Download as docx, pdf, or txt

You might also like

- 20 Pip ChallangeDocument3 pages20 Pip ChallangeNITISH KAMADIYA100% (1)

- Derivatives Project MIHIRDocument14 pagesDerivatives Project MIHIRYogesh KambleNo ratings yet

- SWING TRADING OPTIONS: Maximizing Profits with Short-Term Option Strategies (2024 Guide for Beginners)From EverandSWING TRADING OPTIONS: Maximizing Profits with Short-Term Option Strategies (2024 Guide for Beginners)No ratings yet

- Dividend Yield: RecapitalisationDocument6 pagesDividend Yield: RecapitalisationArun NadarNo ratings yet

- Derivatives 101Document30 pagesDerivatives 101sv798dctq9No ratings yet

- Study Notes On DerivativesDocument13 pagesStudy Notes On DerivativesAbrar Ahmed100% (2)

- Derivatives ManagementDocument13 pagesDerivatives ManagementMaharajascollege KottayamNo ratings yet

- Project topic:-TYPES OF OPTIONDocument17 pagesProject topic:-TYPES OF OPTIONShreya JoshiNo ratings yet

- Notes F.D. Unit - 3Document14 pagesNotes F.D. Unit - 3kamya saxenaNo ratings yet

- Options - FinalDocument12 pagesOptions - FinalNa Ri TaNo ratings yet

- Options Trading For Beginners: Tips, Formulas and Strategies For Traders to Make Money with OptionsFrom EverandOptions Trading For Beginners: Tips, Formulas and Strategies For Traders to Make Money with OptionsNo ratings yet

- Financial DerivativesDocument13 pagesFinancial DerivativesVasugi KumarNo ratings yet

- What Are DerivativesDocument11 pagesWhat Are DerivativesJayash KaushalNo ratings yet

- Greeks: Type Delta Value Profits When..Document6 pagesGreeks: Type Delta Value Profits When..Anurag SinghNo ratings yet

- Derivatives & OptionsDocument30 pagesDerivatives & OptionsakshastarNo ratings yet

- What Is An Option?: Key TakeawaysDocument7 pagesWhat Is An Option?: Key Takeawaysramyatan SinghNo ratings yet

- Financial Engineering & Risk Management: Unit - VDocument16 pagesFinancial Engineering & Risk Management: Unit - VPrakash ChoudharyNo ratings yet

- Learning About Trading PlatformDocument8 pagesLearning About Trading PlatformGuan ChuangNo ratings yet

- Project 5.3 Option MarketDocument22 pagesProject 5.3 Option MarketKavita KohliNo ratings yet

- Topics: 1. DerivativesDocument9 pagesTopics: 1. Derivativespankaj baviskarNo ratings yet

- Stock Options: Stock OptionsDocument9 pagesStock Options: Stock Optionscreative dailyNo ratings yet

- Options 101 The Ultimate Beginners Guide To OptionsDocument47 pagesOptions 101 The Ultimate Beginners Guide To OptionsChicobiNo ratings yet

- Basic Options TradingDocument38 pagesBasic Options TradingKévin EonNo ratings yet

- Financial DerivativesDocument4 pagesFinancial DerivativesDanielNo ratings yet

- Chapter-3 Options: Meaning of Options-Options Are Financial Derivatives That Give Buyers TheDocument15 pagesChapter-3 Options: Meaning of Options-Options Are Financial Derivatives That Give Buyers TheRaj KumarNo ratings yet

- Terminologies: DEMAT AccountDocument5 pagesTerminologies: DEMAT Accountdinesh kumarNo ratings yet

- Forex - : Corporate Hedge ToolsDocument15 pagesForex - : Corporate Hedge ToolsJai GuptaNo ratings yet

- PresentationDocument6 pagesPresentationcreative dailyNo ratings yet

- Answers To Chapter 10 QuestionsDocument10 pagesAnswers To Chapter 10 QuestionsMoNo ratings yet

