Wurgler Baker Investor Sentiment

Wurgler Baker Investor Sentiment

You might also like

- Investing Cheat SheetDocument1 pageInvesting Cheat SheetAashish BikerYogiNo ratings yet

- Chapter 3 Homework Template 7.6 21Document27 pagesChapter 3 Homework Template 7.6 21Ahmed Mahmoud100% (1)

- Sample 2Document2 pagesSample 2vijay kumarmodi100% (1)

- Applied Linear Regression Models 4th Ed NoteDocument46 pagesApplied Linear Regression Models 4th Ed Noteken_ng333No ratings yet

- Bac 309Document63 pagesBac 309WINFRED KYALONo ratings yet

- Eco-Elasticity of DD & SPDocument20 pagesEco-Elasticity of DD & SPSandhyaAravindakshanNo ratings yet

- Notes On Efficient Market HypothesisDocument4 pagesNotes On Efficient Market HypothesiskokkokkokokkNo ratings yet

- Contributions To Modem EconometricsDocument285 pagesContributions To Modem Econometricsاحمد صابرNo ratings yet

- Fama French (2015) - International Tests of A Five-Factor Asset Pricing ModelDocument23 pagesFama French (2015) - International Tests of A Five-Factor Asset Pricing ModelBayu D. PutraNo ratings yet

- CAPMDocument34 pagesCAPMadityav_13100% (1)

- Journal On The Importance of InvestmentDocument25 pagesJournal On The Importance of InvestmentJRNo ratings yet

- Quantitative Analysis and ModellingDocument3 pagesQuantitative Analysis and Modellinglartey_615472767No ratings yet

- Two Stage Fama MacbethDocument5 pagesTwo Stage Fama Macbethkty21joy100% (1)

- Shiller BubblesDocument17 pagesShiller BubblesLolo Set100% (1)

- Fama 1981Document22 pagesFama 1981Marcelo BalzanaNo ratings yet

- MKT Risk Premium PaperDocument114 pagesMKT Risk Premium PaperLee BollingerNo ratings yet

- 1993-00 A Closed-Form Solution For Options With Stochastic Volatility With Applications To Bond and Currency Options - HestonDocument17 pages1993-00 A Closed-Form Solution For Options With Stochastic Volatility With Applications To Bond and Currency Options - Hestonrdouglas2002No ratings yet

- Cost and Management Accounting - Course OutlineDocument9 pagesCost and Management Accounting - Course OutlineJajJay100% (1)

- Dynamic Risk ParityDocument18 pagesDynamic Risk ParityRohit ChandraNo ratings yet

- Shortfall SurpriseDocument21 pagesShortfall SurpriseJunqiang Xie100% (1)

- Basic Econometrics Revision - Econometric ModellingDocument65 pagesBasic Econometrics Revision - Econometric ModellingTrevor ChimombeNo ratings yet

- Macroeconomic Analysis 2003: Monetary Policy: Transmission MechanismDocument26 pagesMacroeconomic Analysis 2003: Monetary Policy: Transmission MechanismYasir IrfanNo ratings yet

- Forecasting Volatility of Stock Indices With ARCH ModelDocument18 pagesForecasting Volatility of Stock Indices With ARCH Modelravi_nyseNo ratings yet

- Does Trade Cause Growth?: A. F D RDocument21 pagesDoes Trade Cause Growth?: A. F D Rjana_duhaNo ratings yet

- Sta404 Chapter 08Document120 pagesSta404 Chapter 08Ibnu IyarNo ratings yet

- Chapter 4 - PRODUCT PRICINGDocument61 pagesChapter 4 - PRODUCT PRICINGMatt Russell Yuson100% (1)

- Advanced Econometrics - HEC LausanneDocument2 pagesAdvanced Econometrics - HEC LausanneRavi SharmaNo ratings yet

- Bowerman CH15 APPT FinalDocument38 pagesBowerman CH15 APPT FinalMuktesh Singh100% (1)

- Lahore University of Management Sciences ECON 330 - EconometricsDocument3 pagesLahore University of Management Sciences ECON 330 - EconometricsshyasirNo ratings yet

- BondsDocument55 pagesBondsfecaxeyivuNo ratings yet

- Foundations of Quantitative MethodsDocument160 pagesFoundations of Quantitative MethodsHIMANSHU PATHAKNo ratings yet

