Download as pdf or txt

You might also like

- Case 1 - Financial Statements 2014 Using Financial Ratios To Identify CompaniesDocument3 pagesCase 1 - Financial Statements 2014 Using Financial Ratios To Identify CompaniesFarhanie Nordin0% (1)

- Book BuildingDocument24 pagesBook Buildingmariam_abbasi5100% (2)

- HW Listening - StartupsDocument2 pagesHW Listening - StartupsLuis Manuel JuárezNo ratings yet

- USA Eco Indicators Dashboard - Consumer Spending, Confidence & SentimentDocument1 pageUSA Eco Indicators Dashboard - Consumer Spending, Confidence & SentimentWallstreetableNo ratings yet

- By David Harding and Georgia Nakou, Winton Capital ManagementDocument5 pagesBy David Harding and Georgia Nakou, Winton Capital ManagementCoco BungbingNo ratings yet

- HCL Infosystems Limited: HCL & Nokia - Long Term Distribution StrategyDocument8 pagesHCL Infosystems Limited: HCL & Nokia - Long Term Distribution Strategyajitprasad01No ratings yet

- 3 MF Portfolios To Build in This Market-Sharekhan-202004Document14 pages3 MF Portfolios To Build in This Market-Sharekhan-202004vikuNo ratings yet

- Oracle Database 11g OverviewDocument46 pagesOracle Database 11g OverviewEddie Awad91% (11)

- 434311562motilal Oswal Passive Funds PitchBook 31 Jul 2020 - V2Document95 pages434311562motilal Oswal Passive Funds PitchBook 31 Jul 2020 - V2dabster7000No ratings yet

- Invest Update - January 2011Document8 pagesInvest Update - January 2011geetanjali04No ratings yet

- 5 Trends Defining The Future of ManufacturingDocument42 pages5 Trends Defining The Future of ManufacturingTurant SundariNo ratings yet

- Use of Boolean in FTADocument46 pagesUse of Boolean in FTAManoj MishraNo ratings yet

- Managing The Financial Crisis: Argentina (2002)Document63 pagesManaging The Financial Crisis: Argentina (2002)ankushishwarNo ratings yet

- Isbl OsblDocument3 pagesIsbl OsblDina RosmaNo ratings yet

- Baltimore Metropolitan Area: Market ReportDocument21 pagesBaltimore Metropolitan Area: Market ReportAnonymous Feglbx5No ratings yet

- JUL 23 BBVA Global Weekly WatchDocument6 pagesJUL 23 BBVA Global Weekly WatchMiir ViirNo ratings yet

- GDP (RHS) M2 Loans M1 DPK: Dsta - Divisi Statistik Moneter Dan FiskalDocument7 pagesGDP (RHS) M2 Loans M1 DPK: Dsta - Divisi Statistik Moneter Dan FiskalHurin Aghnia Nur AinaniNo ratings yet

- Jan Hatzius Economic Outlook October 2022Document41 pagesJan Hatzius Economic Outlook October 2022VolgaNo ratings yet

- "Planning Your Financial Future": Mangala Boyagoda 26 October 2010Document71 pages"Planning Your Financial Future": Mangala Boyagoda 26 October 2010Inde Pendent LkNo ratings yet

- AltairDocument1 pageAltairjozefRudyNo ratings yet

- Southeast Texas Labor StatisticsDocument1 pageSoutheast Texas Labor StatisticsCharlie FoxworthNo ratings yet

- Growth-Trend Timing and 60-40 Variations: Lethargic Asset Allocation (LAA)Document15 pagesGrowth-Trend Timing and 60-40 Variations: Lethargic Asset Allocation (LAA)Ricardo GutierrezNo ratings yet

- Flex 2 BasicsDocument15 pagesFlex 2 Basicsapi-3768994No ratings yet

- Ideas & InsightsDocument2 pagesIdeas & Insightsag rNo ratings yet

- Libro Modulo III Capítulo 3 - 9 (Koch y Macdonald)Document185 pagesLibro Modulo III Capítulo 3 - 9 (Koch y Macdonald)Remy Angel Terceros FernandezNo ratings yet

- Central Bank Monetary Policy Analysis: - Guillermo Varela HerreraDocument6 pagesCentral Bank Monetary Policy Analysis: - Guillermo Varela HerreraGuillermo VarelaNo ratings yet

- August 2010 - Bethesda 20816 Market StatsDocument3 pagesAugust 2010 - Bethesda 20816 Market StatsJosette SkillingNo ratings yet

- PMI SL Purchasing Managers' IndexDocument2 pagesPMI SL Purchasing Managers' IndexSemitha KanakarathnaNo ratings yet

