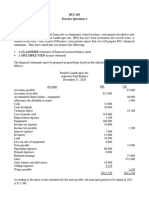

Final Accounts Ques

Final Accounts Ques

You might also like

- Chapter-04 Completing The Accounting Cycle (Maths)Document9 pagesChapter-04 Completing The Accounting Cycle (Maths)ShifatNo ratings yet

- B Exercises: E3-1B (Transaction Analysis-Service Company)Document8 pagesB Exercises: E3-1B (Transaction Analysis-Service Company)Saleh RaoufNo ratings yet

- Financial StatementsDocument3 pagesFinancial StatementsSoumendra RoyNo ratings yet

- Tugas 7 - ELRISKA TIFFANI - 142200111Document8 pagesTugas 7 - ELRISKA TIFFANI - 142200111Elriska Tiffani50% (2)

- Answer To Sample Question 3Document3 pagesAnswer To Sample Question 3Farid Abbasov0% (1)

- Summarizing (Trial Balance) : (Go Through The Reference Books For Details)Document6 pagesSummarizing (Trial Balance) : (Go Through The Reference Books For Details)sujitNo ratings yet

- Project On NJ India Invest PVT LTDDocument77 pagesProject On NJ India Invest PVT LTDrajveerpatidar69% (26)

- Financial Account Trading Profit and Loss ExampleDocument3 pagesFinancial Account Trading Profit and Loss Exampleahmedkingdom774No ratings yet

- Tutorial 7 QADocument4 pagesTutorial 7 QAJin HueyNo ratings yet

- Problem #1: Adjusting EntriesDocument5 pagesProblem #1: Adjusting EntriesShahzad AsifNo ratings yet

- Trial Balance and Final Accounts ProblemsDocument6 pagesTrial Balance and Final Accounts Problemsbhanu.chandu100% (1)

- Accounting Week13 Lec01 & Lec02 NotesDocument3 pagesAccounting Week13 Lec01 & Lec02 NotesABUBAKAR FawadNo ratings yet

- Igcse - Extented Tutoring - 2023 - 2024 - Final AccountsDocument7 pagesIgcse - Extented Tutoring - 2023 - 2024 - Final AccountsMUSTHARI KHANNo ratings yet

- Unit 2Document15 pagesUnit 2neharajt06061No ratings yet

- Accounting Fundamentals - PWS - 7Document11 pagesAccounting Fundamentals - PWS - 7Meet PatelNo ratings yet

- Jayalakshmi Institute of Technology Accounting For Management Unit - Ii QuestionsDocument2 pagesJayalakshmi Institute of Technology Accounting For Management Unit - Ii QuestionsJayalakshmi Institute of TechnologyNo ratings yet

- January 31: Birendra Mahato Adjusting Entries and WorksheetDocument17 pagesJanuary 31: Birendra Mahato Adjusting Entries and WorksheetAjit UpretyNo ratings yet

- Problem 1Document3 pagesProblem 1karthikeyan01No ratings yet

- Final Accounts: Problem SheetDocument2 pagesFinal Accounts: Problem SheetSaransh MaheshwariNo ratings yet

- Financial Statements of NonDocument3 pagesFinancial Statements of NonYashi GuptaNo ratings yet

- CA Final - FR Faster Batch - Consolidation Additional QuestionsDocument8 pagesCA Final - FR Faster Batch - Consolidation Additional QuestionsRonaldo GOmesNo ratings yet

- Accounting Cycle WorksheetDocument11 pagesAccounting Cycle Worksheettarikuabdisa0No ratings yet

- Class ExerciseDocument14 pagesClass ExerciseAbdul Basit MalikNo ratings yet

- Batch 2-1Document2 pagesBatch 2-1kp7659165No ratings yet

- 0438-Principles of AccountingDocument7 pages0438-Principles of AccountingHuma IjazNo ratings yet

- FS Withoutadj QuesDocument2 pagesFS Withoutadj QuesHimank SaklechaNo ratings yet

- Suggested Answer CAP II June 2017rDocument104 pagesSuggested Answer CAP II June 2017rBAZINGANo ratings yet

