Download as docx, pdf, or txt

You might also like

- ACCT 338 Module Ten in Class Activities SOLUTION 1Document14 pagesACCT 338 Module Ten in Class Activities SOLUTION 1Cali100% (1)

- Lecture Notes - STD Costing and Variance AnalysisDocument6 pagesLecture Notes - STD Costing and Variance AnalysisBarby Angel100% (4)

- Exp ADocument39 pagesExp Aapi-250737955100% (1)

- 3 Exercise Problems CamsDocument36 pages3 Exercise Problems Camsparth raizadaNo ratings yet

- 01 05 Strategic Costing MidtermDocument142 pages01 05 Strategic Costing MidtermAine Arie HNo ratings yet

- Standard Cost and VariancesDocument39 pagesStandard Cost and VariancesChristian AribasNo ratings yet

- CMA II - Chapter 3, Flexible Budgets & StandardsDocument77 pagesCMA II - Chapter 3, Flexible Budgets & StandardsLakachew Getasew0% (1)

- Standard Costs and Operating Performance MeasuresDocument108 pagesStandard Costs and Operating Performance MeasuresCharlaign MalacasNo ratings yet

- Chap 011 Standard CostingDocument109 pagesChap 011 Standard CostingSpheros Indonesia100% (1)

- 4 - Standard CostingDocument72 pages4 - Standard CostingJovelle AlcoberNo ratings yet

- Standard Cost SystemDocument39 pagesStandard Cost SystemTricia Marie TumandaNo ratings yet

- Standard Costing & Variance Analysis!Document37 pagesStandard Costing & Variance Analysis!kunalNo ratings yet

- Group 6 Standard Cost and VariancesDocument15 pagesGroup 6 Standard Cost and VariancesMangoStarr Aibelle VegasNo ratings yet

- Standard CostingDocument101 pagesStandard CostingSana IjazNo ratings yet

- L-31, 32, 33,34 Standard CostingDocument52 pagesL-31, 32, 33,34 Standard CostingYashvi GargNo ratings yet

- Standard CostingDocument36 pagesStandard CostingParamjit Sharma96% (24)

- Standard CostingDocument6 pagesStandard CostingTariq mahmoodNo ratings yet

- Variance Analysis PDFDocument6 pagesVariance Analysis PDFTariq mahmoodNo ratings yet

- ACCT 2200 - Chapter 9Document26 pagesACCT 2200 - Chapter 9afsdasdf3qf4341f4asDNo ratings yet

- Hansen AISE IM - Ch09Document10 pagesHansen AISE IM - Ch09Andriana ButeraNo ratings yet

- Accounting & Control: Cost ManagementDocument35 pagesAccounting & Control: Cost ManagementMeriskaNo ratings yet

- Managerial Accounting: Tool For Business Decision Making Third EditionDocument43 pagesManagerial Accounting: Tool For Business Decision Making Third EditionAnne Dorcas S. DomingoNo ratings yet

- Chapter 9Document39 pagesChapter 9Thảo Thiên ChiNo ratings yet

- Standard Costing Standard Costing: A Managerial Control ToolDocument8 pagesStandard Costing Standard Costing: A Managerial Control ToolTrine De LeonNo ratings yet

- 6e ch09Document35 pages6e ch09KM RobinNo ratings yet

- Variance Analysis AND Standard CostingDocument38 pagesVariance Analysis AND Standard CostingYenLinNo ratings yet

- Synth 1 (STD COSTING)Document11 pagesSynth 1 (STD COSTING)Hassan AdamNo ratings yet

- Sva - Student Copy P1Document101 pagesSva - Student Copy P1Joyce MamokoNo ratings yet

- Topic 11 A181 - Variance AnalysisDocument38 pagesTopic 11 A181 - Variance AnalysisEngku FarahNo ratings yet

- Cost and Management AccountingDocument12 pagesCost and Management Accountingneha chodryNo ratings yet

- Module 2 Sub Mod 2 Standard Costing and Material Variance FinalDocument31 pagesModule 2 Sub Mod 2 Standard Costing and Material Variance Finalmaheshbendigeri5945No ratings yet

- 4th (Managerial Accounting)Document20 pages4th (Managerial Accounting)Amara ELprida SaniNo ratings yet

- Standard Costing & Variance AnalysisDocument43 pagesStandard Costing & Variance Analysis21-51749No ratings yet

- STANDARD COSTING and Variance AnalysisDocument28 pagesSTANDARD COSTING and Variance AnalysisDanica VillaganteNo ratings yet

- Cost Management: Guan Hansen MowenDocument35 pagesCost Management: Guan Hansen MowenevasariNo ratings yet

- Standard Costs and The Balanced ScorecardDocument32 pagesStandard Costs and The Balanced Scorecardshule1100% (1)

