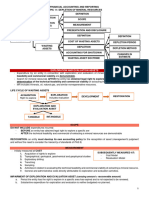

Exploration and Evaluation Expenditures

Exploration and Evaluation Expenditures

You might also like

- Auditing and Assurance - Mining Industries WORDDocument16 pagesAuditing and Assurance - Mining Industries WORDJazmine Hupp Uy0% (1)

- HOTEL - Hotel Investment Outlook 2017 (JLL)Document20 pagesHOTEL - Hotel Investment Outlook 2017 (JLL)pierrefranc0% (1)

- Section 15 3Document26 pagesSection 15 3Tuanhuyen1100% (1)

- DrillingDocument217 pagesDrillingMuhammad Sani Lawal LikkoNo ratings yet

- Audit in Specialized IndustriesDocument8 pagesAudit in Specialized IndustriesRhea Mae AgbayaniNo ratings yet

- ACC 107 - Table of Specifications Final Exam CoverageDocument1 pageACC 107 - Table of Specifications Final Exam CoverageEunice Lyafe PanilagNo ratings yet

- 2 S 31 Mineral Economic 31 EP 2017Document42 pages2 S 31 Mineral Economic 31 EP 2017TapiaNo ratings yet

- Wasting AssetsDocument4 pagesWasting AssetsjomelNo ratings yet

- Wasting Assets Lecture NotesDocument4 pagesWasting Assets Lecture Noteshoneyjoy salapantanNo ratings yet

- CONFRACS - Module 8 - Exploration and Evaluation of Mineral ResourcesDocument8 pagesCONFRACS - Module 8 - Exploration and Evaluation of Mineral ResourcesMatth FlorezNo ratings yet

- Jacobs Consultancy - Sales PresentationDocument9 pagesJacobs Consultancy - Sales PresentationvandelfinNo ratings yet

- FAR.2910 - Wasting Assets.Document4 pagesFAR.2910 - Wasting Assets.Edmark LuspeNo ratings yet

- 1 Rahul GuptaDocument9 pages1 Rahul GuptacyrilbhaskerNo ratings yet

- AF210 - Topic 5 - Lecture - MWDocument10 pagesAF210 - Topic 5 - Lecture - MWStanley RobertNo ratings yet

- 1.1 Petroleum Economics IntroDocument17 pages1.1 Petroleum Economics IntroZafNo ratings yet

- PMRC 131 - Mining Financial Analysis PDFDocument26 pagesPMRC 131 - Mining Financial Analysis PDFEmmanuel CaguimbalNo ratings yet

- DepletionDocument23 pagesDepletionRose DepistaNo ratings yet

- Depletion of Mineral Resources (Millan)Document3 pagesDepletion of Mineral Resources (Millan)didit.canonNo ratings yet

- Chapter 7 - Surface MiningDocument43 pagesChapter 7 - Surface MiningKajal Nayak100% (1)

- Chapter 7 - Surface MiningDocument43 pagesChapter 7 - Surface MiningLobsang MatosNo ratings yet

- 01 - Materials & Services MGTDocument6 pages01 - Materials & Services MGTmariechuNo ratings yet

- SRK - Valuation of Mineral AssetsDocument40 pagesSRK - Valuation of Mineral AssetsBill LiNo ratings yet

- Materi Webinar Open Pit / Tambang TerbukaDocument32 pagesMateri Webinar Open Pit / Tambang TerbukaNanda Yuri HayuNo ratings yet

- Ifrs 6 Exploration For and Evaluation of Mineral Resources: Fact SheetDocument8 pagesIfrs 6 Exploration For and Evaluation of Mineral Resources: Fact SheetTun Win KyawNo ratings yet

- Pfrs 6 Exploration For and Evaluation of Mineral ResourcesDocument8 pagesPfrs 6 Exploration For and Evaluation of Mineral ResourcesFritzie Marie A. PeregrinNo ratings yet

- FAR 11 Depletion of Mineral ResourcesDocument3 pagesFAR 11 Depletion of Mineral ResourcesShaira Mae DausNo ratings yet

