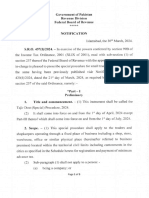

Sec 114

Sec 114

You might also like

- Dependent PrepositionsDocument3 pagesDependent Prepositionsvyvyly80% (20)

- WETEX Latest 2023 - Booklet - EngDocument11 pagesWETEX Latest 2023 - Booklet - Engsanjay nepaliNo ratings yet

- The Sales Tax Act, 1990Document509 pagesThe Sales Tax Act, 1990Muhammad Hassaan AhmadNo ratings yet

- Sales Tax Act, 1990 (Amended-Upto-01!07!2021)Document271 pagesSales Tax Act, 1990 (Amended-Upto-01!07!2021)Taimur RahmanNo ratings yet

- Finance Bill 2018Document36 pagesFinance Bill 2018Iddi KassiNo ratings yet

- Tax Laws Updates For December 2013Document72 pagesTax Laws Updates For December 2013Archana ThirunagariNo ratings yet

- The Workers' Welfare Fund Ordinance, 1971: PreliminaryDocument11 pagesThe Workers' Welfare Fund Ordinance, 1971: PreliminaryChad HarrisNo ratings yet

- Income Tax ActDocument126 pagesIncome Tax ActRohit ThakuriNo ratings yet

- Tax Laws Updates For June 2013 ExamsDocument68 pagesTax Laws Updates For June 2013 Examsnisarg_No ratings yet

- TDS Not DeductDocument6 pagesTDS Not DeductAnil WayanadNo ratings yet

- Income Tax Act, 1961Document13 pagesIncome Tax Act, 1961Sanketh_Surey_6489No ratings yet

- Income Tax Ordinance 2001 Updated Till 30.06.2016Document544 pagesIncome Tax Ordinance 2001 Updated Till 30.06.2016Nazim Iqbal0% (1)

- Income Tax Ordinance, 2001: Government of PakistanDocument550 pagesIncome Tax Ordinance, 2001: Government of PakistanShehzad RaufNo ratings yet

- It Act - Part I PDFDocument637 pagesIt Act - Part I PDFKritika SinghNo ratings yet

- Section 137 To 146aDocument11 pagesSection 137 To 146aSher DilNo ratings yet

- IT Ordinance, 1984 As of July, 2019Document389 pagesIT Ordinance, 1984 As of July, 2019rabeeiNo ratings yet

- DT RTP NovDocument52 pagesDT RTP NovKeshav KhandelwalNo ratings yet

- Finance Act 2022Document43 pagesFinance Act 2022Mark GechureNo ratings yet

- Seventh Schedule Updated Till 20.04.2023Document12 pagesSeventh Schedule Updated Till 20.04.2023Ahmed Yar KhanNo ratings yet

- Tax Credits 61. Charitable Donations.Document15 pagesTax Credits 61. Charitable Donations.Siddiqui Muhammad AshfaqueNo ratings yet

- Advance RulingsDocument7 pagesAdvance RulingsManohar LalNo ratings yet

- Explanation:-For The Purposes of This Sub-Rule, The ExpressionsDocument5 pagesExplanation:-For The Purposes of This Sub-Rule, The ExpressionsRakesh BenganiNo ratings yet

- Income Tax ActDocument812 pagesIncome Tax ActvermanavalNo ratings yet

- Commercial Tax LawDocument39 pagesCommercial Tax LawAnonymous I5hdhuCxNo ratings yet

- Income Tax Ordinance, 2001Document774 pagesIncome Tax Ordinance, 2001Ahmed Yar KhanNo ratings yet

- Incom Tax 2....Document7 pagesIncom Tax 2....SohaibNo ratings yet

- Tax Audit ReportDocument18 pagesTax Audit ReportNeha DenglaNo ratings yet

- Income Tax ActDocument801 pagesIncome Tax Actrsanofar.1993No ratings yet

- The Income Tax Ordinance, 1984 (CHAPTER-VI Exemptions and Allowances)Document12 pagesThe Income Tax Ordinance, 1984 (CHAPTER-VI Exemptions and Allowances)Tareq ChowdhuryNo ratings yet

- Lecture Synopsis-2 For Overall Discussion On Principles of TaxationDocument8 pagesLecture Synopsis-2 For Overall Discussion On Principles of TaxationProgga MehnazNo ratings yet

