Download as doc, pdf, or txt

You might also like

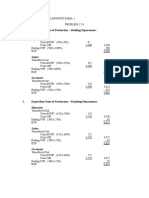

- 6 Alvaro, Fernel Jean C. AE212-1742 TTHS 3-5PM ExercisesDocument7 pages6 Alvaro, Fernel Jean C. AE212-1742 TTHS 3-5PM ExercisesNhel Alvaro100% (1)

- Process and Job Order Costing - EditedDocument6 pagesProcess and Job Order Costing - EditedJasper Andrew AdjaraniNo ratings yet

- Cost Accounting Reviewer (Finals)Document11 pagesCost Accounting Reviewer (Finals)Cho AndreaNo ratings yet

- 1Document2 pages1Your MaterialsNo ratings yet

- Practical Earned Value Analysis: 25 Project Indicators from 5 MeasurementsFrom EverandPractical Earned Value Analysis: 25 Project Indicators from 5 MeasurementsNo ratings yet

- Cont HSE Alignment Kickoff Meeting F0228Document2 pagesCont HSE Alignment Kickoff Meeting F0228NAGARJUNA75% (4)

- RFP For End To End Reconciliation of Debit Card Transactions and ATMsDocument111 pagesRFP For End To End Reconciliation of Debit Card Transactions and ATMsGilbert KamanziNo ratings yet

- Halal Industry Master Plan: P Ro M in enDocument16 pagesHalal Industry Master Plan: P Ro M in enNote 8100% (1)

- SCF 07 Quality ManagementDocument48 pagesSCF 07 Quality ManagementGyorgy LukacsNo ratings yet

- Cost of Production Report - Average CostingDocument12 pagesCost of Production Report - Average CostingKhai Ed PabelicoNo ratings yet

- 10 Cost of Production Report FIFODocument21 pages10 Cost of Production Report FIFOephreenNo ratings yet

- 9 Cost of Production Report AVERAGEDocument22 pages9 Cost of Production Report AVERAGEephreenNo ratings yet

- Average Method Department 2 Equivalent Units of ProductionDocument5 pagesAverage Method Department 2 Equivalent Units of ProductionRoschelle MiguelNo ratings yet

- Illustration 13-11 Cutting Department Equivalent Production Computations-FIFO Month of February 2018Document10 pagesIllustration 13-11 Cutting Department Equivalent Production Computations-FIFO Month of February 2018studentoneNo ratings yet

- Module No 2 - Average CostingDocument8 pagesModule No 2 - Average CostingAnthony DyNo ratings yet

- Module No 4 Accounting For Spoiled UnitsDocument18 pagesModule No 4 Accounting For Spoiled UnitsAnnabelle RafolsNo ratings yet

- Multiple Choices - TheoreticalDocument8 pagesMultiple Choices - TheoreticalIsabelle AmbataliNo ratings yet

- Problem 10-10 COSTDocument3 pagesProblem 10-10 COSTElaine Fiona VillafuerteNo ratings yet

- Illustration - Cost of Production ReportDocument9 pagesIllustration - Cost of Production ReportJomari FalibleNo ratings yet

- Process CostingDocument15 pagesProcess CostingJake BorinagaNo ratings yet

- Molding Department Equivalent Production Computations Month of June MaterialsDocument5 pagesMolding Department Equivalent Production Computations Month of June MaterialsGwyneth Jhane Ybañez LibosadaNo ratings yet

- Work in Process, Beginning:: Required: Prepare A Production Report For The Department Using The Weighted-Average MethodDocument6 pagesWork in Process, Beginning:: Required: Prepare A Production Report For The Department Using The Weighted-Average MethodJhunorlando DisonoNo ratings yet

- Ae212 Exercise 7-3 To 7-6Document7 pagesAe212 Exercise 7-3 To 7-6Nhel AlvaroNo ratings yet

- Practice Problems With Answers - Process Costing Average MethodDocument3 pagesPractice Problems With Answers - Process Costing Average MethodAndrea ValdezNo ratings yet

- Chapter 13-1, 13-7 & 13-9Document5 pagesChapter 13-1, 13-7 & 13-9Elaine Fiona VillafuerteNo ratings yet

- Ae 211 Module 6 - Exercise 6-5 To 6-9Document7 pagesAe 211 Module 6 - Exercise 6-5 To 6-9Nhel AlvaroNo ratings yet

- Pa2.M-1403 Process CostingDocument16 pagesPa2.M-1403 Process CostingJeric Israel0% (3)

- Exercise 7-3 To 7-6Document6 pagesExercise 7-3 To 7-6Nhel AlvaroNo ratings yet

- ProcessDocument11 pagesProcessElaine YapNo ratings yet

- AP 1402 CashDocument13 pagesAP 1402 CashElaine YapNo ratings yet

- Assembly Department Equivalent Units of Production Month of May 2018Document9 pagesAssembly Department Equivalent Units of Production Month of May 2018Gileah Ymalay ZuasolaNo ratings yet