- Unit 1 ORDocument42 pagesUnit 1 ORRatandeep SinghNo ratings yet

- Market Efficiency Market Anomalies Causes Evidences and Some Behavioral Aspects of Market AnomaliesDocument14 pagesMarket Efficiency Market Anomalies Causes Evidences and Some Behavioral Aspects of Market AnomaliesSounay PhothisaneNo ratings yet

- Beta Leverage and The Cost of CapitalDocument3 pagesBeta Leverage and The Cost of CapitalpumaguaNo ratings yet

- 08 Valuation of Stocks and BondsDocument43 pages08 Valuation of Stocks and BondsRaviPratapGond100% (1)

- 12 - Chapter 5 PDFDocument49 pages12 - Chapter 5 PDFShipra Chaudhary100% (1)

- Queuing Analysis: Chapter OutlineDocument22 pagesQueuing Analysis: Chapter OutlineMike SerquinaNo ratings yet

- Presentation 2: Options Futures and Other Derivatives Hull Pretince HallDocument13 pagesPresentation 2: Options Futures and Other Derivatives Hull Pretince HallYolibi KhunNo ratings yet

- PPT5-Mathematics of FinanceDocument22 pagesPPT5-Mathematics of FinanceRano Acun100% (2)

- Paper On Mcap To GDPDocument20 pagesPaper On Mcap To GDPgreyistariNo ratings yet

- ECO551 C6 Central Bank and The Conduct of The Monetary Policy Edit 2Document35 pagesECO551 C6 Central Bank and The Conduct of The Monetary Policy Edit 2aisyahNo ratings yet

- An Instructive Example: Decision Theory General Equilibrium Theory Mechanism Design TheoryDocument25 pagesAn Instructive Example: Decision Theory General Equilibrium Theory Mechanism Design TheoryRadha RampalliNo ratings yet

- IPO UnderpricingDocument9 pagesIPO UnderpricingHendra Gun DulNo ratings yet

- Pairs Trading (Copulas)Document20 pagesPairs Trading (Copulas)alexa_sherpyNo ratings yet

- General Linear Model: Statistical MethodsDocument9 pagesGeneral Linear Model: Statistical MethodsErmita YusidaNo ratings yet

- Poisson Inverse GammaDocument18 pagesPoisson Inverse GammaAnonymous Y2ibaULes1No ratings yet

- Finance and Location Strategies For RetailingDocument20 pagesFinance and Location Strategies For RetailingParameshwara AcharyaNo ratings yet

- The Markowitz Mean Variance Optimization Model Finance EssayDocument34 pagesThe Markowitz Mean Variance Optimization Model Finance EssayHND Assignment Help100% (1)

- SSRN Id593584Document28 pagesSSRN Id593584Loulou DePanamNo ratings yet

- Title: "Correlation Between Different Stock Markets" Alisha Singh Ashish Jain 1. AbstractDocument14 pagesTitle: "Correlation Between Different Stock Markets" Alisha Singh Ashish Jain 1. Abstractsinghalisha1989No ratings yet

- Clean Sweep Informed Trading Through Intermarket Sweep Orders by Chakravarty Et Al 2011 JFQADocument39 pagesClean Sweep Informed Trading Through Intermarket Sweep Orders by Chakravarty Et Al 2011 JFQAEleanor RigbyNo ratings yet

- Some Applications of Mathematics in Finance (7 November 2008)Document52 pagesSome Applications of Mathematics in Finance (7 November 2008)Join RiotNo ratings yet

- Chapter 7, Part 1Document19 pagesChapter 7, Part 1Oona NiallNo ratings yet

- Lecture 1 ECN 2331 (Scope of Statistical Methods For Economic Analysis) - 1Document15 pagesLecture 1 ECN 2331 (Scope of Statistical Methods For Economic Analysis) - 1sekelanilunguNo ratings yet

- Introduction To Multiple Linear RegressionDocument49 pagesIntroduction To Multiple Linear RegressionRennate MariaNo ratings yet

- Chapter 3 Economic and Econometric ModelsDocument41 pagesChapter 3 Economic and Econometric ModelsGojart KamberiNo ratings yet

- Introduction To Quantitative AnalysisDocument6 pagesIntroduction To Quantitative AnalysisBattle ALONE009No ratings yet

