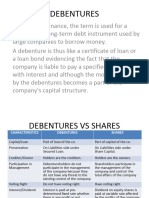

Issue of Debentures (Key-Terms)

Issue of Debentures (Key-Terms)

You might also like

- Types of DebenturesDocument9 pagesTypes of DebentureshitekshaNo ratings yet

- Company Accounts-Issue of Debentures: Meaning of Key Terms Used in The ChapterDocument9 pagesCompany Accounts-Issue of Debentures: Meaning of Key Terms Used in The ChapterKanakpreetNo ratings yet

- (Issue) Key Terms and Chapter Summary-8Document2 pages(Issue) Key Terms and Chapter Summary-8Gyro SplashNo ratings yet

- Issue and Redemption of DebenturesDocument78 pagesIssue and Redemption of DebenturesApollo Institute of Hospital Administration50% (2)

- Leac 202Document69 pagesLeac 202Aditya Singh RajputNo ratings yet

- Leac202 DebenturesDocument75 pagesLeac202 DebenturesMidhunidharNo ratings yet

- Debenture Accounting PDFDocument75 pagesDebenture Accounting PDFMuhammad Faran KhanNo ratings yet

- Redemption of Debentures PDFDocument22 pagesRedemption of Debentures PDFVikas MandloiNo ratings yet

- Chapter-2 Issue of Debentures BY: G Arun Kumar Mcom Mba Net Asst Professor in Commerce GDC Men SrikakulamDocument39 pagesChapter-2 Issue of Debentures BY: G Arun Kumar Mcom Mba Net Asst Professor in Commerce GDC Men SrikakulamgeddadaarunNo ratings yet

- 67188bos54090 Cp10u3Document31 pages67188bos54090 Cp10u3Pawan TalrejaNo ratings yet

- Issue of DebenturesDocument39 pagesIssue of Debenturesyashwanth86No ratings yet

- Leac 202Document75 pagesLeac 202Ias Aspirant AbhiNo ratings yet

- ChapterDocument78 pagesChaptershaannivasNo ratings yet

- Issue of DebentureDocument17 pagesIssue of DebentureCma Vikas RajpalaniNo ratings yet

- DebenturesDocument6 pagesDebenturesSrishti Goel100% (1)

- Chapter 7sDocument96 pagesChapter 7ssgangwar2005sgNo ratings yet

- Company Acc - Issue of Debentures @CA - Study - NotesDocument9 pagesCompany Acc - Issue of Debentures @CA - Study - Notesbhawanar3950No ratings yet

- Issue of Debentures: UNIT - 3Document31 pagesIssue of Debentures: UNIT - 3Hansika ChawlaNo ratings yet

- 12 AccountancyDocument7 pages12 AccountancyAlim AbbasNo ratings yet

- Meaning of DebenturesDocument13 pagesMeaning of DebenturesAmal DevadasNo ratings yet

- Accountancy PDF 1Document16 pagesAccountancy PDF 1najeelmk3No ratings yet

- Debentures: Fundamentals of AccountingDocument63 pagesDebentures: Fundamentals of AccountingSangam NeupaneNo ratings yet

- Meaning and DefinitionDocument8 pagesMeaning and DefinitionSuit ChetriNo ratings yet

- Issue of Debentures Redemption of Debentures UnderwrtingDocument47 pagesIssue of Debentures Redemption of Debentures UnderwrtingKeshav PantNo ratings yet

- DEBENTURESDocument6 pagesDEBENTURESsuraj singh officialNo ratings yet

- Real Options A New Way To ThinkDocument20 pagesReal Options A New Way To ThinkAjay TahilramaniNo ratings yet

- Chapter-8 Issue of Debentures: Debenture: The Word Debenture' Has Been Derived From A Latin Word Debere' WhichDocument8 pagesChapter-8 Issue of Debentures: Debenture: The Word Debenture' Has Been Derived From A Latin Word Debere' Whichramandeep kaurNo ratings yet

- Issue of DebenturesDocument23 pagesIssue of Debenturesramandeep kaurNo ratings yet

- Company Acc Unit 3Document39 pagesCompany Acc Unit 3Megha DevanpalliNo ratings yet

- Borrowing Powers (Debentures and Charges) : Dr. Bharat G. KauraniDocument25 pagesBorrowing Powers (Debentures and Charges) : Dr. Bharat G. Kauranishubham kumarNo ratings yet

