Case Study 2.internal Control-Cash

Case Study 2.internal Control-Cash

You might also like

- How To Avoid The Next Stock Market Crash (Liberated Stock Trader - Effective Investor Series Book 1)Document54 pagesHow To Avoid The Next Stock Market Crash (Liberated Stock Trader - Effective Investor Series Book 1)MAHINo ratings yet

- CH 08Document4 pagesCH 08vivienNo ratings yet

- ch08 ProblemDocument9 pagesch08 Problemapi-281193111No ratings yet

- CH 02Document3 pagesCH 02vivienNo ratings yet

- Cs 105 ExamDocument5 pagesCs 105 ExamBlythe AzodnemNo ratings yet

- IFRS Edition (2nd) : Fraud, Internal Control, and CashDocument54 pagesIFRS Edition (2nd) : Fraud, Internal Control, and CashLilis100% (2)

- CH 07Document5 pagesCH 07Ngọc NgốNo ratings yet

- ch08 PDFDocument4 pagesch08 PDFRabie HarounNo ratings yet

- Governance Activities-And-QuizzesdocxDocument4 pagesGovernance Activities-And-Quizzesdocxjp bNo ratings yet

- CH05 PaiDocument12 pagesCH05 PaiKanbiro OrkaidoNo ratings yet

- Cbe CH3 N 4Document13 pagesCbe CH3 N 4Solomon Abebe100% (2)

- FA Exercise Ch7Document2 pagesFA Exercise Ch7Sha EemNo ratings yet

- Practice Questions # 4 Internal Control and Cash With AnswersDocument9 pagesPractice Questions # 4 Internal Control and Cash With AnswersIzzahIkramIllahiNo ratings yet

- Acc CH 7Document8 pagesAcc CH 7Trickster TwelveNo ratings yet

- 5) Cash and Bank SystemDocument2 pages5) Cash and Bank SystemkasimranjhaNo ratings yet

- 5) Cash and Bank SystemDocument2 pages5) Cash and Bank Systemmzohair733No ratings yet

- Act 2112-3112-Introduction To Accounting Semester 1-2019 Tutorial Topic 3 - Accounting Systems and ControlDocument1 pageAct 2112-3112-Introduction To Accounting Semester 1-2019 Tutorial Topic 3 - Accounting Systems and Controltharshini rajNo ratings yet

- Cash in Bank Per Books Per Bank: InstructionsDocument9 pagesCash in Bank Per Books Per Bank: InstructionsDetha Prasetio KumaraNo ratings yet

- Bank Reconciliation Statement - Principles of AccountingDocument8 pagesBank Reconciliation Statement - Principles of AccountingAbdulla MaseehNo ratings yet

- Tutorial QuestionsDocument3 pagesTutorial QuestionsJaden EuNo ratings yet

- Chapter 5 - Cash Book & Bank ReconciliationsDocument6 pagesChapter 5 - Cash Book & Bank ReconciliationskundiarshdeepNo ratings yet

- ACC201 PPTs - 2T2019 - Workshop 06 - Week 07Document23 pagesACC201 PPTs - 2T2019 - Workshop 06 - Week 07Luu MinhNo ratings yet

- Bank ReconciliationDocument18 pagesBank ReconciliationFem FataleNo ratings yet

- 07 - Petty Cash Fund and Bank ReconciliationDocument2 pages07 - Petty Cash Fund and Bank ReconciliationCy Miolata100% (2)

- HFO HomeworkDocument2 pagesHFO HomeworkAna May Durante BaldelomarNo ratings yet

- ACC101 Chapter6newxcxDocument18 pagesACC101 Chapter6newxcxAhmed RawyNo ratings yet

- Fabm2 Q2 W1 QaDocument16 pagesFabm2 Q2 W1 Qajoshua.mayo.09152004No ratings yet

- Accounting Chapter 22 Test: True/FalseDocument3 pagesAccounting Chapter 22 Test: True/FalseZayli Morales100% (1)

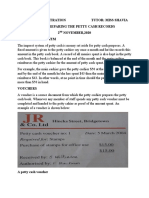

- Office Administration Tutor: Miss Shavia Topic: Preparing The Petty Cash Records 2 NOVEMBER, 2020 The Imprest SystemDocument5 pagesOffice Administration Tutor: Miss Shavia Topic: Preparing The Petty Cash Records 2 NOVEMBER, 2020 The Imprest SystemChristine RamkissoonNo ratings yet

