Download as pdf or txt

You might also like

- RBGH Financials 31 December 2020 Colour 18.03.2021 3 Full PageseddDocument3 pagesRBGH Financials 31 December 2020 Colour 18.03.2021 3 Full PageseddFuaad DodooNo ratings yet

- Unaudited Financial Statements For The Period Ended 31 March, 2022Document2 pagesUnaudited Financial Statements For The Period Ended 31 March, 2022Fuaad DodooNo ratings yet

- Summary Consolidated and Separate Financial Statements For The Period Ended 30 Sept 2021 (Unaudited)Document1 pageSummary Consolidated and Separate Financial Statements For The Period Ended 30 Sept 2021 (Unaudited)Fuaad DodooNo ratings yet

- Unaudited Financial Statements For The Period Ended 30 September, 2021Document2 pagesUnaudited Financial Statements For The Period Ended 30 September, 2021Fuaad DodooNo ratings yet

- Globus Bank 2021 ABRIDGED FSDocument1 pageGlobus Bank 2021 ABRIDGED FSAwojuyigbeNo ratings yet

- CAL BankDocument2 pagesCAL BankFuaad DodooNo ratings yet

- Unaudited Summary Consolidated and Separate Financial StatementsDocument2 pagesUnaudited Summary Consolidated and Separate Financial Statementsbentilwilliams65No ratings yet

- Societe Generale Ghana PLC Unaudited Financial Statements For The Quarter Ended 30 September 2021Document2 pagesSociete Generale Ghana PLC Unaudited Financial Statements For The Quarter Ended 30 September 2021Fuaad DodooNo ratings yet

- UBA - June2021 FN StatementsDocument2 pagesUBA - June2021 FN StatementsFuaad DodooNo ratings yet

- Final 2021 CBG Summary Fs 2021 SignedDocument2 pagesFinal 2021 CBG Summary Fs 2021 SignedFuaad DodooNo ratings yet

- Societe Generale Ghana PLC 2021 Audited Financial StatementsDocument2 pagesSociete Generale Ghana PLC 2021 Audited Financial StatementsFuaad DodooNo ratings yet

- Ratio Analysis of Lanka Ashok Leyland PLCDocument6 pagesRatio Analysis of Lanka Ashok Leyland PLCThe MutantzNo ratings yet

- 2021 2020 Bank Group Bank Group: in Thousands of Ghana Cedis in Thousands of Ghana CedisDocument2 pages2021 2020 Bank Group Bank Group: in Thousands of Ghana Cedis in Thousands of Ghana CedisFuaad DodooNo ratings yet

- ILAM FAHARI I REIT - Audited Finacncials 2020Document1 pageILAM FAHARI I REIT - Audited Finacncials 2020An AntonyNo ratings yet

- Societe Generale Ghana PLC Unaudited Financial Statements For The Half Year Ended 30 June 2021Document2 pagesSociete Generale Ghana PLC Unaudited Financial Statements For The Half Year Ended 30 June 2021Fuaad DodooNo ratings yet

- Adb Fin Statement - Dec 2020 - Final 2Document2 pagesAdb Fin Statement - Dec 2020 - Final 2Fuaad DodooNo ratings yet

- Ecobank Ghana Limited: Un-Audited Financial Statements For The Three-Month Period Ended 31 March 2022Document8 pagesEcobank Ghana Limited: Un-Audited Financial Statements For The Three-Month Period Ended 31 March 2022Fuaad DodooNo ratings yet

- Q2fy23 Investor SheetDocument13 pagesQ2fy23 Investor SheetHello Brother2No ratings yet

- Financial Statements: For The Year Ended 31 December 2019Document11 pagesFinancial Statements: For The Year Ended 31 December 2019RajithWNNo ratings yet

- Sri Lanka Telecom PLC: Condensed Consolidated Interim Financial Statements For The Quarter Ended 31 December 2019Document14 pagesSri Lanka Telecom PLC: Condensed Consolidated Interim Financial Statements For The Quarter Ended 31 December 2019Nilupul BasnayakeNo ratings yet