- Unit 3: Issue of Debentures: Learning OutcomesDocument30 pagesUnit 3: Issue of Debentures: Learning Outcomesashish malhotraNo ratings yet

- 19 DebenturesDocument2 pages19 DebenturesTEXTILIONSNo ratings yet

- Corporate and Company AccountsDocument58 pagesCorporate and Company Accountsdhiyarj10No ratings yet

- Business Finance Project - DebenturesDocument16 pagesBusiness Finance Project - DebenturesMuhammad TalhaNo ratings yet

- Debentures: Sowmya.L 2018258034Document14 pagesDebentures: Sowmya.L 2018258034mba tourismNo ratings yet

- Issue of Debentures Redemption of Debentures UnderwrtingDocument47 pagesIssue of Debentures Redemption of Debentures UnderwrtingRAMA ChauhanNo ratings yet

- Creditorship Securities or DebenturesDocument6 pagesCreditorship Securities or DebenturesAditya Sawant100% (1)

- DebenturesDocument4 pagesDebentureschandni.workbackupNo ratings yet

- DebenturesDocument26 pagesDebenturesSamiksha PawarNo ratings yet

- debenturesDocument11 pagesdebenturesizahharis3No ratings yet

- Attributes: Corporate Finance InstrumentDocument2 pagesAttributes: Corporate Finance InstrumentShayan ZafarNo ratings yet

- Issue and Kinds of Debenture CompanyDocument10 pagesIssue and Kinds of Debenture CompanyHemanta PahariNo ratings yet

- Debentures 130314034401 Phpapp02Document36 pagesDebentures 130314034401 Phpapp02nemewep527No ratings yet

- DEBENTURESDocument9 pagesDEBENTURESKajal RaiNo ratings yet

- CL Topic 6Document11 pagesCL Topic 6magdawaks46No ratings yet

- Definition, Type and Issue of Debentures: New Inspiron™ 14R LaptopsDocument3 pagesDefinition, Type and Issue of Debentures: New Inspiron™ 14R LaptopsGause KaniNo ratings yet

- Debentures and ChargesDocument4 pagesDebentures and Chargesrobertkarabo.jNo ratings yet

- 4 DebenturesDocument16 pages4 DebenturesSakshiNo ratings yet

- Debenture PrintDocument3 pagesDebenture PrintSuman DhunganaNo ratings yet

- Project Report On "Debentures"Document14 pagesProject Report On "Debentures"Imran Shaikh88% (8)

- 3 June Company Law CornerDocument13 pages3 June Company Law CornerVarun ShahNo ratings yet

- Debenture Vs Shares-2Document19 pagesDebenture Vs Shares-2nemewep527No ratings yet

- DebenturesDocument6 pagesDebenturesSenelwa AnayaNo ratings yet

- DebenturesDocument6 pagesDebenturesSenelwa AnayaNo ratings yet

- Dividends & Debentures.Document10 pagesDividends & Debentures.amisha dhingraNo ratings yet

- Acc DebenturesDocument12 pagesAcc DebenturesDRISYANo ratings yet

- DebentureDocument9 pagesDebenturedrsurendrakumarNo ratings yet

- Unit 7 - Debentures and ChargesDocument2 pagesUnit 7 - Debentures and Chargesgillian soonNo ratings yet

- Tax Free Wealth: Learn the strategies and loopholes of the wealthy on lowering taxes by leveraging Cash Value Life Insurance, 1031 Real Estate Exchanges, 401k & IRA InvestingFrom EverandTax Free Wealth: Learn the strategies and loopholes of the wealthy on lowering taxes by leveraging Cash Value Life Insurance, 1031 Real Estate Exchanges, 401k & IRA InvestingNo ratings yet

- AQM No. IMO Norte-2021-003 - 501 LFPs - Payments Thru ReimbursementsDocument3 pagesAQM No. IMO Norte-2021-003 - 501 LFPs - Payments Thru ReimbursementsGee YeeNo ratings yet

- What Is 13th Month PayDocument1 pageWhat Is 13th Month PayKatKatNo ratings yet

- Grade 10 Unit 1 EntrepDocument33 pagesGrade 10 Unit 1 EntrepIsaac Buan100% (2)

