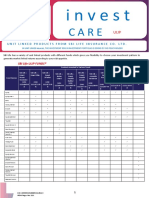

Fund Information: Launch Date Net Asset Value Per Unit (NAVPU) Bloomberg Ticker Total Fund NAV (MN)

Fund Information: Launch Date Net Asset Value Per Unit (NAVPU) Bloomberg Ticker Total Fund NAV (MN)

You might also like

- Polimeni and An (2024) SSRNDocument48 pagesPolimeni and An (2024) SSRNWSB-TVNo ratings yet

- Study Questions SolutionDocument7 pagesStudy Questions SolutionJessica100% (2)

- Business Valuation TemplateDocument2 pagesBusiness Valuation TemplateAkshay MathurNo ratings yet

- Fabozzi CH 03 Measuring Yield HW AnswersDocument5 pagesFabozzi CH 03 Measuring Yield HW AnswershardiNo ratings yet

- Aditya Birla Mutual FundDocument66 pagesAditya Birla Mutual Fundpratim shindeNo ratings yet

- Investment Objective Historical Performance: Pami Horizon Fund, IncDocument1 pageInvestment Objective Historical Performance: Pami Horizon Fund, IncRamil MontealtoNo ratings yet

- Fs PDFDocument1 pageFs PDFJuhaizan Mohd YusofNo ratings yet

- Fund Fact Sheets - Prosperity World Equity Index Feeder FundDocument1 pageFund Fact Sheets - Prosperity World Equity Index Feeder FundAJ HiltiNo ratings yet

- December 2020: Quarterly Commentary ReportDocument8 pagesDecember 2020: Quarterly Commentary ReportYog MehtaNo ratings yet

- BF Fund Fact Sheet Sep 2023Document2 pagesBF Fund Fact Sheet Sep 2023DAR RYLNo ratings yet

- Malabar Midcap Fund Monthly Factsheet - April 2024Document1 pageMalabar Midcap Fund Monthly Factsheet - April 2024Suleiman HaqNo ratings yet

- Report On Indonesia Financial Sector Development Q2 2023Document34 pagesReport On Indonesia Financial Sector Development Q2 2023Raymond SihotangNo ratings yet

- Vanguard Global Stock Index FundDocument4 pagesVanguard Global Stock Index FundjorgeperezsidecarshotmailomNo ratings yet

- Life InsuranceDocument10 pagesLife Insurancemegha_pawar_4No ratings yet

- FSISectoralFund MonthlyDocument1 pageFSISectoralFund MonthlyVNo ratings yet

- Global Balanced IndexDocument2 pagesGlobal Balanced Indexgbolaamusa1No ratings yet

- Welspun Enterprises LTD - Investor Presentation - 2Document36 pagesWelspun Enterprises LTD - Investor Presentation - 2Dwijendra ChanumoluNo ratings yet

- Hpam Ultima Ekuitas 1Document2 pagesHpam Ultima Ekuitas 1Esge KuNo ratings yet

- I Balanced Fund Apr 23Document3 pagesI Balanced Fund Apr 23mid_cycloneNo ratings yet

- 2021 DECEMBER Fund-Fact-SheetDocument41 pages2021 DECEMBER Fund-Fact-SheetRyan Jacob SolisNo ratings yet

- Jufo 26 05 2011 PDFDocument38 pagesJufo 26 05 2011 PDFMahmoud ElyamanyNo ratings yet

- Investmentz AugustDocument11 pagesInvestmentz AugustAnimesh PalNo ratings yet

- Jubilant Life Sciences Research Report PDFDocument50 pagesJubilant Life Sciences Research Report PDFAbhiroop DasNo ratings yet

- Peso Asia Pacific Property Income Fund - Fund Fact Sheet - October - 2020Document2 pagesPeso Asia Pacific Property Income Fund - Fund Fact Sheet - October - 2020Jayr LegaspiNo ratings yet

