Download as pdf or txt

You might also like

- Effects On PPC Due To Various Govt. PoliciesDocument20 pagesEffects On PPC Due To Various Govt. PoliciesNaman Verma54% (390)

- FatDocument33 pagesFathanyapanda75% (4)

- Learn Financial Tearms for Stock Selection Criteria and Stock Screening Before TradingFrom EverandLearn Financial Tearms for Stock Selection Criteria and Stock Screening Before TradingNo ratings yet

- Financial MarketDocument16 pagesFinancial MarketchitkarashellyNo ratings yet

- Financial MarketDocument15 pagesFinancial MarketchitkarashellyNo ratings yet

- Features and Functions of Financial MarketDocument3 pagesFeatures and Functions of Financial MarketMaica PontillasNo ratings yet

- BFI Module 1 ScriptDocument29 pagesBFI Module 1 ScriptJanine anzanoNo ratings yet

- 1 The Investment Industry A Top Down ViewDocument21 pages1 The Investment Industry A Top Down ViewhimanshuNo ratings yet

- Module in Financial Management - 02Document9 pagesModule in Financial Management - 02Karen DammogNo ratings yet

- Retailing FsDocument11 pagesRetailing Fsnianidi0125No ratings yet

- Chapter 1: The Investment Industry: A Top Down ViewDocument18 pagesChapter 1: The Investment Industry: A Top Down ViewApratim BhaskarNo ratings yet

- Financial Markets and Institutions: What Is Intermediation' and Disintermediation'Document67 pagesFinancial Markets and Institutions: What Is Intermediation' and Disintermediation'Shalini SumanNo ratings yet

- Financial Environment Chapter 1 IntroductionDocument19 pagesFinancial Environment Chapter 1 IntroductionKing LionNo ratings yet

- An Overview of Indian Financial SystemDocument7 pagesAn Overview of Indian Financial SystemPavnesh KumarNo ratings yet

- Classical Neoclassical Economics Mainstream Economics Bank Deposits Loans Heterodox Economists Assets Liabilities Savers BorrowersDocument20 pagesClassical Neoclassical Economics Mainstream Economics Bank Deposits Loans Heterodox Economists Assets Liabilities Savers BorrowersKajal ChaudharyNo ratings yet

- Chapter 2 Financial Institutions in The Financial System 2010 FinalDocument17 pagesChapter 2 Financial Institutions in The Financial System 2010 FinalfiraolmosisabonkeNo ratings yet

- Financial IntermediariesDocument6 pagesFinancial IntermediariesJasmeet SinghNo ratings yet

- FIM - AssignmentDocument7 pagesFIM - AssignmentAkshatNo ratings yet

- Fmi EditDocument30 pagesFmi EditKanbiro OrkaidoNo ratings yet

- Lecture Note Law of Banking andDocument59 pagesLecture Note Law of Banking andEmebet Debissa100% (1)

- First Thing We Have To Cover, All The Materials You Will Find in The Website of Bangladesh Bank. (Cheque The Website of Bangladesh Bank)Document12 pagesFirst Thing We Have To Cover, All The Materials You Will Find in The Website of Bangladesh Bank. (Cheque The Website of Bangladesh Bank)afnan huqNo ratings yet

- Fin. Man 2Document24 pagesFin. Man 2Erick MequisoNo ratings yet

- Lec 01Document14 pagesLec 01charles luisNo ratings yet

- Business Environment Assignment - 2Document6 pagesBusiness Environment Assignment - 2Sohel AnsariNo ratings yet

- Ifs Materials ForDocument49 pagesIfs Materials ForKesavan Keshav100% (1)

- Financial LiteracyDocument67 pagesFinancial LiteracyDhiya MalarvannanNo ratings yet

- Money and banking ررقملا مسا Economics مسقلا حيمس اشر ذاتسلاا مسا Differentia between direct and indirect finance refer to different category and types of both kind of finance ثحبلا ناونعDocument6 pagesMoney and banking ررقملا مسا Economics مسقلا حيمس اشر ذاتسلاا مسا Differentia between direct and indirect finance refer to different category and types of both kind of finance ثحبلا ناونعHabiba MohamedNo ratings yet