- MBA630 Price-Barret Minor Project 1Document21 pagesMBA630 Price-Barret Minor Project 1sylvia priceNo ratings yet

- Market Data Book 2015 ProspectusDocument6 pagesMarket Data Book 2015 ProspectusPanosMitsopoulosNo ratings yet

- India Strategy - InCred - 28 AugDocument37 pagesIndia Strategy - InCred - 28 AugDeepul WadhwaNo ratings yet

- Airbnb CaseDocument12 pagesAirbnb CaseEslam SamyNo ratings yet

- Economics WordsearchDocument1 pageEconomics WordsearchSandy SaddlerNo ratings yet

- Patagonia, Inc.:: A Company AnalysisDocument5 pagesPatagonia, Inc.:: A Company AnalysisRsn786No ratings yet

- Rift Valley Universty Chiro CampusDocument37 pagesRift Valley Universty Chiro CampusBobasa S AhmedNo ratings yet

- Aca Labor Digests MidtermsDocument195 pagesAca Labor Digests MidtermsPaul Tisoy100% (2)

- CH 12Document45 pagesCH 12Pulkit AggarwalNo ratings yet

- AS-Solved Past Paper Business 9609 P1 2023-2022Document51 pagesAS-Solved Past Paper Business 9609 P1 2023-2022TheOfficialTitaniumNo ratings yet

- Strategic Management-Module-1Document44 pagesStrategic Management-Module-1Mahesh RangaswamyNo ratings yet

- Credit Terms Newest FormDocument1 pageCredit Terms Newest FormPhú Nguyễn HoàngNo ratings yet

- Ekt Trade & Investment PLC Showroom Customer Satisfaction Survey FormDocument3 pagesEkt Trade & Investment PLC Showroom Customer Satisfaction Survey FormSisay TesfayeNo ratings yet

- Part 2-1 English For Finance & Banking - DR DjenouhatDocument25 pagesPart 2-1 English For Finance & Banking - DR DjenouhatKawthar LebibNo ratings yet

- 500 Banking Awarenes One LinerDocument35 pages500 Banking Awarenes One LinerLatta SakthyyNo ratings yet

- Role of e Choupal in Rural MarketingDocument72 pagesRole of e Choupal in Rural MarketingAkshay MadharNo ratings yet

- (BSI) BS 25999-1 Code of Practice For Business Continuity ManagementDocument39 pages(BSI) BS 25999-1 Code of Practice For Business Continuity Managementkhaledsyria100% (1)

- Energy Industry Team To Launch Crypto Mining FundDocument3 pagesEnergy Industry Team To Launch Crypto Mining FundPR.comNo ratings yet

- Quiz 1 and 2Document14 pagesQuiz 1 and 2Nichole TumulakNo ratings yet

- Pakistan Problems of Governance PDFDocument130 pagesPakistan Problems of Governance PDFInam ur RehmanNo ratings yet

- Distressed Debt Investing - Wisdom From Seth Klarman - Part 1Document5 pagesDistressed Debt Investing - Wisdom From Seth Klarman - Part 1pjs15100% (1)

- Accounting As The Language of BusinessDocument2 pagesAccounting As The Language of BusinessjuliahuiniNo ratings yet

- Exam Content Manual PreviewDocument6 pagesExam Content Manual PreviewThu Giang DuongNo ratings yet

- Master Your FinancesDocument15 pagesMaster Your FinancesBrendan GirdwoodNo ratings yet

- F2 Syllabus Overview: Created By: Global CGMA University and Academic Center of ExcellenceDocument93 pagesF2 Syllabus Overview: Created By: Global CGMA University and Academic Center of Excellencesike1977No ratings yet

- Ae113: Midterm Quiz 3 Name: Cherie Lyn Ananayo ID: 20-2007-496 SUBJECT & SCHEDULE: AE113 WSAT 7:30-11:30 SCORE: - DATE: 29/05/21Document2 pagesAe113: Midterm Quiz 3 Name: Cherie Lyn Ananayo ID: 20-2007-496 SUBJECT & SCHEDULE: AE113 WSAT 7:30-11:30 SCORE: - DATE: 29/05/21Cherie Soriano AnanayoNo ratings yet