- What Does The Fund Invest In?: Sun Life Grepa Growth PLUS FundDocument1 pageWhat Does The Fund Invest In?: Sun Life Grepa Growth PLUS FundBee ThreeallNo ratings yet

- Peso Powerhouse Fund - Fund Fact Sheet - December - 2020Document2 pagesPeso Powerhouse Fund - Fund Fact Sheet - December - 2020Jayr LegaspiNo ratings yet

- Hpam Ultima Ekuitas 1Document2 pagesHpam Ultima Ekuitas 1Serly MarcelinaNo ratings yet

- PT JAPFA Comfeed Indonesia TBK: Muddling ThroughDocument7 pagesPT JAPFA Comfeed Indonesia TBK: Muddling Throughisramiz nurtantioNo ratings yet

- JG Summit Holdings Inco.: Industry: Food & Beverage Sector: Food ProductsDocument6 pagesJG Summit Holdings Inco.: Industry: Food & Beverage Sector: Food ProductsPatrickBeronaNo ratings yet

- Initiating Coverage - Unichem LabsDocument12 pagesInitiating Coverage - Unichem LabsshahavNo ratings yet

- Ishares Core S&P 500 Index Etf (Xus)Document4 pagesIshares Core S&P 500 Index Etf (Xus)Roi SoleilNo ratings yet

- Conservative Mutual Funds AssessmentDocument24 pagesConservative Mutual Funds AssessmentRula Abu NuwarNo ratings yet

- ATRAM Phil Equity Smart Index Fund Fact Sheet Apr 2020Document2 pagesATRAM Phil Equity Smart Index Fund Fact Sheet Apr 2020anton clementeNo ratings yet

- Strategic Bond Fund (59) : Fixed Income Investment GradeDocument2 pagesStrategic Bond Fund (59) : Fixed Income Investment GradeHayston DezmenNo ratings yet

- PBIC-Pakistan Credit Strategy 2011Document22 pagesPBIC-Pakistan Credit Strategy 2011hussainmhNo ratings yet

- Peso Emperor Fund - Fund Fact Sheet - October - 2020Document2 pagesPeso Emperor Fund - Fund Fact Sheet - October - 2020Jayr LegaspiNo ratings yet

- MP - 3 - Peso Growth FundDocument2 pagesMP - 3 - Peso Growth FundFrank TaquioNo ratings yet

- PIATAFDocument1 pagePIATAFEileen LauNo ratings yet

- MR DCVFM Vn30etf 202307Document1 pageMR DCVFM Vn30etf 202307ผีเสื้อ ราตรีNo ratings yet

- KUBCQ4Newsletter FinalDocument11 pagesKUBCQ4Newsletter FinalVenkata SubramanianNo ratings yet

- Fund Factsheet August 2022Document32 pagesFund Factsheet August 2022santhoshkumarNo ratings yet

- Strategy-2020 - IGISDocument74 pagesStrategy-2020 - IGISmuddasir1980No ratings yet

- MIDTERM PROJECT Group 2Document7 pagesMIDTERM PROJECT Group 2Jane GalangueNo ratings yet

- Tweedy Browne 1Q11Document13 pagesTweedy Browne 1Q11sbaines_1No ratings yet

- PRU - Asia Pacific Ex-Japan FundDocument2 pagesPRU - Asia Pacific Ex-Japan FundNapolean DynamiteNo ratings yet

- Global Multi-Asset Fund - Brochure - BancassuranceDocument3 pagesGlobal Multi-Asset Fund - Brochure - BancassuranceJeffrey Ru LouisNo ratings yet

- Weekly Wrap: Recovery Hopes Bolster PCOMP Above 6,600Document2 pagesWeekly Wrap: Recovery Hopes Bolster PCOMP Above 6,600Romel Alvendia ValenciaNo ratings yet

- Viewpdf 2Document3 pagesViewpdf 2gqq68mrnpmNo ratings yet

- Fund Fact Sheets NAVPU Captains FundDocument1 pageFund Fact Sheets NAVPU Captains FundJohh-RevNo ratings yet