- Montecillo, Review QuestionsDocument7 pagesMontecillo, Review QuestionsIvory Mae MontecilloNo ratings yet

- Lec 38Document14 pagesLec 38Chitresh MeenaNo ratings yet

- Introduction To Finance Lecture 1Document26 pagesIntroduction To Finance Lecture 1sestiliocharlesoremNo ratings yet

- Class Notes by Dr. DuttaDocument34 pagesClass Notes by Dr. Duttasakshi agrawalNo ratings yet

- 1 The Investment Industry A Top Down ViewDocument24 pages1 The Investment Industry A Top Down Viewakash jainNo ratings yet

- Ilovepdf MergedDocument582 pagesIlovepdf MergedSahil SawantNo ratings yet

- Geocf Reading and PrecisDocument15 pagesGeocf Reading and Preciseddiliasi555No ratings yet

- Business Finance Lesson 1 Financial SystemDocument3 pagesBusiness Finance Lesson 1 Financial SystemMatthew SuckNo ratings yet

- 1 The Investment Industry A Top Down ViewDocument20 pages1 The Investment Industry A Top Down Viewrajeshaisdu009No ratings yet

- Capital Market Assignment2Document2 pagesCapital Market Assignment2Benjamen KamzaNo ratings yet

- Actividad de Semana 1Document4 pagesActividad de Semana 1Daniela Agudelo riosNo ratings yet

- Cbar Reporting ExplanationDocument3 pagesCbar Reporting ExplanationMaica PontillasNo ratings yet

- Financial System PDFDocument1 pageFinancial System PDFMadeline MartinezNo ratings yet

- Financia Institutions and Markets Chapter 1Document12 pagesFinancia Institutions and Markets Chapter 1Surafel BefekaduNo ratings yet

- Module #4: Non-State InstitutionsDocument12 pagesModule #4: Non-State InstitutionsToga MarMarNo ratings yet

- Ucsp Module4Document8 pagesUcsp Module4Brendan Lewis DelgadoNo ratings yet

- Strategic Management Graded Assignment 1 2Document9 pagesStrategic Management Graded Assignment 1 2Keshav mananNo ratings yet

- Investment Analysis and Portfolio Management by M. Ranganatham)Document3 pagesInvestment Analysis and Portfolio Management by M. Ranganatham)Han ONo ratings yet

- An Overview of Financial SystemDocument6 pagesAn Overview of Financial SystemAshwani BhallaNo ratings yet

- Summer Internship ReportDocument16 pagesSummer Internship ReportRavi MehraNo ratings yet

- Lec 11Document21 pagesLec 11ROADYNo ratings yet

- Chapter 1 What Is Institutional Economics About?Document50 pagesChapter 1 What Is Institutional Economics About?Atul AryaNo ratings yet

- Finance Module 02 - Week 2R PDFDocument8 pagesFinance Module 02 - Week 2R PDFChristian ZebuaNo ratings yet

- UCSPDocument5 pagesUCSPNikka N. NazarioNo ratings yet

- Ebf - Part 1 + 2Document36 pagesEbf - Part 1 + 2Phạm HằngNo ratings yet

- Iem Notes RtuDocument13 pagesIem Notes RtugkgrasNo ratings yet

- Financial Market and InstitutionsDocument24 pagesFinancial Market and InstitutionsNehaChaudharyNo ratings yet

- The Time Value of Money and What Is Its Significance in Modern Day EconomyDocument2 pagesThe Time Value of Money and What Is Its Significance in Modern Day EconomyNitanshu ChavdaNo ratings yet

- Capital Market & Money MarketDocument8 pagesCapital Market & Money Marketshital maneNo ratings yet

- Module 2Document11 pagesModule 2Sherri BonquinNo ratings yet

- Mohit SinghDocument19 pagesMohit SinghAnkit KumarNo ratings yet

- Introduction To FinanceDocument68 pagesIntroduction To FinancejohnnybondNo ratings yet

- Philippine FINANCIAL SYSTEMDocument10 pagesPhilippine FINANCIAL SYSTEMFind DeviceNo ratings yet

