Pages 178

Pages 178

You might also like

- Sample SPA - SSS ClaimDocument2 pagesSample SPA - SSS ClaimA.T.Comia91% (43)

- Salvacion CapistranoDocument14 pagesSalvacion CapistranoHazel Ann DuermeNo ratings yet

- Performance Task No 2 - Group Work - Planning Concepts and Tools P1Document8 pagesPerformance Task No 2 - Group Work - Planning Concepts and Tools P1Corn SaladNo ratings yet

- Activity Sheet Adjusting Entries DeferralsDocument1 pageActivity Sheet Adjusting Entries DeferralsShania LiwanagNo ratings yet

- 1 Accounting For Merchandising BusinessDocument23 pages1 Accounting For Merchandising BusinessKhay2 ManaliliDelaCruz100% (1)

- (1000) ScalesDocument83 pages(1000) ScalesJuan Prado Sánchez100% (2)

- M.O.O.The R. Words and PhrasesDocument3 pagesM.O.O.The R. Words and PhrasesA. J. Bey100% (4)

- Q4 ABM Fundamentals of ABM1 11 Week 4Document4 pagesQ4 ABM Fundamentals of ABM1 11 Week 4Celine Angela AbreaNo ratings yet

- PT .1 in AccountingDocument8 pagesPT .1 in AccountingMerdwindelle Allagones100% (1)

- JOURNALIZINGDocument2 pagesJOURNALIZINGArneld SantiagoNo ratings yet

- FAR Assignment 1Document3 pagesFAR Assignment 1The Psycho100% (1)

- Adjusting EntryDocument38 pagesAdjusting EntryNicaela Margareth YusoresNo ratings yet

- 06 Activity 1Document5 pages06 Activity 1Laisan SantosNo ratings yet

- Accounting Cycle of A Service Business-ExerciseDocument50 pagesAccounting Cycle of A Service Business-ExerciseHannah GarciaNo ratings yet

- Or, Deposit Slip and Withdrawl SlipDocument4 pagesOr, Deposit Slip and Withdrawl SlipJessica Rose AlbaracinNo ratings yet

- Fabm2 Q2 M4 - 4 CsefDocument20 pagesFabm2 Q2 M4 - 4 CsefZeus MalicdemNo ratings yet

- ACTIVITY. On February 1, 20A4, Mira Delamar Opened A Store That SellsDocument1 pageACTIVITY. On February 1, 20A4, Mira Delamar Opened A Store That SellsMiguel Lulab100% (1)

- Acctg. Equation Puring CompanyDocument8 pagesAcctg. Equation Puring CompanyAngelNo ratings yet

- Accounting 101Document17 pagesAccounting 101Jenne Santiago BabantoNo ratings yet

- 01 Quiz 1Document2 pages01 Quiz 1Laisan SantosNo ratings yet

- Inancial CCTG: Adjusting The AccountsDocument28 pagesInancial CCTG: Adjusting The AccountsLj BesaNo ratings yet

- Las-Business-Finance-Q1 Week 1Document16 pagesLas-Business-Finance-Q1 Week 1Kinn Jay100% (1)

- Rovelyn E. Forcadas ABM-11 Activity #9-BDocument2 pagesRovelyn E. Forcadas ABM-11 Activity #9-BRovelyn E. ForcadasNo ratings yet

- General Journal, GeveraDocument2 pagesGeneral Journal, GeveraFeiya LiuNo ratings yet

- Accounting Cycle of A Merchandising BusinessDocument21 pagesAccounting Cycle of A Merchandising Businesszedrick edenNo ratings yet

- FABM ActivityDocument3 pagesFABM ActivityRey VillaNo ratings yet

- Fundamentals of Accountancy, Business and Management 1: Quarter 4 - Week 7Document6 pagesFundamentals of Accountancy, Business and Management 1: Quarter 4 - Week 7nicss bonaobraNo ratings yet

