Professional Documents

Culture Documents

Chapter 1 - Business Combinations Statutory Merger and Statutory Consolidation

Chapter 1 - Business Combinations Statutory Merger and Statutory Consolidation

Uploaded by

Kaori MiyazonoCopyright

Available Formats

Share this document

Did you find this document useful?

Is this content inappropriate?

Report this DocumentCopyright:

Available Formats

Chapter 1 - Business Combinations Statutory Merger and Statutory Consolidation

Chapter 1 - Business Combinations Statutory Merger and Statutory Consolidation

Uploaded by

Kaori MiyazonoCopyright:

Available Formats

Chapter 1 - Business Combinations: Statutory Merger and

Statutory Consolidation

Saturday, 14 August 2021 11:29 am

rules that govern how a company is

run and one of the first items to be

Included in this Chapter: established by the BOD at the time a

✓ Reasons for the popularity of business combination company is started

✓ Methods and techniques in dealing with them

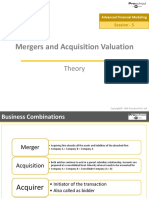

Nature of a Business Combination

Board of directors A business combination may be:

▫ Friendly • Submitted to the stockholders for approval

→ The BOD of the potential combining companies negotiates mutually agreeable terms of a • Normally, 2/3 or 3/4 positive vote is required by corporate by-laws

proposed combination to bind all stockholders to the combination

Why lower? Isn't the ▫ Unfriendly (hostile takeovers)

acquisition supposed to be at → The BOD of a company targeted for acquisition resists the combination

premium price? ▫ Resistance

→ Involves various moves by the target company A formal tender offer enables the acquiring firm to deal directly with

→ Defensive tactics or moves to resist the proposed business combination: individual shareholders

• Poison Pill - An amendment of the Articles of incorporation or by-laws to

make it more difficult to obtain stockholder approval for a takeover

• At a price substantially lower in excess of the • Greenmail - Acquisition of common stock presently owned by the prospective → a public solicitation to all shareholders requesting

prospective acquirer's cost acquiring (acquirer) company that they tender their stock for sale at a specific

• The purchased shares are then held as • White Knight or White Squire - A search for a candidate to be the acquirer in price during a certain time

treasury or retired a friendly takeover → Relatively quick and easily executed

How? • Largely ineffective - it may result to an • Pac-man Defense - attempting on unfriendly takeover of the would be A shield bearer → Preferred mean of acquiring public companies

expensive excise tax; the excess of the price acquiring company or armor bearer

paid over the market price is expensed • Selling the "Crown Jewels" or "Scorched Earth" - The sale of valuable assets or a knight

to others to make the firm less attractive to the "would be acquirer"

Burned by flames or • Shark Repellent - acquisition of substantial amounts of outstanding common

Entity's own shares that have heat stock for the treasury or for the retirement, or the incurring of substantial Any one of a number of measures taken

been issued and then re-

long term debt in exchange for outstanding common stock by a company to fend off an unwanted

acquired but not canceled

• Leveraged buyouts - management desires to own the business, arrange to or hostile takeover attempt

buy out the stockholders using the company's assets to finance the deal

The bonds issued often take

• Mudslinging Defense - an attempt to discredit one's competitor, opponent,

the form of high-interest,

etc., by malicious or scandalous attacks

high-risk "junk" bonds When the acquiring company offers stock instead of cash, the perspective

• Defensive Acquisition Tactic - When a major reason for an attempted acquiring (acquirer) company's management may try to convince the

takeover is the prospective acquiring (acquirer) company's favorable cash shareholders that the stock would be a bad investment

position, the prospective acquiring (acquirer) company may try to rid itself of

this excess cash by attempting to takeover of its own

✓ Reasons for Business Combinations There are several ways of business expansion. The ff are the reasons

why business combination may be preferred as compared to other

means:

1. Cost Advantage - less expensive to obtain needed amenities through combination than through

development

2. Lower Risk - the acquisition of the reputable product lines and markets is usually less risky than a risk management strategy that

developing new products and market; low threat when the purpose is diversification mixes a wide variety of

3. Avoidance of Takeovers - small companies tend to be more susceptible to corporate takeovers investments within a portfolio.

How? 4. Acquisition of Intangible Assets - bring together both intangible and tangible resources

5. Other Reasons - for business tax advantages, for personal income, estate-tax advantages, or for

personal reasons

Types of Business Combinations

Three schemes:

1. Based on the structure of the combination

2. Based on the method used to accomplished the combination

3. Based on the accounting method used

Possible Structures: (Factors that might

• Overriding objective - increase profitability determine the structure of business combination)

• Firms can become more efficient by horizontally, or vertically

Structure of Business Combination

• Legal & Tax strategies

integrating operations, through conglomerate operations • Market and regulatory considerations:

• Horizontal Integration - involves companies within the same industry that have previously ▫ One becomes a subsidiary of

been competitors another

a large corporation formed by the Normally, a company ▫ Two are legally merged into one

merging of separate and diverse

• Vertical Integration - take place between two companies involved in the same industry but at and its suppliers or ▫ One transfers its net assets to

different levels

firms customers another

involve (something) as a • Conglomerate Combination - involving companies in unrelated industries having little, If any, ▫ Owner transfer their equity interest

necessary or inevitable production or market similarities for the purpose of entering into new markets or industries to the other owner

part or consequence • Circular Combination - entails some diversification, but does not have a drastic change in ▫ Two or more transfer their net

likely to have a strong or far- assets, owners transfer their equity

operation as a conglomerate reaching effect; radical and interests, to a newly-formed entity

extreme (roll-up, put-together transaction)