- Managerial Accounting 10th Edition Crosson Solutions ManualDocument70 pagesManagerial Accounting 10th Edition Crosson Solutions Manualgregorysosabqsyoptdfw100% (33)

- Standard CostingDocument55 pagesStandard CostingVijeshNo ratings yet

- Chap 4 MNGT Acctng PDFDocument4 pagesChap 4 MNGT Acctng PDFRose Ann YaboraNo ratings yet

- Standard Costing and Variance AnalysisDocument64 pagesStandard Costing and Variance AnalysisPooja Grover ShandilyaNo ratings yet

- Managerial Accounting 10Th Edition Crosson Solutions Manual Full Chapter PDFDocument68 pagesManagerial Accounting 10Th Edition Crosson Solutions Manual Full Chapter PDFykydxnjk4100% (14)

- Standard Cost and Variances Final ReportDocument45 pagesStandard Cost and Variances Final ReportChristian AribasNo ratings yet

- (Mas) 04 - Standard Costing and Variance AnalysisDocument7 pages(Mas) 04 - Standard Costing and Variance AnalysisCykee Hanna Quizo Lumongsod0% (1)

- Standard Costs and Operating Performance MeasuresDocument50 pagesStandard Costs and Operating Performance MeasuresJadeNo ratings yet

- Absorption Vs Variable CostingDocument8 pagesAbsorption Vs Variable CostingMary JaneNo ratings yet

- Standard Cost & Balanced Scorecard: Din Islam (Din)Document40 pagesStandard Cost & Balanced Scorecard: Din Islam (Din)ykamal7No ratings yet

- Standard Cost and Operating Performance Measures FinalDocument20 pagesStandard Cost and Operating Performance Measures FinalNieje Opema GutangNo ratings yet

- SCM Discussion 6Document10 pagesSCM Discussion 6M4ZONSK1E OfficialNo ratings yet

- Standard Costing & Variance AnalysisDocument29 pagesStandard Costing & Variance Analysisadityaraj143143No ratings yet

- Cost Terminology Engineering EconomicDocument22 pagesCost Terminology Engineering EconomicmarifrazzaqNo ratings yet

- Variances of Direct MaterialDocument17 pagesVariances of Direct MaterialChintan TejaniNo ratings yet

- Accounting Group AssigmnetDocument9 pagesAccounting Group AssigmnetABNETNo ratings yet

- Standart Costing PDFDocument3 pagesStandart Costing PDFVIHARI DNo ratings yet

- CH00 Standard Costing and Variance AnalysisDocument75 pagesCH00 Standard Costing and Variance AnalysisDimple AtienzaNo ratings yet

- CVP Analysis IibsDocument32 pagesCVP Analysis IibsSoumendra RoyNo ratings yet

- Standard CostingDocument15 pagesStandard CostingNamrata NeopaneyNo ratings yet

- Standard Costing - MBA513 - DexterSPerez - Dec11.2021Document24 pagesStandard Costing - MBA513 - DexterSPerez - Dec11.2021XanderPerezNo ratings yet

- Cost & Managerial Accounting II EssentialsFrom EverandCost & Managerial Accounting II EssentialsRating: 4 out of 5 stars4/5 (1)

- CPA Review Notes 2019 - BEC (Business Environment Concepts)From EverandCPA Review Notes 2019 - BEC (Business Environment Concepts)Rating: 4 out of 5 stars4/5 (9)

- HBO REPORT Chapter 4Document39 pagesHBO REPORT Chapter 4CaliNo ratings yet

- RM 20-90Document1 pageRM 20-90CaliNo ratings yet

- Tax Remedies Under The NircDocument119 pagesTax Remedies Under The NircCaliNo ratings yet

- Statement of AffairsDocument4 pagesStatement of AffairsCaliNo ratings yet

- Midterm - Seatwork No. 2 (FRANCHISE OPERATIONS)Document2 pagesMidterm - Seatwork No. 2 (FRANCHISE OPERATIONS)CaliNo ratings yet

- Revenue Recognition - Long-Term Construction Contracts (Part 2)Document6 pagesRevenue Recognition - Long-Term Construction Contracts (Part 2)CaliNo ratings yet

- Palma Malthusian Theory of PopulationDocument6 pagesPalma Malthusian Theory of PopulationCaliNo ratings yet

- PNOC vs. CADocument2 pagesPNOC vs. CACaliNo ratings yet

- RR No. 11-2018 SummaryDocument6 pagesRR No. 11-2018 SummaryCaliNo ratings yet

- Cost Accounting Ch03 1Document86 pagesCost Accounting Ch03 1Cali100% (1)

- Weight of Finished Product Weight of Raw Materialscharged : Process Costing: Lost UnitsDocument2 pagesWeight of Finished Product Weight of Raw Materialscharged : Process Costing: Lost UnitsCaliNo ratings yet

