Download as docx, pdf, or txt

You might also like

- FM Chap 6 8 ProbsDocument41 pagesFM Chap 6 8 ProbsMychie Lynne Mayuga91% (11)

- Corporate Finance Assignment Chapter 2 PDFDocument12 pagesCorporate Finance Assignment Chapter 2 PDFAna Carolina Silva100% (1)

- Problem SolvingDocument10 pagesProblem SolvingRegina De LunaNo ratings yet

- Taxation SituationalDocument113 pagesTaxation SituationalDaryl Mae Mansay100% (1)

- Assign 7 Chapter 9 Financial Forecasting For Strategic Growth Cabrera 2019-2020Document6 pagesAssign 7 Chapter 9 Financial Forecasting For Strategic Growth Cabrera 2019-2020mhikeedelantar100% (2)

- This Study Resource Was: CASTILLO, Lauren Financial Management Mam Barquez BSA-3 Problem 1 (Pro Forma Statements)Document5 pagesThis Study Resource Was: CASTILLO, Lauren Financial Management Mam Barquez BSA-3 Problem 1 (Pro Forma Statements)KATHRYN CLAUDETTE RESENTE100% (2)

- CHAPTER 7 AnswerDocument7 pagesCHAPTER 7 AnswerKenncy100% (5)

- DTDocument19 pagesDTJanesene Sol100% (4)

- Chapter 5 Financial Management by CabreraDocument19 pagesChapter 5 Financial Management by CabreraLars FriasNo ratings yet

- A. Trend Percentages: RequiredDocument5 pagesA. Trend Percentages: RequiredAngel NuevoNo ratings yet

- 3-14 Free Cash Flow: Bailey Corporation's Financial Statements (Dollars and Shares Are in Millions) Are ProvidedDocument8 pages3-14 Free Cash Flow: Bailey Corporation's Financial Statements (Dollars and Shares Are in Millions) Are ProvidedCASTOR, Vincent Paul0% (1)

- Assign 5 Chapter 7 Cash Flow Analysis Answer Cabrera 2019-2020Document6 pagesAssign 5 Chapter 7 Cash Flow Analysis Answer Cabrera 2019-2020mhikeedelantar50% (2)

- R e V I e W Q U e S T I o N S A N D P R o B L e M SDocument21 pagesR e V I e W Q U e S T I o N S A N D P R o B L e M SMonina CahiligNo ratings yet

- CHAPTER 8 AnswerDocument14 pagesCHAPTER 8 AnswerKenncyNo ratings yet

- Foundations of Financial Management: Spreadsheet TemplatesDocument14 pagesFoundations of Financial Management: Spreadsheet Templatesalaa_h1No ratings yet

- Mauro 5-4Document1 pageMauro 5-4drgNo ratings yet

- FM AssignmentDocument4 pagesFM AssignmentAnonymous s9cw5oy3100% (1)

- Sol. Man. - Chapter 10 - Cash To Accrual Basis of Acctg.Document7 pagesSol. Man. - Chapter 10 - Cash To Accrual Basis of Acctg.KATHRYN CLAUDETTE RESENTE100% (1)

- Financial Management 16th Edition Chapter 7Document32 pagesFinancial Management 16th Edition Chapter 7drcoolzNo ratings yet

- Hirschey - 2002 - Information Contents of Accounting Goodwill Numbers PDFDocument19 pagesHirschey - 2002 - Information Contents of Accounting Goodwill Numbers PDFalfianaNo ratings yet

- THE RAYMOND - Ratio AnalysisDocument13 pagesTHE RAYMOND - Ratio AnalysisKathir VelNo ratings yet

- Montealto FinMan Chapter910Document7 pagesMontealto FinMan Chapter910Rey HandumonNo ratings yet

- FINANCIAL MANAGEMENT AssignmentDocument2 pagesFINANCIAL MANAGEMENT Assignmentfinn mertensNo ratings yet

- DT 2Document8 pagesDT 2Janesene SolNo ratings yet

- Pagupat Financial-Management Chapter-910Document10 pagesPagupat Financial-Management Chapter-910Rey HandumonNo ratings yet

- Assign 6 Chapter 8 Operating and Financial Leverage Cabrera 2019-2020Document12 pagesAssign 6 Chapter 8 Operating and Financial Leverage Cabrera 2019-2020mhikeedelantar100% (1)

- Assignment Week 1Document1 pageAssignment Week 1Manjit KaurNo ratings yet

- Chapter 5-The Statement of Cash Flows: Multiple ChoiceDocument29 pagesChapter 5-The Statement of Cash Flows: Multiple ChoiceJoebin Corporal Lopez100% (1)