- Case 2-4 - SceDocument3 pagesCase 2-4 - SceNica CabradillaNo ratings yet

- Analysis of Common Business TransactionsDocument18 pagesAnalysis of Common Business TransactionsClarisse RosalNo ratings yet

- Problem 15Document1 pageProblem 15Alyssa Jane G. AlvarezNo ratings yet

- ABM FABM1 AIRs LM Q4-M12Document12 pagesABM FABM1 AIRs LM Q4-M12ajcervantes065No ratings yet

- SW-16 UTB Merchandising AsDocument4 pagesSW-16 UTB Merchandising AsAlexis Marie Balagot100% (1)

- Bank ReconciliationDocument60 pagesBank ReconciliationLourdes EyoNo ratings yet

- Thor General Merchandise ProblemDocument3 pagesThor General Merchandise ProblemEdmundo Otañes GasatanNo ratings yet

- General Journal: Date Account Titles and Explanation Debit Credit Posting ReferenceDocument9 pagesGeneral Journal: Date Account Titles and Explanation Debit Credit Posting ReferenceCherrie Mae BanaagNo ratings yet

- Accounting Cycle and Book of AccountsDocument23 pagesAccounting Cycle and Book of AccountsChaaaNo ratings yet

- Entrepreneurship 2nd Q.exam OktcindyDocument8 pagesEntrepreneurship 2nd Q.exam OktcindyDaryl MacatbagNo ratings yet

- Exercise 3 Leah GarciaDocument12 pagesExercise 3 Leah GarciaMa Sophia Mikaela EreceNo ratings yet

- Fabm1 Completing The Accounting CycleDocument16 pagesFabm1 Completing The Accounting CycleVenice100% (1)

- Bart M ManuelDocument27 pagesBart M ManuelBea TiuNo ratings yet

- I. Multiple Choice: Read and Analyze Each Item. Circle The Letter of The Best Answer. 1Document3 pagesI. Multiple Choice: Read and Analyze Each Item. Circle The Letter of The Best Answer. 1HLeigh Nietes-GabutanNo ratings yet

- Fundamentals of Accountancy, Business and Management 1Document19 pagesFundamentals of Accountancy, Business and Management 1Shiellai Mae Polintang0% (1)

- Fabm1 Quarter1 Module 6.2 Week 6Document22 pagesFabm1 Quarter1 Module 6.2 Week 6Danny BulacsoNo ratings yet

- Fabm Nites PrintDocument3 pagesFabm Nites Printwiz wizNo ratings yet

- Fabm2 - Se (2) Answer KeyDocument2 pagesFabm2 - Se (2) Answer Keyl m100% (1)

- Journal Entry DiscussionDocument8 pagesJournal Entry DiscussionAyesha Eunice SalvaleonNo ratings yet

- Abm Fabm1 Airs LM q4-m9Document18 pagesAbm Fabm1 Airs LM q4-m9MEDILEN O. BORRESNo ratings yet

- Practical Accounting 1Document90 pagesPractical Accounting 1Honie Rose MondayNo ratings yet

- Financial Statemtents ShortDocument7 pagesFinancial Statemtents Shortgk concepcionNo ratings yet

- ADJUSTING AND CLOSING ENTRIES Assignment Nov 20 2020Document4 pagesADJUSTING AND CLOSING ENTRIES Assignment Nov 20 2020Kayle MallillinNo ratings yet

- Balance Sheet Only-Agatha TradingDocument1 pageBalance Sheet Only-Agatha TradingJasmine Acta0% (1)

- Fabm 1 ExamDocument2 pagesFabm 1 ExamJasfer Niño100% (1)

- PeriodicDocument23 pagesPeriodicalmorsNo ratings yet

- Midterm 2nd 3rd Meeting RevisedDocument6 pagesMidterm 2nd 3rd Meeting RevisedChristopher CristobalNo ratings yet

- Business Math Quarter 3 Week 2Document8 pagesBusiness Math Quarter 3 Week 2Gladys Angela ValdemoroNo ratings yet