- Chapter V: Process Cost Accounting - General ProceduresDocument3 pagesChapter V: Process Cost Accounting - General ProceduresSweet Jenesie MirandaNo ratings yet

- Process CostingDocument3 pagesProcess CostingenzoNo ratings yet

- Materials:: PROBLEM 12-8 1. Equivalent Units of Production - Molding DepartmentDocument7 pagesMaterials:: PROBLEM 12-8 1. Equivalent Units of Production - Molding DepartmentGileah Ymalay ZuasolaNo ratings yet

- Materials Labor Overhead: Equivalent Units For MaterialsDocument25 pagesMaterials Labor Overhead: Equivalent Units For MaterialsShaira Mica SanitaNo ratings yet

- Advance Financial Accounting and Reporting Padj/Rf: Process Costing A. ProblemsDocument4 pagesAdvance Financial Accounting and Reporting Padj/Rf: Process Costing A. ProblemsRoxell CaibogNo ratings yet

- Process CostingDocument4 pagesProcess CostingAndrea Nicole MASANGKAY100% (1)

- Process Costing Single Dept. 2024Document7 pagesProcess Costing Single Dept. 2024riza utboNo ratings yet

- Pamantasan NG Lungsod NG Valenzuela Junior Philippine Institute of Accountants Ate-Kuya System 2019: Cost AccountingDocument2 pagesPamantasan NG Lungsod NG Valenzuela Junior Philippine Institute of Accountants Ate-Kuya System 2019: Cost AccountingJea SegumalianNo ratings yet

- Mock Exam Cost Acct 2023Document6 pagesMock Exam Cost Acct 2023Lam HảiNo ratings yet

- Cost of Production ReportDocument10 pagesCost of Production ReportNo NotreallyNo ratings yet

- 05.16.2023 ASSIGNMENT Activity Problem With Theories-Process Costing and JOB Order Costing - With ANSWER KEYDocument11 pages05.16.2023 ASSIGNMENT Activity Problem With Theories-Process Costing and JOB Order Costing - With ANSWER KEYAngel Cil RuleteNo ratings yet

- Process Costing - CompleeteDocument42 pagesProcess Costing - CompleeteKarimatun NisaNo ratings yet

- ACCTG 201 Illustrative ProblemsDocument4 pagesACCTG 201 Illustrative ProblemsJewel Anne RentumaNo ratings yet

- Equivalent Units of Production - Molding Department:: MaterialsDocument3 pagesEquivalent Units of Production - Molding Department:: MaterialsElaine Fiona VillafuerteNo ratings yet

- CostaccDocument4 pagesCostaccjaringanlimagNo ratings yet

- CostAccountingModule FinalPeriod2022Document25 pagesCostAccountingModule FinalPeriod2022Jr Reyes PedidaNo ratings yet

- Lecture 11 Process Costing - 2ndDocument35 pagesLecture 11 Process Costing - 2ndMahyy AdelNo ratings yet

- CHAPTER FOUR Process CostingDocument10 pagesCHAPTER FOUR Process Costingzewdie100% (1)

- Lecture Normal CostingDocument3 pagesLecture Normal CostingwaddeornNo ratings yet

- AKS 2019 Cost Accounting-Lecture-01Document4 pagesAKS 2019 Cost Accounting-Lecture-01Kyle Christian Sandiego FernandoNo ratings yet

- DocDocument8 pagesDocJAY AUBREY PINEDANo ratings yet

- Final ExamDocument4 pagesFinal ExamJojo EstebanNo ratings yet

- Process-Additional CPAR PDFDocument15 pagesProcess-Additional CPAR PDFomer 2 gerdNo ratings yet

- Long QuizDocument4 pagesLong QuizJoshua Rey Sapuras0% (1)

- Flow of Production Physical Units Equivalent Units Direct Materials Conversion CostsDocument2 pagesFlow of Production Physical Units Equivalent Units Direct Materials Conversion CostsMuhamad Ihsan RafiansyahNo ratings yet

- Quiz 1 Problem Sol1Document9 pagesQuiz 1 Problem Sol1acidoleannamaeNo ratings yet

- Process Costing Pa MoreDocument3 pagesProcess Costing Pa MoreAlle NadroNo ratings yet

- Class Case For Chapter 17 2015 AdjustedDocument8 pagesClass Case For Chapter 17 2015 Adjustedahmed.alaradi88No ratings yet

- Process CostingDocument2 pagesProcess CostingLyre LevierNo ratings yet

- 13 Dela Cruz - Discussion Questions and Problems PDFDocument15 pages13 Dela Cruz - Discussion Questions and Problems PDFMau Dela CruzNo ratings yet

- Quiz1 AdvcostDocument8 pagesQuiz1 AdvcostPatOcampo100% (3)

- 17-16 (25 Min.) Equivalent Units, Zero Beginning InventoryDocument5 pages17-16 (25 Min.) Equivalent Units, Zero Beginning Inventorymohamet farahNo ratings yet