- Adequity TrustDocument2 pagesAdequity TrustedenrealtyNo ratings yet

- Century Pacific Food: 1Q19: Tempered Opex Buoys MarginsDocument9 pagesCentury Pacific Food: 1Q19: Tempered Opex Buoys MarginsManjit Kour SinghNo ratings yet

- BMO Low Volatility US Equity ETF-EN-CAD UnitsDocument4 pagesBMO Low Volatility US Equity ETF-EN-CAD Unitsmaxime1.pelletierNo ratings yet

- Hpam Ultima Ekuitas 1: Month MonthDocument2 pagesHpam Ultima Ekuitas 1: Month MonthSaid Al MusayyabNo ratings yet

- JAI Budget HighlightsDocument20 pagesJAI Budget Highlightsghufran1986No ratings yet

- Equity Valuation Report - Corticeira AmorimDocument3 pagesEquity Valuation Report - Corticeira AmorimFEPFinanceClubNo ratings yet

- Infosys Annual Report AnalysisDocument9 pagesInfosys Annual Report AnalysisAbhishek PaulNo ratings yet

- ATRAM Alpha Opportunity Fund - Fact Sheet - Apr 2020Document2 pagesATRAM Alpha Opportunity Fund - Fact Sheet - Apr 2020anton clementeNo ratings yet

- ABYT Independent Research Report 20071217Document16 pagesABYT Independent Research Report 20071217minihero0806No ratings yet

- AD15 June11Document2 pagesAD15 June11Alvin LimNo ratings yet

- Asset Allocation Fund (5) : Hybrid Hybrid BalancedDocument2 pagesAsset Allocation Fund (5) : Hybrid Hybrid BalancedHayston DezmenNo ratings yet

- Japfa Comfeed Indonesia TBK (JPFA) : In-DepthDocument16 pagesJapfa Comfeed Indonesia TBK (JPFA) : In-DepthVictorioNo ratings yet

- 2023.05 - Asset Class Forecast - Q2 2023 - enDocument6 pages2023.05 - Asset Class Forecast - Q2 2023 - enAnshuman GhoshNo ratings yet

- Quantum Strategy II: Winning Strategies of Professional InvestmentFrom EverandQuantum Strategy II: Winning Strategies of Professional InvestmentNo ratings yet

- When Transfer Prices Are NeededDocument3 pagesWhen Transfer Prices Are NeededJasonNo ratings yet

- Convexity and Volatility PDFDocument20 pagesConvexity and Volatility PDFcaxapNo ratings yet

- Managingbenefits GuidanceDocument52 pagesManagingbenefits Guidancetitli123No ratings yet

- Mba ProjectDocument75 pagesMba Projectmicky101010No ratings yet

- Financial Consideration and Valuation of Family BusinessDocument7 pagesFinancial Consideration and Valuation of Family BusinessAbdinasir abdullahi AbdiNo ratings yet

- Bottom Up BetaDocument9 pagesBottom Up BetaFatima KhandwalaNo ratings yet

- Insurance Code Amended Insurers' Capital Raised: Michelle V. Remo Philippine Daily InquirerDocument1 pageInsurance Code Amended Insurers' Capital Raised: Michelle V. Remo Philippine Daily InquirerJonna Maye Loras CanindoNo ratings yet

- 2021 Cfa Liii Mockexam-Pm-NewDocument25 pages2021 Cfa Liii Mockexam-Pm-NewHoang Thi Phuong ThuyNo ratings yet

- 6 Key Lessons From Rich DadDocument31 pages6 Key Lessons From Rich DadBeowulf Odin SonNo ratings yet

- R Stdev: X X N X Var X StddevDocument2 pagesR Stdev: X X N X Var X StddevnngggNo ratings yet

- Algorithmic Trading Step-By-Step Guide To Develop Your Own Winning Trading Strategy Using Financial Machine Learning Without... (Investors Press) (Z-Library)Document124 pagesAlgorithmic Trading Step-By-Step Guide To Develop Your Own Winning Trading Strategy Using Financial Machine Learning Without... (Investors Press) (Z-Library)papa kingNo ratings yet