- ES 200 - Module B - Lec - 4 - TNDocument23 pagesES 200 - Module B - Lec - 4 - TNdummy PavanNo ratings yet

- RPM Course Overview Mining For Non Miners Advanced Underground Coal.v1Document1 pageRPM Course Overview Mining For Non Miners Advanced Underground Coal.v1Prakash RajakNo ratings yet

- 1.1 Petroleum Economics IntroDocument17 pages1.1 Petroleum Economics IntroPRIYAH CoomarasamyNo ratings yet

- Economic EvaluationDocument17 pagesEconomic Evaluationadryan castroNo ratings yet

- PFRS 6 - Here Are Problems and Solutions. There Are Some Theories As Well That May HelpDocument5 pagesPFRS 6 - Here Are Problems and Solutions. There Are Some Theories As Well That May HelpJezela CastilloNo ratings yet

- Cost Control Training: Analisis Rantai NilaiDocument13 pagesCost Control Training: Analisis Rantai NilaiNovi AndryNo ratings yet

- SPE Introduction To E&P Petroleum Economics & Commercial: November 28, 2019 Lamé VerreDocument43 pagesSPE Introduction To E&P Petroleum Economics & Commercial: November 28, 2019 Lamé Verrejhon berez223344No ratings yet

- Chapter 28: Depletion Pfrs/Ifrs 6: Financial Reporting For The Exploration and Evaluation of Mineral ResourcesDocument3 pagesChapter 28: Depletion Pfrs/Ifrs 6: Financial Reporting For The Exploration and Evaluation of Mineral ResourcesKaryl FailmaNo ratings yet

- Exploration and Evaluation of Mineral Resources Under PFRS 6Document2 pagesExploration and Evaluation of Mineral Resources Under PFRS 6missyNo ratings yet

- PFRS 6 - 1Document1 pagePFRS 6 - 1Ella MaeNo ratings yet

- CHAPTER 5 - Feasibility StudyDocument15 pagesCHAPTER 5 - Feasibility StudynaurahimanNo ratings yet

- 5 - Lifecycle of Engineered ObjectsDocument16 pages5 - Lifecycle of Engineered ObjectsMasood AhmedNo ratings yet

- S3-5 Part 1Document14 pagesS3-5 Part 1LingNo ratings yet

- Shutdown & Turnaround ManagementDocument2 pagesShutdown & Turnaround ManagementPSP RaoNo ratings yet

- Wasting Assets Impairment of AssetsDocument14 pagesWasting Assets Impairment of AssetsJohn Ferd M. FerminNo ratings yet

- Training Hand Out - Economic Evaluation and Modeling of Mining ProjectsDocument73 pagesTraining Hand Out - Economic Evaluation and Modeling of Mining ProjectsAriyanto WibowoNo ratings yet

- 11.1.1.7.1 ProjectAnalyticsProductGuideDocument280 pages11.1.1.7.1 ProjectAnalyticsProductGuidetranganathanNo ratings yet

- ISO Basic PPT 9K1Document22 pagesISO Basic PPT 9K1Suhas AgawaneNo ratings yet

- Assignment For MID Topic: Mine Planning & DesignDocument57 pagesAssignment For MID Topic: Mine Planning & DesignUdit kumarNo ratings yet

- Maintenance Engineer PDDocument6 pagesMaintenance Engineer PDJulio CarlosNo ratings yet

- ExtendedAbstract Prohitech Paper68Document3 pagesExtendedAbstract Prohitech Paper68pablo gonzalezNo ratings yet

- Aud Application 2 - Handout 7 Wasting Asset (UST)Document5 pagesAud Application 2 - Handout 7 Wasting Asset (UST)RNo ratings yet

- Ppe 1Document48 pagesPpe 1Jasmine ManuelNo ratings yet

- Overview PSAK 64 Exploration and Evaluation Activities PDFDocument4 pagesOverview PSAK 64 Exploration and Evaluation Activities PDFpalti_siahaan6960No ratings yet