▫ Group of former owners of one

obtains control of a combined entity

Methods/Types of Combinations/ Legal forms of Effecting Business

Combinations

From legal, accounting, organizational perspective, the specific procedures to be used in accounting

for business combination is effected through:

Assets less liabilities Assets, securities, debt Acquirer accounts for the combination

I. Acquisition of Net Assets

instruments received Record each asset acquired, each

→ Books of the acquired company are closed out, its assets and liabilities are transferred to

from acquirer liability assumed, and the consideration

the books of the acquirer

→ Features of asset and liabilities acquisition: Acquired company given in exchange

• Acquirer acquires the net assets of the other enterprise for cash or other property, distributes to its

debt instruments, and equity instruments, or combination stockholders

• Acquirer must acquire 100% of the net assets of the acquired company Liquidates

• It only involves when the acquirer survives

• Acquirer debits an account "Investment in

II. Acquisition of Common Stock

Subsidiary"

→ Books of the acquirer and the acquired company remain intact and consolidated financial

• The stock of the acquired company is recorded as an

statements are prepared periodically

inter-corporate investment • When other factors are present that lead to the acquirer gaining control

→ Feature of a stock acquisition:

• Does not necessarily have to involve the acquisition • Non-controlling Interest

• Acquirer acquires voting (common) stock from another enterprise for cash or other

of all of a company's outstanding voting (common) → Total of the shares of the acquired company not held by the

property, debt instruments, and equity instruments, or combination

shares controlling shareholder

• Acquirer must obtain control by purchasing 50% or more of the voting stock or

possibly less

• Acquired company need not be dissolved

• The selling firm may continue to survive as a legal entity Both the acquirer and the acquired company remain as separate legal entity

or liquidate entirely III. Asset Acquisition

• Acquirer typically targets key assets, buy asset but not → Acquisition by one firm of assets (and possibly liabilities) of another firm, but not its

assume liabilities shares

• Acquirer may not buy the entire entity

Acquisition of Net Assets Classification:

• Statutory Merger

→ Acquirer survives though it may be continued as a separate division of the acquirer

• The board of directors of the companies involved → Acquired company ceases to exist as a separate legal entity

normally negotiates the terms of a plan of merger, → X company + Y company = X company or Y company

consolidation

• be approved by the stockholders of each company • Statutory Consolidation

involved → New corporation is formed to acquire two or more other corporations May be operated as separate division of new corporation

• Laws or corporation by laws dictate the percentage → Acquired corporation cease to exist as separate legal entities

of positive votes required by approval of the plan → X company + Y company = Z company

→ Stockholders of the acquired companies (X,Y) become stockholders in the new entity (Z)

Merger Consolidation

→ All but one of the combining companies go → All the combining companies are dissolved

out of existence → New corporation is formed to take over their

net assets

→ First key aspect

→ Control can usually be obtained by:

→ In accounting, refers to the accounting process ○ Buying the assets themselves

or procedures of combining parent and ○ Buying enough shares in the corporation

Book Notes Page 1

→ All but one of the combining companies go → All the combining companies are dissolved

out of existence → New corporation is formed to take over their

net assets

→ First key aspect

→ Control can usually be obtained by:

→ In accounting, refers to the accounting process ○ Buying the assets themselves

or procedures of combining parent and ○ Buying enough shares in the corporation

subsidiary financial statements

PFRS 3 → Economic events that might result to obtaining

→ Accounting standard relevant for control:

accounting for business combinations ○ Transferring cash or other assets, net assets

→ Appendix A - different terms

Accounting Concept of Business Combination ○ Incurring liabilities

→ Appendix B - application guidance ○ Issuing equity instruments

Business Combination ○ Combination of the above

→ A transaction or other event in which an acquirer obtains control of one or more businesses ○ Transaction not involving consideration,

→ "true mergers", "mergers of equals" (combination by contract alone)

→ Must involve the acquisition of a business, three elements:

▫ Inputs - economic resource merely need to have the ability to contribute to the creation

of outputs

The focus on outputs is on returns from goods and ▫ Process - system, standard, protocol, convention, or rule that when applied to an input or → Second key aspect

services provided investment income and other inputs, creates outputs → Integrated set of activities and assets that is capable of being conducted and

income ▫ Output - the result of inputs and processes, that provide goods or services to customers, managed for the purpose of providing goods or services to customers,

generate income generating investment income (such as dividends or interest) or generating

other income from ordinary activities - PFRS 3

→ Purpose to define - to distinguish acquisition of group of assets and the

Scope of Business Combination acquisition of an entity that is capable of producing output

Not scope of Business Combination

1. Combinations involving mutual entities

• If it results in the formation of all types of joint

2. Combinations achieved by contract alone (dual listing stapling)

arrangements

→ Two entities enter into a contractual arrangement which may cover An entity other than an investor-owned entity, that A mutual insurance

