Download as pdf or txt

You might also like

- TGDocument2 pagesTGpr995No ratings yet

- Gov. Walz 2021 Tax Returns - RedactedDocument22 pagesGov. Walz 2021 Tax Returns - RedactedTim Walz for Governor0% (1)

- AbideDocument1 pageAbideWisdom NyamhosvaNo ratings yet

- Gov. Walz 2019 Federal Tax Return - RedactedDocument11 pagesGov. Walz 2019 Federal Tax Return - RedactedTim Walz for GovernorNo ratings yet

- Current Bill: Hello Ninoska C Briceño-Moreno, Here's What You Owe For This Billing PeriodDocument2 pagesCurrent Bill: Hello Ninoska C Briceño-Moreno, Here's What You Owe For This Billing PeriodIvan PortacioNo ratings yet

- Isba ChecklistDocument1 pageIsba ChecklistAnonymous zNjWCxV9dNo ratings yet

- US Internal Revenue Service: f1099msc - 2002Document7 pagesUS Internal Revenue Service: f1099msc - 2002IRSNo ratings yet

- DSP Inc 1099-11 Print - CFMDocument1 pageDSP Inc 1099-11 Print - CFMKenneth BarcottNo ratings yet

- 1040 ArmstrongDocument2 pages1040 Armstrongapi-458373647No ratings yet

- Form 1099 MISC David Kovach-1Document1 pageForm 1099 MISC David Kovach-1dolapo BalogunNo ratings yet

- Tax FormsDocument2 pagesTax FormsBridget May Cruz100% (1)

- 1098 STATEMENT YE098 900961 01 197: Annual Tax and Interest Statement 1098 - 2020Document6 pages1098 STATEMENT YE098 900961 01 197: Annual Tax and Interest Statement 1098 - 2020Mike TerrellNo ratings yet

- Please To Do Not Use The Back ButtonDocument2 pagesPlease To Do Not Use The Back ButtonDavid MillerNo ratings yet

- Semir Demiri 50 14Th ST North Edgartown Ma 02539Document2 pagesSemir Demiri 50 14Th ST North Edgartown Ma 02539SemirNo ratings yet

- Short Form Request For Individual Tax Return TranscriptDocument2 pagesShort Form Request For Individual Tax Return TranscriptAmber CarterNo ratings yet

- Or Wcomp 0.72 or Wcomp 0.72Document1 pageOr Wcomp 0.72 or Wcomp 0.72aaronNo ratings yet

- LIBRO 9 Derecho RomanoDocument30 pagesLIBRO 9 Derecho RomanoDomingo VasquezNo ratings yet

- Wage and Tax Statement: OMB No. 1545-0008Document7 pagesWage and Tax Statement: OMB No. 1545-0008LUZILLE MEDINANo ratings yet

- W2 & Earnings: Emma MimsDocument1 pageW2 & Earnings: Emma MimsIsaiah MimsNo ratings yet

- 2020 Federal TurboTax ExtensionDocument1 page2020 Federal TurboTax ExtensiongeneNo ratings yet

- 0LH47 0LH47 0429 20180101 W2Report W2Report 001Document2 pages0LH47 0LH47 0429 20180101 W2Report W2Report 001charly4877No ratings yet

- Pay Stub - ROY STEPHENDocument6 pagesPay Stub - ROY STEPHENKeller Brown JnrNo ratings yet

- Fax Cover SheetDocument7 pagesFax Cover Sheettarijt240% (1)

- New Jersey Amended Resident Income Tax Return: A / / B / / C / / DDocument3 pagesNew Jersey Amended Resident Income Tax Return: A / / B / / C / / DЛена КиселеваNo ratings yet

- Schedule 1 For 2019 Form 1040Document1 pageSchedule 1 For 2019 Form 1040CNBC.comNo ratings yet

- TB US TaxRefund 2009 ENG PackDocument8 pagesTB US TaxRefund 2009 ENG Packabsolute_absurdNo ratings yet

- W2Document1,223 pagesW2Doru OanceaNo ratings yet

- Laura and John Arnold Foundation 2022 Tax Forms, Obtained by Gabe KaminskyDocument144 pagesLaura and John Arnold Foundation 2022 Tax Forms, Obtained by Gabe KaminskyGabe KaminskyNo ratings yet

- DSP Inc 1099-11 Print - CFMDocument1 pageDSP Inc 1099-11 Print - CFMJackson kaylaNo ratings yet

- CORRECTED (If Checked) : Payment Card and Third Party Network TransactionsDocument2 pagesCORRECTED (If Checked) : Payment Card and Third Party Network TransactionsCarter Nisely100% (1)

- 2019 W-2 Gregorio MartinezDocument2 pages2019 W-2 Gregorio Martinezporhj perraNo ratings yet