- Overview PSAK 64 Exploration and Evaluation ActivitiesDocument4 pagesOverview PSAK 64 Exploration and Evaluation Activitiespalti_siahaan6960No ratings yet

- 8.9.10.decision Analysisi and Portfolio ManagementDocument33 pages8.9.10.decision Analysisi and Portfolio ManagementBuğrahan İlginNo ratings yet

- Organization: Building A High-Performance Facilities EngineeringDocument6 pagesOrganization: Building A High-Performance Facilities Engineeringlhphong021191No ratings yet

- Intro To Field Development Planning (FDP)Document31 pagesIntro To Field Development Planning (FDP)HECTOR FLORESNo ratings yet

- Builders PlantDocument29 pagesBuilders PlantJulaida KaliwonNo ratings yet

- Accounting For DepreciationDocument55 pagesAccounting For DepreciationraghavNo ratings yet

- FA SessionNo3Document56 pagesFA SessionNo3Nazir AnsariNo ratings yet

- NZ Guideline-Scoping-Pre-FeasibilityDocument4 pagesNZ Guideline-Scoping-Pre-FeasibilityPatricioCastroNo ratings yet

- Chapter 34 Exploration and Evaluation of Mineral ResourcesDocument2 pagesChapter 34 Exploration and Evaluation of Mineral ResourcesEllen MaskariñoNo ratings yet

- Programme in Technical and Operational Surface Mining ExcellenceDocument3 pagesProgramme in Technical and Operational Surface Mining Excellenceantonio rodriguesvieiraNo ratings yet

- Chapter6-Investment DecisionDocument14 pagesChapter6-Investment DecisionchandoraNo ratings yet

- Cost Recovery: Turning Your Accounts Payable Department into a Profit CenterFrom EverandCost Recovery: Turning Your Accounts Payable Department into a Profit CenterNo ratings yet

- The FMDQ Daily Quotations List (November 12, 2013)Document2 pagesThe FMDQ Daily Quotations List (November 12, 2013)pmgtsNo ratings yet

- A Level, Partnership Accounts BasicsDocument16 pagesA Level, Partnership Accounts BasicsMohsen Shafiq80% (5)

- BPI02 - BPI Payroll Waiver Form (Annex A)Document1 pageBPI02 - BPI Payroll Waiver Form (Annex A)Icelle IsideraNo ratings yet

- Moldova CEMDocument122 pagesMoldova CEMOlga SicoraNo ratings yet

- A Literature Review On The Net Present Value (NPV) Valuation MethodDocument5 pagesA Literature Review On The Net Present Value (NPV) Valuation MethodressaevansNo ratings yet

- Lakh Datta Flour MillsDocument14 pagesLakh Datta Flour MillsjimmuNo ratings yet

- Leasing Standard IFRS 16Document6 pagesLeasing Standard IFRS 16Ani Nalitayui LifityaNo ratings yet

- Fin242 Lesson Plan March 2021Document2 pagesFin242 Lesson Plan March 2021Hazieq AushafNo ratings yet

- Test Bank For Risk Management and Insurance 12th Edition James S TrieschmannDocument24 pagesTest Bank For Risk Management and Insurance 12th Edition James S TrieschmannGeorgeWangeprm100% (44)

- TVS Motor - Taxmann VersionDocument19 pagesTVS Motor - Taxmann VersionSripal JainNo ratings yet

- CWT IdeologyDocument116 pagesCWT IdeologyЕкатерина РодионоваNo ratings yet

- Consumer Buying Behaviour Towards Life Insurance in Shirram Life InsuranceDocument74 pagesConsumer Buying Behaviour Towards Life Insurance in Shirram Life InsuranceAman KumarNo ratings yet

- (FA) 2 Multi-Step - Essay Practice Problem Solutions v2Document18 pages(FA) 2 Multi-Step - Essay Practice Problem Solutions v2Swapan Kumar SahaNo ratings yet