- FINANCIAL SYSTEM Role in Economic DevelopmentDocument4 pagesFINANCIAL SYSTEM Role in Economic Developmentrevathi alekhya80% (10)

- Notes For HRMDocument7 pagesNotes For HRMBhavya NarangNo ratings yet

- Novel Drug Delivery SystemsDocument150 pagesNovel Drug Delivery SystemsBhavya NarangNo ratings yet

- Kirkpatrick Model Evaluation ModelDocument4 pagesKirkpatrick Model Evaluation ModelBhavya NarangNo ratings yet

- BSCExplanationDocument13 pagesBSCExplanationBhavya NarangNo ratings yet

- 2 EthicsGuideDocument15 pages2 EthicsGuideBhavya NarangNo ratings yet

- Noc20 Mg10 Assigment 1Document1 pageNoc20 Mg10 Assigment 1Bhavya NarangNo ratings yet

- q2 2023 Iqvia Indian Pharmaceutical Market Quarterly ReportDocument6 pagesq2 2023 Iqvia Indian Pharmaceutical Market Quarterly ReportBhavya NarangNo ratings yet

- BrandEquity JMRADocument9 pagesBrandEquity JMRABhavya NarangNo ratings yet

- Mathematical Modeling and Drug Release KineticsDocument31 pagesMathematical Modeling and Drug Release KineticsBhavya NarangNo ratings yet

- 002 DemandSupplyDocument28 pages002 DemandSupplyBhavya NarangNo ratings yet

- Market / Industry StructuresDocument17 pagesMarket / Industry StructuresBhavya NarangNo ratings yet

- Patent Cooperation TreatyDocument11 pagesPatent Cooperation TreatyBhavya NarangNo ratings yet

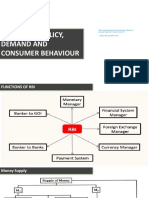

- Monetary Policy, Demand and Consumer Behaviour: Alculator/repo-Rate-Vs-Bank-Rate - HTML - Repo Rate and Bank RatreDocument23 pagesMonetary Policy, Demand and Consumer Behaviour: Alculator/repo-Rate-Vs-Bank-Rate - HTML - Repo Rate and Bank RatreBhavya NarangNo ratings yet

- More For Patrnt SearchDocument15 pagesMore For Patrnt SearchBhavya NarangNo ratings yet

- In Vitro in Vivo: Correlations (Ivivc)Document9 pagesIn Vitro in Vivo: Correlations (Ivivc)Bhavya NarangNo ratings yet

- 1.1 Indian Patent ActDocument74 pages1.1 Indian Patent ActBhavya NarangNo ratings yet

- Guidelines For Keeping Laboratory NotebooksDocument13 pagesGuidelines For Keeping Laboratory NotebooksBhavya NarangNo ratings yet

- Pre and Post Grant OppositionDocument21 pagesPre and Post Grant OppositionBhavya NarangNo ratings yet

- Revocation of PatentDocument13 pagesRevocation of PatentBhavya NarangNo ratings yet

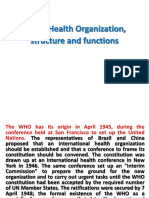

- World Health Organization, Structure and FunctionsDocument24 pagesWorld Health Organization, Structure and FunctionsBhavya NarangNo ratings yet

- 3.1 Conditions of Patentability & Non Patentable InventionsDocument23 pages3.1 Conditions of Patentability & Non Patentable InventionsBhavya NarangNo ratings yet

- 1.4 Amendments To 1970 Act - 2005Document21 pages1.4 Amendments To 1970 Act - 2005Bhavya NarangNo ratings yet

- 1.2 Patents in Brief - Filing of Patent Flow ChartDocument7 pages1.2 Patents in Brief - Filing of Patent Flow ChartBhavya NarangNo ratings yet

- MGT401 Midterm Paperz by YushaDocument27 pagesMGT401 Midterm Paperz by Yushamoni763No ratings yet

