Download as docx, pdf, or txt

You might also like

- Hhmi Cell Cycle and Cancer - CompletedDocument3 pagesHhmi Cell Cycle and Cancer - CompletedAbel89% (9)

- Oosterhof FG - Dietrich Bonhoeffer - The Cost of Discipleship PDFDocument8 pagesOosterhof FG - Dietrich Bonhoeffer - The Cost of Discipleship PDFJoshua ChuaNo ratings yet

- Boylan - The Spiritual Life of The PriestDocument63 pagesBoylan - The Spiritual Life of The Priestpablotrollano100% (1)

- Kohinoor 181 11 5851 FacDocument37 pagesKohinoor 181 11 5851 FacSharif KhanNo ratings yet

- P and L PDFDocument2 pagesP and L PDFjigar jainNo ratings yet

- SIP5 7KE85 V07.80 Manual C018-6 en PDFDocument502 pagesSIP5 7KE85 V07.80 Manual C018-6 en PDFDoan Anh TuanNo ratings yet

- Philip Merlan, From Platonism To NeoplatonismDocument267 pagesPhilip Merlan, From Platonism To NeoplatonismAnonymous fgaljTd100% (1)

- Navana CNG Limited IncomeDocument4 pagesNavana CNG Limited IncomeHridoyNo ratings yet

- HCL Technologies: PrintDocument2 pagesHCL Technologies: PrintSachin SinghNo ratings yet

- bajaj prev.5 yrs P&LDocument2 pagesbajaj prev.5 yrs P&Larsoni1999No ratings yet

- New Manoj Grill UdhyogDocument24 pagesNew Manoj Grill UdhyoggpdharanNo ratings yet

- Tata Motors: PrintDocument2 pagesTata Motors: Printprathamesh tawareNo ratings yet

- WiproDocument9 pagesWiprorastehertaNo ratings yet

- Trend AnalysisDocument42 pagesTrend AnalysisMd. Tauhidur Rahman 07-18-45No ratings yet

- PSML 2020-21Document13 pagesPSML 2020-21jjtn4yf4r8No ratings yet

- New ExcelDocument25 pagesNew Excelred8blue8No ratings yet

- Standard-Ceramic-Limited NewDocument10 pagesStandard-Ceramic-Limited NewTahmid ShovonNo ratings yet

- Asian Paints PLDocument2 pagesAsian Paints PLPriyalNo ratings yet

- Capital Contribution: Stockholder TINDocument17 pagesCapital Contribution: Stockholder TINEddie ParazoNo ratings yet

- Answer To The Question No 1 (I) ACI Group of Company Balance Sheet (Vertical Analysis) For The Years Ended June 30, 2019Document4 pagesAnswer To The Question No 1 (I) ACI Group of Company Balance Sheet (Vertical Analysis) For The Years Ended June 30, 2019Estiyak JahanNo ratings yet

- BreakdownDocument2 pagesBreakdownquenguyen9866No ratings yet

- Vodafone Idea Limited: PrintDocument1 pageVodafone Idea Limited: PrintPrakhar KapoorNo ratings yet

- Rak Ceramics: Income StatementDocument27 pagesRak Ceramics: Income StatementRafsan JahangirNo ratings yet

- Reformulated Income Statement of Century Ply: Operating RevenueDocument2 pagesReformulated Income Statement of Century Ply: Operating RevenueBhoomika GuptaNo ratings yet

- J and J Medical ClinicDocument17 pagesJ and J Medical ClinicHarold Kent MendozaNo ratings yet

- FinancialsDocument2 pagesFinancialsSailesh RankaNo ratings yet

- E. Sensitivities and ScenariosDocument3 pagesE. Sensitivities and ScenariosDadangNo ratings yet

- Income Statement of Mahaweli Reach HotelDocument7 pagesIncome Statement of Mahaweli Reach Hotelदेवीना गिरीNo ratings yet

- Company Info - Print FinancialsDocument2 pagesCompany Info - Print FinancialsJoydeep GoraiNo ratings yet

- Clarissa Computation StramaDocument29 pagesClarissa Computation StramaZejkeara ImperialNo ratings yet

- Submitted By: Name: R.Akash PRN: 16020841177 Finance 2016-18 Submitted To: Prof. Pooja GuptaDocument44 pagesSubmitted By: Name: R.Akash PRN: 16020841177 Finance 2016-18 Submitted To: Prof. Pooja Guptaranjana kashyapNo ratings yet

- Pran Group MIS ReportDocument14 pagesPran Group MIS ReportNazer HossainNo ratings yet

- Company Info - Print Financials2Document2 pagesCompany Info - Print Financials2rojaNo ratings yet

- MahindraDocument5 pagesMahindraworkf17hoursformeNo ratings yet

- Beximco PHARMACEUTICALS LTD ISDocument2 pagesBeximco PHARMACEUTICALS LTD ISSuny ChowdhuryNo ratings yet

- Company Info - Print FinancialsDocument2 pagesCompany Info - Print Financialsjayashankar4355No ratings yet