- AKUZAWA NewApproachVolatilitySkewDocument38 pagesAKUZAWA NewApproachVolatilitySkewfloqfloNo ratings yet

- Intacc Number 1Document2 pagesIntacc Number 1L LawlietNo ratings yet

- Bunny School FeesDocument1 pageBunny School FeesyouvsyouNo ratings yet

- Wholsale Energy MarketDocument105 pagesWholsale Energy Marketpodgorica56No ratings yet

- Private Banking by Mr. Najmuddin Mohd LutfiDocument11 pagesPrivate Banking by Mr. Najmuddin Mohd Lutfihafis82No ratings yet

- Understanding The Mind of The Commercial Bankers: Kuliah 12Document14 pagesUnderstanding The Mind of The Commercial Bankers: Kuliah 12Mahasewa IdNo ratings yet

- Stock and Their Valuation: Melziel A. Emba Far Eastern University - ManilaDocument40 pagesStock and Their Valuation: Melziel A. Emba Far Eastern University - ManilaJOHN PAOLO EVORANo ratings yet

- INDIAN ECONOMY AND POLICY MCQ PreparationDocument1 pageINDIAN ECONOMY AND POLICY MCQ PreparationChandan ArunNo ratings yet

- Tax QuizDocument2 pagesTax QuizMJ ArazasNo ratings yet

- Vinall 2014 - ValuationDocument19 pagesVinall 2014 - ValuationOmar MalikNo ratings yet

- Receipt and Payment AccountDocument3 pagesReceipt and Payment AccountAjay PratapNo ratings yet

- Concept of Lease ContractDocument7 pagesConcept of Lease ContractSah AnuNo ratings yet

- Interview Case Study 2 - Strategic Commodity SpecialistDocument5 pagesInterview Case Study 2 - Strategic Commodity SpecialisttalytaamorimNo ratings yet

- Newfmtb2 1Document28 pagesNewfmtb2 1fasdsadsaNo ratings yet

- Sobha - Update - Oct23 - HSIE-202310052150043697257Document12 pagesSobha - Update - Oct23 - HSIE-202310052150043697257sankalp111No ratings yet

Download as doc, pdf, or txt

You might also like

- Auditing and Assurance - Mining Industries WORDDocument16 pagesAuditing and Assurance - Mining Industries WORDJazmine Hupp Uy0% (1)

- HOTEL - Hotel Investment Outlook 2017 (JLL)Document20 pagesHOTEL - Hotel Investment Outlook 2017 (JLL)pierrefranc0% (1)

- Section 15 3Document26 pagesSection 15 3Tuanhuyen1100% (1)

- DrillingDocument217 pagesDrillingMuhammad Sani Lawal LikkoNo ratings yet

- Audit in Specialized IndustriesDocument8 pagesAudit in Specialized IndustriesRhea Mae AgbayaniNo ratings yet

- ACC 107 - Table of Specifications Final Exam CoverageDocument1 pageACC 107 - Table of Specifications Final Exam CoverageEunice Lyafe PanilagNo ratings yet

- 2 S 31 Mineral Economic 31 EP 2017Document42 pages2 S 31 Mineral Economic 31 EP 2017TapiaNo ratings yet

- Wasting AssetsDocument4 pagesWasting AssetsjomelNo ratings yet

- Wasting Assets Lecture NotesDocument4 pagesWasting Assets Lecture Noteshoneyjoy salapantanNo ratings yet

- CONFRACS - Module 8 - Exploration and Evaluation of Mineral ResourcesDocument8 pagesCONFRACS - Module 8 - Exploration and Evaluation of Mineral ResourcesMatth FlorezNo ratings yet

- Jacobs Consultancy - Sales PresentationDocument9 pagesJacobs Consultancy - Sales PresentationvandelfinNo ratings yet

- FAR.2910 - Wasting Assets.Document4 pagesFAR.2910 - Wasting Assets.Edmark LuspeNo ratings yet