- Unit 2 WorksheetDocument13 pagesUnit 2 WorksheetHhvvgg BbbbNo ratings yet

- Accountancy and Auditing-2016 PDFDocument6 pagesAccountancy and Auditing-2016 PDFMian Abdullah YaseenNo ratings yet

- Accountancy I 2016 PDFDocument4 pagesAccountancy I 2016 PDFShahid RazwanNo ratings yet

- PracticeDocument1 pagePracticeNana CatNo ratings yet

- Acc311 2021 2Document4 pagesAcc311 2021 2hoghidan1No ratings yet

- Homework 4題目Document2 pagesHomework 4題目劉百祥No ratings yet

- Adjusting EntriesDocument5 pagesAdjusting EntriesM Hassan BrohiNo ratings yet

- Principles of Accounts: Name and Index No: Class: Date Topic: Level: ReferenceDocument2 pagesPrinciples of Accounts: Name and Index No: Class: Date Topic: Level: ReferenceCindy SweNo ratings yet

- ACP314 Competency PracticeDocument1 pageACP314 Competency PracticeJastine Rose CañeteNo ratings yet

- Chapter: Common Size, Comparative and Trend AnalysisDocument6 pagesChapter: Common Size, Comparative and Trend Analysiseldridatech pvt ltdNo ratings yet

- QN 1Document2 pagesQN 1Rax-Nguajandja KapuireNo ratings yet

- Accountancy Auditing 2016Document7 pagesAccountancy Auditing 2016Abdul basitNo ratings yet

- Accounts HomeworkDocument9 pagesAccounts HomeworkSasha KingNo ratings yet

- ISSo FPDocument6 pagesISSo FPabbeangedesireNo ratings yet

- Exercises - Trial Balance and Final Accounts - PracticeDocument23 pagesExercises - Trial Balance and Final Accounts - PracticeDilfaraz Kalawat79% (38)

- Dixion Company Worksheet For The Month Ended June 30,2017Document7 pagesDixion Company Worksheet For The Month Ended June 30,2017Hà HoàngNo ratings yet

- BUS 285 F23 Practice Questions in WordDocument6 pagesBUS 285 F23 Practice Questions in WordLê AnhNo ratings yet

- Book 2Document8 pagesBook 2May ManseNo ratings yet

- Finalterm Examination: Unfair Means in Completing ItDocument4 pagesFinalterm Examination: Unfair Means in Completing ItMuhammad Abdullah SaniNo ratings yet

- Book 1Document2 pagesBook 1Eman RehanNo ratings yet

- MGT 101Document13 pagesMGT 101MuzzamilNo ratings yet

- Elaine Joyce R. Garcia BSA 2ADocument6 pagesElaine Joyce R. Garcia BSA 2AWesNo ratings yet

- Project For ITT - 10Document1 pageProject For ITT - 10PRASHANT SHELKENo ratings yet

- Question 3-FSDocument1 pageQuestion 3-FSRax-Nguajandja KapuireNo ratings yet

- Problems On Final Accounts-Sole ProprietorshipDocument12 pagesProblems On Final Accounts-Sole ProprietorshipRishiShuklaNo ratings yet

- Financial Accounting - Mid Term Question PaperDocument3 pagesFinancial Accounting - Mid Term Question PapersahittiNo ratings yet

- Class Exercise Session 5 and 6Document8 pagesClass Exercise Session 5 and 6Sumeet KumarNo ratings yet

- Ingenuity International School and College Baridhara, Gulshan, Dhaka. MCT-4 Sub: Accounting Class-Std - VIIIDocument2 pagesIngenuity International School and College Baridhara, Gulshan, Dhaka. MCT-4 Sub: Accounting Class-Std - VIIINayna Sharmin100% (1)

- Adam's Learning Centre, Lahore: Company AccountsDocument6 pagesAdam's Learning Centre, Lahore: Company AccountsMasood Ahmad AadamNo ratings yet

- Pilot Test Solution Official (NLKT)Document36 pagesPilot Test Solution Official (NLKT)an27504No ratings yet

- mgt101 Questions With AnswersDocument11 pagesmgt101 Questions With AnswersKinza LaiqatNo ratings yet

- Name of Company:-Madhura EnterprisesDocument39 pagesName of Company:-Madhura EnterprisesTaur VishalNo ratings yet