- Eicher Motors Profit and Loss AccountDocument2 pagesEicher Motors Profit and Loss AccountVaishnav Sunil100% (1)

- Thế Giới Di Động 2022Document16 pagesThế Giới Di Động 2022Phạm Thu HằngNo ratings yet

- Hindustan Unilever: PrintDocument2 pagesHindustan Unilever: PrintAbhay Kumar SinghNo ratings yet

- Company Info - Print FinancialsDocument2 pagesCompany Info - Print FinancialsBhawani CreationsNo ratings yet

- Hero Motocorp: PrintDocument2 pagesHero Motocorp: PrintPhuntru PhiNo ratings yet

- Unaudited FS - 2nd QuarterDocument37 pagesUnaudited FS - 2nd Quarterprasenjitpandit4No ratings yet

- UploadDocument83 pagesUploadAli BMSNo ratings yet

- Hindustan Unilever: PrintDocument2 pagesHindustan Unilever: PrintUTSAVNo ratings yet

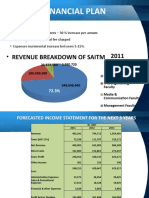

- Financial Plan: - Revenue Breakdown of SaitmDocument6 pagesFinancial Plan: - Revenue Breakdown of SaitmUdeeshan JonasNo ratings yet

- Britannia Industries: PrintDocument2 pagesBritannia Industries: PrintTanmoy BhuniaNo ratings yet

- Profit & Loss PT TCP M Arif Rahman - 2005151018 - Akp-3aDocument1 pageProfit & Loss PT TCP M Arif Rahman - 2005151018 - Akp-3aM Arif RahmanNo ratings yet

- EREGL DCF ModelDocument10 pagesEREGL DCF ModelKevser BozoğluNo ratings yet

- Group Project KHT Fall 20Document23 pagesGroup Project KHT Fall 20SAKIB MD SHAFIUDDINNo ratings yet

- ROIC SpreadsheetDocument8 pagesROIC Spreadsheetveda20No ratings yet

- Verana Exhibit and SchedsDocument45 pagesVerana Exhibit and SchedsPrincess Dianne MaitelNo ratings yet

- Financial Statements Analysis: Arsalan FarooqueDocument31 pagesFinancial Statements Analysis: Arsalan FarooqueMuhib NoharioNo ratings yet

- BA Data BankDocument33 pagesBA Data BanksauravNo ratings yet

- BSBFIM601 Assessment 1: Sales and Profit BudgetsDocument8 pagesBSBFIM601 Assessment 1: Sales and Profit Budgetsprasannareddy9989100% (1)

- Cipla P& LDocument2 pagesCipla P& LNEHA LALNo ratings yet

- Attock Refinery FM Assignment#3Document13 pagesAttock Refinery FM Assignment#3Vishal MalhiNo ratings yet

- Comprehensive IncomeDocument4 pagesComprehensive IncomePrincess EscaranNo ratings yet

- Bajaj Aut1Document2 pagesBajaj Aut1Rinku RajpootNo ratings yet

- CMA CIA 3 YateeDocument38 pagesCMA CIA 3 YateeYATEE TRIVEDI 21111660No ratings yet

- Axis BankDocument14 pagesAxis BankAswini Kumar BhuyanNo ratings yet

- Purcari Lucru IndividualDocument7 pagesPurcari Lucru IndividualLenuța PapucNo ratings yet

- I. Assets: 2018 2019Document7 pagesI. Assets: 2018 2019Kean DeeNo ratings yet

- Asses Income Statement BrightDocument2 pagesAsses Income Statement BrightJoanna JacksonNo ratings yet

- Final Ma Jud Ni FinancialsDocument78 pagesFinal Ma Jud Ni FinancialsMichael A. BerturanNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Executive Summary: Credit SanctioningDocument18 pagesExecutive Summary: Credit SanctioningMd. Tauhidur Rahman 07-18-45No ratings yet

- M. Corporate FinanceDocument62 pagesM. Corporate FinanceMd. Tauhidur Rahman 07-18-45No ratings yet

- Table of Contant: SL No. Particulars Page RefDocument10 pagesTable of Contant: SL No. Particulars Page RefMd. Tauhidur Rahman 07-18-45No ratings yet

- Presentation On Equity Analysis - Fuel - Power - Sectro (Group 6) Final...Document25 pagesPresentation On Equity Analysis - Fuel - Power - Sectro (Group 6) Final...Md. Tauhidur Rahman 07-18-45No ratings yet

- Porter's 5 Forces Model-FinalDocument7 pagesPorter's 5 Forces Model-FinalMd. Tauhidur Rahman 07-18-45No ratings yet

- Square Tex Paramount Tex Envoy Tex: Gordon Growth Model (V)Document50 pagesSquare Tex Paramount Tex Envoy Tex: Gordon Growth Model (V)Md. Tauhidur Rahman 07-18-45No ratings yet

- Presentation On Equity Analysis Part 1 (Group 6)Document4 pagesPresentation On Equity Analysis Part 1 (Group 6)Md. Tauhidur Rahman 07-18-45No ratings yet

