A Comparative Analysis of The Economic Growth of China and India

A Comparative Analysis of The Economic Growth of China and India

You might also like

- Case Study On BRICSDocument12 pagesCase Study On BRICSTalha AmirNo ratings yet

- An Comparative Analysis of Economic Growth Between India and ChinaDocument32 pagesAn Comparative Analysis of Economic Growth Between India and ChinasubornoNo ratings yet

- China and India and BrazilDocument11 pagesChina and India and Brazilcsc_abcNo ratings yet

- 67 Chinas Economic Growth Effects and Consequences On The WorldDocument16 pages67 Chinas Economic Growth Effects and Consequences On The WorldNisar Ahmed MagsiNo ratings yet

- The World Under Pressure: How China and India Are Influencing the Global Economy and EnvironmentFrom EverandThe World Under Pressure: How China and India Are Influencing the Global Economy and EnvironmentNo ratings yet

- Impact of Financial Development and Technological Innovation On The Volatility of Green Growth - Evidence From ChinaDocument18 pagesImpact of Financial Development and Technological Innovation On The Volatility of Green Growth - Evidence From ChinaThanh Phúc NguyễnNo ratings yet

- Md. Noor Alam - (3-20-44-021) - EM-559 Globalization and Strategy - Mid Term-IDocument13 pagesMd. Noor Alam - (3-20-44-021) - EM-559 Globalization and Strategy - Mid Term-INoor AlamNo ratings yet

- DF FD GrowthDocument15 pagesDF FD GrowthMinh PhươngNo ratings yet

- The Contribution of Economic Sectors To Economic Growth: The Cases of Malaysia and ChinaDocument13 pagesThe Contribution of Economic Sectors To Economic Growth: The Cases of Malaysia and ChinaNita Kumala SariNo ratings yet

- Comparing China and IndiaDocument43 pagesComparing China and IndiaKingsley ONo ratings yet

- The Contribution of Human Capital To China's Economic GrowthDocument35 pagesThe Contribution of Human Capital To China's Economic GrowthIrcham NizarNo ratings yet

- Framing India: Pre-Post Globalization: February 2013Document17 pagesFraming India: Pre-Post Globalization: February 2013Ashutosh SharmaNo ratings yet

- Economic Systems: Jens Ho Lscher, Enrico Marelli, Marcello SignorelliDocument6 pagesEconomic Systems: Jens Ho Lscher, Enrico Marelli, Marcello Signorellikalita_onlineNo ratings yet

- The Contribution of Economic Sectors To Economic Growth The Cases of Malaysia and ChinaDocument13 pagesThe Contribution of Economic Sectors To Economic Growth The Cases of Malaysia and ChinaPurityNo ratings yet

- An Overview of Fruits and Vegetables Trade of China: March 2018Document13 pagesAn Overview of Fruits and Vegetables Trade of China: March 2018Lalu Kosim PutradiNo ratings yet

- Institute of Developing Economies: Infrastructure Development and Economic Growth in ChinaDocument39 pagesInstitute of Developing Economies: Infrastructure Development and Economic Growth in ChinaduplesyNo ratings yet

- India Vs ChinaDocument9 pagesIndia Vs ChinaArjun MalhotraNo ratings yet

- A10818 M1Document20 pagesA10818 M1Ahmad Nawaz ChaudhryNo ratings yet

- TBL - Gu, 2020Document27 pagesTBL - Gu, 2020RodolfoNo ratings yet

- A Theoretical and Empirical Studies On The High-Quality Development of China's EconomyDocument17 pagesA Theoretical and Empirical Studies On The High-Quality Development of China's EconomyIJELS Research JournalNo ratings yet

- Jurnal Financial Developing PDFDocument12 pagesJurnal Financial Developing PDFMichael ComunityNo ratings yet

- Xiong Yuning Research On The Cultivation of The Digital Economy Ecosystem 1 15Document15 pagesXiong Yuning Research On The Cultivation of The Digital Economy Ecosystem 1 15Yunita DwiNo ratings yet

