Download as docx, pdf, or txt

You might also like

- Tutorial - Financial StatementDocument18 pagesTutorial - Financial StatementmellNo ratings yet

- QUIZ - CHAPTER 15 - PPE PART 1 - 2020edDocument3 pagesQUIZ - CHAPTER 15 - PPE PART 1 - 2020edjanna napili100% (1)

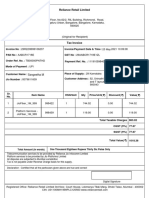

- Reliance Retail Limited: Sangeetha MDocument3 pagesReliance Retail Limited: Sangeetha MHariharan RNo ratings yet

- PGP I 2021 Fra Quiz 1Document3 pagesPGP I 2021 Fra Quiz 1Pulkit SethiaNo ratings yet

- Exercises On Formation of Final Accounts: Particulars Amount AmountDocument4 pagesExercises On Formation of Final Accounts: Particulars Amount AmountNeelu AggrawalNo ratings yet

- ACC 281 SEMINAR QUESTIONS Version 2Document8 pagesACC 281 SEMINAR QUESTIONS Version 2Joel SimonNo ratings yet

- Baf 1201 Fa2Document3 pagesBaf 1201 Fa2ReginaNo ratings yet

- Mdarasa PFT CAT 1 - SEM 1 2024Document4 pagesMdarasa PFT CAT 1 - SEM 1 2024Sam OwinoNo ratings yet

- Kenya Methodist University: Endof2 Trimester 2021 ExaminationsDocument6 pagesKenya Methodist University: Endof2 Trimester 2021 ExaminationsJoe 254No ratings yet

- ADVANCED ACC - Revision ParkDocument20 pagesADVANCED ACC - Revision ParkTimothy KawumaNo ratings yet

- Trial Balance As On 31Document3 pagesTrial Balance As On 31Lipson ThomasNo ratings yet

- Manufacturing Accounts - Extra Questions - A LevelDocument6 pagesManufacturing Accounts - Extra Questions - A LevelMUSTHARI KHANNo ratings yet

- Ugbs 208 Assignment OneDocument3 pagesUgbs 208 Assignment Onequarcoonathaniel025No ratings yet

- Cost & Management - X Is The Manufacture of MumbaiDocument6 pagesCost & Management - X Is The Manufacture of MumbaiSailpoint CourseNo ratings yet

- BACC 233 Assignment 2 Jan-Jun 2024Document5 pagesBACC 233 Assignment 2 Jan-Jun 2024TarusengaNo ratings yet

- BFC 3225 Intermediate Accounting I 2 - 2Document6 pagesBFC 3225 Intermediate Accounting I 2 - 2karashinokov siwoNo ratings yet

- Lecture 6 - Practice Questions-1Document4 pagesLecture 6 - Practice Questions-1donkhalif13No ratings yet

- Accounting - X Is The Manufacture of MumbaiDocument4 pagesAccounting - X Is The Manufacture of MumbaiSailpoint CourseNo ratings yet

- Business Income IllustrationsDocument12 pagesBusiness Income IllustrationsPatricia NjeriNo ratings yet

- Quiz 3 Ppe QuestionsDocument4 pagesQuiz 3 Ppe QuestionsJessica Marie MigrasoNo ratings yet

- Exercises On Formation of Final Accounts: Particulars Amount AmountDocument4 pagesExercises On Formation of Final Accounts: Particulars Amount AmountNeelu AggrawalNo ratings yet

- Final Accounts Practice QuestionDocument12 pagesFinal Accounts Practice QuestionMadhav AgarwalNo ratings yet

- Lecture 4 Part 2 - QuestionDocument4 pagesLecture 4 Part 2 - QuestionIsyraf Hatim Mohd TamizamNo ratings yet

- Acc.2023 Practical Exam Sample QN - PaperDocument5 pagesAcc.2023 Practical Exam Sample QN - PaperMidhun PerozhiNo ratings yet

- Cost AccountingDocument3 pagesCost AccountingXen XeonNo ratings yet

- Unit 1 B&P ExamplesDocument9 pagesUnit 1 B&P ExamplesAllaretrashNo ratings yet

- CPA Taxation Part 1 Section 3 QuestionsDocument5 pagesCPA Taxation Part 1 Section 3 QuestionsVictory NyamburaNo ratings yet

- Taxation Module 3: Numerical Problems Income From Business or ProfessionDocument5 pagesTaxation Module 3: Numerical Problems Income From Business or ProfessionShankar HunnurNo ratings yet

- Adjusting Entries From The Desk F JASDocument3 pagesAdjusting Entries From The Desk F JASMalik of ChakwalNo ratings yet

- 2.manufacturing Accounts IllustrationDocument2 pages2.manufacturing Accounts Illustrationdaniel.maina2005No ratings yet