- January 6, 2021 Zechariah Kennedy 612 Colony Lakes DR Lexington, SC 29073-6742Document8 pagesJanuary 6, 2021 Zechariah Kennedy 612 Colony Lakes DR Lexington, SC 29073-6742Zechariah Kennedy100% (1)

- Shared Temp ELA0Request For Transcript of Tax Ret B 2 11 OutputDocument1 pageShared Temp ELA0Request For Transcript of Tax Ret B 2 11 OutputBlessing Nel GuillaumeNo ratings yet

- Show 2Document2 pagesShow 2Lexi BrownNo ratings yet

- Tax File 2106 Ss FileingDocument5 pagesTax File 2106 Ss FileingWALLAUERNo ratings yet

- MyComputerCareercom at Raleigh LLC-Aretha J BosireDocument1 pageMyComputerCareercom at Raleigh LLC-Aretha J BosireAretha JBNo ratings yet

- Repayment Application DocumentDocument10 pagesRepayment Application DocumentPratham TiwariNo ratings yet

- GKEDC Form 990 Page 1 For 2013 Through 2019Document7 pagesGKEDC Form 990 Page 1 For 2013 Through 2019Don MooreNo ratings yet

- Tax - 2020-2021 PDFDocument2 pagesTax - 2020-2021 PDFShanto ChowdhuryNo ratings yet

- 2021 - Robinhood Securities 1099Document8 pages2021 - Robinhood Securities 1099Estranged GedNo ratings yet

- 0LH47 0LH47 0429 20180101 1095report 001Document1 page0LH47 0LH47 0429 20180101 1095report 001charly4877No ratings yet

- Top of Form Panel 0 4 None 0 0: Legal Name: Social Security NumberDocument2 pagesTop of Form Panel 0 4 None 0 0: Legal Name: Social Security NumberJason RileyNo ratings yet

- Deed in LieuDocument33 pagesDeed in LieuSteven WhitfordNo ratings yet

- National Education Association's (NEA) Tax FormsDocument108 pagesNational Education Association's (NEA) Tax FormsJoeSchoffstallNo ratings yet

- Va W4Document4 pagesVa W4Jeannie ArringtonNo ratings yet

- U.S. Individual Income Tax Return: Filing StatusDocument2 pagesU.S. Individual Income Tax Return: Filing StatuspeachyNo ratings yet

- FD 941 Apr-Jun 2017 PDFDocument3 pagesFD 941 Apr-Jun 2017 PDFScott WinklerNo ratings yet

- 70 Kevin Lin PDFDocument8 pages70 Kevin Lin PDFKenneth LinNo ratings yet

- Electronic Filing Instructions For Your 2008 Federal Tax ReturnDocument14 pagesElectronic Filing Instructions For Your 2008 Federal Tax ReturnjakeNo ratings yet

- SSF SS 1098T PDFDocument1 pageSSF SS 1098T PDFJoseph FabreNo ratings yet

- Profit or Loss From Business: Schedule C (Form 1040) 09Document2 pagesProfit or Loss From Business: Schedule C (Form 1040) 09John Bean100% (1)

- U.S. Individual Income Tax Return: Filing StatusDocument2 pagesU.S. Individual Income Tax Return: Filing StatusSammi Bowe100% (1)

- 1098-T Copy B: 12,589.34 University of Oklahoma 1000 ASP AVE ROOM 105 Norman OK 73019 (405) 325-9000Document2 pages1098-T Copy B: 12,589.34 University of Oklahoma 1000 ASP AVE ROOM 105 Norman OK 73019 (405) 325-9000Lane ElliottNo ratings yet

- TY2019 - Fair Fight Action - Form 990-PDocument37 pagesTY2019 - Fair Fight Action - Form 990-PWashington ExaminerNo ratings yet

- $0 Copy B: Miscellaneous InformationDocument2 pages$0 Copy B: Miscellaneous InformationGustavo BonillaNo ratings yet

- Jaleica Coding and Billing LLC.: 437 Melissa Circle Romeoville IL.60446Document8 pagesJaleica Coding and Billing LLC.: 437 Melissa Circle Romeoville IL.60446Julius Masigan100% (1)

- f1040 - Schedule - C - 2019-00-00-ED SNIDER YOUTH HOCKEY FOUNDATIONDocument2 pagesf1040 - Schedule - C - 2019-00-00-ED SNIDER YOUTH HOCKEY FOUNDATIONKeller Brown Jnr50% (2)

- 1099 Ssdi 2010Document1 page1099 Ssdi 2010Gary McclainNo ratings yet

- UntitledDocument10 pagesUntitledJosh SofferNo ratings yet

- IBR FormDocument3 pagesIBR FormBlayne MozisekNo ratings yet

- Important Information About Form 1099-G: J Cruz 598 Courtlandt Av Apt 2B Bronx Ny 10451Document1 pageImportant Information About Form 1099-G: J Cruz 598 Courtlandt Av Apt 2B Bronx Ny 10451Victor ErazoNo ratings yet