- ABM 3 Quarterly ExamDocument2 pagesABM 3 Quarterly ExamLenyBarrogaNo ratings yet

- Name of Examinee: - : Prepare The FollowingDocument15 pagesName of Examinee: - : Prepare The FollowingNoel CarpioNo ratings yet

- Week 6Document11 pagesWeek 6Kim Albero CubelNo ratings yet

- Module 0 Review Accounting 1 PDFDocument40 pagesModule 0 Review Accounting 1 PDFJmaseNo ratings yet

- Accounting 2 - Unit 3 - Lesson 1 To 3Document62 pagesAccounting 2 - Unit 3 - Lesson 1 To 3Merdwindelle AllagonesNo ratings yet

- ABM - 111 - Final ExaminationDocument2 pagesABM - 111 - Final ExaminationTimothy JamesNo ratings yet

- Fundamentals of Accountancy Business and Management 1 11 FourthDocument4 pagesFundamentals of Accountancy Business and Management 1 11 FourthPaulo Amposta CarpioNo ratings yet

- Practice Problem 21: Name Date Course/Year ScoreDocument3 pagesPractice Problem 21: Name Date Course/Year ScorePaw VerdilloNo ratings yet

- Module-1 GovtAcctgDocument8 pagesModule-1 GovtAcctgKrestyl Ann GabaldaNo ratings yet

- Rizal Place in Dapitan (Group 5)Document5 pagesRizal Place in Dapitan (Group 5)Krestyl Ann GabaldaNo ratings yet

- Chips Not DoneDocument42 pagesChips Not DoneKrestyl Ann GabaldaNo ratings yet

- Bag o Na ChipsDocument45 pagesBag o Na ChipsKrestyl Ann GabaldaNo ratings yet

- Parcor QuizbowlDocument38 pagesParcor QuizbowlKrestyl Ann GabaldaNo ratings yet

- Net Estate & Estate Tax: Conjugal Partnership of GainsDocument10 pagesNet Estate & Estate Tax: Conjugal Partnership of GainsKrestyl Ann GabaldaNo ratings yet

- Conceptual Framework and Accounting StandardsDocument4 pagesConceptual Framework and Accounting StandardsKrestyl Ann GabaldaNo ratings yet

- Article 1176-1185 FinalDocument37 pagesArticle 1176-1185 FinalKrestyl Ann Gabalda100% (1)

- Cost AccountingDocument64 pagesCost AccountingKrestyl Ann GabaldaNo ratings yet

- Forms of Business Organization Learning ObjectivesDocument5 pagesForms of Business Organization Learning ObjectivesKrestyl Ann GabaldaNo ratings yet

- Activity With Youtube Video Shareholders Equity Part 1Document2 pagesActivity With Youtube Video Shareholders Equity Part 1Krestyl Ann GabaldaNo ratings yet

- PIS 2019 With VATDocument19 pagesPIS 2019 With VATKrestyl Ann GabaldaNo ratings yet

- Tak - An NakoDocument30 pagesTak - An NakoKrestyl Ann GabaldaNo ratings yet

- Accounting Research Method ACCTG 322 Jhoelyn MaguadDocument3 pagesAccounting Research Method ACCTG 322 Jhoelyn MaguadKrestyl Ann GabaldaNo ratings yet

- Rizal Long QuizDocument2 pagesRizal Long QuizKrestyl Ann GabaldaNo ratings yet

- Students Perception Towards Digital Payment System-A Study With A Special Reference To Mangalore UniversityDocument20 pagesStudents Perception Towards Digital Payment System-A Study With A Special Reference To Mangalore UniversityKrestyl Ann GabaldaNo ratings yet

- United States Court of Appeals, Third CircuitDocument1 pageUnited States Court of Appeals, Third CircuitScribd Government DocsNo ratings yet

- Goods Supply Agreement TemplateDocument8 pagesGoods Supply Agreement TemplateSanjeev ThakurNo ratings yet

- Statement of JurisdictionDocument13 pagesStatement of JurisdictionMouneeshNo ratings yet