- J.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Medicinal Plants in Chhattisgarh, India - Success StoriesDocument2 pagesMedicinal Plants in Chhattisgarh, India - Success StoriesUtkarsh GhateNo ratings yet

- LLAWJDOC6002 - Credit and Security Law SyllabusDocument3 pagesLLAWJDOC6002 - Credit and Security Law SyllabusWing Laam Tam (Bobo)No ratings yet

- Economic Growth Vs Economic Development Best 7 DifferencesDocument9 pagesEconomic Growth Vs Economic Development Best 7 DifferencesEdmar OducayenNo ratings yet

- BESALA Loan Application-EVELYN BULATAODocument1 pageBESALA Loan Application-EVELYN BULATAOYul BackNo ratings yet

- ESOP Whitepaper PDFDocument11 pagesESOP Whitepaper PDFnkashimpuriaNo ratings yet

- PROPERTY Outline and CasesDocument61 pagesPROPERTY Outline and CasesJessica LagmanNo ratings yet

- Unit 2 LPBDocument9 pagesUnit 2 LPBVeena ReddyNo ratings yet

- Ap A1Document23 pagesAp A1Liên ĐỗNo ratings yet

- British Council IELTS Online ApplicationDocument3 pagesBritish Council IELTS Online ApplicationNasrullah AliNo ratings yet

- Case Studies Chap 05 M@ADocument3 pagesCase Studies Chap 05 M@AZeeshan AliNo ratings yet

- Bar Exam Questions in Mercantile Law (MCQ)Document30 pagesBar Exam Questions in Mercantile Law (MCQ)Bion Henrik PrioloNo ratings yet

- Four-Way Bank Transfer MessageDocument9 pagesFour-Way Bank Transfer MessagescribdirrfanNo ratings yet

- Evaluation and Inference of Financial PerformanceDocument82 pagesEvaluation and Inference of Financial PerformanceIlakkiya ManiNo ratings yet

- Social and Financial LiteracyDocument9 pagesSocial and Financial LiteracyjaisymentarNo ratings yet

- Chapter 8 Advanced Accounting Chapter 8 Advanced AccountingDocument22 pagesChapter 8 Advanced Accounting Chapter 8 Advanced AccountingNur AmaliyahNo ratings yet

- 0731 I K JG 000169791Document1 page0731 I K JG 000169791Fikri FarhanNo ratings yet

- MidtermsE 94%Document17 pagesMidtermsE 94%jrence67% (3)

- MTP Session 1 Reading 1. Slides 2. Class NotesDocument42 pagesMTP Session 1 Reading 1. Slides 2. Class NotesDevbratRathNo ratings yet

- Meaning of Plastic Money: IntroducationDocument27 pagesMeaning of Plastic Money: IntroducationVish SahaniNo ratings yet

- Banking and Insurance - 2 MARKSDocument13 pagesBanking and Insurance - 2 MARKSkirandegol18No ratings yet

- PMD Pro Guide PDFDocument163 pagesPMD Pro Guide PDFKaka SuleNo ratings yet

- Training Material On West Bengal Service RulesDocument99 pagesTraining Material On West Bengal Service Rulesp2c9100% (2)

- Credit Cards QuizDocument2 pagesCredit Cards Quizapi-372302973No ratings yet

- Audit and Accounts in CompaniesDocument23 pagesAudit and Accounts in CompaniesAmishaNo ratings yet

- Contemporary Issues in Accounting 2nd Edition Rankin Solutions ManualDocument18 pagesContemporary Issues in Accounting 2nd Edition Rankin Solutions Manualbenjaminnelsonijmekzfdos100% (15)

- WRONGFUL Foreclosure Action NOTICE JeaDocument19 pagesWRONGFUL Foreclosure Action NOTICE JeaAlbertelli_Law100% (1)

- Biography Dhirubhai AmbaniDocument11 pagesBiography Dhirubhai AmbaniBhasabi KaulNo ratings yet

- BSBFIM501 Assessment Templates V3.0920Document18 pagesBSBFIM501 Assessment Templates V3.0920Layla Correa da SilvaNo ratings yet

- FSRE 2022-23 Topic 4Document22 pagesFSRE 2022-23 Topic 4Ali Al RostamaniNo ratings yet