- Process Assets Mutual Fund Monitoring Appropriate Investments Funds AccordinglyDocument6 pagesProcess Assets Mutual Fund Monitoring Appropriate Investments Funds Accordinglytriptim_3No ratings yet

- Derivatives FinalDocument37 pagesDerivatives FinalmannashkshitigarNo ratings yet

- Futures in Stock Market Definition, Example, and How To TradeDocument4 pagesFutures in Stock Market Definition, Example, and How To TradeACC200 MNo ratings yet

- Derivatives: Types of Derivative ContractsDocument20 pagesDerivatives: Types of Derivative ContractsXandarnova corpsNo ratings yet

- Marketable SecuritiesDocument64 pagesMarketable Securitiessrajan singhNo ratings yet

- Explain What A Preemptive Rights Offering Is With Example and Why A Standby Underwriting Arrangements May Be Needed. Also, Define Subscription PriceDocument4 pagesExplain What A Preemptive Rights Offering Is With Example and Why A Standby Underwriting Arrangements May Be Needed. Also, Define Subscription PriceuzairNo ratings yet

- Derivatives: 1. Before Reading The Text, Try Answering The Following QuestionsDocument6 pagesDerivatives: 1. Before Reading The Text, Try Answering The Following QuestionsAdina MihaelaNo ratings yet

- CC CC C C CCCCC CC: CCCCCCCCCCCCCCCCCCCCCCCCCCC C C C CC C CC CDocument10 pagesCC CC C C CCCCC CC: CCCCCCCCCCCCCCCCCCCCCCCCCCC C C C CC C CC CberatjusufiNo ratings yet

- Futures & OptionsDocument15 pagesFutures & Optionsagt0062No ratings yet

- Option Pricing (FD)Document3 pagesOption Pricing (FD)Shrestha VarshneyNo ratings yet

- Exotic Options Workbook and Ref MaterialDocument32 pagesExotic Options Workbook and Ref MaterialKINGER4715No ratings yet

- DerivativesDocument20 pagesDerivativesShruti MhatreNo ratings yet

- Foreign Exchange OptionsDocument7 pagesForeign Exchange OptionstinotendacarltonNo ratings yet

- We Care For You - Please Check Before You InvestDocument21 pagesWe Care For You - Please Check Before You InvestVishnupriya VinothkumarNo ratings yet

- Chapter 4 Sent DRMDocument41 pagesChapter 4 Sent DRMSarvar PathanNo ratings yet

- The Strategic Options Trader: A Complete Guide to Getting Started and Making Money with Stock OptionsFrom EverandThe Strategic Options Trader: A Complete Guide to Getting Started and Making Money with Stock OptionsNo ratings yet

- FD - Unit - III OptionsDocument11 pagesFD - Unit - III OptionspulpsenseNo ratings yet

- Foreign Currency Derivatives and Swaps: QuestionsDocument6 pagesForeign Currency Derivatives and Swaps: QuestionsCarl AzizNo ratings yet

- FMI Unit 5Document11 pagesFMI Unit 5Debajit DasNo ratings yet

- OptionsDocument11 pagesOptionsapi-3770121No ratings yet

- OptionsDocument4 pagesOptionsIsaac Alexis RiveraNo ratings yet

- Given Below Are The Types of Orders Which Are Used For Buying and Selling of SharesDocument15 pagesGiven Below Are The Types of Orders Which Are Used For Buying and Selling of Shareshai_sekhNo ratings yet

- Handz University: Trading OptionsDocument44 pagesHandz University: Trading OptionsAman JainNo ratings yet

- Derivatives: Presented by Jeetendra Singh ROLL NODocument23 pagesDerivatives: Presented by Jeetendra Singh ROLL NOgameplay84No ratings yet

- A Study On Investors Preference of Commodity Markets With Special Reference To Share KhanDocument98 pagesA Study On Investors Preference of Commodity Markets With Special Reference To Share KhanAnu Joseph100% (1)

- Options, Warrants & SwapsDocument9 pagesOptions, Warrants & SwapsSergio CastroNo ratings yet