- Black Scholes Model ReportDocument6 pagesBlack Scholes Model ReportminhalNo ratings yet

- Servay Papar - Nur SyahirahDocument1 pageServay Papar - Nur Syahirahbaby potatoNo ratings yet

- ch01R StudentDocument70 pagesch01R StudentChuan ShihNo ratings yet

- I) Riba Is A Cause of Injustice and ExploitationDocument1 pageI) Riba Is A Cause of Injustice and ExploitationWai SeenNo ratings yet

- A STUDY ON Financial Statement Analysis of Axis BankDocument94 pagesA STUDY ON Financial Statement Analysis of Axis BankKeleti Santhosh75% (8)

- Module 4 Corporate Ratio CalculationsDocument3 pagesModule 4 Corporate Ratio Calculationssherif_awadNo ratings yet

- Purchase Requisition (PR) Document in SAP MM. Purchase Requisition (PR) Is An Internal Purchasing Document in SAPDocument5 pagesPurchase Requisition (PR) Document in SAP MM. Purchase Requisition (PR) Is An Internal Purchasing Document in SAPashwiniNo ratings yet

- Importance of Partnership AgreementDocument3 pagesImportance of Partnership AgreementHarshraj AhirwarNo ratings yet

- Session 4 (Global Marketing)Document30 pagesSession 4 (Global Marketing)Hassan ShafiqNo ratings yet

- The Budget Explained in 5 MinutesDocument5 pagesThe Budget Explained in 5 MinutesTulsi OjhaNo ratings yet

- Mentorship Report On Digitization in BankingDocument46 pagesMentorship Report On Digitization in BankingravneetNo ratings yet

- Financing Decision: Compiled By: RabachDocument14 pagesFinancing Decision: Compiled By: RabachRafael M. BachanichaNo ratings yet

- Individual Submission Week 11Document5 pagesIndividual Submission Week 11Sachin VSNo ratings yet

- Personal Banking JamaicaDocument28 pagesPersonal Banking JamaicaDuane WilliamsNo ratings yet

- Environment: The Functions of EnvironmentDocument2 pagesEnvironment: The Functions of EnvironmentZyaban Dorayakiez CuphuwNo ratings yet

- Report On Food Tourism Part-1Document26 pagesReport On Food Tourism Part-1lionsreeNo ratings yet

- Fin Statement Analysis - Atlas BatteryDocument34 pagesFin Statement Analysis - Atlas BatterytabinahassanNo ratings yet

- E - Commerce Chapter 11Document19 pagesE - Commerce Chapter 11Md. RuHul A.No ratings yet

- Strategic Management Essentials: Chapter OneDocument41 pagesStrategic Management Essentials: Chapter OnevrendyNo ratings yet

- Beauty and The E-Commerce Beast PDFDocument14 pagesBeauty and The E-Commerce Beast PDFFranck MauryNo ratings yet

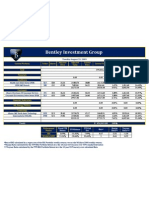

- Bentley Investment Group: Tuesday August 25, 2009Document1 pageBentley Investment Group: Tuesday August 25, 2009bentleyinvestmentgroupNo ratings yet

- Presented By: Room To ReadDocument20 pagesPresented By: Room To ReadDevendra Bundel100% (1)

- File BRPD Circular No 05Document3 pagesFile BRPD Circular No 05Arifur RahmanNo ratings yet

- Week 3 Statement of Financial PositionDocument22 pagesWeek 3 Statement of Financial PositionKushal KhatiwadaNo ratings yet

- Grant Thornton's Certification in Financial Modeling and Valuation For Working ProfessionalsDocument3 pagesGrant Thornton's Certification in Financial Modeling and Valuation For Working ProfessionalsMinaketan DasNo ratings yet

- EU Food and Drink IndustryDocument9 pagesEU Food and Drink IndustryMuhammad HarisNo ratings yet

- Tugas 2Document14 pagesTugas 2Tri Sunanda FathanahNo ratings yet

- ET Phones Home - Fundoo ProfessorDocument1 pageET Phones Home - Fundoo ProfessorSubham JainNo ratings yet

- Urbanization and Economic Growth: The Arguments and Evidence For Africa and AsiaDocument19 pagesUrbanization and Economic Growth: The Arguments and Evidence For Africa and AsiamaizansofiaNo ratings yet