- The Growing Role of Forensic Science in Criminal Investigation: Admissibility in The Indian Legal System and Future PerspectiveDocument8 pagesThe Growing Role of Forensic Science in Criminal Investigation: Admissibility in The Indian Legal System and Future PerspectiveMavvyy KishwarNo ratings yet

- Phil. Export v. Amalmagated Management, Et. Al.Document8 pagesPhil. Export v. Amalmagated Management, Et. Al.CZARINA ANN CASTRONo ratings yet

- Duties of Agent PrincipalDocument18 pagesDuties of Agent PrincipalJulietha YusnizamNo ratings yet

- Comments To Commentary On UCP 600 - A Critical ReviewDocument7 pagesComments To Commentary On UCP 600 - A Critical Reviewvkrm14No ratings yet

- Civil - 104 - GR 208140Document7 pagesCivil - 104 - GR 208140Firdous Gayak SumailNo ratings yet

- Case Digest On CopyrightDocument4 pagesCase Digest On CopyrightAllan CalvoNo ratings yet

- Requirements For Cpa AccreditationDocument1 pageRequirements For Cpa AccreditationJ'ca EdulanNo ratings yet

- Slide1 Slide 2 What Is Competition ActDocument2 pagesSlide1 Slide 2 What Is Competition Actrobin hoodNo ratings yet

- Name: Charlotte Cabading Subject: ENG 111 Course/Year/Set: BSDRM SET ADocument10 pagesName: Charlotte Cabading Subject: ENG 111 Course/Year/Set: BSDRM SET AJudeza Jaira B. LabadanNo ratings yet

- Board-Excom For BUCAP July 2020Document4 pagesBoard-Excom For BUCAP July 2020Jebs KwanNo ratings yet

- A Caricature Grievances Speech AquinoDocument39 pagesA Caricature Grievances Speech AquinoJessa CañadaNo ratings yet

- E-Governance Police Prison PSUsDocument4 pagesE-Governance Police Prison PSUssh LaksNo ratings yet

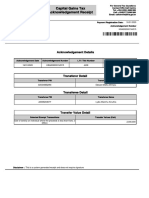

- Capital Gains Tax Acknowledgment ReceiptDocument1 pageCapital Gains Tax Acknowledgment ReceiptDavid MugambiNo ratings yet

- Proposed Guidelines On Conduct of VideoconferencingDocument6 pagesProposed Guidelines On Conduct of VideoconferencingPolo MartinezNo ratings yet

- Traffic CountDocument32 pagesTraffic Countobrkh 07No ratings yet

- The Competition Commission of PakistanDocument10 pagesThe Competition Commission of Pakistanranag28No ratings yet

- UTHR LQDA - Tyvaso Patent IPR - 11 Aug 21Document44 pagesUTHR LQDA - Tyvaso Patent IPR - 11 Aug 21XDL1No ratings yet

- History and Development of Securities Laws in IndiaDocument3 pagesHistory and Development of Securities Laws in IndiaTathagat ShívanshNo ratings yet

- Ii LL.B 3RD Sem Viva Voce SCHDocument1 pageIi LL.B 3RD Sem Viva Voce SCHshivaNo ratings yet

- Zaragoza Vs TanDocument4 pagesZaragoza Vs TanADNo ratings yet

- Jorge Stalin Vitar Semanate, 21jan 1805 QuitoDocument3 pagesJorge Stalin Vitar Semanate, 21jan 1805 QuitoDamian RobleroNo ratings yet

- Taxguru - In-Revised Procedure For MVATCSTPTRCPTEC Registration in MaharashtraDocument3 pagesTaxguru - In-Revised Procedure For MVATCSTPTRCPTEC Registration in MaharashtraOmPrakashAgrawalNo ratings yet

- 01 Quiz 1aDocument3 pages01 Quiz 1aJoffrey MellamaNo ratings yet

- Form LCM - Labuan Company Managementv2 - 04032021Document18 pagesForm LCM - Labuan Company Managementv2 - 04032021danNo ratings yet