- RBGH Financials 30 June 2021 Colour 15.07.2021 2 Full Pages EdtDocument2 pagesRBGH Financials 30 June 2021 Colour 15.07.2021 2 Full Pages EdtFuaad DodooNo ratings yet

- Standard Chartered Bank Ghana PLC: Unaudited Financial Statements For The Period Ended 30 September 2021Document1 pageStandard Chartered Bank Ghana PLC: Unaudited Financial Statements For The Period Ended 30 September 2021Fuaad DodooNo ratings yet

- VIL Reg 33 Results Q4FY24Document10 pagesVIL Reg 33 Results Q4FY24Samim Al RashidNo ratings yet

- B - 02 - KFH - Fs 31 December 2020 - enDocument69 pagesB - 02 - KFH - Fs 31 December 2020 - enRizkyAufaSNo ratings yet

- BK Group PLC Financial Results: Net Interest Income 51,762,974 46,360,210Document3 pagesBK Group PLC Financial Results: Net Interest Income 51,762,974 46,360,210chegeNo ratings yet

- Hong Fok Corporation Limited: Revenue (Note 1)Document10 pagesHong Fok Corporation Limited: Revenue (Note 1)Theng RogerNo ratings yet

- Q3 Financial Statement q3 For Period 30 September 2021Document2 pagesQ3 Financial Statement q3 For Period 30 September 2021Fuaad DodooNo ratings yet

- Societe Generale Ghana PLC Unaudited Financial Statements For The Quarter Ended 31 March 2022Document2 pagesSociete Generale Ghana PLC Unaudited Financial Statements For The Quarter Ended 31 March 2022Fuaad DodooNo ratings yet

- + UpdatedDocument22 pages+ UpdatedRobert ManjoNo ratings yet

- Consolidated Bank (Ghana) Limited: Unaudited Summary Financial StatementsDocument2 pagesConsolidated Bank (Ghana) Limited: Unaudited Summary Financial StatementsFuaad DodooNo ratings yet

- KPIs Bharti Airtel 04022020Document13 pagesKPIs Bharti Airtel 04022020laksikaNo ratings yet

- AmSpa Financials 150222Document59 pagesAmSpa Financials 150222Amelia SmithNo ratings yet

- Uba Annual Report Accounts 2022Document286 pagesUba Annual Report Accounts 2022G mbawalaNo ratings yet

- 2021 Full Year FinancialsDocument2 pages2021 Full Year FinancialsFuaad DodooNo ratings yet

- Quarterly Analysis: Analysis of Variation in Interim Results and Final AccountsDocument1 pageQuarterly Analysis: Analysis of Variation in Interim Results and Final Accounts.No ratings yet

- Net Revenue $ 15,301 $ 16,883 $ 14,950 Operating Expenses: Consolidated Statement of OperationsDocument1 pageNet Revenue $ 15,301 $ 16,883 $ 14,950 Operating Expenses: Consolidated Statement of OperationsMaanvee JaiswalNo ratings yet

- United Bank Limited and Its Subsidiary CompaniesDocument15 pagesUnited Bank Limited and Its Subsidiary Companieszaighum sultanNo ratings yet

- Cscstel 202206 Q2Document13 pagesCscstel 202206 Q2Al TanNo ratings yet

- Top Glove 2020, 2021Document3 pagesTop Glove 2020, 2021nabil izzatNo ratings yet

- TML q4 Fy 21 Consolidated ResultsDocument6 pagesTML q4 Fy 21 Consolidated ResultsGyanendra AryaNo ratings yet

- GT BankDocument1 pageGT BankFuaad DodooNo ratings yet

- Financial Statement 2020Document3 pagesFinancial Statement 2020Fuaad DodooNo ratings yet

- Quarterly Report 20221231Document21 pagesQuarterly Report 20221231Ang SHNo ratings yet