• Scope exception only applies to the financial statements

• operation under a single management provides dividends, lower costs or other economic company, a credit union, a

of the joint venture or the joint operation itself

• equalization of voting power and earnings attributable to both entities' equity benefits directly to its owners, members or participants cooperative entity

• If it involves entities or businesses under common

investors

control

→ May involve a 'stapling' or formation of a dual listed corporation

• If the acquisition of an asset or group of assets does not

→ Accounting - requires one of the combining entities to be identified as the acquirer, and

constitute a business

○ Asset acquisition one to be identified as the acquiree/acquired company

○ Identifies and recognizes the individual identifiable

assets acquired and liabilities assumed Acquisition Method

○ Allocates the cost of the group of assets and liabilities → Applied on the acquisition date which is the date the acquirer obtains control of the acquiree

to the individual assets and liabilities on the basis of

→ Approaches a business combination from the perspective of the acquirer

their relative fair value at the date of purchase

○ Does not give rise to goodwill → All assets and liabilities are identified and reported at their fair values

→ Required method of accounting for a business combination

1. Identify the acquirer

• Acquirer - the entity that obtains control of the acquiree

• One of the combining entities should be identified as the acquirer

• In the event that the overriding principle of 'control' in PFRS 3 does not conclusively

determine the identity of the acquirer, PFRS 3 provides additional guidance

2. Determining the acquisition date Other important dates:

• Acquisition date ✓ The date contract is signed

✓ The date the consideration is paid

→ Date on which the acquirer obtains control of the acquiree ✓ A date nominated in the contract

→ Does not depend on the date the acquirer receives physical possession of the assets ✓ The date on which assets acquired are delivered to the acquirer

acquired or actually pays out the consideration to the acquiree ✓ The date on which an offer becomes unconditional

→ In time when the net assets of the acquired company become the net assets of the

acquirer

• Business combination occurs at the date of the assets or net assets are under the control

of the acquirer

• The use of control in determining the acquisition date ensures that the substance of the

transaction determines the accounting rather than the form of the transaction

• Areas where the selection of the date affects the accounting for business combination:

□ Identifiable assets acquired and liabilities assumed by the acquirer are measured at

the fair value on the acquisition date

□ Consideration paid by the acquirer is determined as the sum of the fair values of

assets given, equity issued and/ or liabilities undertaken in an exchange for the net

assets or shares of another entity

□ Acquirer may acquire only some of the shares of the acquiree, the non-controlling

interest is measured at fair value on acquisition date

□ Acquirer may have previously held an equity interest in the acquiree prior to

obtaining control of the acquiree, the value of this investment is measured at fair

value on acquisition date

• The effect of determining the acquisition date is that the financial position of the

combined entity on acquisition date should report the assets and liabilities of the

acquiree on that date

• Any profits reports as a result of the acquiree's operation within the business

combination should reflect profits earned after the acquisition date

3. Calculate the fair value of the consideration transferred

• Consideration transferred

→ Measured at fair value at acquisition date

→ Calculated as the sum of acquisition date fair values of:

□ The assets transferred by the acquirer

□ The liabilities incurred by the acquirer to former owners of the acquiree

□ The equity interest issued by the acquirer

• Consideration transferred includes:

✓ Cash or other monetary assets

▪ Fair value = the amount of cash or cash equivalent dispersed

▪ Problem that may arise - when the settlement is deferred to a time after the

acquisition date

▫ Deferred payment fair value = the amount the entity would have to

borrow to settle the debt immediately (present value of the obligation)

▫ Discount rate used = entity's incremental borrowing rate • The acquirer is in effect selling the non-

✓ Non-monetary assets monetary asset to the acquiree

→ Assets such as property, plant, and equipment, investments, licenses and • Thus, it is earning an income equal to the fair

patents value of the asset

▪ Fair value = if active second-hand market exists, obtained by reference to • Gain or loss = fair value less carrying amount

those

✓ Equity instruments

▪ Fair value = for listed entities, reference is made to the quoted prices of the

shares at acquisition date

✓ Liabilities Undertaken Future losses or other costs expected to be incurred as a result

▪ Fair value = present values of expected future cash outflows of the combination are not liabilities of the acquirer and not

✓ Contingent Consideration included on the calculation

→ An obligation of the acquirer to transfer additional assets or equity interests

to the former owners of an acquiree as part of the exchange for control of the

acquiree if the specified future events occur or conditions are met

→ May also give the acquirer the right to the return of previously transferred

consideration if specified conditions are met

→ An add-on to the base acquisition price that is based on events occurring or

conditions being met some time after the purchase takes place

✓ Share-based payment awards

→ Exchanged for awards held by the acquiree's employees

▪ Measurement = market based measure

▪ The acquirer is obliged to replace the acquiree's awards if the acquiree or the

employees have the ability to enforce replacement, either all or a portion of

the market-based measure of the acquirer's replacement awards is included

Includes: in measuring consideration transferred in the business combination

• Legal fees • Acquisition-Related Costs

• Finder's brokerage fees → Further item to be considered in determining the cost of the business combination

• Advisory, accounting, valuation, → Excluded from the measurement of the consideration paid

and other professional or → Not part of the fair value of the acquiree and are not assets

consulting fees → They are as follows: Reasons:

□ Costs directly attributable to the combination • Acquisition-related costs are not part of the fair value exchange

□ Indirect, ongoing costs, general costs including the cost to maintain an between the buyer and seller