- Final Chapter 6Document12 pagesFinal Chapter 6Nigussie BerhanuNo ratings yet

- CHAPTER 8 Internal Control and CashDocument8 pagesCHAPTER 8 Internal Control and CashAhmed RawyNo ratings yet

- CH 08Document4 pagesCH 08flrnciairnNo ratings yet

- Unit 5 CashDocument9 pagesUnit 5 CashNigussie BerhanuNo ratings yet

- Petty Cash BookDocument3 pagesPetty Cash BookFredhope Mtonga100% (1)

- CHAPTER SIX - Doc Internal Control Over CashDocument7 pagesCHAPTER SIX - Doc Internal Control Over CashYared DemissieNo ratings yet

- CASH Pertemuan 4Document5 pagesCASH Pertemuan 4Alim Try AlimNo ratings yet

- CH 5 Cash and ReceivblesDocument92 pagesCH 5 Cash and ReceivblesYohanna SisayNo ratings yet

- Petty CashDocument9 pagesPetty Cashramsha_tajammalNo ratings yet

- Bank Statement Template 25Document4 pagesBank Statement Template 25skhushbusahniNo ratings yet

- Petty Cash and Bank ReconciliationDocument3 pagesPetty Cash and Bank ReconciliationSalma HanaaaNo ratings yet

- B07 Akuntansi KasDocument27 pagesB07 Akuntansi KasFransisca Maya PermatasariNo ratings yet

- 10 - Soln Int CTRL - Part 1Document6 pages10 - Soln Int CTRL - Part 1ng li qiNo ratings yet

- MODAUD1 UNIT 2 - Audit of Cash and Cash TransactionsDocument8 pagesMODAUD1 UNIT 2 - Audit of Cash and Cash TransactionsJake Bundok100% (1)

- Accounting Assignment 05A 207Document11 pagesAccounting Assignment 05A 207Aniyah's RanticsNo ratings yet

- Petty CashDocument11 pagesPetty CashKim HaejinNo ratings yet

- Chapter - 6Document12 pagesChapter - 6Mehamed NureNo ratings yet

- Chapter 4 - Checking AccountsDocument7 pagesChapter 4 - Checking AccountsChristian Paul CayagoNo ratings yet

- Accounting Principle Kieso 8e - Ch08Document43 pagesAccounting Principle Kieso 8e - Ch08Sania M. JayantiNo ratings yet

- Exercise Cash ControlDocument6 pagesExercise Cash ControlYallyNo ratings yet

- Chapter 5Document5 pagesChapter 5Abrha636No ratings yet

- 05 Accounting For CashDocument37 pages05 Accounting For CashTahir DestaNo ratings yet

- Fundamentals of Book Keeping and Office PracticeDocument34 pagesFundamentals of Book Keeping and Office PracticemuteyobarlinNo ratings yet

- Acct 2600 Exam 2 Study SheetDocument11 pagesAcct 2600 Exam 2 Study Sheetapi-236442317No ratings yet

- Chapter 11 - Maintaining Petty Cash RecordsDocument28 pagesChapter 11 - Maintaining Petty Cash Recordsshemida100% (3)

- Chapter 13 RecitationDocument2 pagesChapter 13 RecitationPatricia ByunNo ratings yet

- Worksheet 3 Q2 Acctg. 2Document14 pagesWorksheet 3 Q2 Acctg. 2Allan TaripeNo ratings yet

- Accounting Cash Internal ControlsDocument14 pagesAccounting Cash Internal ControlsDave A ValcarcelNo ratings yet

- Unclaimed Money - Step by Step Guide how you claim your moneyFrom EverandUnclaimed Money - Step by Step Guide how you claim your moneyNo ratings yet

- The Young Entrepreneurs Financial Literacy Handbook Personal FinanceFrom EverandThe Young Entrepreneurs Financial Literacy Handbook Personal FinanceNo ratings yet

- College of Management: Capiz State UniversityDocument4 pagesCollege of Management: Capiz State UniversityDave IsoyNo ratings yet

