Download as pdf or txt

You might also like

- Dwnload Full College Accounting Chapters 1-27-22nd Edition Heintz Test Bank PDFDocument35 pagesDwnload Full College Accounting Chapters 1-27-22nd Edition Heintz Test Bank PDFouthaulpreter6cdttp100% (18)

- Template For New CISO Presentation To Board of DirectorsDocument39 pagesTemplate For New CISO Presentation To Board of DirectorsНиколай ЯрченковNo ratings yet

- HW - Third AttemptDocument49 pagesHW - Third AttemptRolando GrayNo ratings yet

- MODULE 4 Home Office and Branch Accounting PPT PDFDocument95 pagesMODULE 4 Home Office and Branch Accounting PPT PDFDanicaNo ratings yet

- Apollo Global Management LLC Feb Investor Presentation Update VFinalDocument40 pagesApollo Global Management LLC Feb Investor Presentation Update VFinalPepe Jara GinsbergNo ratings yet

- The Complete List of Unicorn CompaniesDocument39 pagesThe Complete List of Unicorn CompaniesKhushiNo ratings yet

- Accolite, Inc.: Private OwnershipDocument2 pagesAccolite, Inc.: Private Ownershiphitesh guptaNo ratings yet

- Final Version WeWork Article HBS HeaderDocument25 pagesFinal Version WeWork Article HBS HeaderDuc Beo100% (1)

- Ebix Investor Presentation WebDocument38 pagesEbix Investor Presentation Webamir.workNo ratings yet

- Venture Capital Advantages and DisadvantagesDocument24 pagesVenture Capital Advantages and DisadvantagesRLC VenturesNo ratings yet

- Info SysDocument11 pagesInfo Syskrishjain1178No ratings yet

- Ch.1 Business CombinationsDocument29 pagesCh.1 Business CombinationsdhfbbbbbbbbbbbbbbbbbhNo ratings yet

- BBIX Introduction - 20230519 - NTTIDocument9 pagesBBIX Introduction - 20230519 - NTTIMTsN 6 TulungagungNo ratings yet

- EFG HermesIRPresentation-3Q2014Document23 pagesEFG HermesIRPresentation-3Q2014marwan el deebNo ratings yet

- RFBR Apac Capital Markets PhilippinesDocument8 pagesRFBR Apac Capital Markets PhilippinesJheiaNo ratings yet

- Sole Proprietorship ("SP") General Partnership ("GP") Limited Partnership ("LP") Limited Liability Company ("LLC") Corporation ("Corp.")Document1 pageSole Proprietorship ("SP") General Partnership ("GP") Limited Partnership ("LP") Limited Liability Company ("LLC") Corporation ("Corp.")new smirdNo ratings yet

- Supply Chain Profile of US Airlines IndustryDocument6 pagesSupply Chain Profile of US Airlines IndustryHarshit GuptaNo ratings yet

- Verizon Reimagines Corporate Real EstateDocument27 pagesVerizon Reimagines Corporate Real EstateSheza AksarNo ratings yet

- Using Esops in Corporate TransactionsDocument12 pagesUsing Esops in Corporate Transactionsno nameNo ratings yet

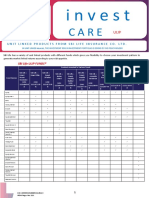

- SBI Life ULIP News Letter April 2023Document34 pagesSBI Life ULIP News Letter April 2023Kritika ThakurNo ratings yet

- Investment Product Guide, March 2018Document35 pagesInvestment Product Guide, March 2018Hiren ParekhNo ratings yet

- Aboitiz Equity Venture AEVDocument2 pagesAboitiz Equity Venture AEVJannelle RazaloNo ratings yet

- BCFV (LatamSeRecupera)Document18 pagesBCFV (LatamSeRecupera)arturocalleNo ratings yet

- Bala Surekha PDocument1 pageBala Surekha PMadhu MithaNo ratings yet

- NB Vendor Questionnaire v2.4Document10 pagesNB Vendor Questionnaire v2.4serpentor83No ratings yet

- RLC Ventures EIS GuideDocument24 pagesRLC Ventures EIS GuideRLC VenturesNo ratings yet

- Solved The Federal Government Gives Huge Rewards For Taking Action ToDocument1 pageSolved The Federal Government Gives Huge Rewards For Taking Action ToAnbu jaromiaNo ratings yet