- Assign 2 Chapter 5 Understanding The Financial Statements Prob 8 Answer Cabrera 2019-2020Document5 pagesAssign 2 Chapter 5 Understanding The Financial Statements Prob 8 Answer Cabrera 2019-2020mhikeedelantar100% (1)

- Financial ManagementDocument9 pagesFinancial ManagementPrincess TaizeNo ratings yet

- 05.02 - ProblemSolvingChapter16.docx-2Document5 pages05.02 - ProblemSolvingChapter16.docx-2Murien Lim100% (1)

- Forecasting Short Term Operating Sample ProblemsDocument8 pagesForecasting Short Term Operating Sample ProblemsJanaisa BugayongNo ratings yet

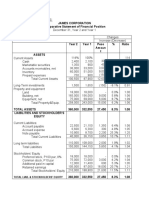

- Horizontal Analysis:: James Corporation Comparative Statement of Financial PositionDocument7 pagesHorizontal Analysis:: James Corporation Comparative Statement of Financial PositionJohn Francis IdananNo ratings yet

- Forecasting Short-Term (Operating) Financial Requirements: S A R Q P I. QuestionsDocument8 pagesForecasting Short-Term (Operating) Financial Requirements: S A R Q P I. QuestionsShiela Mae BautistaNo ratings yet

- BS Accountancy Problem 10: Financial ManagementDocument5 pagesBS Accountancy Problem 10: Financial ManagementJeanell GarciaNo ratings yet

- Quiz 1 in Ia3Document6 pagesQuiz 1 in Ia3Dorothy NadelaNo ratings yet

- Timothy - Chap 9Document33 pagesTimothy - Chap 9Chaeyeon Jung0% (1)

- Gilbert CompanyDocument15 pagesGilbert CompanyThricia Mae IgnacioNo ratings yet

- DFDocument1 pageDFJanesene Sol0% (1)

- Chapter 28 - AnswerDocument6 pagesChapter 28 - Answerwynellamae100% (1)

- Chapter 14 Answer PDF FreeDocument24 pagesChapter 14 Answer PDF FreeAang GrandeNo ratings yet

- Assignment 3 SolutionDocument7 pagesAssignment 3 SolutionAaryaAustNo ratings yet

- Chapter 3 Financial AnalysisDocument59 pagesChapter 3 Financial AnalysisRegina De LunaNo ratings yet

- Econ DevelopmentDocument21 pagesEcon DevelopmentKheajoy99 KimNo ratings yet

- Chapter 17 - AnswerDocument6 pagesChapter 17 - Answerwynellamae67% (3)

- Silver Company Provided The Following Information at Year-EndDocument1 pageSilver Company Provided The Following Information at Year-EndKatrina Dela CruzNo ratings yet

- Chapter 13 Financial Management by CabreraDocument25 pagesChapter 13 Financial Management by CabreraLars FriasNo ratings yet

- Fin 2 PDFDocument48 pagesFin 2 PDFMicaela Encinas0% (1)

- Chapter 03 - AnswerDocument10 pagesChapter 03 - AnswerGeomari D. BigalbalNo ratings yet

- Fman April 3,2020 - Operating and Financial LeverageDocument2 pagesFman April 3,2020 - Operating and Financial LeverageAngela Dela PeñaNo ratings yet

- Review ch.6Document15 pagesReview ch.6LâmViên100% (9)

- Int. Acctg. 3 - Valix2019 - Chapter18Document29 pagesInt. Acctg. 3 - Valix2019 - Chapter18Toni Rose Hernandez LualhatiNo ratings yet

- Almendraejo Strategic3Document5 pagesAlmendraejo Strategic3Miafe B. AlmendralejoNo ratings yet

- CHAPTER 19 - AnswerDocument12 pagesCHAPTER 19 - Answernash100% (5)

- Financial Markets (Chapter 8)Document4 pagesFinancial Markets (Chapter 8)Kyla DayawonNo ratings yet

- Acca110 Adorable Ac21 As03Document6 pagesAcca110 Adorable Ac21 As03Shaneen AdorableNo ratings yet

- MOD2 Statement of Cash FlowsDocument2 pagesMOD2 Statement of Cash FlowsGemma DenolanNo ratings yet

- Cash Flow StatementDocument18 pagesCash Flow Statementriya SharmaNo ratings yet

- Taxation SituationalDocument113 pagesTaxation SituationalSamyung maeNo ratings yet

- Taxation SituationalDocument114 pagesTaxation Situationalosomochristian095No ratings yet