- Sustainability 10 01194 v2 PDFDocument20 pagesSustainability 10 01194 v2 PDFRajendra LamsalNo ratings yet

- Indo-China Trade Trends Composition and FutureDocument10 pagesIndo-China Trade Trends Composition and FutureMohammed RazikNo ratings yet

- Changes in Vietnam - China Trade in The Context of China's Economic Slowdown: Some Analysis and ImplicationsDocument13 pagesChanges in Vietnam - China Trade in The Context of China's Economic Slowdown: Some Analysis and ImplicationsJenNo ratings yet

- Lessons From Korean Innovation Model For ASEAN Countries Towards A Knowledge EconomyDocument22 pagesLessons From Korean Innovation Model For ASEAN Countries Towards A Knowledge EconomyLam TranNo ratings yet

- China's Path Towards New Growth - Drivers of Human Capital, InnovationDocument21 pagesChina's Path Towards New Growth - Drivers of Human Capital, InnovationMurad HajiyevNo ratings yet

- Li HumanCapitalChinas 2017Document24 pagesLi HumanCapitalChinas 2017Tomas Enrique CARDENASNo ratings yet

- China and India: Economic Performance, Competition and Cooperation An UpdateDocument38 pagesChina and India: Economic Performance, Competition and Cooperation An UpdateSameer AnsariNo ratings yet

- A Celio Hiratuka (2018) CHANGES IN THE CHINESE DEVELOPMENT STRATEGYDocument25 pagesA Celio Hiratuka (2018) CHANGES IN THE CHINESE DEVELOPMENT STRATEGY14641 14641No ratings yet

- Indian Economic GrowthDocument24 pagesIndian Economic GrowthManas PuriNo ratings yet

- The Effect of Economic Growth in Terms of Expenditure On Poverty in IndonesiaDocument12 pagesThe Effect of Economic Growth in Terms of Expenditure On Poverty in IndonesiaIvan Rahmat SantosoNo ratings yet

- SSRN Id2658996Document19 pagesSSRN Id2658996haianh110603No ratings yet

- Jungho Baek@ndsu EduDocument32 pagesJungho Baek@ndsu Edutran phankNo ratings yet

- CAS Report SitharaDocument7 pagesCAS Report SitharaNAVYA PNo ratings yet

- Contemporary Indian Economy: A Review of Recent Trend and Debates Over Development ParadigmDocument12 pagesContemporary Indian Economy: A Review of Recent Trend and Debates Over Development ParadigmShefali KotichaNo ratings yet

- SSRN Id3127280Document61 pagesSSRN Id3127280SD RanaNo ratings yet

- EsaayDocument7 pagesEsaayerkaim.dzhunushovaNo ratings yet

- The Elephant and The DragonDocument3 pagesThe Elephant and The DragonHassan RazaNo ratings yet

- IFM Project-18IB343 (Apparels in China)Document16 pagesIFM Project-18IB343 (Apparels in China)RABIA MONGA-IBNo ratings yet

- An Study On Public Expenditure On Social Sector in Tamil Nadu From 2001-2002 To 2017-2018Document7 pagesAn Study On Public Expenditure On Social Sector in Tamil Nadu From 2001-2002 To 2017-2018IAEME PublicationNo ratings yet

- Final Business ReportDocument13 pagesFinal Business ReportFahad AhmedNo ratings yet

- Comparing China and India: An Introduction: The European Journal of Comparative Economics June 2009Document4 pagesComparing China and India: An Introduction: The European Journal of Comparative Economics June 2009Upasana GuptaNo ratings yet

- Ifm - Term PaperDocument19 pagesIfm - Term PaperpriyankaNo ratings yet

- FDI Sector Analysis BricsDocument7 pagesFDI Sector Analysis Bricsminushastri33No ratings yet