- Chapter-1 (To Industry, Company & Topic)Document69 pagesChapter-1 (To Industry, Company & Topic)pmcmbharat264No ratings yet

Download as pdf or txt

You might also like

- Types of DebenturesDocument9 pagesTypes of DebentureshitekshaNo ratings yet

- Company Accounts-Issue of Debentures: Meaning of Key Terms Used in The ChapterDocument9 pagesCompany Accounts-Issue of Debentures: Meaning of Key Terms Used in The ChapterKanakpreetNo ratings yet

- (Issue) Key Terms and Chapter Summary-8Document2 pages(Issue) Key Terms and Chapter Summary-8Gyro SplashNo ratings yet

- Issue and Redemption of DebenturesDocument78 pagesIssue and Redemption of DebenturesApollo Institute of Hospital Administration50% (2)

- Leac 202Document69 pagesLeac 202Aditya Singh RajputNo ratings yet

- Leac202 DebenturesDocument75 pagesLeac202 DebenturesMidhunidharNo ratings yet

- Debenture Accounting PDFDocument75 pagesDebenture Accounting PDFMuhammad Faran KhanNo ratings yet

- Redemption of Debentures PDFDocument22 pagesRedemption of Debentures PDFVikas MandloiNo ratings yet

- Chapter-2 Issue of Debentures BY: G Arun Kumar Mcom Mba Net Asst Professor in Commerce GDC Men SrikakulamDocument39 pagesChapter-2 Issue of Debentures BY: G Arun Kumar Mcom Mba Net Asst Professor in Commerce GDC Men SrikakulamgeddadaarunNo ratings yet

- 67188bos54090 Cp10u3Document31 pages67188bos54090 Cp10u3Pawan TalrejaNo ratings yet

- Issue of DebenturesDocument39 pagesIssue of Debenturesyashwanth86No ratings yet

- Leac 202Document75 pagesLeac 202Ias Aspirant AbhiNo ratings yet

- ChapterDocument78 pagesChaptershaannivasNo ratings yet

- Issue of DebentureDocument17 pagesIssue of DebentureCma Vikas RajpalaniNo ratings yet

- DebenturesDocument6 pagesDebenturesSrishti Goel100% (1)

- Chapter 7sDocument96 pagesChapter 7ssgangwar2005sgNo ratings yet

- Company Acc - Issue of Debentures @CA - Study - NotesDocument9 pagesCompany Acc - Issue of Debentures @CA - Study - Notesbhawanar3950No ratings yet

- Issue of Debentures: UNIT - 3Document31 pagesIssue of Debentures: UNIT - 3Hansika ChawlaNo ratings yet

- 12 AccountancyDocument7 pages12 AccountancyAlim AbbasNo ratings yet

- Meaning of DebenturesDocument13 pagesMeaning of DebenturesAmal DevadasNo ratings yet

- Accountancy PDF 1Document16 pagesAccountancy PDF 1najeelmk3No ratings yet

- Debentures: Fundamentals of AccountingDocument63 pagesDebentures: Fundamentals of AccountingSangam NeupaneNo ratings yet

- Meaning and DefinitionDocument8 pagesMeaning and DefinitionSuit ChetriNo ratings yet

- Issue of Debentures Redemption of Debentures UnderwrtingDocument47 pagesIssue of Debentures Redemption of Debentures UnderwrtingKeshav PantNo ratings yet

- DEBENTURESDocument6 pagesDEBENTURESsuraj singh officialNo ratings yet

- Real Options A New Way To ThinkDocument20 pagesReal Options A New Way To ThinkAjay TahilramaniNo ratings yet

- Chapter-8 Issue of Debentures: Debenture: The Word Debenture' Has Been Derived From A Latin Word Debere' WhichDocument8 pagesChapter-8 Issue of Debentures: Debenture: The Word Debenture' Has Been Derived From A Latin Word Debere' Whichramandeep kaurNo ratings yet

- Issue of DebenturesDocument23 pagesIssue of Debenturesramandeep kaurNo ratings yet

- Company Acc Unit 3Document39 pagesCompany Acc Unit 3Megha DevanpalliNo ratings yet

- Borrowing Powers (Debentures and Charges) : Dr. Bharat G. KauraniDocument25 pagesBorrowing Powers (Debentures and Charges) : Dr. Bharat G. Kauranishubham kumarNo ratings yet