- Group Income StatementDocument1 pageGroup Income StatementAJNAZ PACIFICNo ratings yet

- Ecobank GhanaDocument8 pagesEcobank GhanaFuaad DodooNo ratings yet

- Goil Company Limited: Group Unaudited Statement of Comprehensive Income For The Period Ended March 31,2022Document4 pagesGoil Company Limited: Group Unaudited Statement of Comprehensive Income For The Period Ended March 31,2022Fuaad DodooNo ratings yet

- Access BankDocument1 pageAccess BankFuaad DodooNo ratings yet

- Quarterly Report 20191231Document21 pagesQuarterly Report 20191231Ang SHNo ratings yet

- Enterprise Group PLC: Unaudited Financial Statements For The Year Ended 31 December 2021Document8 pagesEnterprise Group PLC: Unaudited Financial Statements For The Year Ended 31 December 2021Fuaad DodooNo ratings yet

- JLR Ar Fy23 24Document4 pagesJLR Ar Fy23 24Rishit PrakashNo ratings yet

- United Bank For Africa (Ghana) Limited Summary Financial Statements For The Year Ended 31 December 2020Document2 pagesUnited Bank For Africa (Ghana) Limited Summary Financial Statements For The Year Ended 31 December 2020Fuaad DodooNo ratings yet

- Financial Report Q1 2021Document21 pagesFinancial Report Q1 2021FiestaNo ratings yet

- Standard Chartered PLC Full Year 2022 ReportDocument9 pagesStandard Chartered PLC Full Year 2022 Reporthoneysgh.394No ratings yet

- Lloyds Banking Group-2021-Annual-Report - Part2 - Financial ResultsDocument24 pagesLloyds Banking Group-2021-Annual-Report - Part2 - Financial ResultsyahbNo ratings yet

- Blackstone 1 Q 20 Earnings Press ReleaseDocument40 pagesBlackstone 1 Q 20 Earnings Press ReleaseZerohedgeNo ratings yet

- UntitledDocument288 pagesUntitledOlamide AjiboyeNo ratings yet

- Annual Report 2019Document4 pagesAnnual Report 2019Rahman GafarNo ratings yet

- Consolidated Financial Statements Mar 09Document15 pagesConsolidated Financial Statements Mar 09Naseer AhmadNo ratings yet

- Consolidated Bank (Ghana) Limited: Unaudited Summary Financial StatementsDocument2 pagesConsolidated Bank (Ghana) Limited: Unaudited Summary Financial StatementsFuaad DodooNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- 19th Edition of The Ghana Club 100 Rankings OutcomeDocument3 pages19th Edition of The Ghana Club 100 Rankings OutcomeFuaad DodooNo ratings yet

- Daily Equity Market Report - 18.10.2022Document1 pageDaily Equity Market Report - 18.10.2022Fuaad DodooNo ratings yet

- Daily Equity Market Report - 17.10.2022Document1 pageDaily Equity Market Report - 17.10.2022Fuaad DodooNo ratings yet

- Press Release 2Document1 pagePress Release 2Fuaad DodooNo ratings yet

- Daily Equity Market Report - 05.10.2022Document1 pageDaily Equity Market Report - 05.10.2022Fuaad DodooNo ratings yet

- Weekly Capital Market Report - Week Ending 14.10.2022Document2 pagesWeekly Capital Market Report - Week Ending 14.10.2022Fuaad DodooNo ratings yet

- Weekly Capital Market Report - Week Ending 07.10.2022Document2 pagesWeekly Capital Market Report - Week Ending 07.10.2022Fuaad DodooNo ratings yet

- Daily Equity Market Report - 11.10.2022Document1 pageDaily Equity Market Report - 11.10.2022Fuaad DodooNo ratings yet

- Daily Equity Market Report - 06.10.2022Document1 pageDaily Equity Market Report - 06.10.2022Fuaad DodooNo ratings yet