- Strategic Cost AccountingDocument6 pagesStrategic Cost AccountingPauline OsorioNo ratings yet

Download as pdf or txt

You might also like

- Investing Cheat SheetDocument1 pageInvesting Cheat SheetAashish BikerYogiNo ratings yet

- Chapter 3 Homework Template 7.6 21Document27 pagesChapter 3 Homework Template 7.6 21Ahmed Mahmoud100% (1)

- Sample 2Document2 pagesSample 2vijay kumarmodi100% (1)

- Applied Linear Regression Models 4th Ed NoteDocument46 pagesApplied Linear Regression Models 4th Ed Noteken_ng333No ratings yet

- Bac 309Document63 pagesBac 309WINFRED KYALONo ratings yet

- Eco-Elasticity of DD & SPDocument20 pagesEco-Elasticity of DD & SPSandhyaAravindakshanNo ratings yet

- Notes On Efficient Market HypothesisDocument4 pagesNotes On Efficient Market HypothesiskokkokkokokkNo ratings yet

- Contributions To Modem EconometricsDocument285 pagesContributions To Modem Econometricsاحمد صابرNo ratings yet

- Fama French (2015) - International Tests of A Five-Factor Asset Pricing ModelDocument23 pagesFama French (2015) - International Tests of A Five-Factor Asset Pricing ModelBayu D. PutraNo ratings yet

- CAPMDocument34 pagesCAPMadityav_13100% (1)

- Journal On The Importance of InvestmentDocument25 pagesJournal On The Importance of InvestmentJRNo ratings yet

- Quantitative Analysis and ModellingDocument3 pagesQuantitative Analysis and Modellinglartey_615472767No ratings yet

- Two Stage Fama MacbethDocument5 pagesTwo Stage Fama Macbethkty21joy100% (1)

- Shiller BubblesDocument17 pagesShiller BubblesLolo Set100% (1)

- Fama 1981Document22 pagesFama 1981Marcelo BalzanaNo ratings yet

- MKT Risk Premium PaperDocument114 pagesMKT Risk Premium PaperLee BollingerNo ratings yet

- 1993-00 A Closed-Form Solution For Options With Stochastic Volatility With Applications To Bond and Currency Options - HestonDocument17 pages1993-00 A Closed-Form Solution For Options With Stochastic Volatility With Applications To Bond and Currency Options - Hestonrdouglas2002No ratings yet

- Cost and Management Accounting - Course OutlineDocument9 pagesCost and Management Accounting - Course OutlineJajJay100% (1)

- Dynamic Risk ParityDocument18 pagesDynamic Risk ParityRohit ChandraNo ratings yet

- Shortfall SurpriseDocument21 pagesShortfall SurpriseJunqiang Xie100% (1)

- Basic Econometrics Revision - Econometric ModellingDocument65 pagesBasic Econometrics Revision - Econometric ModellingTrevor ChimombeNo ratings yet

- Macroeconomic Analysis 2003: Monetary Policy: Transmission MechanismDocument26 pagesMacroeconomic Analysis 2003: Monetary Policy: Transmission MechanismYasir IrfanNo ratings yet

- Forecasting Volatility of Stock Indices With ARCH ModelDocument18 pagesForecasting Volatility of Stock Indices With ARCH Modelravi_nyseNo ratings yet

- Does Trade Cause Growth?: A. F D RDocument21 pagesDoes Trade Cause Growth?: A. F D Rjana_duhaNo ratings yet

- Sta404 Chapter 08Document120 pagesSta404 Chapter 08Ibnu IyarNo ratings yet

- Chapter 4 - PRODUCT PRICINGDocument61 pagesChapter 4 - PRODUCT PRICINGMatt Russell Yuson100% (1)

- Advanced Econometrics - HEC LausanneDocument2 pagesAdvanced Econometrics - HEC LausanneRavi SharmaNo ratings yet

- Bowerman CH15 APPT FinalDocument38 pagesBowerman CH15 APPT FinalMuktesh Singh100% (1)

- Lahore University of Management Sciences ECON 330 - EconometricsDocument3 pagesLahore University of Management Sciences ECON 330 - EconometricsshyasirNo ratings yet

- BondsDocument55 pagesBondsfecaxeyivuNo ratings yet

- Foundations of Quantitative MethodsDocument160 pagesFoundations of Quantitative MethodsHIMANSHU PATHAKNo ratings yet