- For 1099Document3 pagesFor 1099enudo SolomonNo ratings yet

- Jean Gil Linares 2023Document8 pagesJean Gil Linares 2023jeancarlosgil.linares1No ratings yet

- Merged DocumentDocument93 pagesMerged DocumentsurekhaNo ratings yet

- Vaccum Cleaner Bill 2019Document2 pagesVaccum Cleaner Bill 2019KrishnaKumar MNo ratings yet

- CBDT Circular No 14 XL-35 Dated 11041955Document2 pagesCBDT Circular No 14 XL-35 Dated 11041955arunjain022No ratings yet

- PNBONE Mpassbook 114911 5-5-2023 28-11-2023 1780XXXXXXXX83Document5 pagesPNBONE Mpassbook 114911 5-5-2023 28-11-2023 1780XXXXXXXX83jattkhatri4No ratings yet

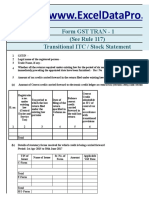

- GST TRAN 1 Return Excel TemplateDocument14 pagesGST TRAN 1 Return Excel TemplateRaju Ranjan KumarNo ratings yet

- ICARE First Preboard TAXDocument12 pagesICARE First Preboard TAXLuna VNo ratings yet

- Annexure 2Document13 pagesAnnexure 2anujbeniwalNo ratings yet

- 14Nov21-Brochure - Telemedicon-202Document2 pages14Nov21-Brochure - Telemedicon-202TULSI CHARAN DASNo ratings yet

- Quiz Chapter 2 Statement of Comprehensive IncomeDocument13 pagesQuiz Chapter 2 Statement of Comprehensive Incomefinn mertensNo ratings yet

- DD Employee Authorization Form EZPaynote 121621ADocument1 pageDD Employee Authorization Form EZPaynote 121621AaolincinboxNo ratings yet

- Challan 280Document2 pagesChallan 280Rahul SinglaNo ratings yet

- Visitor Permit Application FormDocument2 pagesVisitor Permit Application FormJames GiddingsNo ratings yet

- LLP Agreement Format For Removal of PartnerDocument2 pagesLLP Agreement Format For Removal of PartnersureshkumarNo ratings yet

- Amazon Welding M.C InvoiceDocument1 pageAmazon Welding M.C InvoiceSyprotech SolutionsNo ratings yet

- Collection Information Statement For Wage Earners and Self-Employed IndividualsDocument7 pagesCollection Information Statement For Wage Earners and Self-Employed IndividualsAnonymous dfLfinUrp60% (5)

- BankWORKS Acquiring BrochureDocument4 pagesBankWORKS Acquiring Brochurepriyak_chariNo ratings yet

- Sworn Statement For Tax Clearance SampleDocument1 pageSworn Statement For Tax Clearance SampleRachel ChanNo ratings yet

- Account Statement 011219 290220Document14 pagesAccount Statement 011219 290220ManishNo ratings yet

- Import License No. Hs Code Descrip On Pcs Fob Cif BM % BMT % PPN % PPNBM % PPH % BM (RP) BMT (RP) PPN (RP) PPNBM (RP) PPH (RP) Border Post BorderDocument1 pageImport License No. Hs Code Descrip On Pcs Fob Cif BM % BMT % PPN % PPNBM % PPH % BM (RP) BMT (RP) PPN (RP) PPNBM (RP) PPH (RP) Border Post BorderarcandraNo ratings yet

- EventsDocument42 pagesEventsumakamalftsNo ratings yet

- Conneqt Business Solutions Limited: 304994 Ashitosh MoreDocument1 pageConneqt Business Solutions Limited: 304994 Ashitosh MoreBhushan JadhavNo ratings yet

- Confirmation For Booking ID # 571708753Document1 pageConfirmation For Booking ID # 571708753Abdul Muhith PadilNo ratings yet

- Acc 324 Week 6 - 1Document3 pagesAcc 324 Week 6 - 1Accounting GuyNo ratings yet

- 210 - RFP - Sewa Ruangan, Internet, Listrik & Over Time SguDocument8 pages210 - RFP - Sewa Ruangan, Internet, Listrik & Over Time SguSulis SetioriniNo ratings yet

- Art Integrated Activity Source DocumntsDocument9 pagesArt Integrated Activity Source DocumntsFabzrocks FareehaNo ratings yet

- LP02 Trade Vendor Form E379!1!1Document1 pageLP02 Trade Vendor Form E379!1!1juniyantiNo ratings yet

- VisaMasterCard Card Auto DebitDocument2 pagesVisaMasterCard Card Auto DebitMuizz LynnNo ratings yet