- 6 PDFDocument10 pages6 PDFNalin KarunarathneNo ratings yet

- Determinants of Economic Growth in Sub SDocument7 pagesDeterminants of Economic Growth in Sub SInnocent escoNo ratings yet

- Impact of Foreign Direct Investment (FDI) On The Growth of The Indian EconomyDocument5 pagesImpact of Foreign Direct Investment (FDI) On The Growth of The Indian EconomyDylan WilcoxNo ratings yet

- 3-A027-National Systems of Innovation Toward A Theory of Innovation and Interactive Learning by Lundvall, Bengt-Åke (Z-LibDocument18 pages3-A027-National Systems of Innovation Toward A Theory of Innovation and Interactive Learning by Lundvall, Bengt-Åke (Z-Libwen zhangNo ratings yet

- Economies 06 00056Document23 pagesEconomies 06 00056Divine Lerre RocacorbaNo ratings yet

- 19 Dr. v. K. Goswami Eng Vol4 Issue1Document8 pages19 Dr. v. K. Goswami Eng Vol4 Issue1Subbarao VenkataNo ratings yet

- India and China: A Special Economic Analysis: New Tigers of AsiaDocument60 pagesIndia and China: A Special Economic Analysis: New Tigers of AsiaLiang WangNo ratings yet

- The System of Innovation and Its Impact On Economic DevelopmentDocument3 pagesThe System of Innovation and Its Impact On Economic DevelopmentEditor IJTSRDNo ratings yet

- He2019 Article EntrepreneurshipInChinaDocument10 pagesHe2019 Article EntrepreneurshipInChinaJose TapiaNo ratings yet

- Research Paper On Comparative Analysis of Growth Models: India Vs ChinaDocument3 pagesResearch Paper On Comparative Analysis of Growth Models: India Vs ChinaKanishq BawejaNo ratings yet

- Make in India: Impact On Indian EconomyDocument7 pagesMake in India: Impact On Indian EconomyJAIVANTNo ratings yet

- Andriansyah Et Al. (2023)Document28 pagesAndriansyah Et Al. (2023)Pawestri UtamiNo ratings yet

- China's Environmental Governance in Transition: Arthur P. J. Mol & Neil T. CarterDocument22 pagesChina's Environmental Governance in Transition: Arthur P. J. Mol & Neil T. CarteransidNo ratings yet

- China (2022)Document22 pagesChina (2022)Faus VegaNo ratings yet

- ePRANCARDVIEWDocument1 pageePRANCARDVIEWAadhityaNo ratings yet

- 11114-Article Text-13345-1-10-20191118Document10 pages11114-Article Text-13345-1-10-20191118AadhityaNo ratings yet

- International Space LawDocument9 pagesInternational Space LawAadhityaNo ratings yet

- Sovereignity and JurisdictionDocument27 pagesSovereignity and JurisdictionAadhityaNo ratings yet

- Impact of The Right To Information ActDocument23 pagesImpact of The Right To Information ActAadhityaNo ratings yet

- Patent Law and BiotechnologyDocument12 pagesPatent Law and BiotechnologyAadhityaNo ratings yet

- World Development: Jeannine E. Relly, Md. Fazle Rabbi, Meghna Sabharwal, Rajdeep Pakanati, Ethan H. SchwalbeDocument15 pagesWorld Development: Jeannine E. Relly, Md. Fazle Rabbi, Meghna Sabharwal, Rajdeep Pakanati, Ethan H. SchwalbeAadhityaNo ratings yet

- SSRN Id1999541Document15 pagesSSRN Id1999541AadhityaNo ratings yet

- Right To Information Act (RTI ACT 2005) A Perspective Study On Government Employees of IndiaDocument9 pagesRight To Information Act (RTI ACT 2005) A Perspective Study On Government Employees of IndiaAadhityaNo ratings yet

- RighttoInformation BOOKDocument86 pagesRighttoInformation BOOKAadhityaNo ratings yet