- Bonesupport q4 Uncalled Share Drop Gives Attractive Entry Points 2024-02-16Document17 pagesBonesupport q4 Uncalled Share Drop Gives Attractive Entry Points 2024-02-16Antonio Rodríguez de la TorreNo ratings yet

- WorldcomDocument18 pagesWorldcomLakshmeesh RamMohan Maddala100% (1)

- Ebix: New Problems Emerge in Singapore, Sweden, and IndiaDocument30 pagesEbix: New Problems Emerge in Singapore, Sweden, and IndiagothamcityresearchNo ratings yet

- Carta Investor PitchDocument23 pagesCarta Investor PitchCLIFFNo ratings yet

- Why Wealthy People Are WealthyDocument1 pageWhy Wealthy People Are WealthyJithin Shyam T. VNo ratings yet

- Aboitiz Equity VenturesDocument6 pagesAboitiz Equity VenturesJoyce Ann Agdippa BarcelonaNo ratings yet

- Leadership Style (Organisational Theory and Design)Document16 pagesLeadership Style (Organisational Theory and Design)Pragyal MathurNo ratings yet

- EBZ Group Corporate PresentationDocument37 pagesEBZ Group Corporate PresentationJoel JustinNo ratings yet

- CORRECTED TRANSCRIPT - The Coca-Cola Co. (KO-US), Q4 2022 Earnings Call, 14-February-2023 8 - 30 AM ETDocument19 pagesCORRECTED TRANSCRIPT - The Coca-Cola Co. (KO-US), Q4 2022 Earnings Call, 14-February-2023 8 - 30 AM ETindierlianti3010No ratings yet

- HSBC List of Subsidiaries SEC InfoDocument9 pagesHSBC List of Subsidiaries SEC InfoPAAWS2No ratings yet

- Family Office PPTDocument9 pagesFamily Office PPTanish mahtoNo ratings yet

- ★(完成版)オリックス銀行の課題と成長戦略 20221014 EDocument48 pages★(完成版)オリックス銀行の課題と成長戦略 20221014 EĐỗ Quốc BảoNo ratings yet

- COBIT OverviewDocument17 pagesCOBIT OverviewLarbi BattiNo ratings yet

- Chapter-Two: Financail Assets, Financial Transaction and Financail IntrmefdiationDocument46 pagesChapter-Two: Financail Assets, Financial Transaction and Financail IntrmefdiationOmerNo ratings yet

- Avenue Commercial Investors Update Oct 2010Document3 pagesAvenue Commercial Investors Update Oct 2010scribd3780No ratings yet

- Apple Inc - Project Report: Qasim RasheedDocument13 pagesApple Inc - Project Report: Qasim RasheedqasimrasheedNo ratings yet

- Venture Capital For Sustainability - 2007: Created With The Support of The European CommissionDocument28 pagesVenture Capital For Sustainability - 2007: Created With The Support of The European Commissionm_arnoneNo ratings yet

- The Statement of Cash FlowsDocument51 pagesThe Statement of Cash FlowsrudraNo ratings yet

- Configuração Rapida Oracle CloudDocument608 pagesConfiguração Rapida Oracle CloudDanielNo ratings yet

- Asset Securitisation and Long Term Financing in The Power SectorDocument63 pagesAsset Securitisation and Long Term Financing in The Power SectorState House NigeriaNo ratings yet

- Airbnb, Inc. (PronouncedDocument19 pagesAirbnb, Inc. (PronouncedISST Subic BayNo ratings yet

- Topics Covered: How Corporations Issue SecuritiesDocument7 pagesTopics Covered: How Corporations Issue SecuritiesTam DoNo ratings yet

- SBI Life ULIP News Letter January 2022Document39 pagesSBI Life ULIP News Letter January 2022Srigandh's WealthNo ratings yet

- The Pyramid of Power The Perception Deception Documentary and Movie StoryDocument8 pagesThe Pyramid of Power The Perception Deception Documentary and Movie StoryvNo ratings yet

- NICE Information Service: 2021 Investors RelationsDocument23 pagesNICE Information Service: 2021 Investors RelationspuchooNo ratings yet

- Are We Heading Towards A Corporate Tax System Fit For The 21st Century?Document6 pagesAre We Heading Towards A Corporate Tax System Fit For The 21st Century?Devi PurnamasariNo ratings yet

- Fa InternalsDocument18 pagesFa InternalsAditya PatilNo ratings yet

- AGR ProfileDocument26 pagesAGR ProfilesritraderNo ratings yet

- AccountingDocument67 pagesAccountinggunanNo ratings yet

- The Little Four About To Eat The Big Four's LunchDocument7 pagesThe Little Four About To Eat The Big Four's LunchsciomakoNo ratings yet