- Sro 457Document5 pagesSro 457Farhan NazirNo ratings yet

- The Income Tax (Am) Act, 2020Document10 pagesThe Income Tax (Am) Act, 2020TonyNo ratings yet

- Income Tax Ordinance, 2001: Government of PakistanDocument670 pagesIncome Tax Ordinance, 2001: Government of PakistanRiffat AsgharNo ratings yet

- Income Tax (Amendment) Bill, 2024Document18 pagesIncome Tax (Amendment) Bill, 2024RebeccaNo ratings yet

- Income Tax Ordinance, 2001: Government of PakistanDocument715 pagesIncome Tax Ordinance, 2001: Government of PakistanAmir MughalNo ratings yet

- GSTNTF55Document7 pagesGSTNTF55JGVNo ratings yet

- Indian Income Tax Act 2008Document1,065 pagesIndian Income Tax Act 2008ananthca100% (2)

- Tax Ordinance Sub Section 114 and 115Document4 pagesTax Ordinance Sub Section 114 and 115faiz kamranNo ratings yet

- Iris FAQsDocument74 pagesIris FAQsHammad SalahuddinNo ratings yet

- The Sales Tax Rules 2006Document99 pagesThe Sales Tax Rules 2006Hassan RazaNo ratings yet

- 2020812168165722SalesTaxAct, 1990updatedupto (30 06 2020)Document273 pages2020812168165722SalesTaxAct, 1990updatedupto (30 06 2020)Farhan RafiqNo ratings yet

- B27B_2023_Companies_Amendment_Bill (1)Document20 pagesB27B_2023_Companies_Amendment_Bill (1)mostu922No ratings yet

- Chapter 3: Meetings of Board and Its Powers: 1) Amendment in Section 173 - Rule 4Document8 pagesChapter 3: Meetings of Board and Its Powers: 1) Amendment in Section 173 - Rule 4anil agarwalNo ratings yet

- Income Tax Ordinance, 2001: Government of PakistanDocument574 pagesIncome Tax Ordinance, 2001: Government of PakistanadnanjavNo ratings yet

- Payments To Non-ResidentsDocument8 pagesPayments To Non-Residentssmyns.bwNo ratings yet

- 2021841585948283SalesTaxAct, 1990updatedupto30 06 2021Document286 pages2021841585948283SalesTaxAct, 1990updatedupto30 06 2021Farooq AkramNo ratings yet

- Seventh Schedule Updated Till 20.04.2023Document12 pagesSeventh Schedule Updated Till 20.04.2023ali aabisNo ratings yet

- Chapter VIII Rebates and ReliefsDocument14 pagesChapter VIII Rebates and ReliefsShweta VermaNo ratings yet

- Create LawDocument56 pagesCreate Lawcall.ppmgyNo ratings yet

- Taxguru Consultancy & Online Publication LLPDocument24 pagesTaxguru Consultancy & Online Publication LLPPiyush SharmaNo ratings yet

- ANTIGUA and BARBUDA Law Miscellaneous Amendments Bill 2018-PVDocument10 pagesANTIGUA and BARBUDA Law Miscellaneous Amendments Bill 2018-PVOw EmanNo ratings yet

- Capital GainsDocument26 pagesCapital GainsGavinNo ratings yet

- Income Tax Lawproclamation No 173 of 1961Document19 pagesIncome Tax Lawproclamation No 173 of 1961Saam MohaNo ratings yet

- 01 Law1993Document17 pages01 Law1993GgoudNo ratings yet

- Create LawDocument47 pagesCreate LawRen Mar CruzNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- QCR Required For CompaniesDocument1 pageQCR Required For CompanieswaqaswaNo ratings yet

- Small Medium and Large CompaniesDocument3 pagesSmall Medium and Large CompanieswaqaswaNo ratings yet

- CPR ProcedureDocument2 pagesCPR ProcedurewaqaswaNo ratings yet

- Audit Fee by IcapDocument2 pagesAudit Fee by IcapwaqaswaNo ratings yet

- 9 (2) Mir-Iv-2008 (239) 12122022 35747 PMDocument32 pages9 (2) Mir-Iv-2008 (239) 12122022 35747 PMwaqaswaNo ratings yet

- By LawsDocument11 pagesBy LawswaqaswaNo ratings yet

- Phase 4 MapDocument1 pagePhase 4 MapwaqaswaNo ratings yet

- Government of Pakistan Revenue Division Federal Board of RevenueDocument17 pagesGovernment of Pakistan Revenue Division Federal Board of RevenuewaqaswaNo ratings yet

