Mrs. Rosalie Rosales-Makil, Cpa, LPT, MbaDocument18 pagesBank Reconciliation: Mrs. Rosalie Rosales-Makil, Cpa, LPT, MbaPSHNo ratings yet

- ACGA 504/ HCGA 507 General Accounting - Part 2Document17 pagesACGA 504/ HCGA 507 General Accounting - Part 2Eliza BethNo ratings yet

- Bank Reconciliation StatementDocument7 pagesBank Reconciliation StatementAhmed DeoNo ratings yet

- Uas Pengakun 2Document4 pagesUas Pengakun 2Givania RahmadhaniNo ratings yet

- Principles of Financial Accounting: Chapter 7 - Fraud, Internal Controls, & CashDocument12 pagesPrinciples of Financial Accounting: Chapter 7 - Fraud, Internal Controls, & CashAli Zain Parhar100% (2)

- What Is Bank Reconciliation.Document11 pagesWhat Is Bank Reconciliation.Sabrena FennaNo ratings yet

- Bank Reconciliation Statement - Process - Format - ExampleDocument5 pagesBank Reconciliation Statement - Process - Format - ExampleCykee100% (1)

- Actg14 Activity Group4Document2 pagesActg14 Activity Group4anneNo ratings yet

- BA3 M KIT Chapter 16Document4 pagesBA3 M KIT Chapter 16Nivneth PeirisNo ratings yet

- Bank Reconciliation & Proof of CashDocument25 pagesBank Reconciliation & Proof of CashTanya MaxNo ratings yet

- Module 6 P2 Internal Control - BSA & BSMADocument14 pagesModule 6 P2 Internal Control - BSA & BSMAramosmikay0222No ratings yet

- 5 D35 J1 XIzyh 2 HN 4 C OI59 N PVLG ISz 8 e Re CG TOm UTGbm WHWD WYhthrce 0Document14 pages5 D35 J1 XIzyh 2 HN 4 C OI59 N PVLG ISz 8 e Re CG TOm UTGbm WHWD WYhthrce 0ramosmikay0222No ratings yet

- Module 6 Part 2 Internal ControlDocument15 pagesModule 6 Part 2 Internal ControlKRISTINA CASSANDRA CUEVASNo ratings yet

- Bank Reconciliation Statement PreparationDocument5 pagesBank Reconciliation Statement PreparationsteveNo ratings yet

- Bank Reconciliation Statement: Strictly ConfidentialDocument3 pagesBank Reconciliation Statement: Strictly Confidentialnegussie biruNo ratings yet

- Reviewer in Accounting - xlsx-3Document59 pagesReviewer in Accounting - xlsx-3Franchesca CortezNo ratings yet

- ABM FABM2 Q2 Wk3 LAS3Document11 pagesABM FABM2 Q2 Wk3 LAS3ayaNo ratings yet

- UntitledDocument6 pagesUntitledÂn LyNo ratings yet

- Bank Reconciliations Credit Memo PDF FormatDocument8 pagesBank Reconciliations Credit Memo PDF FormatGeorge MockNo ratings yet

- 2 BRSDocument20 pages2 BRSasadimohammadsameerNo ratings yet

- Bài-tập-bank-reconciliation MLDocument6 pagesBài-tập-bank-reconciliation MLMai Lâm LêNo ratings yet

- Simulation 1 - Financial Accounting - March 4Document4 pagesSimulation 1 - Financial Accounting - March 4Ednalyn PascualNo ratings yet

- F.A.B.M PortfolioDocument28 pagesF.A.B.M PortfolioLjoy Vlog SurvivedNo ratings yet

- Illustration 8-5 Bank Reconciliation FormatDocument7 pagesIllustration 8-5 Bank Reconciliation FormatAbrar ShaikhNo ratings yet

- A. Bank To Book MethodDocument5 pagesA. Bank To Book MethodDiane MagnayeNo ratings yet

- June Bank ReconciliationDocument1 pageJune Bank ReconciliationSteven SandersonNo ratings yet

- MG T 101 Short Notes Lectures 2345Document29 pagesMG T 101 Short Notes Lectures 2345Abdul wadoodNo ratings yet

- Lesson 5: Bank Reconciliation What Is A Bank Reconciliation?Document9 pagesLesson 5: Bank Reconciliation What Is A Bank Reconciliation?Reymark TalaveraNo ratings yet