- 1 Rahul GuptaDocument9 pages1 Rahul GuptacyrilbhaskerNo ratings yet

- AF210 - Topic 5 - Lecture - MWDocument10 pagesAF210 - Topic 5 - Lecture - MWStanley RobertNo ratings yet

- 1.1 Petroleum Economics IntroDocument17 pages1.1 Petroleum Economics IntroZafNo ratings yet

- PMRC 131 - Mining Financial Analysis PDFDocument26 pagesPMRC 131 - Mining Financial Analysis PDFEmmanuel CaguimbalNo ratings yet

- DepletionDocument23 pagesDepletionRose DepistaNo ratings yet

- Depletion of Mineral Resources (Millan)Document3 pagesDepletion of Mineral Resources (Millan)didit.canonNo ratings yet

- Chapter 7 - Surface MiningDocument43 pagesChapter 7 - Surface MiningKajal Nayak100% (1)

- Chapter 7 - Surface MiningDocument43 pagesChapter 7 - Surface MiningLobsang MatosNo ratings yet

- 01 - Materials & Services MGTDocument6 pages01 - Materials & Services MGTmariechuNo ratings yet

- SRK - Valuation of Mineral AssetsDocument40 pagesSRK - Valuation of Mineral AssetsBill LiNo ratings yet

- Materi Webinar Open Pit / Tambang TerbukaDocument32 pagesMateri Webinar Open Pit / Tambang TerbukaNanda Yuri HayuNo ratings yet

- Ifrs 6 Exploration For and Evaluation of Mineral Resources: Fact SheetDocument8 pagesIfrs 6 Exploration For and Evaluation of Mineral Resources: Fact SheetTun Win KyawNo ratings yet

- Pfrs 6 Exploration For and Evaluation of Mineral ResourcesDocument8 pagesPfrs 6 Exploration For and Evaluation of Mineral ResourcesFritzie Marie A. PeregrinNo ratings yet

- FAR 11 Depletion of Mineral ResourcesDocument3 pagesFAR 11 Depletion of Mineral ResourcesShaira Mae DausNo ratings yet

- ES 200 - Module B - Lec - 4 - TNDocument23 pagesES 200 - Module B - Lec - 4 - TNdummy PavanNo ratings yet

- RPM Course Overview Mining For Non Miners Advanced Underground Coal.v1Document1 pageRPM Course Overview Mining For Non Miners Advanced Underground Coal.v1Prakash RajakNo ratings yet

- 1.1 Petroleum Economics IntroDocument17 pages1.1 Petroleum Economics IntroPRIYAH CoomarasamyNo ratings yet

- Economic EvaluationDocument17 pagesEconomic Evaluationadryan castroNo ratings yet

- PFRS 6 - Here Are Problems and Solutions. There Are Some Theories As Well That May HelpDocument5 pagesPFRS 6 - Here Are Problems and Solutions. There Are Some Theories As Well That May HelpJezela CastilloNo ratings yet

- Cost Control Training: Analisis Rantai NilaiDocument13 pagesCost Control Training: Analisis Rantai NilaiNovi AndryNo ratings yet

- SPE Introduction To E&P Petroleum Economics & Commercial: November 28, 2019 Lamé VerreDocument43 pagesSPE Introduction To E&P Petroleum Economics & Commercial: November 28, 2019 Lamé Verrejhon berez223344No ratings yet

- Chapter 28: Depletion Pfrs/Ifrs 6: Financial Reporting For The Exploration and Evaluation of Mineral ResourcesDocument3 pagesChapter 28: Depletion Pfrs/Ifrs 6: Financial Reporting For The Exploration and Evaluation of Mineral ResourcesKaryl FailmaNo ratings yet

- Exploration and Evaluation of Mineral Resources Under PFRS 6Document2 pagesExploration and Evaluation of Mineral Resources Under PFRS 6missyNo ratings yet

- PFRS 6 - 1Document1 pagePFRS 6 - 1Ella MaeNo ratings yet

- CHAPTER 5 - Feasibility StudyDocument15 pagesCHAPTER 5 - Feasibility StudynaurahimanNo ratings yet