- Quantitative Financial Analytics The Path To Investment Profits (Dobelman, John A.Williams, Edward E) (Z-Library)Document621 pagesQuantitative Financial Analytics The Path To Investment Profits (Dobelman, John A.Williams, Edward E) (Z-Library)amitlkoyogaNo ratings yet

- Binmaley School of FisheriesDocument5 pagesBinmaley School of FisheriesNathan SorianoNo ratings yet

- IndicatorsDocument22 pagesIndicatorsManda Satyanarayana ReddyNo ratings yet

- Question Set Fabozzi, Chapter 12Document14 pagesQuestion Set Fabozzi, Chapter 12Hoang HaNo ratings yet

- Techniques For Risk AnalysisDocument7 pagesTechniques For Risk AnalysisshahiankitNo ratings yet

- 25 Income Under The Head PGBPDocument28 pages25 Income Under The Head PGBPzhuzhuzNo ratings yet

- UntitledDocument21 pagesUntitledaung sanNo ratings yet

- Synopsis On: "Working Capital Management"Document8 pagesSynopsis On: "Working Capital Management"diwakar0000000No ratings yet

- HDFC Bank: Three Segments of HDFC Banking ServicesDocument6 pagesHDFC Bank: Three Segments of HDFC Banking ServicesCharul AgrawalNo ratings yet

- Abandonment Option (Contd..)Document9 pagesAbandonment Option (Contd..)Pranav PNo ratings yet

- Power of AttorneyDocument2 pagesPower of AttorneyKamboj OfficeNo ratings yet

- Practice Sheet (Capm Model) : Prepared and Compiled by Prof Ankit WaliaDocument3 pagesPractice Sheet (Capm Model) : Prepared and Compiled by Prof Ankit WaliaSafe IndiaNo ratings yet

- Mechanics of Option Markets and Properties of Stock OptionsDocument53 pagesMechanics of Option Markets and Properties of Stock OptionsNaman JainNo ratings yet

- Passive Fund Factsheet January 2024Document97 pagesPassive Fund Factsheet January 2024asaultpraveenNo ratings yet

- Tutorial 8 AnswersDocument7 pagesTutorial 8 AnswersFahad Afzal Cheema100% (1)

- Solution Manual For Financial ACCT 2010 1st Edition by GodwinDocument12 pagesSolution Manual For Financial ACCT 2010 1st Edition by Godwina527996566No ratings yet

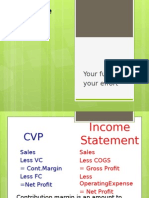

- Cost Volume Profit (CVP) Analysis and Break Even Point AnalysisDocument22 pagesCost Volume Profit (CVP) Analysis and Break Even Point Analysisimelda100% (1)

- Turner Construction CompanyDocument2 pagesTurner Construction CompanySwapnil J. SoniNo ratings yet

- Letters and Application For B A English Language Paper B Punjab University Lahore PakistanDocument15 pagesLetters and Application For B A English Language Paper B Punjab University Lahore Pakistanapi-217232127No ratings yet

- Nokia Demand Supply Analysis PDFDocument21 pagesNokia Demand Supply Analysis PDFvineetarora1000% (1)

- La Colosa Goes World ClassDocument3 pagesLa Colosa Goes World ClassYuri Andrei GarciaNo ratings yet

- Parle+Report+CODocument78 pagesParle+Report+COSaurabh AtriNo ratings yet

- Accounting QuestionsDocument4 pagesAccounting Questionsjohana galvezNo ratings yet

- Singapore Property Weekly Issue 197Document14 pagesSingapore Property Weekly Issue 197Propwise.sgNo ratings yet

- Op-Ed: Trend of Economic Globalization Unstoppable: by Zhong Xuanli 09:19, October 15, 2018Document2 pagesOp-Ed: Trend of Economic Globalization Unstoppable: by Zhong Xuanli 09:19, October 15, 2018rhiantics_kram11No ratings yet

- UntitledDocument135 pagesUntitledRohol Amin RajuNo ratings yet

- Stasha Jovanovic - Modern Railway Infrastructure Asset ManagementDocument7 pagesStasha Jovanovic - Modern Railway Infrastructure Asset ManagementStasha JovanovicNo ratings yet