Download as pdf or txt

You might also like

- 50 Perguntas e Respostas para Entrevista de Emprego em InglêsDocument14 pages50 Perguntas e Respostas para Entrevista de Emprego em InglêsMariaReginaCuryScaff100% (1)

- Productivity and Reliability-Based Maintenance Management, Second EditionFrom EverandProductivity and Reliability-Based Maintenance Management, Second EditionNo ratings yet

- Sr. No Name Roll No Programme: Case Analysis Section 2 Toffee Inc. Course: Operations Management (Tod 221)Document6 pagesSr. No Name Roll No Programme: Case Analysis Section 2 Toffee Inc. Course: Operations Management (Tod 221)Harshvardhan Jadwani0% (1)

- MBA 670 Exam 1Document14 pagesMBA 670 Exam 1Lauren LoshNo ratings yet

- List of Companies: No. NameDocument7 pagesList of Companies: No. Namett100% (1)

- Jaipur National University, Jaipur: School of Distance Education & Learning Internal Assignment No. 1Document2 pagesJaipur National University, Jaipur: School of Distance Education & Learning Internal Assignment No. 1naren17% (6)

- Lecture - Little's LawDocument36 pagesLecture - Little's LawSamuel Bruce Rockson100% (1)

- QuestionsDocument10 pagesQuestionsYat Kunt ChanNo ratings yet

- Activity-Based Cost Management For Design and Development StageDocument15 pagesActivity-Based Cost Management For Design and Development Stagebimbi purbaNo ratings yet

- CFi Capital Structure Leverage ProblemsDocument6 pagesCFi Capital Structure Leverage ProblemsJustin Russo HarryNo ratings yet

- Quiz Acctng 603Document10 pagesQuiz Acctng 603LJ AggabaoNo ratings yet

- ThroughputDocument15 pagesThroughputVaibhav KocharNo ratings yet

- Product Life Cycle Costing / Whole Life Cycle Costing /life Cycle CostingDocument23 pagesProduct Life Cycle Costing / Whole Life Cycle Costing /life Cycle CostingTapiwa Tbone MadamombeNo ratings yet

- Throughput Accounting and The Theory of ConstraintsDocument8 pagesThroughput Accounting and The Theory of ConstraintsMd AzimNo ratings yet

- Feasibility Study TemplateDocument6 pagesFeasibility Study TemplateMUTHUVEL MNo ratings yet

- Corporate Finance Course OutlineDocument6 pagesCorporate Finance Course OutlineHaroon Z. ChoudhryNo ratings yet

- Assignment 3Document7 pagesAssignment 3Abdullah ghauriNo ratings yet

- Throughput Accounting: Prepared by Gwizu KDocument26 pagesThroughput Accounting: Prepared by Gwizu KTapiwa Tbone Madamombe100% (1)

- Mba First Assignment Questions02062021122015Document2 pagesMba First Assignment Questions02062021122015shahana7100% (2)

- Capital Budgeting Techniques Capital Budgeting TechniquesDocument58 pagesCapital Budgeting Techniques Capital Budgeting TechniquesMuhammad ZeeshanNo ratings yet

- Target CostingDocument9 pagesTarget CostingRahul PandeyNo ratings yet

- CH 13Document28 pagesCH 13ReneeNo ratings yet

- Target - Costing F5 NotesDocument4 pagesTarget - Costing F5 NotesSiddiqua KashifNo ratings yet

- Cost Volume ProfitDocument73 pagesCost Volume ProfitAsiiyah100% (1)

- Target CostDocument5 pagesTarget CostWarda RizviNo ratings yet

- Life Cycle Costing and Environmental AccountingDocument32 pagesLife Cycle Costing and Environmental AccountingImran UmarNo ratings yet

- JitDocument26 pagesJitRachanakumari100% (1)

- Just-in-Time and Lean OperationsDocument90 pagesJust-in-Time and Lean OperationsSaad PirzadaNo ratings yet

- Seminar 15 - Life Cycle Costing (Questions)Document3 pagesSeminar 15 - Life Cycle Costing (Questions)Asfa ahmedNo ratings yet

- Module IV - Working Capital ManagementDocument50 pagesModule IV - Working Capital ManagementAshwin DholeNo ratings yet

- Target Costing PresentationDocument14 pagesTarget Costing PresentationAks SinhaNo ratings yet

- Kaizen CostingDocument20 pagesKaizen Costingjigyasamiddha0% (1)

- Talk 07. Scheduling - MRP & ERPDocument21 pagesTalk 07. Scheduling - MRP & ERPPhuc Linh100% (1)

- CH 3 JITDocument68 pagesCH 3 JITmaheshgNo ratings yet

- Chapter 10 SolutionsDocument68 pagesChapter 10 SolutionsMasha LankNo ratings yet

- Variable Production Overhead Variance (VPOH)Document9 pagesVariable Production Overhead Variance (VPOH)Wee Han ChiangNo ratings yet

- The Learning CurveDocument17 pagesThe Learning CurvemohitkripalaniNo ratings yet