- Unit 3: Issue of Debentures: Learning OutcomesDocument30 pagesUnit 3: Issue of Debentures: Learning Outcomesashish malhotraNo ratings yet

- 19 DebenturesDocument2 pages19 DebenturesTEXTILIONSNo ratings yet

- Corporate and Company AccountsDocument58 pagesCorporate and Company Accountsdhiyarj10No ratings yet

- Business Finance Project - DebenturesDocument16 pagesBusiness Finance Project - DebenturesMuhammad TalhaNo ratings yet

- Debentures: Sowmya.L 2018258034Document14 pagesDebentures: Sowmya.L 2018258034mba tourismNo ratings yet

- Issue of Debentures Redemption of Debentures UnderwrtingDocument47 pagesIssue of Debentures Redemption of Debentures UnderwrtingRAMA ChauhanNo ratings yet

- Creditorship Securities or DebenturesDocument6 pagesCreditorship Securities or DebenturesAditya Sawant100% (1)

- DebenturesDocument4 pagesDebentureschandni.workbackupNo ratings yet

- DebenturesDocument26 pagesDebenturesSamiksha PawarNo ratings yet

- debenturesDocument11 pagesdebenturesizahharis3No ratings yet

- Attributes: Corporate Finance InstrumentDocument2 pagesAttributes: Corporate Finance InstrumentShayan ZafarNo ratings yet

- Issue and Kinds of Debenture CompanyDocument10 pagesIssue and Kinds of Debenture CompanyHemanta PahariNo ratings yet

- Debentures 130314034401 Phpapp02Document36 pagesDebentures 130314034401 Phpapp02nemewep527No ratings yet

- DEBENTURESDocument9 pagesDEBENTURESKajal RaiNo ratings yet

- CL Topic 6Document11 pagesCL Topic 6magdawaks46No ratings yet

- Definition, Type and Issue of Debentures: New Inspiron™ 14R LaptopsDocument3 pagesDefinition, Type and Issue of Debentures: New Inspiron™ 14R LaptopsGause KaniNo ratings yet

- Debentures and ChargesDocument4 pagesDebentures and Chargesrobertkarabo.jNo ratings yet

- 4 DebenturesDocument16 pages4 DebenturesSakshiNo ratings yet

- Debenture PrintDocument3 pagesDebenture PrintSuman DhunganaNo ratings yet

- Project Report On "Debentures"Document14 pagesProject Report On "Debentures"Imran Shaikh88% (8)

- 3 June Company Law CornerDocument13 pages3 June Company Law CornerVarun ShahNo ratings yet

- Debenture Vs Shares-2Document19 pagesDebenture Vs Shares-2nemewep527No ratings yet

- DebenturesDocument6 pagesDebenturesSenelwa AnayaNo ratings yet

- DebenturesDocument6 pagesDebenturesSenelwa AnayaNo ratings yet

- Dividends & Debentures.Document10 pagesDividends & Debentures.amisha dhingraNo ratings yet

- Acc DebenturesDocument12 pagesAcc DebenturesDRISYANo ratings yet

- DebentureDocument9 pagesDebenturedrsurendrakumarNo ratings yet

- Unit 7 - Debentures and ChargesDocument2 pagesUnit 7 - Debentures and Chargesgillian soonNo ratings yet

- Tax Free Wealth: Learn the strategies and loopholes of the wealthy on lowering taxes by leveraging Cash Value Life Insurance, 1031 Real Estate Exchanges, 401k & IRA InvestingFrom EverandTax Free Wealth: Learn the strategies and loopholes of the wealthy on lowering taxes by leveraging Cash Value Life Insurance, 1031 Real Estate Exchanges, 401k & IRA InvestingNo ratings yet

- AQM No. IMO Norte-2021-003 - 501 LFPs - Payments Thru ReimbursementsDocument3 pagesAQM No. IMO Norte-2021-003 - 501 LFPs - Payments Thru ReimbursementsGee YeeNo ratings yet

- What Is 13th Month PayDocument1 pageWhat Is 13th Month PayKatKatNo ratings yet

- Grade 10 Unit 1 EntrepDocument33 pagesGrade 10 Unit 1 EntrepIsaac Buan100% (2)