Download as docx, pdf, or txt

You might also like

- Sample SPA - SSS ClaimDocument2 pagesSample SPA - SSS ClaimA.T.Comia91% (43)

- Salvacion CapistranoDocument14 pagesSalvacion CapistranoHazel Ann DuermeNo ratings yet

- Performance Task No 2 - Group Work - Planning Concepts and Tools P1Document8 pagesPerformance Task No 2 - Group Work - Planning Concepts and Tools P1Corn SaladNo ratings yet

- Activity Sheet Adjusting Entries DeferralsDocument1 pageActivity Sheet Adjusting Entries DeferralsShania LiwanagNo ratings yet

- 1 Accounting For Merchandising BusinessDocument23 pages1 Accounting For Merchandising BusinessKhay2 ManaliliDelaCruz100% (1)

- (1000) ScalesDocument83 pages(1000) ScalesJuan Prado Sánchez100% (2)

- M.O.O.The R. Words and PhrasesDocument3 pagesM.O.O.The R. Words and PhrasesA. J. Bey100% (4)

- Q4 ABM Fundamentals of ABM1 11 Week 4Document4 pagesQ4 ABM Fundamentals of ABM1 11 Week 4Celine Angela AbreaNo ratings yet

- PT .1 in AccountingDocument8 pagesPT .1 in AccountingMerdwindelle Allagones100% (1)

- JOURNALIZINGDocument2 pagesJOURNALIZINGArneld SantiagoNo ratings yet

- FAR Assignment 1Document3 pagesFAR Assignment 1The Psycho100% (1)

- Adjusting EntryDocument38 pagesAdjusting EntryNicaela Margareth YusoresNo ratings yet

- 06 Activity 1Document5 pages06 Activity 1Laisan SantosNo ratings yet

- Accounting Cycle of A Service Business-ExerciseDocument50 pagesAccounting Cycle of A Service Business-ExerciseHannah GarciaNo ratings yet

- Or, Deposit Slip and Withdrawl SlipDocument4 pagesOr, Deposit Slip and Withdrawl SlipJessica Rose AlbaracinNo ratings yet

- Fabm2 Q2 M4 - 4 CsefDocument20 pagesFabm2 Q2 M4 - 4 CsefZeus MalicdemNo ratings yet

- ACTIVITY. On February 1, 20A4, Mira Delamar Opened A Store That SellsDocument1 pageACTIVITY. On February 1, 20A4, Mira Delamar Opened A Store That SellsMiguel Lulab100% (1)

- Acctg. Equation Puring CompanyDocument8 pagesAcctg. Equation Puring CompanyAngelNo ratings yet

- Accounting 101Document17 pagesAccounting 101Jenne Santiago BabantoNo ratings yet

- 01 Quiz 1Document2 pages01 Quiz 1Laisan SantosNo ratings yet

- Inancial CCTG: Adjusting The AccountsDocument28 pagesInancial CCTG: Adjusting The AccountsLj BesaNo ratings yet

- Las-Business-Finance-Q1 Week 1Document16 pagesLas-Business-Finance-Q1 Week 1Kinn Jay100% (1)

- Rovelyn E. Forcadas ABM-11 Activity #9-BDocument2 pagesRovelyn E. Forcadas ABM-11 Activity #9-BRovelyn E. ForcadasNo ratings yet

- General Journal, GeveraDocument2 pagesGeneral Journal, GeveraFeiya LiuNo ratings yet

- Accounting Cycle of A Merchandising BusinessDocument21 pagesAccounting Cycle of A Merchandising Businesszedrick edenNo ratings yet

- FABM ActivityDocument3 pagesFABM ActivityRey VillaNo ratings yet

- Fundamentals of Accountancy, Business and Management 1: Quarter 4 - Week 7Document6 pagesFundamentals of Accountancy, Business and Management 1: Quarter 4 - Week 7nicss bonaobraNo ratings yet