- Federal Board of RevenueDocument9 pagesFederal Board of RevenuewaqaswaNo ratings yet

- Aquino Stands Pat On SK AbolitionDocument20 pagesAquino Stands Pat On SK AbolitionKarl Lara100% (1)

- Professional Security ConsultantsDocument21 pagesProfessional Security ConsultantsJason HerseyNo ratings yet

- Statement Ending 11/30/2022: Summary of AccountsDocument4 pagesStatement Ending 11/30/2022: Summary of AccountsGrégoire TSHIBUYI KATINANo ratings yet

- Pacific Red House Corporation v. Ca, 719 Scra 665Document3 pagesPacific Red House Corporation v. Ca, 719 Scra 665AprilNo ratings yet

- Grievance Machinery and Voluntary ArbitrationDocument3 pagesGrievance Machinery and Voluntary ArbitrationRusty NomadNo ratings yet

- Tutorial 3 - MistakeDocument3 pagesTutorial 3 - Mistakejoanne wongNo ratings yet

- Deed of Family Settlement Between Rival ClaimantsDocument4 pagesDeed of Family Settlement Between Rival ClaimantsMahebub Ghante100% (1)

- Advantest U3641 OperationDocument524 pagesAdvantest U3641 OperationDrewNo ratings yet

- Civpro 10Document2 pagesCivpro 10Jan NiñoNo ratings yet

- Autodesk - 300 Records Profiling - 2nd Lot For ValidationDocument21 pagesAutodesk - 300 Records Profiling - 2nd Lot For ValidationVainiNo ratings yet

- Cariño v. Insular GovernmentDocument5 pagesCariño v. Insular GovernmentJuris PrudenceNo ratings yet

- Civic EducationDocument4 pagesCivic EducationmanuelgraphyxNo ratings yet

- C AE26 MODULE 2 Tax Laws and Tax AdministrationDocument6 pagesC AE26 MODULE 2 Tax Laws and Tax AdministrationBaek hyunNo ratings yet

- BF Goodrich Confidential and Salaried Employees Union v. BF Goodrich, Phils. Inc., 49 SCRA 532Document14 pagesBF Goodrich Confidential and Salaried Employees Union v. BF Goodrich, Phils. Inc., 49 SCRA 532FD BalitaNo ratings yet

- Answer To ComplaintDocument20 pagesAnswer To ComplaintRonna Faith MonzonNo ratings yet

- Arctic Air Acp ManualDocument7 pagesArctic Air Acp ManualvovobossNo ratings yet

- Angeles, Et Al. vs. Ursula Calasanz, Et Al., G.R. No. L-42283, March 18, 1985Document13 pagesAngeles, Et Al. vs. Ursula Calasanz, Et Al., G.R. No. L-42283, March 18, 1985Lloyd Bryne LunzagaNo ratings yet

- People Vs Rosenthal Case DigestDocument2 pagesPeople Vs Rosenthal Case DigestJessamine OrioqueNo ratings yet

- Quorom: LA CARLOTA CITY v. ATTY. REX ROJO (G.R. No. 181367, April 24, 2012)Document23 pagesQuorom: LA CARLOTA CITY v. ATTY. REX ROJO (G.R. No. 181367, April 24, 2012)Ed Von Fernandez CidNo ratings yet

- EU Directives SummaryDocument2 pagesEU Directives SummaryAndres HidalgoNo ratings yet

- Year / Sem Code Subject Units Pre-ReqDocument4 pagesYear / Sem Code Subject Units Pre-ReqthebeautyinsideNo ratings yet

- Form 32ADocument2 pagesForm 32Apvr2k1No ratings yet

- PatDocument6 pagesPatFrances Angelie NacepoNo ratings yet

- Moot Court Memorial RESPONDENTDocument13 pagesMoot Court Memorial RESPONDENTKirtiiii TikamNo ratings yet

- Bernstein v. Pamson Motors LTDDocument8 pagesBernstein v. Pamson Motors LTDMichelle XavierNo ratings yet

- Kalle McWhorter, Prestigious Pets v. Duchouquette: DocketDocument2 pagesKalle McWhorter, Prestigious Pets v. Duchouquette: DocketDefiantly.netNo ratings yet

- Bar Q and A w7Document5 pagesBar Q and A w7klio11111No ratings yet

- 15 TUCP vs. NHADocument7 pages15 TUCP vs. NHAchristopher d. balubayanNo ratings yet