- Trend AnalysisDocument42 pagesTrend AnalysisMd. Tauhidur Rahman 07-18-45No ratings yet

- New - Branch Operations-Managing Risks and Cobmat Against Fraud & Forgery (ToT) As On Jan 28, 2015Document140 pagesNew - Branch Operations-Managing Risks and Cobmat Against Fraud & Forgery (ToT) As On Jan 28, 2015Md. Tauhidur Rahman 07-18-45No ratings yet

- Negotiable Instruments: (Law Regarding Cheques, Drafts, . )Document27 pagesNegotiable Instruments: (Law Regarding Cheques, Drafts, . )Md. Tauhidur Rahman 07-18-45No ratings yet

- List of AcronymsDocument10 pagesList of AcronymsMd. Tauhidur Rahman 07-18-45No ratings yet

- WCP Nietzsche OnNatureGodEthicsDocument4 pagesWCP Nietzsche OnNatureGodEthicsmasohaNo ratings yet

- Galvafroid Data SheetDocument13 pagesGalvafroid Data SheetAdam HughesNo ratings yet

- ZTE Product Introduction and Light PON Solution For BalitowerDocument32 pagesZTE Product Introduction and Light PON Solution For BalitowerOrigoAndoraNo ratings yet

- Important Questions 2016Document57 pagesImportant Questions 2016Anonymous t9LFhvF100% (1)

- MH370 (MAS370) Malaysia Airlines Flight Tracking and History 11-Mar-2014 (KUL - WMKK-PEK - ZBAA) - FlightAwareDocument2 pagesMH370 (MAS370) Malaysia Airlines Flight Tracking and History 11-Mar-2014 (KUL - WMKK-PEK - ZBAA) - FlightAware陳佩No ratings yet

- Capacity PlanDocument1 pageCapacity PlanbishnuNo ratings yet

- Course Title:-Advanced Computer Networking Group Presentation On NFV FunctionalityDocument18 pagesCourse Title:-Advanced Computer Networking Group Presentation On NFV FunctionalityRoha CbcNo ratings yet

- Types of CrutchesDocument19 pagesTypes of CrutchesJOYCE ONYEAGORONo ratings yet

- Evertz MVP Manual PDFDocument2 pagesEvertz MVP Manual PDFDavidNo ratings yet

- Callistephus Chinensis GalaDocument4 pagesCallistephus Chinensis GalaBacic SanjaNo ratings yet

- Draftsmangrade II PDFDocument3 pagesDraftsmangrade II PDFakhilaNo ratings yet

- Neptune Planet Experiment, Ariny Amos (Astronomer) - 1Document1,139 pagesNeptune Planet Experiment, Ariny Amos (Astronomer) - 1Dr. Amos ArinyNo ratings yet

- FIN V1 Chap4 EconDocument15 pagesFIN V1 Chap4 EconV I S W A L S HNo ratings yet

- 1.load Test On DC Shut MotorDocument5 pages1.load Test On DC Shut Motorg3v5No ratings yet

- Diss PrelimDocument2 pagesDiss PrelimRochelle Beatriz Mapanao100% (1)

- Jean AttachmentDocument17 pagesJean AttachmentReena VermaNo ratings yet

- Physics 158 Final Exam Review Package: UBC Engineering Undergraduate SocietyDocument22 pagesPhysics 158 Final Exam Review Package: UBC Engineering Undergraduate SocietySpam MailNo ratings yet

- Dampak Bencana Alam Bagi Sektor Pariwisata Di Bali Ni Ketut Sutrisnawati AKPAR DenpasarDocument10 pagesDampak Bencana Alam Bagi Sektor Pariwisata Di Bali Ni Ketut Sutrisnawati AKPAR DenpasarRihar KoharNo ratings yet

- Revised Final 2.5.2016 Entire Report 2Document117 pagesRevised Final 2.5.2016 Entire Report 2New Mexico Political ReportNo ratings yet

- Question Paper - BiologyDocument5 pagesQuestion Paper - BiologyAratrika ChakravartyNo ratings yet

- IMO MSC 1 - Cir.1200 - Alternative Wind Heeling LeverDocument17 pagesIMO MSC 1 - Cir.1200 - Alternative Wind Heeling LeverDavid AmachreeNo ratings yet

- Electrical Transmission and DistributionDocument31 pagesElectrical Transmission and DistributionPutri Hanifah SNo ratings yet

- 415V CALCULATING SHEET AND SETTING LIST FOR EQUIPMENT PROTECTION OF CHP WAGON TIPPER AND ESP (Supplement For Zero Sequence Current Relay)Document25 pages415V CALCULATING SHEET AND SETTING LIST FOR EQUIPMENT PROTECTION OF CHP WAGON TIPPER AND ESP (Supplement For Zero Sequence Current Relay)Amaresh NayakNo ratings yet

- Star Holman 210HX Conveyor OvenDocument2 pagesStar Holman 210HX Conveyor Ovenwsfc-ebayNo ratings yet

- 2015 - Soil Mechanics II - Final - enDocument7 pages2015 - Soil Mechanics II - Final - enjohn cambixNo ratings yet