- STANDARD COSTING and Variance AnalysisDocument28 pagesSTANDARD COSTING and Variance AnalysisDanica VillaganteNo ratings yet

- Tools and Techniques of Cost ReductionDocument27 pagesTools and Techniques of Cost Reductionপ্রিয়াঙ্কুর ধর100% (2)

- Capacity Planning, Facility Location & LayoutDocument56 pagesCapacity Planning, Facility Location & LayoutFekadu100% (1)

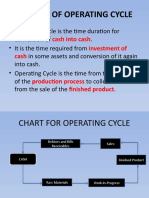

- Concept of Operating Cycle: Cash Into Cash Investment of CashDocument6 pagesConcept of Operating Cycle: Cash Into Cash Investment of CashVenket RamanaNo ratings yet

- Assignment 5 - CH 10 - The Cost of Capital PDFDocument6 pagesAssignment 5 - CH 10 - The Cost of Capital PDFAhmedFawzy0% (1)

- Managerial Accounting Chap 8 Standard Costing and Variance AnalysisDocument85 pagesManagerial Accounting Chap 8 Standard Costing and Variance AnalysisFlores Jevie VargasNo ratings yet

- Just in Time and BackflushingDocument25 pagesJust in Time and BackflushingSilvani Margaretha SimangunsongNo ratings yet

- Cost ManagementDocument18 pagesCost ManagementGeo Rublico ManilaNo ratings yet

- MS 3404 Standard Costing and Variance AnalysisDocument6 pagesMS 3404 Standard Costing and Variance AnalysisMonica GarciaNo ratings yet

- TOCDocument17 pagesTOCpvamanNo ratings yet

- Cost II-ch 1 - CVPDocument45 pagesCost II-ch 1 - CVPYitera SisayNo ratings yet

- Lean in Service Industry by MG. Kanakana (Corresponding Author)Document10 pagesLean in Service Industry by MG. Kanakana (Corresponding Author)Kun HarjiyantoNo ratings yet

- Target Costing Presentation FinalDocument57 pagesTarget Costing Presentation FinalMr Dampha100% (1)

- Throughput AccountingDocument5 pagesThroughput AccountingMohammad Faizan Farooq Qadri AttariNo ratings yet

- ABC Hansen & Mowen ch4 P ('t':'3', 'I':'669594619') D '' Var B Location Settimeout (Function ( If (Typeof Window - Iframe 'Undefined') ( B.href B.href ) ), 15000)Document22 pagesABC Hansen & Mowen ch4 P ('t':'3', 'I':'669594619') D '' Var B Location Settimeout (Function ( If (Typeof Window - Iframe 'Undefined') ( B.href B.href ) ), 15000)Aziza AmranNo ratings yet

- Life Cycle CostingDocument38 pagesLife Cycle CostingD A N Ī S HNo ratings yet

- 3.sales Variance AnalysisDocument38 pages3.sales Variance Analysiskamasuke hegdeNo ratings yet

- Assignment 2: Problem 1Document3 pagesAssignment 2: Problem 1musicslave960% (1)

- Chapter 9 - Inventory Costing and Capacity AnalysisDocument40 pagesChapter 9 - Inventory Costing and Capacity AnalysisBrian SantsNo ratings yet

- CH 8Document16 pagesCH 8emanmamdouh596No ratings yet

- Operations CH 4 - Lean & JITDocument22 pagesOperations CH 4 - Lean & JITMellanie SerranoNo ratings yet

- Liquidity Ratios AssignmentDocument6 pagesLiquidity Ratios AssignmentNoor Hidayah Binti Taslim0% (1)

- Throughput AccountingDocument15 pagesThroughput AccountingNida KarimNo ratings yet

- Lecture 2 BEP Numericals AnswersDocument16 pagesLecture 2 BEP Numericals AnswersSanyam GoelNo ratings yet

- Meyer Appliance Company Makes Cooling Fans The Firms Income Statement Is As Follows ComputeDocument2 pagesMeyer Appliance Company Makes Cooling Fans The Firms Income Statement Is As Follows ComputeDoreenNo ratings yet

- Assignment 5 - Capacity PlanningDocument1 pageAssignment 5 - Capacity Planningamr onsyNo ratings yet

- Part Seven: THE Management of Financial InstitutionsDocument40 pagesPart Seven: THE Management of Financial InstitutionsIrakli SaliaNo ratings yet

- Target Costing Introduction: Today's Topics: HomeworkDocument3 pagesTarget Costing Introduction: Today's Topics: HomeworkpalaviyaNo ratings yet

- Sales Ledger Master Files: Lecture Topic: During The Lecture, Take Notes Here. Insert A Sub-Page For Each Lecture TopicDocument1 pageSales Ledger Master Files: Lecture Topic: During The Lecture, Take Notes Here. Insert A Sub-Page For Each Lecture TopicpalaviyaNo ratings yet