- Fifteen Years of Right To Information Act in India: AlongwaytogoDocument17 pagesFifteen Years of Right To Information Act in India: AlongwaytogoAadhityaNo ratings yet

- V. U. W. Law RiviiwDocument10 pagesV. U. W. Law RiviiwAadhityaNo ratings yet

- Economic GlobalizationDocument5 pagesEconomic GlobalizationAadhityaNo ratings yet

- JIGL MarathonDocument62 pagesJIGL MarathonAadhityaNo ratings yet

- JIGLDocument203 pagesJIGLAadhityaNo ratings yet

- Feminist Justice by Way of Women'S Rights To Property: An Indian Approach After IndependenceDocument19 pagesFeminist Justice by Way of Women'S Rights To Property: An Indian Approach After IndependenceAadhityaNo ratings yet

- Social Media and Social Movements: Sociology Compass September 2016Document11 pagesSocial Media and Social Movements: Sociology Compass September 2016AadhityaNo ratings yet

- Separate Legal Personality Legal Reality and Metaphor: Nichola A eDocument12 pagesSeparate Legal Personality Legal Reality and Metaphor: Nichola A eAadhityaNo ratings yet

- C Law Main Note PDFDocument415 pagesC Law Main Note PDFAadhityaNo ratings yet

- A Ripple in TimeDocument2 pagesA Ripple in TimeAadhityaNo ratings yet

- Civil Courts ActDocument12 pagesCivil Courts ActAadhityaNo ratings yet

- The Conflict Between Communal Religious Freedom and Women's Equality: A Proposal For Reform of The Hindu Succession Act of 1956Document20 pagesThe Conflict Between Communal Religious Freedom and Women's Equality: A Proposal For Reform of The Hindu Succession Act of 1956AadhityaNo ratings yet

- This Content Downloaded From 157.51.59.153 On Fri, 19 Nov 2021 15:20:32 UTCDocument5 pagesThis Content Downloaded From 157.51.59.153 On Fri, 19 Nov 2021 15:20:32 UTCAadhityaNo ratings yet

- What May Be TransferredDocument25 pagesWhat May Be TransferredAadhityaNo ratings yet

- Critical Analysis of Section 6 of The HiDocument2 pagesCritical Analysis of Section 6 of The HiAadhityaNo ratings yet

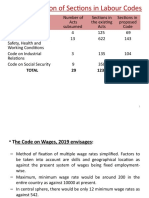

- Rationalization of Sections in Labour Codes: Total 29 1232 480Document49 pagesRationalization of Sections in Labour Codes: Total 29 1232 480AadhityaNo ratings yet

- THM 102 Zimbabwe Tourism GeographyDocument21 pagesTHM 102 Zimbabwe Tourism GeographySimba NemapareNo ratings yet

- AssignmentDocument8 pagesAssignmentpintu ram0% (1)

- Migration of Skilled Nurses From Bangladesh: An Exploratory StudyDocument32 pagesMigration of Skilled Nurses From Bangladesh: An Exploratory StudyNoman HossainNo ratings yet

- Exploring The Factors That Influence The Intentions of Filipino 4 TH Year Medical Technology Students To Work AbroadDocument11 pagesExploring The Factors That Influence The Intentions of Filipino 4 TH Year Medical Technology Students To Work AbroadInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Remittances in NepalDocument32 pagesRemittances in NepalChandan SapkotaNo ratings yet

- Triple-Win Migration: Challenges and OpportunitiesDocument16 pagesTriple-Win Migration: Challenges and OpportunitiesGerman Marshall Fund of the United StatesNo ratings yet

- Prefinal ModuleDocument12 pagesPrefinal ModuleCORES LYRICSNo ratings yet

- Impact of Chinese Goods On Indian MarketDocument18 pagesImpact of Chinese Goods On Indian MarketHiral SoniNo ratings yet

- Annual Report 2015Document300 pagesAnnual Report 2015Iqbal H Biplob100% (1)