- 5 - Lifecycle of Engineered ObjectsDocument16 pages5 - Lifecycle of Engineered ObjectsMasood AhmedNo ratings yet

- S3-5 Part 1Document14 pagesS3-5 Part 1LingNo ratings yet

- Shutdown & Turnaround ManagementDocument2 pagesShutdown & Turnaround ManagementPSP RaoNo ratings yet

- Wasting Assets Impairment of AssetsDocument14 pagesWasting Assets Impairment of AssetsJohn Ferd M. FerminNo ratings yet

- Training Hand Out - Economic Evaluation and Modeling of Mining ProjectsDocument73 pagesTraining Hand Out - Economic Evaluation and Modeling of Mining ProjectsAriyanto WibowoNo ratings yet

- 11.1.1.7.1 ProjectAnalyticsProductGuideDocument280 pages11.1.1.7.1 ProjectAnalyticsProductGuidetranganathanNo ratings yet

- ISO Basic PPT 9K1Document22 pagesISO Basic PPT 9K1Suhas AgawaneNo ratings yet

- Assignment For MID Topic: Mine Planning & DesignDocument57 pagesAssignment For MID Topic: Mine Planning & DesignUdit kumarNo ratings yet

- Maintenance Engineer PDDocument6 pagesMaintenance Engineer PDJulio CarlosNo ratings yet

- ExtendedAbstract Prohitech Paper68Document3 pagesExtendedAbstract Prohitech Paper68pablo gonzalezNo ratings yet

- Aud Application 2 - Handout 7 Wasting Asset (UST)Document5 pagesAud Application 2 - Handout 7 Wasting Asset (UST)RNo ratings yet

- Ppe 1Document48 pagesPpe 1Jasmine ManuelNo ratings yet

- Overview PSAK 64 Exploration and Evaluation Activities PDFDocument4 pagesOverview PSAK 64 Exploration and Evaluation Activities PDFpalti_siahaan6960No ratings yet

- Overview PSAK 64 Exploration and Evaluation ActivitiesDocument4 pagesOverview PSAK 64 Exploration and Evaluation Activitiespalti_siahaan6960No ratings yet

- 8.9.10.decision Analysisi and Portfolio ManagementDocument33 pages8.9.10.decision Analysisi and Portfolio ManagementBuğrahan İlginNo ratings yet

- Organization: Building A High-Performance Facilities EngineeringDocument6 pagesOrganization: Building A High-Performance Facilities Engineeringlhphong021191No ratings yet

- Intro To Field Development Planning (FDP)Document31 pagesIntro To Field Development Planning (FDP)HECTOR FLORESNo ratings yet

- Builders PlantDocument29 pagesBuilders PlantJulaida KaliwonNo ratings yet

- Accounting For DepreciationDocument55 pagesAccounting For DepreciationraghavNo ratings yet

- FA SessionNo3Document56 pagesFA SessionNo3Nazir AnsariNo ratings yet

- NZ Guideline-Scoping-Pre-FeasibilityDocument4 pagesNZ Guideline-Scoping-Pre-FeasibilityPatricioCastroNo ratings yet

- Chapter 34 Exploration and Evaluation of Mineral ResourcesDocument2 pagesChapter 34 Exploration and Evaluation of Mineral ResourcesEllen MaskariñoNo ratings yet

- Programme in Technical and Operational Surface Mining ExcellenceDocument3 pagesProgramme in Technical and Operational Surface Mining Excellenceantonio rodriguesvieiraNo ratings yet

- Chapter6-Investment DecisionDocument14 pagesChapter6-Investment DecisionchandoraNo ratings yet

- Cost Recovery: Turning Your Accounts Payable Department into a Profit CenterFrom EverandCost Recovery: Turning Your Accounts Payable Department into a Profit CenterNo ratings yet

- The FMDQ Daily Quotations List (November 12, 2013)Document2 pagesThe FMDQ Daily Quotations List (November 12, 2013)pmgtsNo ratings yet