- Accounting 2Document18 pagesAccounting 2cherryannNo ratings yet

- Taxation SituationalDocument113 pagesTaxation SituationalMartin GragasinNo ratings yet

- Chapter 13 WorksheetDocument4 pagesChapter 13 WorksheetSy HimNo ratings yet

- Serasa Experian Credit RatingDocument8 pagesSerasa Experian Credit Ratingsrmfilho123No ratings yet

- Chapter 15Document16 pagesChapter 15kylicia bestNo ratings yet

- Accounting For ItDocument7 pagesAccounting For ItAEHYUN YENVYNo ratings yet

- Ch18 Revenue RecognitionDocument42 pagesCh18 Revenue RecognitionSheena Pearl AlinsanganNo ratings yet

- Sesi 1 Receivables War22e - Ch09 Bagian 1Document51 pagesSesi 1 Receivables War22e - Ch09 Bagian 1rina.asmara asmaraNo ratings yet

- Ycoa Accdet Docu MXDocument76 pagesYcoa Accdet Docu MXEnrique MarquezNo ratings yet

- Flores, Erika - CFAS 04Document3 pagesFlores, Erika - CFAS 04Misha Laine de LeonNo ratings yet

- Pfrs 3 and 10 EXAM - FINALDocument12 pagesPfrs 3 and 10 EXAM - FINALElizabeth DumawalNo ratings yet

- Godrej Consumer Products Limited 44 QuarterUpdateDocument9 pagesGodrej Consumer Products Limited 44 QuarterUpdateKhushboo SharmaNo ratings yet

- 6018-P1&P2 - Lembar JawabanDocument35 pages6018-P1&P2 - Lembar JawabanVEMBERIONo ratings yet

- Final Exam Jul 2022Document9 pagesFinal Exam Jul 2022Rosliana RazabNo ratings yet

- TS Grewal Solutions For Class 11 Accountancy Chapter 13 - Depreciation - CBSE TutsDocument44 pagesTS Grewal Solutions For Class 11 Accountancy Chapter 13 - Depreciation - CBSE TutsRahul Kashiramka72% (18)

- BOA Favorite Topics in Oct 2022 and May 2023 CPALEDocument10 pagesBOA Favorite Topics in Oct 2022 and May 2023 CPALEFaith CastroNo ratings yet

- Accountancy Comprehensive ProjectDocument11 pagesAccountancy Comprehensive ProjectPreetiNo ratings yet

- Deferred Revenue Expenditure and The Income-Tax Act, 1961: TaxationDocument5 pagesDeferred Revenue Expenditure and The Income-Tax Act, 1961: Taxationjoseph davidNo ratings yet

- Financial Accounting and Analysis Assignment Sep 2023Document13 pagesFinancial Accounting and Analysis Assignment Sep 2023Jeff DeepNo ratings yet

- Balance Sheet DaburDocument2 pagesBalance Sheet DaburDhruvi PatelNo ratings yet

- Cfap 1 Aafr PK PDFDocument312 pagesCfap 1 Aafr PK PDFMuhammad ShehzadNo ratings yet

- Accounting For Merchandising OperationsDocument58 pagesAccounting For Merchandising OperationsSalvie Perez UtanaNo ratings yet

- Sample Financial Aspect of FeasibilityDocument12 pagesSample Financial Aspect of Feasibilitywarren071809100% (2)

- Verizon Foundation - IRS 990 - Year 2008Document317 pagesVerizon Foundation - IRS 990 - Year 2008CaliforniaALLExposedNo ratings yet

- Paper - 1: Financial Reporting Questions Ind AS 103Document30 pagesPaper - 1: Financial Reporting Questions Ind AS 103sam kapoorNo ratings yet

- Problem 07-18 Requirement 1: Minden Company: Correct!Document3 pagesProblem 07-18 Requirement 1: Minden Company: Correct!foxstupidfoxNo ratings yet

- Technical English For Engineers F2 S7 PDFDocument18 pagesTechnical English For Engineers F2 S7 PDFMichelle Cabello AstorgaNo ratings yet

- Acctng 105 Cash Flow QuizDocument19 pagesAcctng 105 Cash Flow QuizMichael A. AlbercaNo ratings yet

- CBSE Class 12 Accountancy Sample Paper 2019 Solved PDFDocument26 pagesCBSE Class 12 Accountancy Sample Paper 2019 Solved PDFMihir KhandelwalNo ratings yet

- Intermediate Accounting Reporting and Analysis 1st Edition Wahlen Test Bank DownloadDocument109 pagesIntermediate Accounting Reporting and Analysis 1st Edition Wahlen Test Bank DownloadEdna Nunez100% (18)