- Suguna Foods Private Limited ReportDocument8 pagesSuguna Foods Private Limited ReportSHRAYANS NAHATANo ratings yet

- Tutorial 2 SolDocument2 pagesTutorial 2 SolJess Xue100% (1)

- MartabeDocument51 pagesMartabebon1ngNo ratings yet

- L1 Module X Mini-Case Any Monkey Can Beat The MarketDocument5 pagesL1 Module X Mini-Case Any Monkey Can Beat The MarketZion WilliamsNo ratings yet

- 2024 Jan 18Document7 pages2024 Jan 18Alejandro MufardiniNo ratings yet

- Option Pricing of Crude Oil.Document5 pagesOption Pricing of Crude Oil.alexNo ratings yet

- Irc IiDocument473 pagesIrc Iihenrydpsinaga100% (1)

- SBI Life ULIP News Letter April 2023Document34 pagesSBI Life ULIP News Letter April 2023Kritika ThakurNo ratings yet

- Stockholders' Equity Accounts With Normal BalancesDocument3 pagesStockholders' Equity Accounts With Normal BalancesMary67% (3)

- Asset and Liability Management: Presented To Coronation Merchant Bank - Training SchoolDocument26 pagesAsset and Liability Management: Presented To Coronation Merchant Bank - Training SchoolBlake SheltonNo ratings yet

- Avendus Wealth ManagementDocument23 pagesAvendus Wealth ManagementAbhishek NoriNo ratings yet

- Auto Trender PPT SMCDocument14 pagesAuto Trender PPT SMCMithil Doshi100% (1)

- Case Study 1 Sugar BowlDocument3 pagesCase Study 1 Sugar BowlRuben F. Zh100% (1)

- Salary2Wealth PropositionDocument30 pagesSalary2Wealth Propositionpavan kumarNo ratings yet

- Russian Hostile Infiltration of The Western Financial System by Elements of Russian Government and KGBDocument33 pagesRussian Hostile Infiltration of The Western Financial System by Elements of Russian Government and KGBkabud100% (2)

Download as pdf or txt

You might also like

- Polimeni and An (2024) SSRNDocument48 pagesPolimeni and An (2024) SSRNWSB-TVNo ratings yet

- Study Questions SolutionDocument7 pagesStudy Questions SolutionJessica100% (2)

- Business Valuation TemplateDocument2 pagesBusiness Valuation TemplateAkshay MathurNo ratings yet

- Fabozzi CH 03 Measuring Yield HW AnswersDocument5 pagesFabozzi CH 03 Measuring Yield HW AnswershardiNo ratings yet

- Aditya Birla Mutual FundDocument66 pagesAditya Birla Mutual Fundpratim shindeNo ratings yet

- Investment Objective Historical Performance: Pami Horizon Fund, IncDocument1 pageInvestment Objective Historical Performance: Pami Horizon Fund, IncRamil MontealtoNo ratings yet

- Fs PDFDocument1 pageFs PDFJuhaizan Mohd YusofNo ratings yet

- Fund Fact Sheets - Prosperity World Equity Index Feeder FundDocument1 pageFund Fact Sheets - Prosperity World Equity Index Feeder FundAJ HiltiNo ratings yet

- December 2020: Quarterly Commentary ReportDocument8 pagesDecember 2020: Quarterly Commentary ReportYog MehtaNo ratings yet

- BF Fund Fact Sheet Sep 2023Document2 pagesBF Fund Fact Sheet Sep 2023DAR RYLNo ratings yet

- Malabar Midcap Fund Monthly Factsheet - April 2024Document1 pageMalabar Midcap Fund Monthly Factsheet - April 2024Suleiman HaqNo ratings yet

- Report On Indonesia Financial Sector Development Q2 2023Document34 pagesReport On Indonesia Financial Sector Development Q2 2023Raymond SihotangNo ratings yet