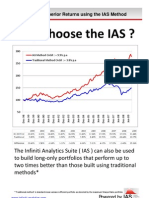

- Why Choose The IASDocument6 pagesWhy Choose The IASPeter UrbaniNo ratings yet

- Informe - Mesto Local - Feb 24Document2 pagesInforme - Mesto Local - Feb 24franjazstoreNo ratings yet

- Exponential Appreciation Fund, LP: December 2021Document2 pagesExponential Appreciation Fund, LP: December 2021Moiz SaeedNo ratings yet

- Innovation and The Financial CrisisDocument20 pagesInnovation and The Financial Crisisttunguz100% (3)

- Primera PlantaDocument1 pagePrimera PlantaGerson AlvaradoNo ratings yet

- PMI SL Purchasing Managers' IndexDocument2 pagesPMI SL Purchasing Managers' IndexSemitha KanakarathnaNo ratings yet

- Msci Ac Asia Pacific Islamic Index Usd GrossDocument3 pagesMsci Ac Asia Pacific Islamic Index Usd GrossAristo Elyan TambuwunNo ratings yet

- Finance in Africa 2023 Mfw4aDocument15 pagesFinance in Africa 2023 Mfw4aahamadouibt4No ratings yet

- ENRM 2002 - Energy Resources and Sustainability Lecture 3 SOLAR and HYDRO RandyRamadharSinghDocument48 pagesENRM 2002 - Energy Resources and Sustainability Lecture 3 SOLAR and HYDRO RandyRamadharSinghRandy Ramadhar SinghNo ratings yet

- Gmo - For Whom The Bond TollsDocument8 pagesGmo - For Whom The Bond Tollsfreemind3682No ratings yet

- Equity Debt Strategy For Mar20Document25 pagesEquity Debt Strategy For Mar20Saad KhanNo ratings yet

- Research Speak 25-6-2010Document12 pagesResearch Speak 25-6-2010A_KinshukNo ratings yet

- Report of The Technical Group On Money Market: Reserve Bank of India May 2005Document29 pagesReport of The Technical Group On Money Market: Reserve Bank of India May 2005api-27174321No ratings yet

- Sensex Market Cap To GDP: Mcap To GDP (Popularly Known As Buffet Indicator)Document4 pagesSensex Market Cap To GDP: Mcap To GDP (Popularly Known As Buffet Indicator)Ankeet ShahNo ratings yet

- Liquidity Risk in Corporate Bond Markets: George Chacko Harvard Business School & IFLDocument26 pagesLiquidity Risk in Corporate Bond Markets: George Chacko Harvard Business School & IFLbadaberaNo ratings yet

- Dpto - 305 Dpto - 306: Se Reduce Y Estandariza Ventana M-31Document1 pageDpto - 305 Dpto - 306: Se Reduce Y Estandariza Ventana M-31GF Del Toro LlamojaNo ratings yet

- 3 RDDocument1 page3 RDBurka DinkaNo ratings yet

- 4Document1 page4Nana BarimaNo ratings yet

- Maintenance Trend Chaart-2024Document3 pagesMaintenance Trend Chaart-2024cghodake1No ratings yet

- MSCI Frontier Markets Small Cap Index (USD)Document3 pagesMSCI Frontier Markets Small Cap Index (USD)Cường KhuấtNo ratings yet

- 65a47e42103b033fe1f1fd6a - Re-Hub - The China Luxury Playbook - January 2024Document17 pages65a47e42103b033fe1f1fd6a - Re-Hub - The China Luxury Playbook - January 202426xvbrb27xNo ratings yet

- Arq - 01Document1 pageArq - 01Jimmy Barzola BautistaNo ratings yet

- R03 Quality Objectives and Action PlansDocument6 pagesR03 Quality Objectives and Action PlansMhyra BellezaNo ratings yet

- HR Report 2022 Ms Abdulwahab Al-HatafDocument13 pagesHR Report 2022 Ms Abdulwahab Al-Hatafabdulwahab alhatefNo ratings yet

- 1.16 Whitehall: Monitoring The Markets Vol. 1 Iss. 16 (May 17, 2011)Document2 pages1.16 Whitehall: Monitoring The Markets Vol. 1 Iss. 16 (May 17, 2011)Whitehall & Company0% (1)

- LBSL Weekly Stock Report 25 May 2023Document13 pagesLBSL Weekly Stock Report 25 May 2023mahmudaNo ratings yet

- Primer Piso: CL. Dormitorio PrincipalDocument1 pagePrimer Piso: CL. Dormitorio PrincipalJimy Rioja HuacchaNo ratings yet

- TexasDocument1 pageTexasDjibzlaeNo ratings yet

- Chapter 07Document20 pagesChapter 07primantNo ratings yet

- Maths & YouDocument499 pagesMaths & YouOctavio M RuizNo ratings yet

- Philippine Rice Trade Liberalization: Impacts On Agriculture and The Economy, and Alternative Policy ActionsDocument12 pagesPhilippine Rice Trade Liberalization: Impacts On Agriculture and The Economy, and Alternative Policy ActionsJofred Dela VegaNo ratings yet