- SASRA Supervisory Report 2011Document68 pagesSASRA Supervisory Report 2011elinzola100% (2)

- Migration AND RemittancesDocument54 pagesMigration AND RemittancesSantosh MahatoNo ratings yet

- SPECPOL Background GuideDocument37 pagesSPECPOL Background Guidemohit kumarNo ratings yet

- Milestones Bangladesh Have Crossed in 50 YearsDocument6 pagesMilestones Bangladesh Have Crossed in 50 Yearssoumic ahmedNo ratings yet

- Workers' Remittances and Economic Growth in The Philippines: July 2007Document17 pagesWorkers' Remittances and Economic Growth in The Philippines: July 2007Floramae PasculadoNo ratings yet

- Wubalem Woreket PDFDocument105 pagesWubalem Woreket PDFYisehak AbrehamNo ratings yet

- All Icai MCQ of Law Nov. 19-39-63Document25 pagesAll Icai MCQ of Law Nov. 19-39-63yakub pashaNo ratings yet

- CFLCBrazil Impact of Western Public Finance in Least Developed CountriesDocument10 pagesCFLCBrazil Impact of Western Public Finance in Least Developed Countriescluadine dinerosNo ratings yet

- English Practice Paper - 6Document12 pagesEnglish Practice Paper - 6PlayMaxNo ratings yet

- Do Victims Only CryDocument143 pagesDo Victims Only Cryivanandres2008No ratings yet

- Mobile Money Competing With Informal Channels To Accelerate The Digitisation of RemittancesDocument26 pagesMobile Money Competing With Informal Channels To Accelerate The Digitisation of RemittancesMo BenNo ratings yet

- FORM A2 Revised FormDocument6 pagesFORM A2 Revised Formcopy catNo ratings yet

- Urban Economy, and Urban Rural LinnkagesDocument26 pagesUrban Economy, and Urban Rural LinnkagesBimantara Von AikenNo ratings yet

- Current State of Nepali EconomyDocument39 pagesCurrent State of Nepali EconomyChandan SapkotaNo ratings yet

- Macroeconomic Situation in BangladeshDocument31 pagesMacroeconomic Situation in BangladeshShyam Bin JamilNo ratings yet

- Mexican Migration - Who Has The Right To MigrateDocument10 pagesMexican Migration - Who Has The Right To Migrateemilio27aNo ratings yet

- Remittance Performance of Islami Banks and Conventional Banks: A Comparative StudyDocument60 pagesRemittance Performance of Islami Banks and Conventional Banks: A Comparative Studynyeemalahad67% (3)

- Light Account Process GuideDocument26 pagesLight Account Process Guidemohamed mansourNo ratings yet

- Messari Report Asia Crypto LandscapeDocument99 pagesMessari Report Asia Crypto LandscapeDicky IrwansyahNo ratings yet

- Ethical Practice in Correspondent BankingDocument35 pagesEthical Practice in Correspondent Bankingmahesh ojhaNo ratings yet

- Caltex Vs Commission On Audit 1992Document1 pageCaltex Vs Commission On Audit 1992Praisah Marjorey PicotNo ratings yet

Download as pdf or txt

You might also like

- Case Study On BRICSDocument12 pagesCase Study On BRICSTalha AmirNo ratings yet

- An Comparative Analysis of Economic Growth Between India and ChinaDocument32 pagesAn Comparative Analysis of Economic Growth Between India and ChinasubornoNo ratings yet

- China and India and BrazilDocument11 pagesChina and India and Brazilcsc_abcNo ratings yet

- 67 Chinas Economic Growth Effects and Consequences On The WorldDocument16 pages67 Chinas Economic Growth Effects and Consequences On The WorldNisar Ahmed MagsiNo ratings yet

- The World Under Pressure: How China and India Are Influencing the Global Economy and EnvironmentFrom EverandThe World Under Pressure: How China and India Are Influencing the Global Economy and EnvironmentNo ratings yet