- NPA HC119i - QuotationDocument1 pageNPA HC119i - QuotationvikasNo ratings yet

- Lecture Note 3 - Globalization and Role of MNCSDocument64 pagesLecture Note 3 - Globalization and Role of MNCSgydoiNo ratings yet

- Company AUM (In CR.) Number of CustomersDocument6 pagesCompany AUM (In CR.) Number of CustomersPraman TorgalmathNo ratings yet

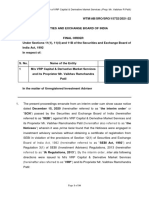

- Final Order in The Matter of VRP Capital & Derivative Market Services (Prop. Mr. Vaibhav R Patil)Document16 pagesFinal Order in The Matter of VRP Capital & Derivative Market Services (Prop. Mr. Vaibhav R Patil)Pratim MajumderNo ratings yet

- Movement Types SAPDocument10 pagesMovement Types SAPsatwikaNo ratings yet

- Ghana - Competitiveness Report - AFCTADocument12 pagesGhana - Competitiveness Report - AFCTAMikeowusuNo ratings yet

- Canadian Dollar: People Also AskDocument1 pageCanadian Dollar: People Also AskLordoc DoctorsaabNo ratings yet

- Sequrity Analysis and Portfolio ManagementDocument55 pagesSequrity Analysis and Portfolio ManagementMohit PalNo ratings yet

- Unit ACTIVITY 3Document2 pagesUnit ACTIVITY 3Alliyah NicolasNo ratings yet

- Inb QuestionDocument6 pagesInb Questionmili ahmed100% (1)

- Export Import ProcedureDocument12 pagesExport Import ProcedureAbrhaNo ratings yet

- High Seas Sale of Goods Under GSTDocument3 pagesHigh Seas Sale of Goods Under GSTSATYANARAYANA MOTAMARRINo ratings yet

- The Political Economy of International TradeDocument16 pagesThe Political Economy of International TradeWilsonNo ratings yet

- Ibt ReviewerDocument10 pagesIbt ReviewerBrenda CastilloNo ratings yet

- Structure and Functions of World Trade Organisation (WTO)Document7 pagesStructure and Functions of World Trade Organisation (WTO)Saahiel SharrmaNo ratings yet

- Chapter-22 - Finance Company OperationsDocument17 pagesChapter-22 - Finance Company Operationsmohammad olickNo ratings yet

- Audit Lingkungan Eksternal (Lanjutan) : Helmina Ardyanfitri, S.M.,M.MDocument17 pagesAudit Lingkungan Eksternal (Lanjutan) : Helmina Ardyanfitri, S.M.,M.MBarron LaksmanaNo ratings yet

- 1.1 British Empire in IndiaDocument37 pages1.1 British Empire in IndialavanyaNo ratings yet

- Clearance & Transportation From Port Unit Charges Sub Total (SGD)Document1 pageClearance & Transportation From Port Unit Charges Sub Total (SGD)Jake RixtonNo ratings yet

- Reflection Paper CONWORLDDocument10 pagesReflection Paper CONWORLDReina Carrie M DimlaNo ratings yet

- Survey of Accounting 6th Edition Warren Solutions ManualDocument25 pagesSurvey of Accounting 6th Edition Warren Solutions Manualbrianhue3zqkp100% (28)

- Tax 1 NotesDocument13 pagesTax 1 NotesCamille Antoinette BarizoNo ratings yet

- AFAR - Sir BradDocument36 pagesAFAR - Sir BradOliveros JaymarkNo ratings yet

- Hallmark Sco For 265 MT Au More Than 5 Years Old To Mr. Marcelo O. Isacchi and David Geffen. - Mr. Hussein OcampoDocument4 pagesHallmark Sco For 265 MT Au More Than 5 Years Old To Mr. Marcelo O. Isacchi and David Geffen. - Mr. Hussein OcampoMarcos RosalesNo ratings yet

- Henok Behailu FINALDocument46 pagesHenok Behailu FINALmusieNo ratings yet

- Questions 2023Document6 pagesQuestions 2023Rajesh YadavNo ratings yet

- INCOTERMS 2000 - Chart of ResponsibilityDocument3 pagesINCOTERMS 2000 - Chart of Responsibilityredback666No ratings yet