Download as pdf or txt

You might also like

- Chapter-04 Completing The Accounting Cycle (Maths)Document9 pagesChapter-04 Completing The Accounting Cycle (Maths)ShifatNo ratings yet

- B Exercises: E3-1B (Transaction Analysis-Service Company)Document8 pagesB Exercises: E3-1B (Transaction Analysis-Service Company)Saleh RaoufNo ratings yet

- Financial StatementsDocument3 pagesFinancial StatementsSoumendra RoyNo ratings yet

- Tugas 7 - ELRISKA TIFFANI - 142200111Document8 pagesTugas 7 - ELRISKA TIFFANI - 142200111Elriska Tiffani50% (2)

- Answer To Sample Question 3Document3 pagesAnswer To Sample Question 3Farid Abbasov0% (1)

- Summarizing (Trial Balance) : (Go Through The Reference Books For Details)Document6 pagesSummarizing (Trial Balance) : (Go Through The Reference Books For Details)sujitNo ratings yet

- Project On NJ India Invest PVT LTDDocument77 pagesProject On NJ India Invest PVT LTDrajveerpatidar69% (26)

- Financial Account Trading Profit and Loss ExampleDocument3 pagesFinancial Account Trading Profit and Loss Exampleahmedkingdom774No ratings yet

- Tutorial 7 QADocument4 pagesTutorial 7 QAJin HueyNo ratings yet

- Problem #1: Adjusting EntriesDocument5 pagesProblem #1: Adjusting EntriesShahzad AsifNo ratings yet

- Trial Balance and Final Accounts ProblemsDocument6 pagesTrial Balance and Final Accounts Problemsbhanu.chandu100% (1)

- Accounting Week13 Lec01 & Lec02 NotesDocument3 pagesAccounting Week13 Lec01 & Lec02 NotesABUBAKAR FawadNo ratings yet

- Igcse - Extented Tutoring - 2023 - 2024 - Final AccountsDocument7 pagesIgcse - Extented Tutoring - 2023 - 2024 - Final AccountsMUSTHARI KHANNo ratings yet

- Unit 2Document15 pagesUnit 2neharajt06061No ratings yet

- Accounting Fundamentals - PWS - 7Document11 pagesAccounting Fundamentals - PWS - 7Meet PatelNo ratings yet

- Jayalakshmi Institute of Technology Accounting For Management Unit - Ii QuestionsDocument2 pagesJayalakshmi Institute of Technology Accounting For Management Unit - Ii QuestionsJayalakshmi Institute of TechnologyNo ratings yet

- January 31: Birendra Mahato Adjusting Entries and WorksheetDocument17 pagesJanuary 31: Birendra Mahato Adjusting Entries and WorksheetAjit UpretyNo ratings yet

- Problem 1Document3 pagesProblem 1karthikeyan01No ratings yet

- Final Accounts: Problem SheetDocument2 pagesFinal Accounts: Problem SheetSaransh MaheshwariNo ratings yet

- Financial Statements of NonDocument3 pagesFinancial Statements of NonYashi GuptaNo ratings yet

- CA Final - FR Faster Batch - Consolidation Additional QuestionsDocument8 pagesCA Final - FR Faster Batch - Consolidation Additional QuestionsRonaldo GOmesNo ratings yet

- Accounting Cycle WorksheetDocument11 pagesAccounting Cycle Worksheettarikuabdisa0No ratings yet

- Class ExerciseDocument14 pagesClass ExerciseAbdul Basit MalikNo ratings yet

- Batch 2-1Document2 pagesBatch 2-1kp7659165No ratings yet

- 0438-Principles of AccountingDocument7 pages0438-Principles of AccountingHuma IjazNo ratings yet

- FS Withoutadj QuesDocument2 pagesFS Withoutadj QuesHimank SaklechaNo ratings yet

- Suggested Answer CAP II June 2017rDocument104 pagesSuggested Answer CAP II June 2017rBAZINGANo ratings yet

- Unit 2 WorksheetDocument13 pagesUnit 2 WorksheetHhvvgg BbbbNo ratings yet

- Accountancy and Auditing-2016 PDFDocument6 pagesAccountancy and Auditing-2016 PDFMian Abdullah YaseenNo ratings yet