- Presentation1 ReshmaDocument26 pagesPresentation1 ReshmaJOE NOBLE 2020519No ratings yet

- 201.AFA IP.L II December 2020Document4 pages201.AFA IP.L II December 2020leyaketjnuNo ratings yet

- Higher National Diploma in Accountancy Hnda 2 Year, Second Semester Examination - 2018 2202-Computer Applications For AccountingDocument14 pagesHigher National Diploma in Accountancy Hnda 2 Year, Second Semester Examination - 2018 2202-Computer Applications For AccountingName of RoshanNo ratings yet

- Department of Commerce 1 Semester Exam 2020/2021 Grade 11 Accounting Page 1 of 9Document9 pagesDepartment of Commerce 1 Semester Exam 2020/2021 Grade 11 Accounting Page 1 of 9Eshal KhanNo ratings yet

- Acc 221-Ias 1 - 032313Document15 pagesAcc 221-Ias 1 - 032313Rahman OmaryNo ratings yet

- Quiz - Topic 5Document3 pagesQuiz - Topic 5mariakate LeeNo ratings yet

- Hba 2302 Advanced TaxationDocument4 pagesHba 2302 Advanced TaxationprescoviaNo ratings yet

- M.B.A (2019 Pattern)Document157 pagesM.B.A (2019 Pattern)girishpawarudgirkarNo ratings yet

- FUFA Question Paper - Compre - FOFA (ECON F212) 1st Sem 2018-19Document2 pagesFUFA Question Paper - Compre - FOFA (ECON F212) 1st Sem 2018-19vineetchahar0210No ratings yet

- Module 3 - SW On MFTG Acctg & CfsDocument2 pagesModule 3 - SW On MFTG Acctg & CfsestebandgonoNo ratings yet

- Ias 1 - Questions..Document8 pagesIas 1 - Questions..Timothy KawumaNo ratings yet

- Company Final Accounts: Debit Rs. Credit RsDocument5 pagesCompany Final Accounts: Debit Rs. Credit RsDebaditya SenguptaNo ratings yet

- Adjustments To Financial Statements Tutorial No: 13Document6 pagesAdjustments To Financial Statements Tutorial No: 13me myselfNo ratings yet

- Financial Reporting and Analysis Assignment 03 Finalising Transactions 005 (1) - 2Document7 pagesFinancial Reporting and Analysis Assignment 03 Finalising Transactions 005 (1) - 2SuryaNo ratings yet

- Company Financial StatementsDocument6 pagesCompany Financial StatementsHasnain MahmoodNo ratings yet

- Unit IDocument10 pagesUnit IkuselvNo ratings yet

- November 2020 Professional Examiniations Public Sector Accounting and Finance (Paper 2.5) Chief Examiner'S Report, Questions and Marking SchemeDocument23 pagesNovember 2020 Professional Examiniations Public Sector Accounting and Finance (Paper 2.5) Chief Examiner'S Report, Questions and Marking SchemeThomas nyadeNo ratings yet

- Revision Sheet - 2023 - 2024Document27 pagesRevision Sheet - 2023 - 2024Yuvraj Chaudhari100% (1)

- PPE ReviewerDocument13 pagesPPE ReviewerMariel DichosoNo ratings yet

- Worksheet AccountingDocument5 pagesWorksheet AccountingDorinNo ratings yet

- Ac QuestionsDocument7 pagesAc QuestionssamsherbdtamangNo ratings yet

- Financial Statements - BasicDocument5 pagesFinancial Statements - BasicMohamed MubarakNo ratings yet

- The Following List of Accounts For Company Y Ltd. Is Available at The End of 200XDocument2 pagesThe Following List of Accounts For Company Y Ltd. Is Available at The End of 200Xai0412No ratings yet

- Test TB Final Ac Single EntryDocument2 pagesTest TB Final Ac Single EntryMegha BhargavaNo ratings yet

- C.A. Foundation Final Accounts For Sole Proprietorship QuestionsDocument2 pagesC.A. Foundation Final Accounts For Sole Proprietorship Questionsgpgaming1693No ratings yet

- 1.3 เฉลย File 1.1 Ch 1 2-2022Document14 pages1.3 เฉลย File 1.1 Ch 1 2-2022Chokthawee RattanawetwongNo ratings yet

- Daa 101 Introduction To Accounting Ii - RispahDocument4 pagesDaa 101 Introduction To Accounting Ii - RispahSpencerNo ratings yet

- O Level Important Questions PDFDocument55 pagesO Level Important Questions PDFibraho100% (1)

- Assignment Final AccountsDocument9 pagesAssignment Final Accountsjasmine chowdhary50% (2)

- CA Inter Costing Practical Questions With SolutionsDocument311 pagesCA Inter Costing Practical Questions With SolutionsAnkit KumarNo ratings yet