- Case 2-4 - SceDocument3 pagesCase 2-4 - SceNica CabradillaNo ratings yet

- Analysis of Common Business TransactionsDocument18 pagesAnalysis of Common Business TransactionsClarisse RosalNo ratings yet

- Problem 15Document1 pageProblem 15Alyssa Jane G. AlvarezNo ratings yet

- ABM FABM1 AIRs LM Q4-M12Document12 pagesABM FABM1 AIRs LM Q4-M12ajcervantes065No ratings yet

- SW-16 UTB Merchandising AsDocument4 pagesSW-16 UTB Merchandising AsAlexis Marie Balagot100% (1)

- Bank ReconciliationDocument60 pagesBank ReconciliationLourdes EyoNo ratings yet

- Thor General Merchandise ProblemDocument3 pagesThor General Merchandise ProblemEdmundo Otañes GasatanNo ratings yet

- General Journal: Date Account Titles and Explanation Debit Credit Posting ReferenceDocument9 pagesGeneral Journal: Date Account Titles and Explanation Debit Credit Posting ReferenceCherrie Mae BanaagNo ratings yet

- Accounting Cycle and Book of AccountsDocument23 pagesAccounting Cycle and Book of AccountsChaaaNo ratings yet

- Entrepreneurship 2nd Q.exam OktcindyDocument8 pagesEntrepreneurship 2nd Q.exam OktcindyDaryl MacatbagNo ratings yet

- Exercise 3 Leah GarciaDocument12 pagesExercise 3 Leah GarciaMa Sophia Mikaela EreceNo ratings yet

- Fabm1 Completing The Accounting CycleDocument16 pagesFabm1 Completing The Accounting CycleVenice100% (1)

- Bart M ManuelDocument27 pagesBart M ManuelBea TiuNo ratings yet

- I. Multiple Choice: Read and Analyze Each Item. Circle The Letter of The Best Answer. 1Document3 pagesI. Multiple Choice: Read and Analyze Each Item. Circle The Letter of The Best Answer. 1HLeigh Nietes-GabutanNo ratings yet

- Fundamentals of Accountancy, Business and Management 1Document19 pagesFundamentals of Accountancy, Business and Management 1Shiellai Mae Polintang0% (1)

- Fabm1 Quarter1 Module 6.2 Week 6Document22 pagesFabm1 Quarter1 Module 6.2 Week 6Danny BulacsoNo ratings yet

- Fabm Nites PrintDocument3 pagesFabm Nites Printwiz wizNo ratings yet

- Fabm2 - Se (2) Answer KeyDocument2 pagesFabm2 - Se (2) Answer Keyl m100% (1)

- Journal Entry DiscussionDocument8 pagesJournal Entry DiscussionAyesha Eunice SalvaleonNo ratings yet

- Abm Fabm1 Airs LM q4-m9Document18 pagesAbm Fabm1 Airs LM q4-m9MEDILEN O. BORRESNo ratings yet

- Practical Accounting 1Document90 pagesPractical Accounting 1Honie Rose MondayNo ratings yet

- Financial Statemtents ShortDocument7 pagesFinancial Statemtents Shortgk concepcionNo ratings yet

- ADJUSTING AND CLOSING ENTRIES Assignment Nov 20 2020Document4 pagesADJUSTING AND CLOSING ENTRIES Assignment Nov 20 2020Kayle MallillinNo ratings yet

- Balance Sheet Only-Agatha TradingDocument1 pageBalance Sheet Only-Agatha TradingJasmine Acta0% (1)

- Fabm 1 ExamDocument2 pagesFabm 1 ExamJasfer Niño100% (1)

- PeriodicDocument23 pagesPeriodicalmorsNo ratings yet

- Midterm 2nd 3rd Meeting RevisedDocument6 pagesMidterm 2nd 3rd Meeting RevisedChristopher CristobalNo ratings yet

- Business Math Quarter 3 Week 2Document8 pagesBusiness Math Quarter 3 Week 2Gladys Angela ValdemoroNo ratings yet