Download as pdf or txt

You might also like

- Dependent PrepositionsDocument3 pagesDependent Prepositionsvyvyly80% (20)

- WETEX Latest 2023 - Booklet - EngDocument11 pagesWETEX Latest 2023 - Booklet - Engsanjay nepaliNo ratings yet

- The Sales Tax Act, 1990Document509 pagesThe Sales Tax Act, 1990Muhammad Hassaan AhmadNo ratings yet

- Sales Tax Act, 1990 (Amended-Upto-01!07!2021)Document271 pagesSales Tax Act, 1990 (Amended-Upto-01!07!2021)Taimur RahmanNo ratings yet

- Finance Bill 2018Document36 pagesFinance Bill 2018Iddi KassiNo ratings yet

- Tax Laws Updates For December 2013Document72 pagesTax Laws Updates For December 2013Archana ThirunagariNo ratings yet

- The Workers' Welfare Fund Ordinance, 1971: PreliminaryDocument11 pagesThe Workers' Welfare Fund Ordinance, 1971: PreliminaryChad HarrisNo ratings yet

- Income Tax ActDocument126 pagesIncome Tax ActRohit ThakuriNo ratings yet

- Tax Laws Updates For June 2013 ExamsDocument68 pagesTax Laws Updates For June 2013 Examsnisarg_No ratings yet

- TDS Not DeductDocument6 pagesTDS Not DeductAnil WayanadNo ratings yet

- Income Tax Act, 1961Document13 pagesIncome Tax Act, 1961Sanketh_Surey_6489No ratings yet

- Income Tax Ordinance 2001 Updated Till 30.06.2016Document544 pagesIncome Tax Ordinance 2001 Updated Till 30.06.2016Nazim Iqbal0% (1)

- Income Tax Ordinance, 2001: Government of PakistanDocument550 pagesIncome Tax Ordinance, 2001: Government of PakistanShehzad RaufNo ratings yet

- It Act - Part I PDFDocument637 pagesIt Act - Part I PDFKritika SinghNo ratings yet

- Section 137 To 146aDocument11 pagesSection 137 To 146aSher DilNo ratings yet

- IT Ordinance, 1984 As of July, 2019Document389 pagesIT Ordinance, 1984 As of July, 2019rabeeiNo ratings yet

- DT RTP NovDocument52 pagesDT RTP NovKeshav KhandelwalNo ratings yet

- Finance Act 2022Document43 pagesFinance Act 2022Mark GechureNo ratings yet

- Seventh Schedule Updated Till 20.04.2023Document12 pagesSeventh Schedule Updated Till 20.04.2023Ahmed Yar KhanNo ratings yet

- Tax Credits 61. Charitable Donations.Document15 pagesTax Credits 61. Charitable Donations.Siddiqui Muhammad AshfaqueNo ratings yet

- Advance RulingsDocument7 pagesAdvance RulingsManohar LalNo ratings yet

- Explanation:-For The Purposes of This Sub-Rule, The ExpressionsDocument5 pagesExplanation:-For The Purposes of This Sub-Rule, The ExpressionsRakesh BenganiNo ratings yet

- Income Tax ActDocument812 pagesIncome Tax ActvermanavalNo ratings yet

- Commercial Tax LawDocument39 pagesCommercial Tax LawAnonymous I5hdhuCxNo ratings yet

- Income Tax Ordinance, 2001Document774 pagesIncome Tax Ordinance, 2001Ahmed Yar KhanNo ratings yet

- Incom Tax 2....Document7 pagesIncom Tax 2....SohaibNo ratings yet

- Tax Audit ReportDocument18 pagesTax Audit ReportNeha DenglaNo ratings yet

- Income Tax ActDocument801 pagesIncome Tax Actrsanofar.1993No ratings yet

- The Income Tax Ordinance, 1984 (CHAPTER-VI Exemptions and Allowances)Document12 pagesThe Income Tax Ordinance, 1984 (CHAPTER-VI Exemptions and Allowances)Tareq ChowdhuryNo ratings yet

- Lecture Synopsis-2 For Overall Discussion On Principles of TaxationDocument8 pagesLecture Synopsis-2 For Overall Discussion On Principles of TaxationProgga MehnazNo ratings yet

- Sro 457Document5 pagesSro 457Farhan NazirNo ratings yet

- The Income Tax (Am) Act, 2020Document10 pagesThe Income Tax (Am) Act, 2020TonyNo ratings yet