- Substandard (Contaminated) Paediatric Medicines Identified in WHODocument4 pagesSubstandard (Contaminated) Paediatric Medicines Identified in WHOFuaad DodooNo ratings yet

- Regulatory Order To ECG - 221004 - 180752Document6 pagesRegulatory Order To ECG - 221004 - 180752Fuaad DodooNo ratings yet

- Fixed Income Market Report - 10.10.2022Document1 pageFixed Income Market Report - 10.10.2022Fuaad DodooNo ratings yet

- R9 News Release Gender Inequalities Persist in Ghana Afrobarometer BH MA 4oct22Document4 pagesR9 News Release Gender Inequalities Persist in Ghana Afrobarometer BH MA 4oct22Fuaad DodooNo ratings yet

- Press ReleaseDocument1 pagePress ReleaseFuaad DodooNo ratings yet

- Daily Equity Market Report - 29.09.2022Document1 pageDaily Equity Market Report - 29.09.2022Fuaad DodooNo ratings yet

- Daily Equity Market Report 03.10.2022 2022-10-03Document1 pageDaily Equity Market Report 03.10.2022 2022-10-03Fuaad DodooNo ratings yet

- Weekly Capital Market Report - Week Ending 30.09.2022Document2 pagesWeekly Capital Market Report - Week Ending 30.09.2022Fuaad DodooNo ratings yet

- Fixed Income Market Report - 03.10.2022Document1 pageFixed Income Market Report - 03.10.2022Fuaad DodooNo ratings yet

- Daily Equity Market Report - 28.09.2022Document1 pageDaily Equity Market Report - 28.09.2022Fuaad DodooNo ratings yet

- Daily Equity Market Report - 04.10.2022Document1 pageDaily Equity Market Report - 04.10.2022Fuaad DodooNo ratings yet

- Daily Equity Market Report - 22.09.2022Document1 pageDaily Equity Market Report - 22.09.2022Fuaad DodooNo ratings yet

- Daily Equity Market Report - 27.09.2022Document1 pageDaily Equity Market Report - 27.09.2022Fuaad DodooNo ratings yet

- Imf MeetingDocument1 pageImf MeetingFuaad DodooNo ratings yet

- Daily Equity Market Report 20.09.2022 2022-09-20Document1 pageDaily Equity Market Report 20.09.2022 2022-09-20Fuaad DodooNo ratings yet

- Weekly Capital Market Report - Week Ending 23.09.2022Document2 pagesWeekly Capital Market Report - Week Ending 23.09.2022Fuaad DodooNo ratings yet

- Fixed Income Market Report - 26.09.2022Document1 pageFixed Income Market Report - 26.09.2022Fuaad DodooNo ratings yet

- Nimed Financial Market Review (16.09.2022)Document4 pagesNimed Financial Market Review (16.09.2022)Fuaad DodooNo ratings yet

- Daily Equity Market Report - 26.09.2022Document1 pageDaily Equity Market Report - 26.09.2022Fuaad DodooNo ratings yet

- Auctresults 1817Document1 pageAuctresults 1817Fuaad DodooNo ratings yet

- Daily Equity Market Report - 19.09.2022Document1 pageDaily Equity Market Report - 19.09.2022Fuaad DodooNo ratings yet

- Fi32BPP Course NotesDocument384 pagesFi32BPP Course NotesZ XNNo ratings yet

- 19bbl018, 045, 048Document17 pages19bbl018, 045, 048Sakshi AgrawalNo ratings yet

- Wasl VATDocument2 pagesWasl VATAMITNo ratings yet

- Dwnload Full Business Ethics Ethical Decision Making and Cases 9th Edition Ferrell Solutions Manual PDFDocument35 pagesDwnload Full Business Ethics Ethical Decision Making and Cases 9th Edition Ferrell Solutions Manual PDFtrichitegraverye1bzv8100% (18)