- Impact of Financial Development and Technological Innovation On The Volatility of Green Growth - Evidence From ChinaDocument18 pagesImpact of Financial Development and Technological Innovation On The Volatility of Green Growth - Evidence From ChinaThanh Phúc NguyễnNo ratings yet

- Md. Noor Alam - (3-20-44-021) - EM-559 Globalization and Strategy - Mid Term-IDocument13 pagesMd. Noor Alam - (3-20-44-021) - EM-559 Globalization and Strategy - Mid Term-INoor AlamNo ratings yet

- DF FD GrowthDocument15 pagesDF FD GrowthMinh PhươngNo ratings yet

- The Contribution of Economic Sectors To Economic Growth: The Cases of Malaysia and ChinaDocument13 pagesThe Contribution of Economic Sectors To Economic Growth: The Cases of Malaysia and ChinaNita Kumala SariNo ratings yet

- Comparing China and IndiaDocument43 pagesComparing China and IndiaKingsley ONo ratings yet

- The Contribution of Human Capital To China's Economic GrowthDocument35 pagesThe Contribution of Human Capital To China's Economic GrowthIrcham NizarNo ratings yet

- Framing India: Pre-Post Globalization: February 2013Document17 pagesFraming India: Pre-Post Globalization: February 2013Ashutosh SharmaNo ratings yet

- Economic Systems: Jens Ho Lscher, Enrico Marelli, Marcello SignorelliDocument6 pagesEconomic Systems: Jens Ho Lscher, Enrico Marelli, Marcello Signorellikalita_onlineNo ratings yet

- The Contribution of Economic Sectors To Economic Growth The Cases of Malaysia and ChinaDocument13 pagesThe Contribution of Economic Sectors To Economic Growth The Cases of Malaysia and ChinaPurityNo ratings yet

- An Overview of Fruits and Vegetables Trade of China: March 2018Document13 pagesAn Overview of Fruits and Vegetables Trade of China: March 2018Lalu Kosim PutradiNo ratings yet

- Institute of Developing Economies: Infrastructure Development and Economic Growth in ChinaDocument39 pagesInstitute of Developing Economies: Infrastructure Development and Economic Growth in ChinaduplesyNo ratings yet

- India Vs ChinaDocument9 pagesIndia Vs ChinaArjun MalhotraNo ratings yet

- A10818 M1Document20 pagesA10818 M1Ahmad Nawaz ChaudhryNo ratings yet

- TBL - Gu, 2020Document27 pagesTBL - Gu, 2020RodolfoNo ratings yet

- A Theoretical and Empirical Studies On The High-Quality Development of China's EconomyDocument17 pagesA Theoretical and Empirical Studies On The High-Quality Development of China's EconomyIJELS Research JournalNo ratings yet

- Jurnal Financial Developing PDFDocument12 pagesJurnal Financial Developing PDFMichael ComunityNo ratings yet

- Xiong Yuning Research On The Cultivation of The Digital Economy Ecosystem 1 15Document15 pagesXiong Yuning Research On The Cultivation of The Digital Economy Ecosystem 1 15Yunita DwiNo ratings yet

- Sustainability 10 01194 v2 PDFDocument20 pagesSustainability 10 01194 v2 PDFRajendra LamsalNo ratings yet

- Indo-China Trade Trends Composition and FutureDocument10 pagesIndo-China Trade Trends Composition and FutureMohammed RazikNo ratings yet

- Changes in Vietnam - China Trade in The Context of China's Economic Slowdown: Some Analysis and ImplicationsDocument13 pagesChanges in Vietnam - China Trade in The Context of China's Economic Slowdown: Some Analysis and ImplicationsJenNo ratings yet

- Lessons From Korean Innovation Model For ASEAN Countries Towards A Knowledge EconomyDocument22 pagesLessons From Korean Innovation Model For ASEAN Countries Towards A Knowledge EconomyLam TranNo ratings yet