- FA2 Revision Questions 2Document9 pagesFA2 Revision Questions 2miss ainaNo ratings yet

- Cash and Cash Equivalents Solved ProblemsDocument25 pagesCash and Cash Equivalents Solved ProblemsddalgisznNo ratings yet

- Unit 8 Cash: Balance Per BankDocument5 pagesUnit 8 Cash: Balance Per BankAnonymous Fn7Ko5riKTNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- J.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineNo ratings yet

- 9 Core Elements of A Quality Management System: Ken CroucherDocument7 pages9 Core Elements of A Quality Management System: Ken CroucherTariq HashamiNo ratings yet

- Persuasive Speech OutlineDocument3 pagesPersuasive Speech OutlinehasanNo ratings yet

- Biocon India Case StudyDocument7 pagesBiocon India Case StudyAmit Jha100% (1)

- Nifty Reits and Invits Whitepaper For Dec 2023 - v1 (Final)Document9 pagesNifty Reits and Invits Whitepaper For Dec 2023 - v1 (Final)JackNo ratings yet

- Pakistan As A Tourist Destination & Tourism Industry in Pakistan-2011Document31 pagesPakistan As A Tourist Destination & Tourism Industry in Pakistan-2011tayyab_mir_488% (8)

- Cost Sheet ExercisesDocument2 pagesCost Sheet ExercisessivapriyakamatNo ratings yet

- RMK Akm 2-CH 21Document14 pagesRMK Akm 2-CH 21Rio Capitano0% (1)

- Istilah Akuntansi Dalam Bahasa InggrisDocument16 pagesIstilah Akuntansi Dalam Bahasa InggrisDhuny OctavianNo ratings yet

- Print - Udyam Registration Certificate 2Document4 pagesPrint - Udyam Registration Certificate 2DanishNo ratings yet

- Culture of The Container StoreDocument9 pagesCulture of The Container StoreSajib ChakrabortyNo ratings yet

- The Global Green Economy ReportDocument65 pagesThe Global Green Economy Reportlee jin huiNo ratings yet

- The Search For A Sound Business IdeaDocument46 pagesThe Search For A Sound Business IdeaMiguel JaralveNo ratings yet

- Chapter-10: Customer OrientationDocument16 pagesChapter-10: Customer Orientationtaranjeet singhNo ratings yet

- United Company For FoodDocument2 pagesUnited Company For FoodmshawkycnNo ratings yet

- Domestic Travel ReadingDocument3 pagesDomestic Travel ReadingBenian TuncelNo ratings yet

- Occupation of The Respondents: InterpretationDocument14 pagesOccupation of The Respondents: InterpretationArjun RajNo ratings yet

- Discussion DDocument2 pagesDiscussion DVarunNo ratings yet

- AFJ Annual 2022 FINAL PDFDocument104 pagesAFJ Annual 2022 FINAL PDFEdwin SinginiNo ratings yet

- Bridgeport CT Adopted Budget 2010-2011Document552 pagesBridgeport CT Adopted Budget 2010-2011BridgeportCTNo ratings yet

- Exploring Recent Long-Distance Passenger Travel Trends in EuropeDocument10 pagesExploring Recent Long-Distance Passenger Travel Trends in EuropeyrperdanaNo ratings yet

- BM2 Chapter 1Document23 pagesBM2 Chapter 1Lowela KasandraNo ratings yet

- FIN3403 Exam 4 PracticeDocument8 pagesFIN3403 Exam 4 Practicek10924No ratings yet

- Intraday: Trading With TheDocument4 pagesIntraday: Trading With Thepetefader100% (2)

- Icici BankDocument16 pagesIcici BankGulafsha AnsariNo ratings yet

- Lululemon Online CaseDocument7 pagesLululemon Online CaseEmil Hopkinson100% (1)

- Catherine Morris - Demystifying SustainabilityDocument34 pagesCatherine Morris - Demystifying SustainabilityshivalikaNo ratings yet

- ITASIA - 24.09.22 Itasia - Daily Sales Invoice & COD MonitoringDocument15 pagesITASIA - 24.09.22 Itasia - Daily Sales Invoice & COD MonitoringCharlene Martinez DeguzmanNo ratings yet