- Income Tax Ordinance, 2001: Government of PakistanDocument670 pagesIncome Tax Ordinance, 2001: Government of PakistanRiffat AsgharNo ratings yet

- Income Tax (Amendment) Bill, 2024Document18 pagesIncome Tax (Amendment) Bill, 2024RebeccaNo ratings yet

- Income Tax Ordinance, 2001: Government of PakistanDocument715 pagesIncome Tax Ordinance, 2001: Government of PakistanAmir MughalNo ratings yet

- GSTNTF55Document7 pagesGSTNTF55JGVNo ratings yet

- Indian Income Tax Act 2008Document1,065 pagesIndian Income Tax Act 2008ananthca100% (2)

- Tax Ordinance Sub Section 114 and 115Document4 pagesTax Ordinance Sub Section 114 and 115faiz kamranNo ratings yet

- Iris FAQsDocument74 pagesIris FAQsHammad SalahuddinNo ratings yet

- The Sales Tax Rules 2006Document99 pagesThe Sales Tax Rules 2006Hassan RazaNo ratings yet

- 2020812168165722SalesTaxAct, 1990updatedupto (30 06 2020)Document273 pages2020812168165722SalesTaxAct, 1990updatedupto (30 06 2020)Farhan RafiqNo ratings yet

- B27B_2023_Companies_Amendment_Bill (1)Document20 pagesB27B_2023_Companies_Amendment_Bill (1)mostu922No ratings yet

- Chapter 3: Meetings of Board and Its Powers: 1) Amendment in Section 173 - Rule 4Document8 pagesChapter 3: Meetings of Board and Its Powers: 1) Amendment in Section 173 - Rule 4anil agarwalNo ratings yet

- Income Tax Ordinance, 2001: Government of PakistanDocument574 pagesIncome Tax Ordinance, 2001: Government of PakistanadnanjavNo ratings yet

- Payments To Non-ResidentsDocument8 pagesPayments To Non-Residentssmyns.bwNo ratings yet

- 2021841585948283SalesTaxAct, 1990updatedupto30 06 2021Document286 pages2021841585948283SalesTaxAct, 1990updatedupto30 06 2021Farooq AkramNo ratings yet

- Seventh Schedule Updated Till 20.04.2023Document12 pagesSeventh Schedule Updated Till 20.04.2023ali aabisNo ratings yet

- Chapter VIII Rebates and ReliefsDocument14 pagesChapter VIII Rebates and ReliefsShweta VermaNo ratings yet

- Create LawDocument56 pagesCreate Lawcall.ppmgyNo ratings yet

- Taxguru Consultancy & Online Publication LLPDocument24 pagesTaxguru Consultancy & Online Publication LLPPiyush SharmaNo ratings yet

- ANTIGUA and BARBUDA Law Miscellaneous Amendments Bill 2018-PVDocument10 pagesANTIGUA and BARBUDA Law Miscellaneous Amendments Bill 2018-PVOw EmanNo ratings yet

- Capital GainsDocument26 pagesCapital GainsGavinNo ratings yet

- Income Tax Lawproclamation No 173 of 1961Document19 pagesIncome Tax Lawproclamation No 173 of 1961Saam MohaNo ratings yet

- 01 Law1993Document17 pages01 Law1993GgoudNo ratings yet

- Create LawDocument47 pagesCreate LawRen Mar CruzNo ratings yet

- Industrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisFrom EverandIndustrial Enterprises Act 2020 (2076): A brief Overview and Comparative AnalysisNo ratings yet

- QCR Required For CompaniesDocument1 pageQCR Required For CompanieswaqaswaNo ratings yet

- Small Medium and Large CompaniesDocument3 pagesSmall Medium and Large CompanieswaqaswaNo ratings yet

- CPR ProcedureDocument2 pagesCPR ProcedurewaqaswaNo ratings yet

- Audit Fee by IcapDocument2 pagesAudit Fee by IcapwaqaswaNo ratings yet

- 9 (2) Mir-Iv-2008 (239) 12122022 35747 PMDocument32 pages9 (2) Mir-Iv-2008 (239) 12122022 35747 PMwaqaswaNo ratings yet

- By LawsDocument11 pagesBy LawswaqaswaNo ratings yet

- Phase 4 MapDocument1 pagePhase 4 MapwaqaswaNo ratings yet

- Government of Pakistan Revenue Division Federal Board of RevenueDocument17 pagesGovernment of Pakistan Revenue Division Federal Board of RevenuewaqaswaNo ratings yet