- The Different Types of Benchmarking - Bernard MarrDocument14 pagesThe Different Types of Benchmarking - Bernard MarrEzra Mikah G. CaalimNo ratings yet

- Gen Maths 07Document26 pagesGen Maths 07Sibin G ThomasNo ratings yet

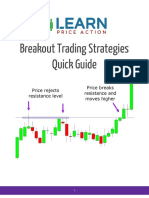

- Breakout Trading Strategies Quick GuideDocument10 pagesBreakout Trading Strategies Quick GuideAdam ChoNo ratings yet

- Current Affairs Pocket PDF - July 2021 by AffairsCloud 1Document127 pagesCurrent Affairs Pocket PDF - July 2021 by AffairsCloud 1kaviNo ratings yet

- SOP For Truck Entry Exit - 015Document4 pagesSOP For Truck Entry Exit - 015syed aquibNo ratings yet

- MAPEH (Health) : Quarter 1 - Module 5: Consumer Health: Consumer LawDocument11 pagesMAPEH (Health) : Quarter 1 - Module 5: Consumer Health: Consumer LawKatrinjhgfgga CasugaNo ratings yet

- KLMinvoice 04062020Document1 pageKLMinvoice 04062020Jack RobinsonNo ratings yet

- Semi Final AccountingDocument8 pagesSemi Final AccountingSherryl DumagpiNo ratings yet

- 3-John Bellamy Foster - Ecology Against Capitalism-Monthly Review Press (2002)Document180 pages3-John Bellamy Foster - Ecology Against Capitalism-Monthly Review Press (2002)Cengiz YılmazNo ratings yet

- Solutions Manual - Chapter 3Document7 pagesSolutions Manual - Chapter 3Renu TharshiniNo ratings yet

- Question-1 I) : SKANS School of Accountancy Principles of Taxation Mid Term ExamDocument4 pagesQuestion-1 I) : SKANS School of Accountancy Principles of Taxation Mid Term ExamMuhammad ArslanNo ratings yet

- SCMDocument11 pagesSCMHardik GangarNo ratings yet

- Types LiquidityDocument10 pagesTypes Liquiditysatori investmentsNo ratings yet

- GM14Document2 pagesGM14bhaktiNo ratings yet

- Main Aur Mera Vyakaran-07 TB 5 ChaptersDocument68 pagesMain Aur Mera Vyakaran-07 TB 5 ChaptersRAVI SHANKARNo ratings yet

- KnowMore Test TasksDocument6 pagesKnowMore Test TasksMonnu montoNo ratings yet

- Uj 7201+Content1+Content1.2Document61 pagesUj 7201+Content1+Content1.2TashNo ratings yet

- Going To University Is More Important Than Ever For Young People - All Must Have DegreesDocument8 pagesGoing To University Is More Important Than Ever For Young People - All Must Have Degreessebastyan_v5466No ratings yet

- Salvador - Kepco-Ilijan Corporation v. CirDocument19 pagesSalvador - Kepco-Ilijan Corporation v. CirAntonio Dominic SalvadorNo ratings yet

- Dot 65841 DS1Document234 pagesDot 65841 DS1soghraNo ratings yet

- ChecklistDocument1 pageChecklistManahil AftabNo ratings yet

- Ehs Hse PlanDocument50 pagesEhs Hse Planjithin shankarNo ratings yet

- Brick Manufacturing ProcessDocument17 pagesBrick Manufacturing Processprahladagarwal100% (3)

- PLDT StramaDocument44 pagesPLDT Stramawilhelmina romanNo ratings yet

- Form 57ADocument4 pagesForm 57AMiguel TancangcoNo ratings yet

- Your TM Bill: Page 1 of 5 Level 51, Menara TM, 50672 Kuala Lumpur ST ID: W10-1808-31001554Document5 pagesYour TM Bill: Page 1 of 5 Level 51, Menara TM, 50672 Kuala Lumpur ST ID: W10-1808-31001554Hazwani HusliNo ratings yet