- China's Path Towards New Growth - Drivers of Human Capital, InnovationDocument21 pagesChina's Path Towards New Growth - Drivers of Human Capital, InnovationMurad HajiyevNo ratings yet

- Li HumanCapitalChinas 2017Document24 pagesLi HumanCapitalChinas 2017Tomas Enrique CARDENASNo ratings yet

- China and India: Economic Performance, Competition and Cooperation An UpdateDocument38 pagesChina and India: Economic Performance, Competition and Cooperation An UpdateSameer AnsariNo ratings yet

- A Celio Hiratuka (2018) CHANGES IN THE CHINESE DEVELOPMENT STRATEGYDocument25 pagesA Celio Hiratuka (2018) CHANGES IN THE CHINESE DEVELOPMENT STRATEGY14641 14641No ratings yet

- Indian Economic GrowthDocument24 pagesIndian Economic GrowthManas PuriNo ratings yet

- The Effect of Economic Growth in Terms of Expenditure On Poverty in IndonesiaDocument12 pagesThe Effect of Economic Growth in Terms of Expenditure On Poverty in IndonesiaIvan Rahmat SantosoNo ratings yet

- SSRN Id2658996Document19 pagesSSRN Id2658996haianh110603No ratings yet

- Jungho Baek@ndsu EduDocument32 pagesJungho Baek@ndsu Edutran phankNo ratings yet

- CAS Report SitharaDocument7 pagesCAS Report SitharaNAVYA PNo ratings yet

- Contemporary Indian Economy: A Review of Recent Trend and Debates Over Development ParadigmDocument12 pagesContemporary Indian Economy: A Review of Recent Trend and Debates Over Development ParadigmShefali KotichaNo ratings yet

- SSRN Id3127280Document61 pagesSSRN Id3127280SD RanaNo ratings yet

- EsaayDocument7 pagesEsaayerkaim.dzhunushovaNo ratings yet

- The Elephant and The DragonDocument3 pagesThe Elephant and The DragonHassan RazaNo ratings yet

- IFM Project-18IB343 (Apparels in China)Document16 pagesIFM Project-18IB343 (Apparels in China)RABIA MONGA-IBNo ratings yet

- An Study On Public Expenditure On Social Sector in Tamil Nadu From 2001-2002 To 2017-2018Document7 pagesAn Study On Public Expenditure On Social Sector in Tamil Nadu From 2001-2002 To 2017-2018IAEME PublicationNo ratings yet

- Final Business ReportDocument13 pagesFinal Business ReportFahad AhmedNo ratings yet

- Comparing China and India: An Introduction: The European Journal of Comparative Economics June 2009Document4 pagesComparing China and India: An Introduction: The European Journal of Comparative Economics June 2009Upasana GuptaNo ratings yet

- Ifm - Term PaperDocument19 pagesIfm - Term PaperpriyankaNo ratings yet

- FDI Sector Analysis BricsDocument7 pagesFDI Sector Analysis Bricsminushastri33No ratings yet

- 6 PDFDocument10 pages6 PDFNalin KarunarathneNo ratings yet

- Determinants of Economic Growth in Sub SDocument7 pagesDeterminants of Economic Growth in Sub SInnocent escoNo ratings yet

- Impact of Foreign Direct Investment (FDI) On The Growth of The Indian EconomyDocument5 pagesImpact of Foreign Direct Investment (FDI) On The Growth of The Indian EconomyDylan WilcoxNo ratings yet

- 3-A027-National Systems of Innovation Toward A Theory of Innovation and Interactive Learning by Lundvall, Bengt-Åke (Z-LibDocument18 pages3-A027-National Systems of Innovation Toward A Theory of Innovation and Interactive Learning by Lundvall, Bengt-Åke (Z-Libwen zhangNo ratings yet

- Economies 06 00056Document23 pagesEconomies 06 00056Divine Lerre RocacorbaNo ratings yet