- Marginal CostingDocument2 pagesMarginal CostingpalaviyaNo ratings yet

- Life Cycle CostingDocument4 pagesLife Cycle CostingpalaviyaNo ratings yet

- Inventory Master File: Lecture Topic: During The Lecture, Take Notes Here. Insert A Sub-Page For Each Lecture TopicDocument3 pagesInventory Master File: Lecture Topic: During The Lecture, Take Notes Here. Insert A Sub-Page For Each Lecture TopicpalaviyaNo ratings yet

- Debtors Master File: Lecture Topic: During The Lecture, Take Notes Here. Insert A Sub-Page For Each Lecture TopicDocument2 pagesDebtors Master File: Lecture Topic: During The Lecture, Take Notes Here. Insert A Sub-Page For Each Lecture TopicpalaviyaNo ratings yet

- TOWS Matrix PDFDocument3 pagesTOWS Matrix PDFpalaviyaNo ratings yet

- Assets Under ConstructionDocument1 pageAssets Under ConstructionpalaviyaNo ratings yet

- Project KenyaDocument25 pagesProject KenyaMohamed TawfikNo ratings yet

- Revocation of Offer and AcceptanceDocument5 pagesRevocation of Offer and AcceptanceSuraya Mazlan80% (5)

- Financial Aspect Feasibility StudyDocument66 pagesFinancial Aspect Feasibility StudyRialeeNo ratings yet

- ListDocument4 pagesListNgeleka kalalaNo ratings yet

- Check - Chapter 10 - She Part 1Document4 pagesCheck - Chapter 10 - She Part 1ARNEL CALUBAGNo ratings yet

- Persuasive Messages - Radical RewriteDocument3 pagesPersuasive Messages - Radical RewriteFarrahNo ratings yet

- Quiz 2Document4 pagesQuiz 2Mark AdaponNo ratings yet

- Multinational Capital Budgeting: Chapter ObjectivesDocument29 pagesMultinational Capital Budgeting: Chapter ObjectivesBhen ChodNo ratings yet

- Globalization: 2. LiberalismDocument5 pagesGlobalization: 2. LiberalismMaryden BurgosNo ratings yet

- The Growth and Structural Change of Chinese Cities LIN 2002Document18 pagesThe Growth and Structural Change of Chinese Cities LIN 2002raulNo ratings yet

- members: Hoàng Thị Mai Xuân Dương Nguyễn Minh Thư Ðỗ Thị Phương Anh Trần Thị Thảo NguyênDocument10 pagesmembers: Hoàng Thị Mai Xuân Dương Nguyễn Minh Thư Ðỗ Thị Phương Anh Trần Thị Thảo NguyênĐỗ Phương AnhNo ratings yet

- Advert For EGP Support OfficersDocument5 pagesAdvert For EGP Support OfficersCharlesNo ratings yet

- Practice Exams - Vol 2 (2020)Document68 pagesPractice Exams - Vol 2 (2020)Ledger Point100% (1)

- Research Paper OutlineDocument2 pagesResearch Paper OutlineKirukaze ItunuzukiNo ratings yet

- Risk Analysis of Infrastructure Projects PDFDocument27 pagesRisk Analysis of Infrastructure Projects PDFMayank K JainNo ratings yet

- Reflection in EntrepDocument1 pageReflection in EntrepJealyn BallaranNo ratings yet

- Market Structures: Imperfect Or: Monopolistic CompetitionDocument29 pagesMarket Structures: Imperfect Or: Monopolistic CompetitionHendrix NailNo ratings yet

- Fashion Forward and Dream DesignsDocument5 pagesFashion Forward and Dream DesignsNana Kweku Asifo OkyereNo ratings yet

- Abra Mining - Iacgr 2020Document65 pagesAbra Mining - Iacgr 2020Nichole John UsonNo ratings yet

- Gicici Bank: Discounting-WorkingDocument8 pagesGicici Bank: Discounting-WorkingManav SinghNo ratings yet

- Dos SANTOS - THE STRUCTURE OF DEPENDENCEDocument6 pagesDos SANTOS - THE STRUCTURE OF DEPENDENCEmehranNo ratings yet

- Auditing Problem From Audit of InvestmentDocument61 pagesAuditing Problem From Audit of InvestmentNicole Anne Santiago SibuloNo ratings yet

- Unemployment and Inflation: © 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O'Sullivan & SheffrinDocument32 pagesUnemployment and Inflation: © 2005 Prentice Hall Business Publishing Survey of Economics, 2/e O'Sullivan & SheffrinAllen CarlNo ratings yet

- Topic:-Arguments in Favour and Against Nationalization of Commercial BanksDocument10 pagesTopic:-Arguments in Favour and Against Nationalization of Commercial BanksRagula praveenNo ratings yet

- GBPP Akuntansi ManajemenDocument3 pagesGBPP Akuntansi ManajemenMappa PbNo ratings yet

- Prepared by Anna Patricia Miravite: Absolute Advantage and Comparative AdvantageDocument3 pagesPrepared by Anna Patricia Miravite: Absolute Advantage and Comparative Advantagehannah iberaNo ratings yet