• General, administrative costs such as internal acquisition department • They are separate transactions for which the buyer pays the fair

✓ Managerial (including the costs of → Accounting for these outlays is a result of the decision to record the identifiable value for the services received

maintaining an internal acquisitions assets acquired and liabilities assumed at fair value • These amounts do not generally represent assets of the acquirer of

department - management salaries, → If associated with a business combination = accounted for as expenses in the acquisition date because the benefits obtained are consumed as the

depreciation, rent, and costs incurred to periods in which they are incurred and the services are received services are received

Book Notes Page 2

→ They are as follows: Reasons:

□ Costs directly attributable to the combination • Acquisition-related costs are not part of the fair value exchange

□ Indirect, ongoing costs, general costs including the cost to maintain an between the buyer and seller

• General, administrative costs such as internal acquisition department • They are separate transactions for which the buyer pays the fair

✓ Managerial (including the costs of → Accounting for these outlays is a result of the decision to record the identifiable value for the services received

maintaining an internal acquisitions assets acquired and liabilities assumed at fair value • These amounts do not generally represent assets of the acquirer of

department - management salaries, → If associated with a business combination = accounted for as expenses in the acquisition date because the benefits obtained are consumed as the

depreciation, rent, and costs incurred to periods in which they are incurred and the services are received services are received

duplicate facilities • Costs of Issuing Equity Instruments/Share Issuance Costs • In contrast to PAS 16

✓ Overhead that are allocated to the merger → Excluded from the consideration and accounted for separately

but would have existed in its absence → These costs are accounted for in accordance with PAS 32

✓ Other costs of which cannot be directly → These outlays should be treated as a reduction in the share capital

attributed to the particular acquisition → Reduce the proceeds from equity issue - reducing the additional paid-in capital, net

of any related income tax benefit

→ Share premium/Additional paid-in capital from the related issuance not enough to

absorb such cost:

▪ excess should be debited to 'Share Issuance Costs'

▪ treated as a contra shareholders' equity account as a deduction in the ff

Including:

order of priority:

• Shutting-down departments

1. Share premium from previous share issuance

• Re-assigning or eliminating jobs

2. Retained Earnings with appropriate disclosure

• changing suppliers or production practices

→ Additional acquisition-related restructuring costs = unless represented by

in connection with business combinations

acquisition-date liabilities, are expensed as incurred and do not affect acquisition

cost

→ Listing fee for initial public offering of shares = outright expense

• Cost of Issuing Debt Instruments

→ The costs of arranging and issuing debt instruments or financial liabilities are an

integral part of the liability issue transaction

→ Deemed as yield adjustments to the cost of borrowing

→ Included in the measurement of the liability as bond issue cost and amortized over

the life of the debt

• Summary:

Acquisition-related costs Examples Treatment

1. Directly attributable costs Legal fees, finders and brokerage fees, Expenses

advisory, accounting valuation (valuers)

and other professional or consulting fees

to affect the combination

2. Indirect acquisition costs General and administrative costs Expenses

3. Cost of issuing securities Transaction costs such as stamp duties on Debit to "Share

new shares, professional adviser's fees, premium" or

underwriting costs and brokerage fees "Additional paid-in

might be incurred capital"

4. Cost of arranging and Professional adviser's fees, underwriting Bond issue costs

issuing debt securities or costs and brokerage fees

financial liabilities

4. Recognize and measure the identifiable assets and liabilities of the

business

• Acquirer shall assess whether any portion of • Principles in assessing what is part of the Business Combination

the transaction price (payments or other ▫ Only the consideration transferred and the assets acquired or liabilities assumed or

arrangements) and any asset acquired or incurred that are part of the exchange for the acquiree shall be included in the business

liabilities assumed or incurred are not a combination accounting

part or a component of the exchange for the ▫ Guidelines to assess what part of the business combination for certain items requires the

acquiree acquirer to evaluate the substance of transactions entered into by the parties:

• Not part = shall be accounted for separately i. Transactions entered into or any amounts paid that are designed primarily for the

from the business combination economic benefit of the acquiree (or its former owners) before the combination Don't apply to any costs incurred by the acquirer on its

– Though not paid directly, the amount paid will still form part of the purchase own behalf = accounted for outside the business

consideration for the business combination as the acquirer is acting on behalf combination

of the acquiree in making the payments

A relationship between Examples of separate transaction that are not ii. Transactions entered into or any amounts paid into by or on behalf of the acquirer

acquirer and the acquiree included in applying the acquisition method: or the combined entity are not part of the business combination, likely to be

that existed before the • A transaction that settles pre-existing accounted for separately

business combination, relationships between the acquirer and the

may include a contractual acquire • Recognition and Measurement of Assets Acquired and Liabilities Assumed: Accounting PFRS 3

or non-contractual • A transaction that compensates employees Records of the Acquirer → set out basic principles for the recognition

relationship or former employees of the acquiree for ▫ The acquirer is required to: and measurement of identifiable assets

future services i. Recognize identifiable assets and liabilities separately from goodwill; and acquired, liabilities assumed and non-

• A transaction that reimburses the acquiree ii. Measure such assets and liabilities at their fair values on the date of acquisition controlling interests

or its former owners for paying the

Contractual: ▫ Identifiable - key word

acquirer's acquisition related costs

• Vendor-customer ▫ As of acquisition date, acquirer should recognize separately from goodwill:

• Franchisor- ▪ Identifiable assets acquired

franchisee ▪ Liabilities assumed

• Licensor-licensee Whether arrangements for contingent ▪ Any non-controlling interests in the acquirer

Non-contractual payments to employees or former owners of ▫ Two recognition criteria for assets and liabilities, the recognition occurs if:

• Plaintiff-defendant an acquiree should be considered as ▪ It is probable that any future economic benefit will flow to or from the entity

contingent consideration that is included in ▪ The item has a cost or value that can be reliably measured

the measurement of the consideration ▫ Acquirer is required to recognized identifiable assets acquired and liabilities assumed

transferred or are separate transactions regardless of the degree of probability of an inflow or outflow of economic benefits

depends on the nature of the arrangement ▫ The assets acquired and liabilities assumed are measured at fair value

• Conditions for Recognition Principle

→ Two conditions have to be met prior to the recognition of assets and liabilities acquired

(1) Assets and liabilities

▫ at the acquisition date, must meet the definition of assets and liabilities in

the Framework

▫ Expected future costs = can't be included in the calculation

▫ Outcomes of applying this recognition condition:

▪ Post-acquisition reorganization

→ Costs the acquirer expects but it is not oblige to incur in the

future to affect its plan to exit an activity of an acquiree

▪ Unrecognized assets and liabilities

→ The acquirer may recognize some assets and liabilities that the

acquiree had not previously recognized in its financial statements

▫ Exception:

→ One area affected by this condition - accounting for contingent

liabilities

(2) Item acquired or assumed The entities involved in the transactions

▫ Must be part of the business acquired rather than the result of a separate may link another transaction with the

transaction business combination, but in substance it

▫ An example of the application of substance over form is a separate transaction

• Measurement Principle for Assets and Liabilities

▫ Identifiable assets acquired and liabilities assumed = measured at their fair values on

acquisition date

▫ Fair value

→ The price that would be received to sell an asset or paid to transfer a liability in an

orderly transaction between market participants at the measurement date

→ A market-based measurement, not an entity-specific measurement

→ The process of determining, necessarily involves judgement and estimation

→ Measurement under the fair value hierarchy:

▫ Level 1 inputs

→ Fully observable

→ Unadjusted quoted prices in an active market for identical assets and

liabilities

▫ Level 2 inputs

→ Directly or indirectly observable inputs other than Level 1 inputs

▫ Level 3 inputs

→ Unobservable inputs for the asset or liability

→ Not based on observable market data

• Valuation Techniques

→ To estimate the price at which an orderly transaction to sell an asset or to transfer the

liability would take place between market participants and the measurement date under

current market conditions

a. Market approach or market-based

→ Uses prices and other relevant information generated by market transactions

involving identical or comparable (similar) assets, liabilities, or a group of assets and

liabilities

→ "analogy or benchmark approach"

b. Income approach or income-based

→ Based on future economic benefit derived from owning the assets or converts

Book Notes Page 3

→ Based on future economic benefit derived from owning the assets or converts

future amounts (cash flows or income and expenses) to a single current

(discounted) amount, reflecting current market expectations about those future

amounts

c. Cost approach or cost-based

→ Reflects the amount that would be required currently to replace the service

capacity of an asset (current replacement cost)

→ Although the result may not reflect fair value

• Valuation of Identifiable assets and liabilities

▫ First step in recording an acquisition

→ To record existing assets and liabilities accounts (except goodwill)

→ General rule - to be recorded at their individually determined fair values

▫ Preferred method

→ Quoted market value - an active market for the item exists

→ Not an active market - used to estimated fair values:

□ independent appraisals

□ discounted cash flow analysis

□ Other types of analysis

→ Some exceptions to the use of fair value that apply to accounts:

□ Assets for resale

□ Deferred taxes

▫ The acquirer is not required to establish values immediately on the acquisition date

• Summary of procedures Acquirer not permitted to recognize a separate

(1) Identifiable Tangible Assets valuation allowance as of the acquisition date for

→ Asset other than intangible asset assets acquired in a business combination that

→ Recognized through probability and reliability test are measured at their acquisition date fair values

a. Current Assets

→ Recorded at estimated fair values

→ All accounts share the rule that only the net fair value is recorded, and

valuation accounts are not used

b. Assets held for sale If the assets had initially been measured

→ Assets that are going to be sold rather than to be used in operations at their fair value at the acquisition date,

→ Should be measure at fair value less costs to sell they are listed as current assets.

c. Property, plant and equipment

→ Estimate of fair value

→ Recorded at the net amount with no separate accumulated depreciation

account

→ No valuation allowance principle also applies

d. Investments in equity-accounted entities

→ Fair value of the associate should be determined on the basis of the value of

the shares of the associate

(2) Identifiable Intangible Assets

→ Recognize regardless of the degree of probability of an inflow of economic benefits

→ Identifiable if:

▪ Can be separated

→ Separability criterion

→ Capable of being separated or divided from the entity sold, transferred,

licensed, rented, or exchanged, either individually or together with a related

contract

▪ Meets the contractual-legal criterion

→ Arises from contractual or legal rights

→ Whether those rights are transferable or separable from the acquiree or from

other rights and obligations

→ When an intangible asset satisfies either of the criteria, sufficient information should exist

to measure reliably its fair value

Marketing- Customer- Artistic-related Contract-based Technologica

related related l-based

Trademarks, Order or Plays, operas and Licensing royalty Patented

trade names, production ballets and standstill technology

service marks, backlog agreements

collective marks,

certification

marks

Trade dress Customer Books, magazines, Advertising Computer

contracts and newspaper, and construction, software and

the related other literary works management, masks works

customer service or supply

relationships contracts

Newspaper Non- Musical works such Lease Unpatented

mastheads contractual as compositions, agreements technology

customer song lyrics and (whether the

relationships advertising jingles acquiree is the

lessee or lessor)

Internet domain Customer lists Pictures and Construction Databases

names photographs permits including

title plants

Non-competition Video and Franchise Trade secrets

agreements audiovisual agreements such as

material, including secret

motion pictures or formulas,

films, music videos processes or

and television recipe

programs

Operating and

broadcasting

rights

Use rights such

as drilling, water,

air, mineral,

timber-getting

and route

authorities

Servicing

contracts such as

mortgage

servicing

contracts

Employment

contracts

→ Other intangible assets being acquired with their proper valuation:

• Emission rights

→ Recognized on the acquisition date at fair value

• Reacquired rights

→ Recognizes separately from goodwill

→ An acquirer may reacquire a right that it had previously granted to the acquiree to

use one or more of the acquirer's recognized or unrecognized assets such as right to

use the acquirer's trade name under franchise agreement

→ Care should be considered to as recognition of intangible assets:

a. Existing Intangible Assets

Such as patent and copyright

→ Recorded at estimated fair value

→ The valuation will typically require the use of discounted cash flow analysis

b. Intangible assets not currently recorded by the acquiree

Book Notes Page 4

You might also like

- Strategic Fit in Mergers & Acquisitions - An ImperativeDocument22 pagesStrategic Fit in Mergers & Acquisitions - An ImperativeAnil Sahu100% (1)

- Capital MarketDocument32 pagesCapital MarketAppan Kandala Vasudevachary80% (5)

- Mergers & Acquisitions: Philip-Indal CaseDocument20 pagesMergers & Acquisitions: Philip-Indal CaseRahul GargNo ratings yet

- Everything You Need To Make Your First Trade PDFDocument14 pagesEverything You Need To Make Your First Trade PDFPrasad Naik50% (2)

- Chapter 21 Merger and AcquisitionDocument2 pagesChapter 21 Merger and AcquisitionLemeryNo ratings yet

- Bus Ass - Joo - S04B - Attack OutlineDocument11 pagesBus Ass - Joo - S04B - Attack OutlineWilliamMunny1100% (4)

- Homework #3 - Coursera CorrectedDocument10 pagesHomework #3 - Coursera CorrectedSaravind67% (3)

- 3 Mergers Acquisitions Accretion Dilution ModelingDocument32 pages3 Mergers Acquisitions Accretion Dilution ModelingTony NguyenNo ratings yet

- Chapter 5 TheoryDocument5 pagesChapter 5 TheoryCaptain Rs -pubg mobileNo ratings yet

- Tong Quan M&aDocument4 pagesTong Quan M&anguyenhaiyennn125No ratings yet

- Private Equity Valuation: FintreeDocument46 pagesPrivate Equity Valuation: FintreeAniket JainNo ratings yet

- Planning A ReorganisationDocument2 pagesPlanning A Reorganisationr.filatou.cypNo ratings yet

- Mergers and Acquisitions PresentationDocument17 pagesMergers and Acquisitions PresentationЕкатерина БелоусоваNo ratings yet

- 2,3 M&aDocument17 pages2,3 M&areysinghania7No ratings yet

- BBL 112 012715Document3 pagesBBL 112 012715Claude PeñaNo ratings yet

- Hostile Takeover in Respect To IndiaDocument39 pagesHostile Takeover in Respect To IndiadebankaNo ratings yet

- Business Law 3E3MzKXXH34eDocument8 pagesBusiness Law 3E3MzKXXH34ebhawnaNo ratings yet

- 4.2 Ch18 Mergers 2020Document5 pages4.2 Ch18 Mergers 2020bobhamilton3489No ratings yet

- The Organization of The Firm Transaction Costs Variations On Asset SpecificityDocument11 pagesThe Organization of The Firm Transaction Costs Variations On Asset Specificitychizz popcornnNo ratings yet

- Stocks and Their ValuationDocument36 pagesStocks and Their ValuationMaria AngelicaNo ratings yet

- Mergers and AcquisitionsDocument15 pagesMergers and AcquisitionsWalid SolimanNo ratings yet

- Template Co-Founder Agreement - Short Form: User NotesDocument13 pagesTemplate Co-Founder Agreement - Short Form: User NotesMohamed K. GummaNo ratings yet

- Basic Concepts of Corporate RestructuringDocument74 pagesBasic Concepts of Corporate RestructuringSaburao ChalawadiNo ratings yet

- Co Founder Agreement Long Form 2016-09-16Document16 pagesCo Founder Agreement Long Form 2016-09-16Mukhtar Oyewo100% (1)

- Long Term Financing 1Document39 pagesLong Term Financing 12023415284No ratings yet

- Mergers and AcquisitionsDocument40 pagesMergers and AcquisitionsAn DoNo ratings yet