- Accountancy I 2016 PDFDocument4 pagesAccountancy I 2016 PDFShahid RazwanNo ratings yet

- PracticeDocument1 pagePracticeNana CatNo ratings yet

- Acc311 2021 2Document4 pagesAcc311 2021 2hoghidan1No ratings yet

- Homework 4題目Document2 pagesHomework 4題目劉百祥No ratings yet

- Adjusting EntriesDocument5 pagesAdjusting EntriesM Hassan BrohiNo ratings yet

- Principles of Accounts: Name and Index No: Class: Date Topic: Level: ReferenceDocument2 pagesPrinciples of Accounts: Name and Index No: Class: Date Topic: Level: ReferenceCindy SweNo ratings yet

- ACP314 Competency PracticeDocument1 pageACP314 Competency PracticeJastine Rose CañeteNo ratings yet

- Chapter: Common Size, Comparative and Trend AnalysisDocument6 pagesChapter: Common Size, Comparative and Trend Analysiseldridatech pvt ltdNo ratings yet

- QN 1Document2 pagesQN 1Rax-Nguajandja KapuireNo ratings yet

- Accountancy Auditing 2016Document7 pagesAccountancy Auditing 2016Abdul basitNo ratings yet

- Accounts HomeworkDocument9 pagesAccounts HomeworkSasha KingNo ratings yet

- ISSo FPDocument6 pagesISSo FPabbeangedesireNo ratings yet

- Exercises - Trial Balance and Final Accounts - PracticeDocument23 pagesExercises - Trial Balance and Final Accounts - PracticeDilfaraz Kalawat79% (38)

- Dixion Company Worksheet For The Month Ended June 30,2017Document7 pagesDixion Company Worksheet For The Month Ended June 30,2017Hà HoàngNo ratings yet

- BUS 285 F23 Practice Questions in WordDocument6 pagesBUS 285 F23 Practice Questions in WordLê AnhNo ratings yet

- Book 2Document8 pagesBook 2May ManseNo ratings yet

- Finalterm Examination: Unfair Means in Completing ItDocument4 pagesFinalterm Examination: Unfair Means in Completing ItMuhammad Abdullah SaniNo ratings yet

- Book 1Document2 pagesBook 1Eman RehanNo ratings yet

- MGT 101Document13 pagesMGT 101MuzzamilNo ratings yet

- Elaine Joyce R. Garcia BSA 2ADocument6 pagesElaine Joyce R. Garcia BSA 2AWesNo ratings yet

- Project For ITT - 10Document1 pageProject For ITT - 10PRASHANT SHELKENo ratings yet

- Question 3-FSDocument1 pageQuestion 3-FSRax-Nguajandja KapuireNo ratings yet

- Problems On Final Accounts-Sole ProprietorshipDocument12 pagesProblems On Final Accounts-Sole ProprietorshipRishiShuklaNo ratings yet

- Financial Accounting - Mid Term Question PaperDocument3 pagesFinancial Accounting - Mid Term Question PapersahittiNo ratings yet

- Class Exercise Session 5 and 6Document8 pagesClass Exercise Session 5 and 6Sumeet KumarNo ratings yet

- Ingenuity International School and College Baridhara, Gulshan, Dhaka. MCT-4 Sub: Accounting Class-Std - VIIIDocument2 pagesIngenuity International School and College Baridhara, Gulshan, Dhaka. MCT-4 Sub: Accounting Class-Std - VIIINayna Sharmin100% (1)

- Adam's Learning Centre, Lahore: Company AccountsDocument6 pagesAdam's Learning Centre, Lahore: Company AccountsMasood Ahmad AadamNo ratings yet

- Pilot Test Solution Official (NLKT)Document36 pagesPilot Test Solution Official (NLKT)an27504No ratings yet

- mgt101 Questions With AnswersDocument11 pagesmgt101 Questions With AnswersKinza LaiqatNo ratings yet

- Name of Company:-Madhura EnterprisesDocument39 pagesName of Company:-Madhura EnterprisesTaur VishalNo ratings yet

- J.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineNo ratings yet

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineFrom EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineNo ratings yet