- Rangga Fakhrurriza - RMP Pertemuan 10Document2 pagesRangga Fakhrurriza - RMP Pertemuan 10Rangga FakhrurrizaKls AAkt 2021No ratings yet

Download as pdf or txt

You might also like

- How To Avoid The Next Stock Market Crash (Liberated Stock Trader - Effective Investor Series Book 1)Document54 pagesHow To Avoid The Next Stock Market Crash (Liberated Stock Trader - Effective Investor Series Book 1)MAHINo ratings yet

- CH 08Document4 pagesCH 08vivienNo ratings yet

- ch08 ProblemDocument9 pagesch08 Problemapi-281193111No ratings yet

- CH 02Document3 pagesCH 02vivienNo ratings yet

- Cs 105 ExamDocument5 pagesCs 105 ExamBlythe AzodnemNo ratings yet

- IFRS Edition (2nd) : Fraud, Internal Control, and CashDocument54 pagesIFRS Edition (2nd) : Fraud, Internal Control, and CashLilis100% (2)

- CH 07Document5 pagesCH 07Ngọc NgốNo ratings yet

- ch08 PDFDocument4 pagesch08 PDFRabie HarounNo ratings yet

- Governance Activities-And-QuizzesdocxDocument4 pagesGovernance Activities-And-Quizzesdocxjp bNo ratings yet

- CH05 PaiDocument12 pagesCH05 PaiKanbiro OrkaidoNo ratings yet

- Cbe CH3 N 4Document13 pagesCbe CH3 N 4Solomon Abebe100% (2)

- FA Exercise Ch7Document2 pagesFA Exercise Ch7Sha EemNo ratings yet

- Practice Questions # 4 Internal Control and Cash With AnswersDocument9 pagesPractice Questions # 4 Internal Control and Cash With AnswersIzzahIkramIllahiNo ratings yet

- Acc CH 7Document8 pagesAcc CH 7Trickster TwelveNo ratings yet

- 5) Cash and Bank SystemDocument2 pages5) Cash and Bank SystemkasimranjhaNo ratings yet

- 5) Cash and Bank SystemDocument2 pages5) Cash and Bank Systemmzohair733No ratings yet

- Act 2112-3112-Introduction To Accounting Semester 1-2019 Tutorial Topic 3 - Accounting Systems and ControlDocument1 pageAct 2112-3112-Introduction To Accounting Semester 1-2019 Tutorial Topic 3 - Accounting Systems and Controltharshini rajNo ratings yet

- Cash in Bank Per Books Per Bank: InstructionsDocument9 pagesCash in Bank Per Books Per Bank: InstructionsDetha Prasetio KumaraNo ratings yet

- Bank Reconciliation Statement - Principles of AccountingDocument8 pagesBank Reconciliation Statement - Principles of AccountingAbdulla MaseehNo ratings yet

- Tutorial QuestionsDocument3 pagesTutorial QuestionsJaden EuNo ratings yet

- Chapter 5 - Cash Book & Bank ReconciliationsDocument6 pagesChapter 5 - Cash Book & Bank ReconciliationskundiarshdeepNo ratings yet

- ACC201 PPTs - 2T2019 - Workshop 06 - Week 07Document23 pagesACC201 PPTs - 2T2019 - Workshop 06 - Week 07Luu MinhNo ratings yet

- Bank ReconciliationDocument18 pagesBank ReconciliationFem FataleNo ratings yet

- 07 - Petty Cash Fund and Bank ReconciliationDocument2 pages07 - Petty Cash Fund and Bank ReconciliationCy Miolata100% (2)

- HFO HomeworkDocument2 pagesHFO HomeworkAna May Durante BaldelomarNo ratings yet

- ACC101 Chapter6newxcxDocument18 pagesACC101 Chapter6newxcxAhmed RawyNo ratings yet

- Fabm2 Q2 W1 QaDocument16 pagesFabm2 Q2 W1 Qajoshua.mayo.09152004No ratings yet

- Accounting Chapter 22 Test: True/FalseDocument3 pagesAccounting Chapter 22 Test: True/FalseZayli Morales100% (1)

- Office Administration Tutor: Miss Shavia Topic: Preparing The Petty Cash Records 2 NOVEMBER, 2020 The Imprest SystemDocument5 pagesOffice Administration Tutor: Miss Shavia Topic: Preparing The Petty Cash Records 2 NOVEMBER, 2020 The Imprest SystemChristine RamkissoonNo ratings yet