- Unit 1 ORDocument42 pagesUnit 1 ORRatandeep SinghNo ratings yet

- Market Efficiency Market Anomalies Causes Evidences and Some Behavioral Aspects of Market AnomaliesDocument14 pagesMarket Efficiency Market Anomalies Causes Evidences and Some Behavioral Aspects of Market AnomaliesSounay PhothisaneNo ratings yet

- Beta Leverage and The Cost of CapitalDocument3 pagesBeta Leverage and The Cost of CapitalpumaguaNo ratings yet

- 08 Valuation of Stocks and BondsDocument43 pages08 Valuation of Stocks and BondsRaviPratapGond100% (1)

- 12 - Chapter 5 PDFDocument49 pages12 - Chapter 5 PDFShipra Chaudhary100% (1)

- Queuing Analysis: Chapter OutlineDocument22 pagesQueuing Analysis: Chapter OutlineMike SerquinaNo ratings yet

- Presentation 2: Options Futures and Other Derivatives Hull Pretince HallDocument13 pagesPresentation 2: Options Futures and Other Derivatives Hull Pretince HallYolibi KhunNo ratings yet

- PPT5-Mathematics of FinanceDocument22 pagesPPT5-Mathematics of FinanceRano Acun100% (2)

- Paper On Mcap To GDPDocument20 pagesPaper On Mcap To GDPgreyistariNo ratings yet

- ECO551 C6 Central Bank and The Conduct of The Monetary Policy Edit 2Document35 pagesECO551 C6 Central Bank and The Conduct of The Monetary Policy Edit 2aisyahNo ratings yet

- An Instructive Example: Decision Theory General Equilibrium Theory Mechanism Design TheoryDocument25 pagesAn Instructive Example: Decision Theory General Equilibrium Theory Mechanism Design TheoryRadha RampalliNo ratings yet

- IPO UnderpricingDocument9 pagesIPO UnderpricingHendra Gun DulNo ratings yet

- Pairs Trading (Copulas)Document20 pagesPairs Trading (Copulas)alexa_sherpyNo ratings yet

- General Linear Model: Statistical MethodsDocument9 pagesGeneral Linear Model: Statistical MethodsErmita YusidaNo ratings yet

- Poisson Inverse GammaDocument18 pagesPoisson Inverse GammaAnonymous Y2ibaULes1No ratings yet

- Finance and Location Strategies For RetailingDocument20 pagesFinance and Location Strategies For RetailingParameshwara AcharyaNo ratings yet

- The Markowitz Mean Variance Optimization Model Finance EssayDocument34 pagesThe Markowitz Mean Variance Optimization Model Finance EssayHND Assignment Help100% (1)

- SSRN Id593584Document28 pagesSSRN Id593584Loulou DePanamNo ratings yet

- Title: "Correlation Between Different Stock Markets" Alisha Singh Ashish Jain 1. AbstractDocument14 pagesTitle: "Correlation Between Different Stock Markets" Alisha Singh Ashish Jain 1. Abstractsinghalisha1989No ratings yet

- Clean Sweep Informed Trading Through Intermarket Sweep Orders by Chakravarty Et Al 2011 JFQADocument39 pagesClean Sweep Informed Trading Through Intermarket Sweep Orders by Chakravarty Et Al 2011 JFQAEleanor RigbyNo ratings yet

- Some Applications of Mathematics in Finance (7 November 2008)Document52 pagesSome Applications of Mathematics in Finance (7 November 2008)Join RiotNo ratings yet

- Chapter 7, Part 1Document19 pagesChapter 7, Part 1Oona NiallNo ratings yet

- Lecture 1 ECN 2331 (Scope of Statistical Methods For Economic Analysis) - 1Document15 pagesLecture 1 ECN 2331 (Scope of Statistical Methods For Economic Analysis) - 1sekelanilunguNo ratings yet

- Introduction To Multiple Linear RegressionDocument49 pagesIntroduction To Multiple Linear RegressionRennate MariaNo ratings yet

- Chapter 3 Economic and Econometric ModelsDocument41 pagesChapter 3 Economic and Econometric ModelsGojart KamberiNo ratings yet

- Introduction To Quantitative AnalysisDocument6 pagesIntroduction To Quantitative AnalysisBattle ALONE009No ratings yet