- Chap 14 - Topic 8Document43 pagesChap 14 - Topic 8Bùi Tường Minh QuangNo ratings yet

- The Organization of The Firm Specialized InvestmentsDocument3 pagesThe Organization of The Firm Specialized Investmentschizz popcornnNo ratings yet

- Summer Preparatory Material - M&a BasicsDocument8 pagesSummer Preparatory Material - M&a BasicsHarsha SrivastavaNo ratings yet

- Fin 520 NoteDocument10 pagesFin 520 NoteEmanuele OlivieriNo ratings yet

- Corporations Cheat Sheet: by ViaDocument6 pagesCorporations Cheat Sheet: by ViaMartin LaiNo ratings yet

- Part 3 - Shariah-Compliant StocksDocument32 pagesPart 3 - Shariah-Compliant StocksIzNew0212No ratings yet

- Merger & Acquisition by RPDocument27 pagesMerger & Acquisition by RPdatun kejati kaltengNo ratings yet

- M&a - Types of AcquisitionsDocument2 pagesM&a - Types of AcquisitionsArijit SahaNo ratings yet

- Lesson 5 EntrepDocument24 pagesLesson 5 EntrepMark Dave YuNo ratings yet

- 1 - Corporate Finance - Introduction PDFDocument29 pages1 - Corporate Finance - Introduction PDFPankaj VarshneyNo ratings yet

- Buscom PPT 1Document24 pagesBuscom PPT 1dmangiginNo ratings yet

- Business LawDocument8 pagesBusiness Lawankita mishraNo ratings yet

- Presentation On Corporate RestructuringDocument29 pagesPresentation On Corporate Restructuringom_mohit11No ratings yet

- Unit 4 Paying For The Acquisition, Sources of Funds (Book)Document10 pagesUnit 4 Paying For The Acquisition, Sources of Funds (Book)divlingvarshneyNo ratings yet

- Company Law 2Document4 pagesCompany Law 2Divya RaoNo ratings yet

- Manajemen Keuangan - Merger and Acquisition PDFDocument36 pagesManajemen Keuangan - Merger and Acquisition PDFvrieskaNo ratings yet

- 21578sm SFM Finalnewvol2 Cp13Document95 pages21578sm SFM Finalnewvol2 Cp13subhradeep sinhaNo ratings yet

- Semester 9Document9 pagesSemester 9Parth Prachi ShrivastavaNo ratings yet

- Mergers and AcquisitionDocument14 pagesMergers and AcquisitionKaushik Thacker100% (2)

- Chapter 2 RestructuringDocument9 pagesChapter 2 RestructuringTarek Bin Azim MahadiNo ratings yet

- Business LawDocument9 pagesBusiness LawPrashant SinghNo ratings yet

- Merger, Acquisition & Restructuring: Basic Concepts and FormulaeDocument56 pagesMerger, Acquisition & Restructuring: Basic Concepts and Formulaemegha balajiNo ratings yet

- Corporation LawDocument76 pagesCorporation LawMary Megan TaboraNo ratings yet

- F Week 6 PresentationDocument37 pagesF Week 6 PresentationGaming champNo ratings yet

- Short and Long Term Finance Incl Islamic Finance Lecture 3Document60 pagesShort and Long Term Finance Incl Islamic Finance Lecture 3Ambreen RabbaniNo ratings yet

- Strategic Management Sessions 31 - 40Document7 pagesStrategic Management Sessions 31 - 40SHEETAL SINGHNo ratings yet

- Topic 5 - Company Borrowing Ca2016Document16 pagesTopic 5 - Company Borrowing Ca2016ShanszhiNo ratings yet

- Merger and Acquistions TheoryDocument214 pagesMerger and Acquistions TheoryPranay Singh RaghuvanshiNo ratings yet

- DBN Products V2020Document2 pagesDBN Products V2020victoria upindiNo ratings yet

- MergerDocument21 pagesMergerPrince SinghNo ratings yet

- SFM CA Final PMDocument34 pagesSFM CA Final PMShrinivas GirnarNo ratings yet

- IV.-Equity-Market-Securities LessonDocument4 pagesIV.-Equity-Market-Securities LessonSandia EspejoNo ratings yet

- Chapter 1 - Business Combinations: Statutory Merger and Statutory Consolidation (W-2PTS)Document5 pagesChapter 1 - Business Combinations: Statutory Merger and Statutory Consolidation (W-2PTS)Anna Bianca C. GoNo ratings yet

- Dividend Investing: A Beginner's Guide: Learn How to Earn Passive Income from Dividend StocksFrom EverandDividend Investing: A Beginner's Guide: Learn How to Earn Passive Income from Dividend StocksNo ratings yet

- Lifecycle of a Technology Company: Step-by-Step Legal Background and Practical Guide from Startup to SaleFrom EverandLifecycle of a Technology Company: Step-by-Step Legal Background and Practical Guide from Startup to SaleNo ratings yet

- Econ65a - Chapter 4 - Theory of Individual BehaviorDocument13 pagesEcon65a - Chapter 4 - Theory of Individual BehaviorKaori MiyazonoNo ratings yet

- Econ65a - Chapter 5 - The Production Process and CostsDocument1 pageEcon65a - Chapter 5 - The Production Process and CostsKaori MiyazonoNo ratings yet