- What Are Options?: Here Is How I Define OptionDocument10 pagesWhat Are Options?: Here Is How I Define OptionAkshay SinghNo ratings yet

- Optiontradingbook PDFDocument18 pagesOptiontradingbook PDFdonhankietNo ratings yet

- OptionsDocument24 pagesOptionsromey4321No ratings yet

- Options Trading: Invest in Stock Markets and Start Making Profit Using the Ultimate Strategies.From EverandOptions Trading: Invest in Stock Markets and Start Making Profit Using the Ultimate Strategies.No ratings yet

- DunnaDocument69 pagesDunnaYanugonda ThulasinathNo ratings yet

- Maruti Suzuki Financial ModellingDocument8 pagesMaruti Suzuki Financial ModellingPooja AdhikariNo ratings yet

- M&A Targets in Asia - Worldwide Brewing CoDocument2 pagesM&A Targets in Asia - Worldwide Brewing CoPooja AdhikariNo ratings yet

- Functional Specialisation Project A-24Document44 pagesFunctional Specialisation Project A-24Pooja Adhikari0% (1)

- Pharmacy Model - DTDocument4 pagesPharmacy Model - DTPooja AdhikariNo ratings yet

- Mayuri Bhogle - Black BookDocument44 pagesMayuri Bhogle - Black BookPooja AdhikariNo ratings yet

- Cab Service ModelDocument2 pagesCab Service ModelPooja AdhikariNo ratings yet

- International Business EnvironmentMCQsDocument18 pagesInternational Business EnvironmentMCQsPooja AdhikariNo ratings yet

- Blackbook Project On Mutual FundsDocument88 pagesBlackbook Project On Mutual FundsPooja Adhikari100% (2)

- A Study of Health Insurance Sector in India.Document45 pagesA Study of Health Insurance Sector in India.Pooja Adhikari100% (1)

- MMS Finance A01 Pooja AdhikariDocument11 pagesMMS Finance A01 Pooja AdhikariPooja AdhikariNo ratings yet

- By Pooja Adhikari (A01) Mayuri Bhogle (A12) Rachna Kukreja (A52)Document13 pagesBy Pooja Adhikari (A01) Mayuri Bhogle (A12) Rachna Kukreja (A52)Pooja AdhikariNo ratings yet

- Advantages:: Accounting Records. It Is A Means To Ensure That Cost Accounting Records Are inDocument4 pagesAdvantages:: Accounting Records. It Is A Means To Ensure That Cost Accounting Records Are inPooja AdhikariNo ratings yet

- A Summer Project Report On: "Comparative Study of Mutual Funds in India"Document55 pagesA Summer Project Report On: "Comparative Study of Mutual Funds in India"Pooja AdhikariNo ratings yet

- Comparative Study On CustomerDocument10 pagesComparative Study On CustomerPooja AdhikariNo ratings yet

- EquityDocument9 pagesEquityPooja AdhikariNo ratings yet

- NISMAOLDocument4 pagesNISMAOLPooja AdhikariNo ratings yet

- A Comparative Study of Customer Perception Toward E-Banking Services Provided by Selected Private & Public Sector Bank in IndiaDocument5 pagesA Comparative Study of Customer Perception Toward E-Banking Services Provided by Selected Private & Public Sector Bank in IndiaPooja AdhikariNo ratings yet

- By Pooja Adhikari (A1)Document11 pagesBy Pooja Adhikari (A1)Pooja AdhikariNo ratings yet

- A STUDY On RISK and Returns in Mutual FundsDocument3 pagesA STUDY On RISK and Returns in Mutual FundsPooja AdhikariNo ratings yet

- 1..research Paper-FebDocument18 pages1..research Paper-FebPooja AdhikariNo ratings yet

- Subic Power Corp V CIR (CTA 6059, May 8 2003)Document16 pagesSubic Power Corp V CIR (CTA 6059, May 8 2003)Firenze PHNo ratings yet

- Story of A Stock Market Legend: Radhakishan DamaniDocument6 pagesStory of A Stock Market Legend: Radhakishan Damaniraj78krNo ratings yet