- ABM 3 Quarterly ExamDocument2 pagesABM 3 Quarterly ExamLenyBarrogaNo ratings yet

- Name of Examinee: - : Prepare The FollowingDocument15 pagesName of Examinee: - : Prepare The FollowingNoel CarpioNo ratings yet

- Week 6Document11 pagesWeek 6Kim Albero CubelNo ratings yet

- Module 0 Review Accounting 1 PDFDocument40 pagesModule 0 Review Accounting 1 PDFJmaseNo ratings yet

- Accounting 2 - Unit 3 - Lesson 1 To 3Document62 pagesAccounting 2 - Unit 3 - Lesson 1 To 3Merdwindelle AllagonesNo ratings yet

- ABM - 111 - Final ExaminationDocument2 pagesABM - 111 - Final ExaminationTimothy JamesNo ratings yet

- Fundamentals of Accountancy Business and Management 1 11 FourthDocument4 pagesFundamentals of Accountancy Business and Management 1 11 FourthPaulo Amposta CarpioNo ratings yet

- Practice Problem 21: Name Date Course/Year ScoreDocument3 pagesPractice Problem 21: Name Date Course/Year ScorePaw VerdilloNo ratings yet

- Module-1 GovtAcctgDocument8 pagesModule-1 GovtAcctgKrestyl Ann GabaldaNo ratings yet

- Rizal Place in Dapitan (Group 5)Document5 pagesRizal Place in Dapitan (Group 5)Krestyl Ann GabaldaNo ratings yet

- Chips Not DoneDocument42 pagesChips Not DoneKrestyl Ann GabaldaNo ratings yet

- Bag o Na ChipsDocument45 pagesBag o Na ChipsKrestyl Ann GabaldaNo ratings yet

- Parcor QuizbowlDocument38 pagesParcor QuizbowlKrestyl Ann GabaldaNo ratings yet

- Net Estate & Estate Tax: Conjugal Partnership of GainsDocument10 pagesNet Estate & Estate Tax: Conjugal Partnership of GainsKrestyl Ann GabaldaNo ratings yet

- Conceptual Framework and Accounting StandardsDocument4 pagesConceptual Framework and Accounting StandardsKrestyl Ann GabaldaNo ratings yet

- Article 1176-1185 FinalDocument37 pagesArticle 1176-1185 FinalKrestyl Ann Gabalda100% (1)

- Cost AccountingDocument64 pagesCost AccountingKrestyl Ann GabaldaNo ratings yet

- Forms of Business Organization Learning ObjectivesDocument5 pagesForms of Business Organization Learning ObjectivesKrestyl Ann GabaldaNo ratings yet

- Activity With Youtube Video Shareholders Equity Part 1Document2 pagesActivity With Youtube Video Shareholders Equity Part 1Krestyl Ann GabaldaNo ratings yet

- PIS 2019 With VATDocument19 pagesPIS 2019 With VATKrestyl Ann GabaldaNo ratings yet

- Tak - An NakoDocument30 pagesTak - An NakoKrestyl Ann GabaldaNo ratings yet

- Accounting Research Method ACCTG 322 Jhoelyn MaguadDocument3 pagesAccounting Research Method ACCTG 322 Jhoelyn MaguadKrestyl Ann GabaldaNo ratings yet

- Rizal Long QuizDocument2 pagesRizal Long QuizKrestyl Ann GabaldaNo ratings yet

- Students Perception Towards Digital Payment System-A Study With A Special Reference To Mangalore UniversityDocument20 pagesStudents Perception Towards Digital Payment System-A Study With A Special Reference To Mangalore UniversityKrestyl Ann GabaldaNo ratings yet

- United States Court of Appeals, Third CircuitDocument1 pageUnited States Court of Appeals, Third CircuitScribd Government DocsNo ratings yet

- Goods Supply Agreement TemplateDocument8 pagesGoods Supply Agreement TemplateSanjeev ThakurNo ratings yet