- Module 8 Lean AccountingDocument5 pagesModule 8 Lean AccountingCaliNo ratings yet

- CARTOON OF AN IMAGE DocumentationDocument38 pagesCARTOON OF AN IMAGE DocumentationDead poolNo ratings yet

- Chapter 1Document19 pagesChapter 1Kyrie IrvingNo ratings yet

- Monthly ExaminationDocument1 pageMonthly ExaminationshaiyokoNo ratings yet

- SPE/IADC-189432-MS Step Change in Wellbore Positioning AccuracyDocument9 pagesSPE/IADC-189432-MS Step Change in Wellbore Positioning AccuracyKd FaNo ratings yet

- Measurement, Instrumentation and Control ME2400 Assignment 2Document13 pagesMeasurement, Instrumentation and Control ME2400 Assignment 2Chinmay TambatNo ratings yet

- Installation and Operating Manual: 6 - 10 kVA UPSDocument46 pagesInstallation and Operating Manual: 6 - 10 kVA UPSPE TruNo ratings yet

- CC1130 FSK RF Module, 410-510Mhz, 860-960Mhz: Technical SpecificationsDocument2 pagesCC1130 FSK RF Module, 410-510Mhz, 860-960Mhz: Technical SpecificationsHe KantaNo ratings yet

- Shear MappingDocument2 pagesShear MappingTheLuckS; ラッキー矢印No ratings yet

- Lecture Notes On CNCDocument125 pagesLecture Notes On CNCniteen_mulmule48580% (5)

- Liquid Immersions Temperature SensorsDocument6 pagesLiquid Immersions Temperature SensorsmansidevNo ratings yet

- Figure of SpeechDocument9 pagesFigure of SpeechReymar PalamiNo ratings yet

- Quiz 002 - Attempt Review4 PDFDocument3 pagesQuiz 002 - Attempt Review4 PDFkatherine anne ortizNo ratings yet

- RT 7000Document2 pagesRT 7000Majeed AhmedNo ratings yet

- Adaptation of Individual Work Performance Questionnaire (IWPQ) Into Bahasa IndonesiaDocument13 pagesAdaptation of Individual Work Performance Questionnaire (IWPQ) Into Bahasa IndonesiaPutu Nilam SariNo ratings yet

- 5070 w11 QP 12Document12 pages5070 w11 QP 12mstudy123456No ratings yet

- Additional Practice Problems For Inventory ManagementDocument4 pagesAdditional Practice Problems For Inventory ManagementJOANNECHUNo ratings yet

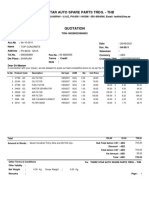

- Three Star Auto Spare Parts Trdg. - THB: 04-10-0011 26/08/2021 Top Concrete PO - BOX: 12515 050305999 06 8823055Document1 pageThree Star Auto Spare Parts Trdg. - THB: 04-10-0011 26/08/2021 Top Concrete PO - BOX: 12515 050305999 06 8823055syed ahmedNo ratings yet

- CMOS Implemented VDTA Based Colpitt OscillatorDocument4 pagesCMOS Implemented VDTA Based Colpitt OscillatorijsretNo ratings yet

- TextileDocument85 pagesTextileGihan Rangana100% (1)

- Glasnik ŠF - 6Document111 pagesGlasnik ŠF - 6ajagodicaNo ratings yet

- 3 Ways To Uninstall Ubuntu Software - WikihowDocument6 pages3 Ways To Uninstall Ubuntu Software - Wikihowjppn33No ratings yet

- Major Kpi ImpDocument7 pagesMajor Kpi ImpImran AslamNo ratings yet

- Modern Compressible Flow With Historical Perspective 3rd Edition Anderson Solutions ManualDocument7 pagesModern Compressible Flow With Historical Perspective 3rd Edition Anderson Solutions Manualserenadinhmzi100% (27)

- 299Document55 pages299Vsrisai ChaitanyaNo ratings yet

- Design and Simulation of InGaAs/GaAsSb Single Quantum Well Structure For Optical Fiber Application: Electronic Band Structure, Carrier Transport, and Optical Gain AnalysisDocument4 pagesDesign and Simulation of InGaAs/GaAsSb Single Quantum Well Structure For Optical Fiber Application: Electronic Band Structure, Carrier Transport, and Optical Gain AnalysisPriyanka KilaniyaNo ratings yet

- CAMCO General Service Manual 0061-1008Document26 pagesCAMCO General Service Manual 0061-1008Mohd Asri TaipNo ratings yet

- Modularization Techniques Interview QuestionDocument7 pagesModularization Techniques Interview QuestionSuresh Logu0% (1)

- Xi Chemistry - Important Topics 2024 - Malik FT - Homelander (Private Group)Document1 pageXi Chemistry - Important Topics 2024 - Malik FT - Homelander (Private Group)salah.malikNo ratings yet