- MA. Course Outlines (Fresh)Document23 pagesMA. Course Outlines (Fresh)Fakhar FarooqNo ratings yet

- Pay Slip AugDocument1 pagePay Slip Augvictor.savioNo ratings yet

- Chapter 18Document24 pagesChapter 18Jec AlmarzaNo ratings yet

- LRN Format - BRDocument2 pagesLRN Format - BRADR LAW FIRM CHENNAINo ratings yet

- MSIG Motor Plus Insurance BrochureDocument24 pagesMSIG Motor Plus Insurance BrochureTai AndyNo ratings yet

- Barclays POINT BrochureDocument6 pagesBarclays POINT BrochureQilong ZhangNo ratings yet

- Falanx Interim ResultsDocument12 pagesFalanx Interim Resultsmontegue.sykesNo ratings yet

- G9's Project Overview Sem 2Document2 pagesG9's Project Overview Sem 2Jenny NguyenNo ratings yet

- Account Statement - 2022 10 01 - 2022 10 13Document1 pageAccount Statement - 2022 10 01 - 2022 10 13Gary EcclesNo ratings yet

- Harrod's Sporting GoodsDocument17 pagesHarrod's Sporting GoodsElisabete PadilhaNo ratings yet

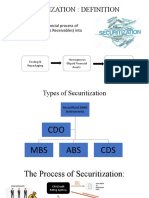

- SECURITIZATIONDocument5 pagesSECURITIZATIONASHISH KUMARNo ratings yet

- Residential StatusDocument8 pagesResidential StatusUthra PandianNo ratings yet

- Credit Schemes in HDFC, Nizamabad: Project Report Submitted To Jawaharlal Nehru Technological University, HyderabadDocument40 pagesCredit Schemes in HDFC, Nizamabad: Project Report Submitted To Jawaharlal Nehru Technological University, HyderabadBnaren NarenNo ratings yet

- Chapter 3 National Income Test BankDocument44 pagesChapter 3 National Income Test BankmchlbahaaNo ratings yet

- MCM Tutorial 2Document3 pagesMCM Tutorial 2SHU WAN TEHNo ratings yet

- Financial Reporting Assignment 1Document3 pagesFinancial Reporting Assignment 1Shu HuiNo ratings yet

- Course Project1 InstructionsDocument4 pagesCourse Project1 InstructionsEnock RutoNo ratings yet

- 5495 15112023090202 UnlockedDocument12 pages5495 15112023090202 Unlockedabhichaudhary3625No ratings yet

- Esma35!43!1410 Mifid II Contact Point Information For NcasDocument63 pagesEsma35!43!1410 Mifid II Contact Point Information For NcasrjxNo ratings yet

- Midland Energy Resources Inc.: Andrew Picone Will Mcdermott Taylor Appel Liam JoyDocument13 pagesMidland Energy Resources Inc.: Andrew Picone Will Mcdermott Taylor Appel Liam JoymariliamonfardineNo ratings yet

- Regional Sales Manager Client Relationship Expert in Denver CO Resume Cynthia ChandlerDocument2 pagesRegional Sales Manager Client Relationship Expert in Denver CO Resume Cynthia ChandlerCynthia ChandlerNo ratings yet

- Chapter 6Document10 pagesChapter 6Moti BekeleNo ratings yet

- Chapter 6Document24 pagesChapter 6Rubén ZúñigaNo ratings yet

- Almeda vs. CADocument7 pagesAlmeda vs. CAAnonymous oDPxEkdNo ratings yet

- The Austerity Delusion (Krugman)Document11 pagesThe Austerity Delusion (Krugman)phdpolitics1No ratings yet

- Retail Capital Gain Based Case Study 1Document8 pagesRetail Capital Gain Based Case Study 1KirankumarNo ratings yet

- Vinacafe Bien Hoa Final ReportDocument24 pagesVinacafe Bien Hoa Final ReportQuang NguyenNo ratings yet