- Applied Time Series Econometrics: A Practical Guide for Macroeconomic Researchers with a Focus on AfricaFrom EverandApplied Time Series Econometrics: A Practical Guide for Macroeconomic Researchers with a Focus on AfricaRating: 3 out of 5 stars3/5 (1)

- Slideshare Is A: Web 2.0 Slide Hosting Service Powerpoint PDF Keynote Opendocument Slide Decks Embedded YoutubeDocument1 pageSlideshare Is A: Web 2.0 Slide Hosting Service Powerpoint PDF Keynote Opendocument Slide Decks Embedded YoutubeAmik TandelNo ratings yet

- Sun PharmaDocument6 pagesSun PharmaAmik TandelNo ratings yet

- Sports Management CompaniesDocument6 pagesSports Management CompaniesAmik TandelNo ratings yet

- Leadership and ManagementDocument11 pagesLeadership and ManagementAmik TandelNo ratings yet

- CBB TestDocument1 pageCBB TestAmik TandelNo ratings yet

- Quasi ReorganizationDocument3 pagesQuasi ReorganizationBeth Diaz LaurenteNo ratings yet

- ABC BearingsDocument2 pagesABC Bearingssarvesh_samdaniNo ratings yet

- Listed Companies Listing-Guide Book PDFDocument49 pagesListed Companies Listing-Guide Book PDF유웃No ratings yet

- Role of Financial Institutional Investors in Capital Market in IndiaDocument86 pagesRole of Financial Institutional Investors in Capital Market in Indiaron8772100% (13)

- Foreclosure & Redemption: A Detailed Analysis: A Project Report OnDocument18 pagesForeclosure & Redemption: A Detailed Analysis: A Project Report OnAnantHimanshuEkka100% (1)

- Financial ScandalsDocument16 pagesFinancial ScandalsGlen Joy Ganancial0% (1)

- Human Resource AuditDocument2 pagesHuman Resource AuditDylan WilcoxNo ratings yet

- Cboe - Options CoursesDocument3 pagesCboe - Options CoursesAnju ShahNo ratings yet

- Port-Folio Management: Module Code: MBA 721Document31 pagesPort-Folio Management: Module Code: MBA 721RabiaChaudhryNo ratings yet

- Ara Asset Management: Analyst Research ReportDocument33 pagesAra Asset Management: Analyst Research Reporthi_chrisleeNo ratings yet

- Katalyst Wealth - A Free Guide To Grow Your Wealth by 190 TimesDocument21 pagesKatalyst Wealth - A Free Guide To Grow Your Wealth by 190 TimesKatalyst WealthNo ratings yet

- CH 15Document25 pagesCH 15SaAl-ismailNo ratings yet

- Advance Accounting Week 2 Homework 1Document3 pagesAdvance Accounting Week 2 Homework 1Nabila Nur IzzaNo ratings yet

- A Comprehensive Review On Capital Structure TheoriesDocument24 pagesA Comprehensive Review On Capital Structure TheoriesCristian Buffalo SlobodeaniucNo ratings yet

- Pas 1: Presentation of Financial StatementsDocument9 pagesPas 1: Presentation of Financial StatementsJung Jeon0% (1)

- WhiteMonk HEG Equity Research ReportDocument15 pagesWhiteMonk HEG Equity Research ReportgirishamrNo ratings yet

- Investment in Equity SecuritiesDocument23 pagesInvestment in Equity SecuritiesJay-L TanNo ratings yet

- CH 4Document59 pagesCH 4ad_jebbNo ratings yet

- Financial Management BasicsDocument19 pagesFinancial Management BasicsAnkith NukulNo ratings yet

- Irins Expert Advisor v1.8 Manual FileDocument6 pagesIrins Expert Advisor v1.8 Manual FileMichael NabuaNo ratings yet

- Investor Definition: What Is An Investor?Document8 pagesInvestor Definition: What Is An Investor?Christine DavidNo ratings yet

- AFIN1Document6 pagesAFIN1Abs PangaderNo ratings yet

- Opposition To Pabst MSJDocument26 pagesOpposition To Pabst MSJTHROnlineNo ratings yet

- Efficient Capital MarketsDocument25 pagesEfficient Capital MarketsAshik Ahmed NahidNo ratings yet

- Kedaara CapitalDocument3 pagesKedaara CapitalALLtyNo ratings yet

- Project Report On Technical AnalysisDocument56 pagesProject Report On Technical AnalysisPrashant GaikarNo ratings yet

- ICICI Pru Balanced Advantage Fund - PortfolioDocument2 pagesICICI Pru Balanced Advantage Fund - PortfolioSunil ChaudharyNo ratings yet