- Medicinal Plants in Chhattisgarh, India - Success StoriesDocument2 pagesMedicinal Plants in Chhattisgarh, India - Success StoriesUtkarsh GhateNo ratings yet

- LLAWJDOC6002 - Credit and Security Law SyllabusDocument3 pagesLLAWJDOC6002 - Credit and Security Law SyllabusWing Laam Tam (Bobo)No ratings yet

- Economic Growth Vs Economic Development Best 7 DifferencesDocument9 pagesEconomic Growth Vs Economic Development Best 7 DifferencesEdmar OducayenNo ratings yet

- BESALA Loan Application-EVELYN BULATAODocument1 pageBESALA Loan Application-EVELYN BULATAOYul BackNo ratings yet

- ESOP Whitepaper PDFDocument11 pagesESOP Whitepaper PDFnkashimpuriaNo ratings yet

- PROPERTY Outline and CasesDocument61 pagesPROPERTY Outline and CasesJessica LagmanNo ratings yet

- Unit 2 LPBDocument9 pagesUnit 2 LPBVeena ReddyNo ratings yet

- Ap A1Document23 pagesAp A1Liên ĐỗNo ratings yet

- British Council IELTS Online ApplicationDocument3 pagesBritish Council IELTS Online ApplicationNasrullah AliNo ratings yet

- Case Studies Chap 05 M@ADocument3 pagesCase Studies Chap 05 M@AZeeshan AliNo ratings yet

- Bar Exam Questions in Mercantile Law (MCQ)Document30 pagesBar Exam Questions in Mercantile Law (MCQ)Bion Henrik PrioloNo ratings yet

- Four-Way Bank Transfer MessageDocument9 pagesFour-Way Bank Transfer MessagescribdirrfanNo ratings yet

- Evaluation and Inference of Financial PerformanceDocument82 pagesEvaluation and Inference of Financial PerformanceIlakkiya ManiNo ratings yet

- Social and Financial LiteracyDocument9 pagesSocial and Financial LiteracyjaisymentarNo ratings yet

- Chapter 8 Advanced Accounting Chapter 8 Advanced AccountingDocument22 pagesChapter 8 Advanced Accounting Chapter 8 Advanced AccountingNur AmaliyahNo ratings yet

- 0731 I K JG 000169791Document1 page0731 I K JG 000169791Fikri FarhanNo ratings yet

- MidtermsE 94%Document17 pagesMidtermsE 94%jrence67% (3)

- MTP Session 1 Reading 1. Slides 2. Class NotesDocument42 pagesMTP Session 1 Reading 1. Slides 2. Class NotesDevbratRathNo ratings yet

- Meaning of Plastic Money: IntroducationDocument27 pagesMeaning of Plastic Money: IntroducationVish SahaniNo ratings yet

- Banking and Insurance - 2 MARKSDocument13 pagesBanking and Insurance - 2 MARKSkirandegol18No ratings yet

- PMD Pro Guide PDFDocument163 pagesPMD Pro Guide PDFKaka SuleNo ratings yet

- Training Material On West Bengal Service RulesDocument99 pagesTraining Material On West Bengal Service Rulesp2c9100% (2)

- Credit Cards QuizDocument2 pagesCredit Cards Quizapi-372302973No ratings yet

- Audit and Accounts in CompaniesDocument23 pagesAudit and Accounts in CompaniesAmishaNo ratings yet

- Contemporary Issues in Accounting 2nd Edition Rankin Solutions ManualDocument18 pagesContemporary Issues in Accounting 2nd Edition Rankin Solutions Manualbenjaminnelsonijmekzfdos100% (15)

- WRONGFUL Foreclosure Action NOTICE JeaDocument19 pagesWRONGFUL Foreclosure Action NOTICE JeaAlbertelli_Law100% (1)

- Biography Dhirubhai AmbaniDocument11 pagesBiography Dhirubhai AmbaniBhasabi KaulNo ratings yet

- BSBFIM501 Assessment Templates V3.0920Document18 pagesBSBFIM501 Assessment Templates V3.0920Layla Correa da SilvaNo ratings yet

- FSRE 2022-23 Topic 4Document22 pagesFSRE 2022-23 Topic 4Ali Al RostamaniNo ratings yet