- A Level, Partnership Accounts BasicsDocument16 pagesA Level, Partnership Accounts BasicsMohsen Shafiq80% (5)

- BPI02 - BPI Payroll Waiver Form (Annex A)Document1 pageBPI02 - BPI Payroll Waiver Form (Annex A)Icelle IsideraNo ratings yet

- Moldova CEMDocument122 pagesMoldova CEMOlga SicoraNo ratings yet

- A Literature Review On The Net Present Value (NPV) Valuation MethodDocument5 pagesA Literature Review On The Net Present Value (NPV) Valuation MethodressaevansNo ratings yet

- Lakh Datta Flour MillsDocument14 pagesLakh Datta Flour MillsjimmuNo ratings yet

- Leasing Standard IFRS 16Document6 pagesLeasing Standard IFRS 16Ani Nalitayui LifityaNo ratings yet

- Fin242 Lesson Plan March 2021Document2 pagesFin242 Lesson Plan March 2021Hazieq AushafNo ratings yet

- Test Bank For Risk Management and Insurance 12th Edition James S TrieschmannDocument24 pagesTest Bank For Risk Management and Insurance 12th Edition James S TrieschmannGeorgeWangeprm100% (44)

- TVS Motor - Taxmann VersionDocument19 pagesTVS Motor - Taxmann VersionSripal JainNo ratings yet

- CWT IdeologyDocument116 pagesCWT IdeologyЕкатерина РодионоваNo ratings yet

- Consumer Buying Behaviour Towards Life Insurance in Shirram Life InsuranceDocument74 pagesConsumer Buying Behaviour Towards Life Insurance in Shirram Life InsuranceAman KumarNo ratings yet

- (FA) 2 Multi-Step - Essay Practice Problem Solutions v2Document18 pages(FA) 2 Multi-Step - Essay Practice Problem Solutions v2Swapan Kumar SahaNo ratings yet

- AKUZAWA NewApproachVolatilitySkewDocument38 pagesAKUZAWA NewApproachVolatilitySkewfloqfloNo ratings yet

- Intacc Number 1Document2 pagesIntacc Number 1L LawlietNo ratings yet

- Bunny School FeesDocument1 pageBunny School FeesyouvsyouNo ratings yet

- Wholsale Energy MarketDocument105 pagesWholsale Energy Marketpodgorica56No ratings yet

- Private Banking by Mr. Najmuddin Mohd LutfiDocument11 pagesPrivate Banking by Mr. Najmuddin Mohd Lutfihafis82No ratings yet

- Understanding The Mind of The Commercial Bankers: Kuliah 12Document14 pagesUnderstanding The Mind of The Commercial Bankers: Kuliah 12Mahasewa IdNo ratings yet

- Stock and Their Valuation: Melziel A. Emba Far Eastern University - ManilaDocument40 pagesStock and Their Valuation: Melziel A. Emba Far Eastern University - ManilaJOHN PAOLO EVORANo ratings yet

- INDIAN ECONOMY AND POLICY MCQ PreparationDocument1 pageINDIAN ECONOMY AND POLICY MCQ PreparationChandan ArunNo ratings yet

- Tax QuizDocument2 pagesTax QuizMJ ArazasNo ratings yet

- Vinall 2014 - ValuationDocument19 pagesVinall 2014 - ValuationOmar MalikNo ratings yet

- Receipt and Payment AccountDocument3 pagesReceipt and Payment AccountAjay PratapNo ratings yet

- Concept of Lease ContractDocument7 pagesConcept of Lease ContractSah AnuNo ratings yet

- Interview Case Study 2 - Strategic Commodity SpecialistDocument5 pagesInterview Case Study 2 - Strategic Commodity SpecialisttalytaamorimNo ratings yet

- Newfmtb2 1Document28 pagesNewfmtb2 1fasdsadsaNo ratings yet

- Sobha - Update - Oct23 - HSIE-202310052150043697257Document12 pagesSobha - Update - Oct23 - HSIE-202310052150043697257sankalp111No ratings yet