- Completing The Cost Cycle and Accounting For Production LossesDocument10 pagesCompleting The Cost Cycle and Accounting For Production LossesKhai Ed PabelicoNo ratings yet

- Cost of Production Report - Average CostingDocument12 pagesCost of Production Report - Average CostingKhai Ed PabelicoNo ratings yet

- Chapter 5 - Labor Accounting - Control and Costing Timekeeping ProceduresDocument6 pagesChapter 5 - Labor Accounting - Control and Costing Timekeeping ProceduresKhai Ed PabelicoNo ratings yet

- Cash Bank ReconciliationDocument1 pageCash Bank ReconciliationKhai Ed PabelicoNo ratings yet

- Chapter 7 - Manufacturing Overhead - Departmentalization Need For DepartmentalizationDocument11 pagesChapter 7 - Manufacturing Overhead - Departmentalization Need For DepartmentalizationKhai Ed PabelicoNo ratings yet

- Financial Accounting QuizDocument11 pagesFinancial Accounting QuizKhai Ed PabelicoNo ratings yet

- Doubtful Accounts DemonstrationDocument25 pagesDoubtful Accounts DemonstrationKhai Ed PabelicoNo ratings yet

- (03A) AR NR Quiz ANSWER KEYDocument8 pages(03A) AR NR Quiz ANSWER KEYKhai Ed PabelicoNo ratings yet

- Business Process TestingDocument25 pagesBusiness Process TestingHardikJindalNo ratings yet

- Credit Sources and Credit CardsDocument11 pagesCredit Sources and Credit CardsPoonam VermaNo ratings yet

- BrochureDocument8 pagesBrochureClyde RetanalNo ratings yet

- Nacpil Vs IBCDocument2 pagesNacpil Vs IBCNiñanne Nicole Baring BalbuenaNo ratings yet

- SAP CRM Technical CourseDocument8 pagesSAP CRM Technical CoursesupreethNo ratings yet

- Orifice SpinkDocument13 pagesOrifice SpinkAlejandro Hernandez TapiaNo ratings yet

- Assessing The Effectiveness of The Internal Control System in The Commercial Banks of Ethiopia: A Case of Hawassa CityDocument5 pagesAssessing The Effectiveness of The Internal Control System in The Commercial Banks of Ethiopia: A Case of Hawassa CityIjsrnet EditorialNo ratings yet

- Market Analysis and Study On Amul Milk IndustryDocument39 pagesMarket Analysis and Study On Amul Milk IndustrysanuNo ratings yet

- Sums For Practice in StatisticsDocument5 pagesSums For Practice in StatisticsRahul WaniNo ratings yet

- EntreprenuershipDocument14 pagesEntreprenuershippeace.missileNo ratings yet

- MisDocument17 pagesMisAyan SnehashisNo ratings yet

- Cold Chain and Energy ManagementDocument14 pagesCold Chain and Energy ManagementKalejaiye Adedayo100% (1)

- Competitor Analysis FINALDocument3 pagesCompetitor Analysis FINALbaculandojennifer9No ratings yet

- 0731 I K JG 000169791Document1 page0731 I K JG 000169791Fikri FarhanNo ratings yet

- Scheme Name Plan Category NameDocument8 pagesScheme Name Plan Category NamePriyamGhoshNo ratings yet

- Applied EconomicsDocument5 pagesApplied EconomicsMaritess Madrid EsperanzaNo ratings yet

- (Funds Settlement) : NSE - Valuation Debit, Valuation Price, Bad and Short Delivery, AuctionDocument2 pages(Funds Settlement) : NSE - Valuation Debit, Valuation Price, Bad and Short Delivery, AuctionHRish BhimberNo ratings yet

- Comparative Analysis of Oyo & Ginger Grp-9 PDFDocument31 pagesComparative Analysis of Oyo & Ginger Grp-9 PDFadityakr2410100% (1)

- Shinny Jewel C. Vingno BSA-2 Problem 1-18Document7 pagesShinny Jewel C. Vingno BSA-2 Problem 1-18Shinny Jewel VingnoNo ratings yet

- SBA Ombudsman Bio - Esther VassarDocument2 pagesSBA Ombudsman Bio - Esther VassarVirgin Islands Youth Advocacy CoalitionNo ratings yet

- Johnstone 9e Auditing Chapter8 PPtFINALDocument73 pagesJohnstone 9e Auditing Chapter8 PPtFINALDakotaMontanaNo ratings yet

- Afm 311 A - 2013Document8 pagesAfm 311 A - 2013Dolly VongweNo ratings yet

- PIADocument146 pagesPIAOwais SabirNo ratings yet

- RUTAGDocument3 pagesRUTAGRidwan AhmedNo ratings yet

- Tibco OverviewDocument8 pagesTibco OverviewJackson WanjohiNo ratings yet

- Material - Debt Investment (Batch 19)Document9 pagesMaterial - Debt Investment (Batch 19)ljaneNo ratings yet