- RMAX 2018 Annual Report BookmarkedDocument129 pagesRMAX 2018 Annual Report Bookmarkedub3rn3o100% (1)

- PSX The Basics of AccountingDocument1 pagePSX The Basics of Accounting마늘빵파스타No ratings yet

- Box - Google SearchDocument2 pagesBox - Google SearchMuhafeez GoolabNo ratings yet

- Business Plan: Company Name: Business Activity (If Trading Company)Document4 pagesBusiness Plan: Company Name: Business Activity (If Trading Company)sohatoNo ratings yet

- EIB Working Papers 2019/04 - Can survey-based information help to assess investment gaps in the EU?From EverandEIB Working Papers 2019/04 - Can survey-based information help to assess investment gaps in the EU?No ratings yet

- Valuable OSS - Delivering a Return on Your Investment in Operational Support Systems (OSS)From EverandValuable OSS - Delivering a Return on Your Investment in Operational Support Systems (OSS)No ratings yet

- Fria Ra 10142Document31 pagesFria Ra 10142Sheryl OgocNo ratings yet

- Chap3 PDFDocument46 pagesChap3 PDFrida0% (1)

- Security Guard Business PlanDocument16 pagesSecurity Guard Business PlanRock Amit JaiswalNo ratings yet

- Accounting Books - Journal, Ledger and Trial BalanceDocument35 pagesAccounting Books - Journal, Ledger and Trial BalanceGhie Ragat100% (3)

- Assignment 1Document17 pagesAssignment 1kerttanaNo ratings yet

- A Comparative Study On Pre-Merger & Post Merger Performance of Kotak Mahindra BankDocument25 pagesA Comparative Study On Pre-Merger & Post Merger Performance of Kotak Mahindra BankSantanu sahaNo ratings yet

- Acc CompilationDocument89 pagesAcc CompilationMehedi Hasan DurjoyNo ratings yet

- Pfrs For Smes - Acpapp WebsiteDocument56 pagesPfrs For Smes - Acpapp WebsiteThessaloe B. Fernandez100% (2)

- NET Paper 2 MCQ - ManagementDocument17 pagesNET Paper 2 MCQ - Managementchanus19No ratings yet

- FM E-NotesDocument30 pagesFM E-Notessuraj mathurNo ratings yet

- Segmental AnalysisDocument2 pagesSegmental AnalysisEsmeldo MicasNo ratings yet

- 11 Bradley Jarrell WACCDocument50 pages11 Bradley Jarrell WACCMiguel AngelNo ratings yet

- Final RequirementDocument18 pagesFinal RequirementZandra GonzalesNo ratings yet

- Nature & Importance of RetailingDocument64 pagesNature & Importance of RetailingSadiq Sagheer100% (3)

- Nasir Glasswire & Tubing Industries-IMDocument33 pagesNasir Glasswire & Tubing Industries-IMzakiur15No ratings yet

- Master Budget TemplateDocument19 pagesMaster Budget TemplateSanie Hizkia Hendrik MendeNo ratings yet

- Accounting Nov 2015 Memo EngDocument15 pagesAccounting Nov 2015 Memo EngAbubakr IsmailNo ratings yet

- Cap Table Cheat SheetDocument5 pagesCap Table Cheat SheetNasrul SalmanNo ratings yet

- The Internal Assessment: Strategic Management Concepts & CasesDocument33 pagesThe Internal Assessment: Strategic Management Concepts & CasesALI SHER HaidriNo ratings yet

- Test Bank For Accounting 25th Edition Carl S Warren DownloadDocument13 pagesTest Bank For Accounting 25th Edition Carl S Warren Downloadsequinsodgershsy100% (52)

- Hershey Foods Corporation - 2005Document10 pagesHershey Foods Corporation - 2005Vinay Singh0% (1)

- Financial Accounting and ReportingDocument6 pagesFinancial Accounting and ReportingCedric MepuaNo ratings yet

- Sbaa 1401Document126 pagesSbaa 1401gayuammu1135No ratings yet

- Coal IndiaDocument24 pagesCoal IndiaAswini Kumar BhuyanNo ratings yet

- Module 2 - Illustrative Problem 1Document19 pagesModule 2 - Illustrative Problem 1asdasdaNo ratings yet

- Statement of Financial Position Ass 1Document10 pagesStatement of Financial Position Ass 1MaitaNo ratings yet