- Black Scholes Model ReportDocument6 pagesBlack Scholes Model ReportminhalNo ratings yet

- Servay Papar - Nur SyahirahDocument1 pageServay Papar - Nur Syahirahbaby potatoNo ratings yet

- ch01R StudentDocument70 pagesch01R StudentChuan ShihNo ratings yet

- I) Riba Is A Cause of Injustice and ExploitationDocument1 pageI) Riba Is A Cause of Injustice and ExploitationWai SeenNo ratings yet

- A STUDY ON Financial Statement Analysis of Axis BankDocument94 pagesA STUDY ON Financial Statement Analysis of Axis BankKeleti Santhosh75% (8)

- Module 4 Corporate Ratio CalculationsDocument3 pagesModule 4 Corporate Ratio Calculationssherif_awadNo ratings yet

- Purchase Requisition (PR) Document in SAP MM. Purchase Requisition (PR) Is An Internal Purchasing Document in SAPDocument5 pagesPurchase Requisition (PR) Document in SAP MM. Purchase Requisition (PR) Is An Internal Purchasing Document in SAPashwiniNo ratings yet

- Importance of Partnership AgreementDocument3 pagesImportance of Partnership AgreementHarshraj AhirwarNo ratings yet

- Session 4 (Global Marketing)Document30 pagesSession 4 (Global Marketing)Hassan ShafiqNo ratings yet

- The Budget Explained in 5 MinutesDocument5 pagesThe Budget Explained in 5 MinutesTulsi OjhaNo ratings yet

- Mentorship Report On Digitization in BankingDocument46 pagesMentorship Report On Digitization in BankingravneetNo ratings yet

- Financing Decision: Compiled By: RabachDocument14 pagesFinancing Decision: Compiled By: RabachRafael M. BachanichaNo ratings yet

- Individual Submission Week 11Document5 pagesIndividual Submission Week 11Sachin VSNo ratings yet

- Personal Banking JamaicaDocument28 pagesPersonal Banking JamaicaDuane WilliamsNo ratings yet

- Environment: The Functions of EnvironmentDocument2 pagesEnvironment: The Functions of EnvironmentZyaban Dorayakiez CuphuwNo ratings yet

- Report On Food Tourism Part-1Document26 pagesReport On Food Tourism Part-1lionsreeNo ratings yet

- Fin Statement Analysis - Atlas BatteryDocument34 pagesFin Statement Analysis - Atlas BatterytabinahassanNo ratings yet

- E - Commerce Chapter 11Document19 pagesE - Commerce Chapter 11Md. RuHul A.No ratings yet

- Strategic Management Essentials: Chapter OneDocument41 pagesStrategic Management Essentials: Chapter OnevrendyNo ratings yet

- Beauty and The E-Commerce Beast PDFDocument14 pagesBeauty and The E-Commerce Beast PDFFranck MauryNo ratings yet

- Bentley Investment Group: Tuesday August 25, 2009Document1 pageBentley Investment Group: Tuesday August 25, 2009bentleyinvestmentgroupNo ratings yet

- Presented By: Room To ReadDocument20 pagesPresented By: Room To ReadDevendra Bundel100% (1)

- File BRPD Circular No 05Document3 pagesFile BRPD Circular No 05Arifur RahmanNo ratings yet

- Week 3 Statement of Financial PositionDocument22 pagesWeek 3 Statement of Financial PositionKushal KhatiwadaNo ratings yet

- Grant Thornton's Certification in Financial Modeling and Valuation For Working ProfessionalsDocument3 pagesGrant Thornton's Certification in Financial Modeling and Valuation For Working ProfessionalsMinaketan DasNo ratings yet

- EU Food and Drink IndustryDocument9 pagesEU Food and Drink IndustryMuhammad HarisNo ratings yet

- Tugas 2Document14 pagesTugas 2Tri Sunanda FathanahNo ratings yet

- ET Phones Home - Fundoo ProfessorDocument1 pageET Phones Home - Fundoo ProfessorSubham JainNo ratings yet

- Urbanization and Economic Growth: The Arguments and Evidence For Africa and AsiaDocument19 pagesUrbanization and Economic Growth: The Arguments and Evidence For Africa and AsiamaizansofiaNo ratings yet

- Strategic Cost AccountingDocument6 pagesStrategic Cost AccountingPauline OsorioNo ratings yet