- Vanguard Global Stock Index FundDocument4 pagesVanguard Global Stock Index FundjorgeperezsidecarshotmailomNo ratings yet

- Life InsuranceDocument10 pagesLife Insurancemegha_pawar_4No ratings yet

- FSISectoralFund MonthlyDocument1 pageFSISectoralFund MonthlyVNo ratings yet

- Global Balanced IndexDocument2 pagesGlobal Balanced Indexgbolaamusa1No ratings yet

- Welspun Enterprises LTD - Investor Presentation - 2Document36 pagesWelspun Enterprises LTD - Investor Presentation - 2Dwijendra ChanumoluNo ratings yet

- Hpam Ultima Ekuitas 1Document2 pagesHpam Ultima Ekuitas 1Esge KuNo ratings yet

- I Balanced Fund Apr 23Document3 pagesI Balanced Fund Apr 23mid_cycloneNo ratings yet

- 2021 DECEMBER Fund-Fact-SheetDocument41 pages2021 DECEMBER Fund-Fact-SheetRyan Jacob SolisNo ratings yet

- Jufo 26 05 2011 PDFDocument38 pagesJufo 26 05 2011 PDFMahmoud ElyamanyNo ratings yet

- Investmentz AugustDocument11 pagesInvestmentz AugustAnimesh PalNo ratings yet

- Jubilant Life Sciences Research Report PDFDocument50 pagesJubilant Life Sciences Research Report PDFAbhiroop DasNo ratings yet

- Peso Asia Pacific Property Income Fund - Fund Fact Sheet - October - 2020Document2 pagesPeso Asia Pacific Property Income Fund - Fund Fact Sheet - October - 2020Jayr LegaspiNo ratings yet

- What Does The Fund Invest In?: Sun Life Grepa Growth PLUS FundDocument1 pageWhat Does The Fund Invest In?: Sun Life Grepa Growth PLUS FundBee ThreeallNo ratings yet

- Peso Powerhouse Fund - Fund Fact Sheet - December - 2020Document2 pagesPeso Powerhouse Fund - Fund Fact Sheet - December - 2020Jayr LegaspiNo ratings yet

- Hpam Ultima Ekuitas 1Document2 pagesHpam Ultima Ekuitas 1Serly MarcelinaNo ratings yet

- PT JAPFA Comfeed Indonesia TBK: Muddling ThroughDocument7 pagesPT JAPFA Comfeed Indonesia TBK: Muddling Throughisramiz nurtantioNo ratings yet

- JG Summit Holdings Inco.: Industry: Food & Beverage Sector: Food ProductsDocument6 pagesJG Summit Holdings Inco.: Industry: Food & Beverage Sector: Food ProductsPatrickBeronaNo ratings yet

- Initiating Coverage - Unichem LabsDocument12 pagesInitiating Coverage - Unichem LabsshahavNo ratings yet

- Ishares Core S&P 500 Index Etf (Xus)Document4 pagesIshares Core S&P 500 Index Etf (Xus)Roi SoleilNo ratings yet

- Conservative Mutual Funds AssessmentDocument24 pagesConservative Mutual Funds AssessmentRula Abu NuwarNo ratings yet

- ATRAM Phil Equity Smart Index Fund Fact Sheet Apr 2020Document2 pagesATRAM Phil Equity Smart Index Fund Fact Sheet Apr 2020anton clementeNo ratings yet

- Strategic Bond Fund (59) : Fixed Income Investment GradeDocument2 pagesStrategic Bond Fund (59) : Fixed Income Investment GradeHayston DezmenNo ratings yet

- PBIC-Pakistan Credit Strategy 2011Document22 pagesPBIC-Pakistan Credit Strategy 2011hussainmhNo ratings yet

- Peso Emperor Fund - Fund Fact Sheet - October - 2020Document2 pagesPeso Emperor Fund - Fund Fact Sheet - October - 2020Jayr LegaspiNo ratings yet