- Federal Board of RevenueDocument9 pagesFederal Board of RevenuewaqaswaNo ratings yet

- Aquino Stands Pat On SK AbolitionDocument20 pagesAquino Stands Pat On SK AbolitionKarl Lara100% (1)

- Professional Security ConsultantsDocument21 pagesProfessional Security ConsultantsJason HerseyNo ratings yet

- Statement Ending 11/30/2022: Summary of AccountsDocument4 pagesStatement Ending 11/30/2022: Summary of AccountsGrégoire TSHIBUYI KATINANo ratings yet

- Pacific Red House Corporation v. Ca, 719 Scra 665Document3 pagesPacific Red House Corporation v. Ca, 719 Scra 665AprilNo ratings yet

- Grievance Machinery and Voluntary ArbitrationDocument3 pagesGrievance Machinery and Voluntary ArbitrationRusty NomadNo ratings yet

- Tutorial 3 - MistakeDocument3 pagesTutorial 3 - Mistakejoanne wongNo ratings yet

- Deed of Family Settlement Between Rival ClaimantsDocument4 pagesDeed of Family Settlement Between Rival ClaimantsMahebub Ghante100% (1)

- Advantest U3641 OperationDocument524 pagesAdvantest U3641 OperationDrewNo ratings yet

- Civpro 10Document2 pagesCivpro 10Jan NiñoNo ratings yet

- Autodesk - 300 Records Profiling - 2nd Lot For ValidationDocument21 pagesAutodesk - 300 Records Profiling - 2nd Lot For ValidationVainiNo ratings yet

- Cariño v. Insular GovernmentDocument5 pagesCariño v. Insular GovernmentJuris PrudenceNo ratings yet

- Civic EducationDocument4 pagesCivic EducationmanuelgraphyxNo ratings yet

- C AE26 MODULE 2 Tax Laws and Tax AdministrationDocument6 pagesC AE26 MODULE 2 Tax Laws and Tax AdministrationBaek hyunNo ratings yet

- BF Goodrich Confidential and Salaried Employees Union v. BF Goodrich, Phils. Inc., 49 SCRA 532Document14 pagesBF Goodrich Confidential and Salaried Employees Union v. BF Goodrich, Phils. Inc., 49 SCRA 532FD BalitaNo ratings yet

- Answer To ComplaintDocument20 pagesAnswer To ComplaintRonna Faith MonzonNo ratings yet

- Arctic Air Acp ManualDocument7 pagesArctic Air Acp ManualvovobossNo ratings yet

- Angeles, Et Al. vs. Ursula Calasanz, Et Al., G.R. No. L-42283, March 18, 1985Document13 pagesAngeles, Et Al. vs. Ursula Calasanz, Et Al., G.R. No. L-42283, March 18, 1985Lloyd Bryne LunzagaNo ratings yet

- People Vs Rosenthal Case DigestDocument2 pagesPeople Vs Rosenthal Case DigestJessamine OrioqueNo ratings yet

- Quorom: LA CARLOTA CITY v. ATTY. REX ROJO (G.R. No. 181367, April 24, 2012)Document23 pagesQuorom: LA CARLOTA CITY v. ATTY. REX ROJO (G.R. No. 181367, April 24, 2012)Ed Von Fernandez CidNo ratings yet

- EU Directives SummaryDocument2 pagesEU Directives SummaryAndres HidalgoNo ratings yet

- Year / Sem Code Subject Units Pre-ReqDocument4 pagesYear / Sem Code Subject Units Pre-ReqthebeautyinsideNo ratings yet

- Form 32ADocument2 pagesForm 32Apvr2k1No ratings yet

- PatDocument6 pagesPatFrances Angelie NacepoNo ratings yet

- Moot Court Memorial RESPONDENTDocument13 pagesMoot Court Memorial RESPONDENTKirtiiii TikamNo ratings yet

- Bernstein v. Pamson Motors LTDDocument8 pagesBernstein v. Pamson Motors LTDMichelle XavierNo ratings yet

- Kalle McWhorter, Prestigious Pets v. Duchouquette: DocketDocument2 pagesKalle McWhorter, Prestigious Pets v. Duchouquette: DocketDefiantly.netNo ratings yet

- Bar Q and A w7Document5 pagesBar Q and A w7klio11111No ratings yet

- 15 TUCP vs. NHADocument7 pages15 TUCP vs. NHAchristopher d. balubayanNo ratings yet