- Final Chapter 6Document12 pagesFinal Chapter 6Nigussie BerhanuNo ratings yet

- CHAPTER 8 Internal Control and CashDocument8 pagesCHAPTER 8 Internal Control and CashAhmed RawyNo ratings yet

- CH 08Document4 pagesCH 08flrnciairnNo ratings yet

- Unit 5 CashDocument9 pagesUnit 5 CashNigussie BerhanuNo ratings yet

- Petty Cash BookDocument3 pagesPetty Cash BookFredhope Mtonga100% (1)

- CHAPTER SIX - Doc Internal Control Over CashDocument7 pagesCHAPTER SIX - Doc Internal Control Over CashYared DemissieNo ratings yet

- CASH Pertemuan 4Document5 pagesCASH Pertemuan 4Alim Try AlimNo ratings yet

- CH 5 Cash and ReceivblesDocument92 pagesCH 5 Cash and ReceivblesYohanna SisayNo ratings yet

- Petty CashDocument9 pagesPetty Cashramsha_tajammalNo ratings yet

- Bank Statement Template 25Document4 pagesBank Statement Template 25skhushbusahniNo ratings yet

- Petty Cash and Bank ReconciliationDocument3 pagesPetty Cash and Bank ReconciliationSalma HanaaaNo ratings yet

- B07 Akuntansi KasDocument27 pagesB07 Akuntansi KasFransisca Maya PermatasariNo ratings yet

- 10 - Soln Int CTRL - Part 1Document6 pages10 - Soln Int CTRL - Part 1ng li qiNo ratings yet

- MODAUD1 UNIT 2 - Audit of Cash and Cash TransactionsDocument8 pagesMODAUD1 UNIT 2 - Audit of Cash and Cash TransactionsJake Bundok100% (1)

- Accounting Assignment 05A 207Document11 pagesAccounting Assignment 05A 207Aniyah's RanticsNo ratings yet

- Petty CashDocument11 pagesPetty CashKim HaejinNo ratings yet

- Chapter - 6Document12 pagesChapter - 6Mehamed NureNo ratings yet

- Chapter 4 - Checking AccountsDocument7 pagesChapter 4 - Checking AccountsChristian Paul CayagoNo ratings yet

- Accounting Principle Kieso 8e - Ch08Document43 pagesAccounting Principle Kieso 8e - Ch08Sania M. JayantiNo ratings yet

- Exercise Cash ControlDocument6 pagesExercise Cash ControlYallyNo ratings yet

- Chapter 5Document5 pagesChapter 5Abrha636No ratings yet

- 05 Accounting For CashDocument37 pages05 Accounting For CashTahir DestaNo ratings yet

- Fundamentals of Book Keeping and Office PracticeDocument34 pagesFundamentals of Book Keeping and Office PracticemuteyobarlinNo ratings yet

- Acct 2600 Exam 2 Study SheetDocument11 pagesAcct 2600 Exam 2 Study Sheetapi-236442317No ratings yet

- Chapter 11 - Maintaining Petty Cash RecordsDocument28 pagesChapter 11 - Maintaining Petty Cash Recordsshemida100% (3)

- Chapter 13 RecitationDocument2 pagesChapter 13 RecitationPatricia ByunNo ratings yet

- Worksheet 3 Q2 Acctg. 2Document14 pagesWorksheet 3 Q2 Acctg. 2Allan TaripeNo ratings yet

- Accounting Cash Internal ControlsDocument14 pagesAccounting Cash Internal ControlsDave A ValcarcelNo ratings yet

- Unclaimed Money - Step by Step Guide how you claim your moneyFrom EverandUnclaimed Money - Step by Step Guide how you claim your moneyNo ratings yet

- The Young Entrepreneurs Financial Literacy Handbook Personal FinanceFrom EverandThe Young Entrepreneurs Financial Literacy Handbook Personal FinanceNo ratings yet

- College of Management: Capiz State UniversityDocument4 pagesCollege of Management: Capiz State UniversityDave IsoyNo ratings yet