- MP - 3 - Peso Growth FundDocument2 pagesMP - 3 - Peso Growth FundFrank TaquioNo ratings yet

- PIATAFDocument1 pagePIATAFEileen LauNo ratings yet

- MR DCVFM Vn30etf 202307Document1 pageMR DCVFM Vn30etf 202307ผีเสื้อ ราตรีNo ratings yet

- KUBCQ4Newsletter FinalDocument11 pagesKUBCQ4Newsletter FinalVenkata SubramanianNo ratings yet

- Fund Factsheet August 2022Document32 pagesFund Factsheet August 2022santhoshkumarNo ratings yet

- Strategy-2020 - IGISDocument74 pagesStrategy-2020 - IGISmuddasir1980No ratings yet

- MIDTERM PROJECT Group 2Document7 pagesMIDTERM PROJECT Group 2Jane GalangueNo ratings yet

- Tweedy Browne 1Q11Document13 pagesTweedy Browne 1Q11sbaines_1No ratings yet

- PRU - Asia Pacific Ex-Japan FundDocument2 pagesPRU - Asia Pacific Ex-Japan FundNapolean DynamiteNo ratings yet

- Global Multi-Asset Fund - Brochure - BancassuranceDocument3 pagesGlobal Multi-Asset Fund - Brochure - BancassuranceJeffrey Ru LouisNo ratings yet

- Weekly Wrap: Recovery Hopes Bolster PCOMP Above 6,600Document2 pagesWeekly Wrap: Recovery Hopes Bolster PCOMP Above 6,600Romel Alvendia ValenciaNo ratings yet

- Viewpdf 2Document3 pagesViewpdf 2gqq68mrnpmNo ratings yet

- Fund Fact Sheets NAVPU Captains FundDocument1 pageFund Fact Sheets NAVPU Captains FundJohh-RevNo ratings yet

- Adequity TrustDocument2 pagesAdequity TrustedenrealtyNo ratings yet

- Century Pacific Food: 1Q19: Tempered Opex Buoys MarginsDocument9 pagesCentury Pacific Food: 1Q19: Tempered Opex Buoys MarginsManjit Kour SinghNo ratings yet

- BMO Low Volatility US Equity ETF-EN-CAD UnitsDocument4 pagesBMO Low Volatility US Equity ETF-EN-CAD Unitsmaxime1.pelletierNo ratings yet

- Hpam Ultima Ekuitas 1: Month MonthDocument2 pagesHpam Ultima Ekuitas 1: Month MonthSaid Al MusayyabNo ratings yet

- JAI Budget HighlightsDocument20 pagesJAI Budget Highlightsghufran1986No ratings yet

- Equity Valuation Report - Corticeira AmorimDocument3 pagesEquity Valuation Report - Corticeira AmorimFEPFinanceClubNo ratings yet

- Infosys Annual Report AnalysisDocument9 pagesInfosys Annual Report AnalysisAbhishek PaulNo ratings yet

- ATRAM Alpha Opportunity Fund - Fact Sheet - Apr 2020Document2 pagesATRAM Alpha Opportunity Fund - Fact Sheet - Apr 2020anton clementeNo ratings yet

- ABYT Independent Research Report 20071217Document16 pagesABYT Independent Research Report 20071217minihero0806No ratings yet

- AD15 June11Document2 pagesAD15 June11Alvin LimNo ratings yet

- Asset Allocation Fund (5) : Hybrid Hybrid BalancedDocument2 pagesAsset Allocation Fund (5) : Hybrid Hybrid BalancedHayston DezmenNo ratings yet

- Japfa Comfeed Indonesia TBK (JPFA) : In-DepthDocument16 pagesJapfa Comfeed Indonesia TBK (JPFA) : In-DepthVictorioNo ratings yet

- 2023.05 - Asset Class Forecast - Q2 2023 - enDocument6 pages2023.05 - Asset Class Forecast - Q2 2023 - enAnshuman GhoshNo ratings yet