- MBA630 Price-Barret Minor Project 1Document21 pagesMBA630 Price-Barret Minor Project 1sylvia priceNo ratings yet

- Market Data Book 2015 ProspectusDocument6 pagesMarket Data Book 2015 ProspectusPanosMitsopoulosNo ratings yet

- India Strategy - InCred - 28 AugDocument37 pagesIndia Strategy - InCred - 28 AugDeepul WadhwaNo ratings yet

- Airbnb CaseDocument12 pagesAirbnb CaseEslam SamyNo ratings yet

- Economics WordsearchDocument1 pageEconomics WordsearchSandy SaddlerNo ratings yet

- Patagonia, Inc.:: A Company AnalysisDocument5 pagesPatagonia, Inc.:: A Company AnalysisRsn786No ratings yet

- Rift Valley Universty Chiro CampusDocument37 pagesRift Valley Universty Chiro CampusBobasa S AhmedNo ratings yet

- Aca Labor Digests MidtermsDocument195 pagesAca Labor Digests MidtermsPaul Tisoy100% (2)

- CH 12Document45 pagesCH 12Pulkit AggarwalNo ratings yet

- AS-Solved Past Paper Business 9609 P1 2023-2022Document51 pagesAS-Solved Past Paper Business 9609 P1 2023-2022TheOfficialTitaniumNo ratings yet

- Strategic Management-Module-1Document44 pagesStrategic Management-Module-1Mahesh RangaswamyNo ratings yet

- Credit Terms Newest FormDocument1 pageCredit Terms Newest FormPhú Nguyễn HoàngNo ratings yet

- Ekt Trade & Investment PLC Showroom Customer Satisfaction Survey FormDocument3 pagesEkt Trade & Investment PLC Showroom Customer Satisfaction Survey FormSisay TesfayeNo ratings yet

- Part 2-1 English For Finance & Banking - DR DjenouhatDocument25 pagesPart 2-1 English For Finance & Banking - DR DjenouhatKawthar LebibNo ratings yet

- 500 Banking Awarenes One LinerDocument35 pages500 Banking Awarenes One LinerLatta SakthyyNo ratings yet

- Role of e Choupal in Rural MarketingDocument72 pagesRole of e Choupal in Rural MarketingAkshay MadharNo ratings yet

- (BSI) BS 25999-1 Code of Practice For Business Continuity ManagementDocument39 pages(BSI) BS 25999-1 Code of Practice For Business Continuity Managementkhaledsyria100% (1)

- Energy Industry Team To Launch Crypto Mining FundDocument3 pagesEnergy Industry Team To Launch Crypto Mining FundPR.comNo ratings yet

- Quiz 1 and 2Document14 pagesQuiz 1 and 2Nichole TumulakNo ratings yet

- Pakistan Problems of Governance PDFDocument130 pagesPakistan Problems of Governance PDFInam ur RehmanNo ratings yet

- Distressed Debt Investing - Wisdom From Seth Klarman - Part 1Document5 pagesDistressed Debt Investing - Wisdom From Seth Klarman - Part 1pjs15100% (1)

- Accounting As The Language of BusinessDocument2 pagesAccounting As The Language of BusinessjuliahuiniNo ratings yet

- Exam Content Manual PreviewDocument6 pagesExam Content Manual PreviewThu Giang DuongNo ratings yet

- Master Your FinancesDocument15 pagesMaster Your FinancesBrendan GirdwoodNo ratings yet

- F2 Syllabus Overview: Created By: Global CGMA University and Academic Center of ExcellenceDocument93 pagesF2 Syllabus Overview: Created By: Global CGMA University and Academic Center of Excellencesike1977No ratings yet

- Ae113: Midterm Quiz 3 Name: Cherie Lyn Ananayo ID: 20-2007-496 SUBJECT & SCHEDULE: AE113 WSAT 7:30-11:30 SCORE: - DATE: 29/05/21Document2 pagesAe113: Midterm Quiz 3 Name: Cherie Lyn Ananayo ID: 20-2007-496 SUBJECT & SCHEDULE: AE113 WSAT 7:30-11:30 SCORE: - DATE: 29/05/21Cherie Soriano AnanayoNo ratings yet

- Chapter-1 (To Industry, Company & Topic)Document69 pagesChapter-1 (To Industry, Company & Topic)pmcmbharat264No ratings yet