- Econ65a - Chapter 3 - Quantitative Demand AnalysisDocument3 pagesEcon65a - Chapter 3 - Quantitative Demand AnalysisKaori MiyazonoNo ratings yet

- MNGT23C - 1st - 2nd MeetingDocument4 pagesMNGT23C - 1st - 2nd MeetingKaori MiyazonoNo ratings yet

- Econ65a - Chapter 1 & 2Document7 pagesEcon65a - Chapter 1 & 2Kaori MiyazonoNo ratings yet

- Unit 3 Chapter 3 (Buss Tax... )Document15 pagesUnit 3 Chapter 3 (Buss Tax... )Kaori MiyazonoNo ratings yet

- Cost AccountingDocument13 pagesCost AccountingKaori MiyazonoNo ratings yet

- Chapter 17 - Partnership FormationDocument3 pagesChapter 17 - Partnership FormationKaori MiyazonoNo ratings yet

- Power of Compounding - Vaishnavi SomaniDocument2 pagesPower of Compounding - Vaishnavi SomaniVaishnavi SomaniNo ratings yet

- Resolution PlanDocument118 pagesResolution PlanedhaNo ratings yet

- Miterm 2 2011 Spring AnsDocument14 pagesMiterm 2 2011 Spring AnsKrystle KhanNo ratings yet

- The Effect of IFRS Convergence On Value Relevance of Accounting Information: Cross-Country Analysis of Indonesia, Malaysia, and SingaporeDocument20 pagesThe Effect of IFRS Convergence On Value Relevance of Accounting Information: Cross-Country Analysis of Indonesia, Malaysia, and SingaporeMohammad Arfandi AdnanNo ratings yet

- K17405ca CĐTT Phan Nguyen Tường VyDocument31 pagesK17405ca CĐTT Phan Nguyen Tường VyPhước NguyễnNo ratings yet

- Deepika Research Paper With Cover Page v2Document22 pagesDeepika Research Paper With Cover Page v2Abhishek BaidNo ratings yet

- Certifications Overview - CFA, FRM and FLIPDocument7 pagesCertifications Overview - CFA, FRM and FLIPlifeeeNo ratings yet

- Further Consolidation Issues II: Accounting For Indirect Interests and Changes in Degree of Ownership of A SubsidiaryDocument24 pagesFurther Consolidation Issues II: Accounting For Indirect Interests and Changes in Degree of Ownership of A SubsidiaryDanish JamaliNo ratings yet

- Long-Term Assets I: Property Plant, and EquipmentDocument13 pagesLong-Term Assets I: Property Plant, and EquipmentErjan BhaehakiNo ratings yet

- Corporation Sec. 1 To Sec. 47 by LawsDocument225 pagesCorporation Sec. 1 To Sec. 47 by LawsWinterNo ratings yet

- MMA11A1 CH 1 - Powerpoint SlidesDocument21 pagesMMA11A1 CH 1 - Powerpoint SlidesAsandaNo ratings yet

- R29 CFA Level 3Document12 pagesR29 CFA Level 3Ashna0188No ratings yet

- CH 04Document58 pagesCH 04Aradhita BaruahNo ratings yet

- Red Flags of Enron's of Revenue and Key Financial MeasuresDocument24 pagesRed Flags of Enron's of Revenue and Key Financial MeasuresJoshua BailonNo ratings yet

- Digital Asset 2021 Outlook The Block ResearchDocument102 pagesDigital Asset 2021 Outlook The Block ResearchChen LiangNo ratings yet

- Partnership - Corporation AccountingDocument45 pagesPartnership - Corporation AccountingAB CloydNo ratings yet

- Basic Framework of Management AccountingDocument18 pagesBasic Framework of Management AccountingCathleen TenaNo ratings yet

- CH 8 AnswersDocument5 pagesCH 8 Answersmharieee13No ratings yet

- Finals Exam - MKTG 85Document3 pagesFinals Exam - MKTG 85Jessica CerezaNo ratings yet

- Addtl Budgeting Problems Aug 22Document2 pagesAddtl Budgeting Problems Aug 22MedhaNo ratings yet

- Module 5 Supplemental Problems-SMALL BUSINESS MANAGEMENTDocument5 pagesModule 5 Supplemental Problems-SMALL BUSINESS MANAGEMENTPhát GamingNo ratings yet

- CFO VP Finance CPA in Orange County CA Resume Scott SussmanDocument2 pagesCFO VP Finance CPA in Orange County CA Resume Scott SussmanScottSussmanNo ratings yet

- Cashflow Ex Cers IceDocument1 pageCashflow Ex Cers IceNuman RoxNo ratings yet

- Unit 4 - Company Accounts Lecture NotesDocument12 pagesUnit 4 - Company Accounts Lecture NotesTan TaylorNo ratings yet

- Nike Case StudyDocument4 pagesNike Case StudyNickiBerrangeNo ratings yet

- Islamic Banking and Financial Services (Haneef, Iman & Umar)Document23 pagesIslamic Banking and Financial Services (Haneef, Iman & Umar)Akmal HaziqNo ratings yet

- Chapter 13 The Stock Market: Financial Markets and Institutions, 7e (Mishkin)Document11 pagesChapter 13 The Stock Market: Financial Markets and Institutions, 7e (Mishkin)Yousef ADNo ratings yet