- Quantum Strategy II: Winning Strategies of Professional InvestmentFrom EverandQuantum Strategy II: Winning Strategies of Professional InvestmentNo ratings yet

- When Transfer Prices Are NeededDocument3 pagesWhen Transfer Prices Are NeededJasonNo ratings yet

- Convexity and Volatility PDFDocument20 pagesConvexity and Volatility PDFcaxapNo ratings yet

- Managingbenefits GuidanceDocument52 pagesManagingbenefits Guidancetitli123No ratings yet

- Mba ProjectDocument75 pagesMba Projectmicky101010No ratings yet

- Financial Consideration and Valuation of Family BusinessDocument7 pagesFinancial Consideration and Valuation of Family BusinessAbdinasir abdullahi AbdiNo ratings yet

- Bottom Up BetaDocument9 pagesBottom Up BetaFatima KhandwalaNo ratings yet

- Insurance Code Amended Insurers' Capital Raised: Michelle V. Remo Philippine Daily InquirerDocument1 pageInsurance Code Amended Insurers' Capital Raised: Michelle V. Remo Philippine Daily InquirerJonna Maye Loras CanindoNo ratings yet

- 2021 Cfa Liii Mockexam-Pm-NewDocument25 pages2021 Cfa Liii Mockexam-Pm-NewHoang Thi Phuong ThuyNo ratings yet

- 6 Key Lessons From Rich DadDocument31 pages6 Key Lessons From Rich DadBeowulf Odin SonNo ratings yet

- R Stdev: X X N X Var X StddevDocument2 pagesR Stdev: X X N X Var X StddevnngggNo ratings yet

- Algorithmic Trading Step-By-Step Guide To Develop Your Own Winning Trading Strategy Using Financial Machine Learning Without... (Investors Press) (Z-Library)Document124 pagesAlgorithmic Trading Step-By-Step Guide To Develop Your Own Winning Trading Strategy Using Financial Machine Learning Without... (Investors Press) (Z-Library)papa kingNo ratings yet

- Suguna Foods Private Limited ReportDocument8 pagesSuguna Foods Private Limited ReportSHRAYANS NAHATANo ratings yet

- Tutorial 2 SolDocument2 pagesTutorial 2 SolJess Xue100% (1)

- MartabeDocument51 pagesMartabebon1ngNo ratings yet

- L1 Module X Mini-Case Any Monkey Can Beat The MarketDocument5 pagesL1 Module X Mini-Case Any Monkey Can Beat The MarketZion WilliamsNo ratings yet

- 2024 Jan 18Document7 pages2024 Jan 18Alejandro MufardiniNo ratings yet

- Option Pricing of Crude Oil.Document5 pagesOption Pricing of Crude Oil.alexNo ratings yet

- Irc IiDocument473 pagesIrc Iihenrydpsinaga100% (1)

- SBI Life ULIP News Letter April 2023Document34 pagesSBI Life ULIP News Letter April 2023Kritika ThakurNo ratings yet

- Stockholders' Equity Accounts With Normal BalancesDocument3 pagesStockholders' Equity Accounts With Normal BalancesMary67% (3)

- Asset and Liability Management: Presented To Coronation Merchant Bank - Training SchoolDocument26 pagesAsset and Liability Management: Presented To Coronation Merchant Bank - Training SchoolBlake SheltonNo ratings yet

- Avendus Wealth ManagementDocument23 pagesAvendus Wealth ManagementAbhishek NoriNo ratings yet

- Auto Trender PPT SMCDocument14 pagesAuto Trender PPT SMCMithil Doshi100% (1)

- Case Study 1 Sugar BowlDocument3 pagesCase Study 1 Sugar BowlRuben F. Zh100% (1)

- Salary2Wealth PropositionDocument30 pagesSalary2Wealth Propositionpavan kumarNo ratings yet

- Russian Hostile Infiltration of The Western Financial System by Elements of Russian Government and KGBDocument33 pagesRussian Hostile Infiltration of The Western Financial System by Elements of Russian Government and KGBkabud100% (2)