- NPA HC119i - QuotationDocument1 pageNPA HC119i - QuotationvikasNo ratings yet

- Lecture Note 3 - Globalization and Role of MNCSDocument64 pagesLecture Note 3 - Globalization and Role of MNCSgydoiNo ratings yet

- Company AUM (In CR.) Number of CustomersDocument6 pagesCompany AUM (In CR.) Number of CustomersPraman TorgalmathNo ratings yet

- Final Order in The Matter of VRP Capital & Derivative Market Services (Prop. Mr. Vaibhav R Patil)Document16 pagesFinal Order in The Matter of VRP Capital & Derivative Market Services (Prop. Mr. Vaibhav R Patil)Pratim MajumderNo ratings yet

- Movement Types SAPDocument10 pagesMovement Types SAPsatwikaNo ratings yet

- Ghana - Competitiveness Report - AFCTADocument12 pagesGhana - Competitiveness Report - AFCTAMikeowusuNo ratings yet

- Canadian Dollar: People Also AskDocument1 pageCanadian Dollar: People Also AskLordoc DoctorsaabNo ratings yet

- Sequrity Analysis and Portfolio ManagementDocument55 pagesSequrity Analysis and Portfolio ManagementMohit PalNo ratings yet

- Unit ACTIVITY 3Document2 pagesUnit ACTIVITY 3Alliyah NicolasNo ratings yet

- Inb QuestionDocument6 pagesInb Questionmili ahmed100% (1)

- Export Import ProcedureDocument12 pagesExport Import ProcedureAbrhaNo ratings yet

- High Seas Sale of Goods Under GSTDocument3 pagesHigh Seas Sale of Goods Under GSTSATYANARAYANA MOTAMARRINo ratings yet

- The Political Economy of International TradeDocument16 pagesThe Political Economy of International TradeWilsonNo ratings yet

- Ibt ReviewerDocument10 pagesIbt ReviewerBrenda CastilloNo ratings yet

- Structure and Functions of World Trade Organisation (WTO)Document7 pagesStructure and Functions of World Trade Organisation (WTO)Saahiel SharrmaNo ratings yet

- Chapter-22 - Finance Company OperationsDocument17 pagesChapter-22 - Finance Company Operationsmohammad olickNo ratings yet

- Audit Lingkungan Eksternal (Lanjutan) : Helmina Ardyanfitri, S.M.,M.MDocument17 pagesAudit Lingkungan Eksternal (Lanjutan) : Helmina Ardyanfitri, S.M.,M.MBarron LaksmanaNo ratings yet

- 1.1 British Empire in IndiaDocument37 pages1.1 British Empire in IndialavanyaNo ratings yet

- Clearance & Transportation From Port Unit Charges Sub Total (SGD)Document1 pageClearance & Transportation From Port Unit Charges Sub Total (SGD)Jake RixtonNo ratings yet

- Reflection Paper CONWORLDDocument10 pagesReflection Paper CONWORLDReina Carrie M DimlaNo ratings yet

- Survey of Accounting 6th Edition Warren Solutions ManualDocument25 pagesSurvey of Accounting 6th Edition Warren Solutions Manualbrianhue3zqkp100% (28)

- Tax 1 NotesDocument13 pagesTax 1 NotesCamille Antoinette BarizoNo ratings yet

- AFAR - Sir BradDocument36 pagesAFAR - Sir BradOliveros JaymarkNo ratings yet

- Hallmark Sco For 265 MT Au More Than 5 Years Old To Mr. Marcelo O. Isacchi and David Geffen. - Mr. Hussein OcampoDocument4 pagesHallmark Sco For 265 MT Au More Than 5 Years Old To Mr. Marcelo O. Isacchi and David Geffen. - Mr. Hussein OcampoMarcos RosalesNo ratings yet

- Henok Behailu FINALDocument46 pagesHenok Behailu FINALmusieNo ratings yet

- Questions 2023Document6 pagesQuestions 2023Rajesh YadavNo ratings yet

- INCOTERMS 2000 - Chart of ResponsibilityDocument3 pagesINCOTERMS 2000 - Chart of Responsibilityredback666No ratings yet

- Rangga Fakhrurriza - RMP Pertemuan 10Document2 pagesRangga Fakhrurriza - RMP Pertemuan 10Rangga FakhrurrizaKls AAkt 2021No ratings yet