- Chapter 16 Practice Problems Solution Manual 2020Document29 pagesChapter 16 Practice Problems Solution Manual 2020James SeelosNo ratings yet

- Annual Gross IncomeDocument4 pagesAnnual Gross IncomeMarilyn Perez OlañoNo ratings yet

- Flytxt - ECB Interest - Form 15CB - 21 Nov 22Document4 pagesFlytxt - ECB Interest - Form 15CB - 21 Nov 22RahulNo ratings yet

- Ethiopian Tax System CH 4Document59 pagesEthiopian Tax System CH 4Kefi Belay100% (7)

- Bar Examination 2006 - TaxationlawDocument7 pagesBar Examination 2006 - TaxationlawLyraNo ratings yet

- COMM 229 Notes Chapter 2:3Document2 pagesCOMM 229 Notes Chapter 2:3Cody ClinkardNo ratings yet

- Um Tagum College Department of Accounting Education: Daily Accomplishment ReportDocument10 pagesUm Tagum College Department of Accounting Education: Daily Accomplishment ReportRose Ann Juleth LicayanNo ratings yet

- Certification: Name of Employee Taxpayer Identification Number Amount of Compensation Tax Due Withheld and RemittedDocument5 pagesCertification: Name of Employee Taxpayer Identification Number Amount of Compensation Tax Due Withheld and RemittedEmman JavierNo ratings yet

- Template - Problem 18.1Document4 pagesTemplate - Problem 18.1dragonx0662No ratings yet

- Advanced Taxation - Singapore (Atx - SGP) : Strategic Professional - OptionsDocument12 pagesAdvanced Taxation - Singapore (Atx - SGP) : Strategic Professional - Optionsnivethababu7No ratings yet

- Cincinnati FY 2023 Budget PresentationDocument12 pagesCincinnati FY 2023 Budget PresentationWVXU NewsNo ratings yet

- Income From House PropertyDocument27 pagesIncome From House PropertyJames Anderson0% (1)

- Goods & Services Tax 2017: It's Application and CalculationDocument14 pagesGoods & Services Tax 2017: It's Application and CalculationayushNo ratings yet

- 02-2004 Vat Philippine Port Authority PpaDocument3 pages02-2004 Vat Philippine Port Authority Ppaapi-247793055No ratings yet

- Good Day!: Income Taxation With Sir Keith G. Naval, CpaDocument12 pagesGood Day!: Income Taxation With Sir Keith G. Naval, Cpaenliven morenoNo ratings yet

- I Tax ReturnDocument3 pagesI Tax ReturnPronay ChakrabortyNo ratings yet

- Jagannath Kishore College, Purulia Pay Slip Government of West BengalDocument1 pageJagannath Kishore College, Purulia Pay Slip Government of West BengaldebabratamathNo ratings yet

- Chapter 3Document21 pagesChapter 3Carlo BaculoNo ratings yet

- IRCTC Retiring RoomDocument2 pagesIRCTC Retiring RoomRaj Aryan 19uee101No ratings yet

- Tax Invoice: Shipping AddressDocument1 pageTax Invoice: Shipping AddressOlga Lucia Holguin RicoNo ratings yet

- PF - (ID) - (MIN) - LA-010 Mineral Purchase RequestDocument1 pagePF - (ID) - (MIN) - LA-010 Mineral Purchase RequestZahra Salsa BilaNo ratings yet

- Business Permit License Office Renewal FormDocument1 pageBusiness Permit License Office Renewal FormAdrian Joseph GarciaNo ratings yet

- CIR v. SONY PHILIPPINES, INC. - DigestDocument2 pagesCIR v. SONY PHILIPPINES, INC. - DigestMark Genesis RojasNo ratings yet

- 1 PDFDocument1 page1 PDFARJUNSINH SEJPALNo ratings yet

- NSDL RPU - E-Tutorial (Version 1.3)Document57 pagesNSDL RPU - E-Tutorial (Version 1.3)Amit NaharNo ratings yet

- Fabm 2: Quarter 4 - Module 4 Principles and Processes of Income and Business TaxationDocument22 pagesFabm 2: Quarter 4 - Module 4 Principles and Processes of Income and Business TaxationFlordilyn DichonNo ratings yet

- Flipkart InvoiceDocument1 pageFlipkart InvoiceRobin TirkeyNo ratings yet

- 342210210082022INAPL6SB22120820221409Document7 pages342210210082022INAPL6SB22120820221409INTERWORLD PACIFIC CONTAINER LINENo ratings yet

- Pointers in Taxation (Atty. Roberto Lock) PDFDocument97 pagesPointers in Taxation (Atty. Roberto Lock) PDFReinald Kurt VillarazaNo ratings yet