- Statement of JurisdictionDocument13 pagesStatement of JurisdictionMouneeshNo ratings yet

- The Growing Role of Forensic Science in Criminal Investigation: Admissibility in The Indian Legal System and Future PerspectiveDocument8 pagesThe Growing Role of Forensic Science in Criminal Investigation: Admissibility in The Indian Legal System and Future PerspectiveMavvyy KishwarNo ratings yet

- Phil. Export v. Amalmagated Management, Et. Al.Document8 pagesPhil. Export v. Amalmagated Management, Et. Al.CZARINA ANN CASTRONo ratings yet

- Duties of Agent PrincipalDocument18 pagesDuties of Agent PrincipalJulietha YusnizamNo ratings yet

- Comments To Commentary On UCP 600 - A Critical ReviewDocument7 pagesComments To Commentary On UCP 600 - A Critical Reviewvkrm14No ratings yet

- Civil - 104 - GR 208140Document7 pagesCivil - 104 - GR 208140Firdous Gayak SumailNo ratings yet

- Case Digest On CopyrightDocument4 pagesCase Digest On CopyrightAllan CalvoNo ratings yet

- Requirements For Cpa AccreditationDocument1 pageRequirements For Cpa AccreditationJ'ca EdulanNo ratings yet

- Slide1 Slide 2 What Is Competition ActDocument2 pagesSlide1 Slide 2 What Is Competition Actrobin hoodNo ratings yet

- Name: Charlotte Cabading Subject: ENG 111 Course/Year/Set: BSDRM SET ADocument10 pagesName: Charlotte Cabading Subject: ENG 111 Course/Year/Set: BSDRM SET AJudeza Jaira B. LabadanNo ratings yet

- Board-Excom For BUCAP July 2020Document4 pagesBoard-Excom For BUCAP July 2020Jebs KwanNo ratings yet

- A Caricature Grievances Speech AquinoDocument39 pagesA Caricature Grievances Speech AquinoJessa CañadaNo ratings yet

- E-Governance Police Prison PSUsDocument4 pagesE-Governance Police Prison PSUssh LaksNo ratings yet

- Capital Gains Tax Acknowledgment ReceiptDocument1 pageCapital Gains Tax Acknowledgment ReceiptDavid MugambiNo ratings yet

- Proposed Guidelines On Conduct of VideoconferencingDocument6 pagesProposed Guidelines On Conduct of VideoconferencingPolo MartinezNo ratings yet

- Traffic CountDocument32 pagesTraffic Countobrkh 07No ratings yet

- The Competition Commission of PakistanDocument10 pagesThe Competition Commission of Pakistanranag28No ratings yet

- UTHR LQDA - Tyvaso Patent IPR - 11 Aug 21Document44 pagesUTHR LQDA - Tyvaso Patent IPR - 11 Aug 21XDL1No ratings yet

- History and Development of Securities Laws in IndiaDocument3 pagesHistory and Development of Securities Laws in IndiaTathagat ShívanshNo ratings yet

- Ii LL.B 3RD Sem Viva Voce SCHDocument1 pageIi LL.B 3RD Sem Viva Voce SCHshivaNo ratings yet

- Zaragoza Vs TanDocument4 pagesZaragoza Vs TanADNo ratings yet

- Jorge Stalin Vitar Semanate, 21jan 1805 QuitoDocument3 pagesJorge Stalin Vitar Semanate, 21jan 1805 QuitoDamian RobleroNo ratings yet

- Taxguru - In-Revised Procedure For MVATCSTPTRCPTEC Registration in MaharashtraDocument3 pagesTaxguru - In-Revised Procedure For MVATCSTPTRCPTEC Registration in MaharashtraOmPrakashAgrawalNo ratings yet

- 01 Quiz 1aDocument3 pages01 Quiz 1aJoffrey MellamaNo ratings yet

- Form LCM - Labuan Company Managementv2 - 04032021Document18 pagesForm LCM - Labuan Company Managementv2 - 04032021danNo ratings yet