- 19 Dr. v. K. Goswami Eng Vol4 Issue1Document8 pages19 Dr. v. K. Goswami Eng Vol4 Issue1Subbarao VenkataNo ratings yet

- India and China: A Special Economic Analysis: New Tigers of AsiaDocument60 pagesIndia and China: A Special Economic Analysis: New Tigers of AsiaLiang WangNo ratings yet

- The System of Innovation and Its Impact On Economic DevelopmentDocument3 pagesThe System of Innovation and Its Impact On Economic DevelopmentEditor IJTSRDNo ratings yet

- He2019 Article EntrepreneurshipInChinaDocument10 pagesHe2019 Article EntrepreneurshipInChinaJose TapiaNo ratings yet

- Research Paper On Comparative Analysis of Growth Models: India Vs ChinaDocument3 pagesResearch Paper On Comparative Analysis of Growth Models: India Vs ChinaKanishq BawejaNo ratings yet

- Make in India: Impact On Indian EconomyDocument7 pagesMake in India: Impact On Indian EconomyJAIVANTNo ratings yet

- Andriansyah Et Al. (2023)Document28 pagesAndriansyah Et Al. (2023)Pawestri UtamiNo ratings yet

- China's Environmental Governance in Transition: Arthur P. J. Mol & Neil T. CarterDocument22 pagesChina's Environmental Governance in Transition: Arthur P. J. Mol & Neil T. CarteransidNo ratings yet

- China (2022)Document22 pagesChina (2022)Faus VegaNo ratings yet

- ePRANCARDVIEWDocument1 pageePRANCARDVIEWAadhityaNo ratings yet

- 11114-Article Text-13345-1-10-20191118Document10 pages11114-Article Text-13345-1-10-20191118AadhityaNo ratings yet

- International Space LawDocument9 pagesInternational Space LawAadhityaNo ratings yet

- Sovereignity and JurisdictionDocument27 pagesSovereignity and JurisdictionAadhityaNo ratings yet

- Impact of The Right To Information ActDocument23 pagesImpact of The Right To Information ActAadhityaNo ratings yet

- Patent Law and BiotechnologyDocument12 pagesPatent Law and BiotechnologyAadhityaNo ratings yet

- World Development: Jeannine E. Relly, Md. Fazle Rabbi, Meghna Sabharwal, Rajdeep Pakanati, Ethan H. SchwalbeDocument15 pagesWorld Development: Jeannine E. Relly, Md. Fazle Rabbi, Meghna Sabharwal, Rajdeep Pakanati, Ethan H. SchwalbeAadhityaNo ratings yet

- SSRN Id1999541Document15 pagesSSRN Id1999541AadhityaNo ratings yet

- Right To Information Act (RTI ACT 2005) A Perspective Study On Government Employees of IndiaDocument9 pagesRight To Information Act (RTI ACT 2005) A Perspective Study On Government Employees of IndiaAadhityaNo ratings yet

- RighttoInformation BOOKDocument86 pagesRighttoInformation BOOKAadhityaNo ratings yet

- Fifteen Years of Right To Information Act in India: AlongwaytogoDocument17 pagesFifteen Years of Right To Information Act in India: AlongwaytogoAadhityaNo ratings yet

- V. U. W. Law RiviiwDocument10 pagesV. U. W. Law RiviiwAadhityaNo ratings yet

- Economic GlobalizationDocument5 pagesEconomic GlobalizationAadhityaNo ratings yet

- JIGL MarathonDocument62 pagesJIGL MarathonAadhityaNo ratings yet

- JIGLDocument203 pagesJIGLAadhityaNo ratings yet

- Feminist Justice by Way of Women'S Rights To Property: An Indian Approach After IndependenceDocument19 pagesFeminist Justice by Way of Women'S Rights To Property: An Indian Approach After IndependenceAadhityaNo ratings yet

- Social Media and Social Movements: Sociology Compass September 2016Document11 pagesSocial Media and Social Movements: Sociology Compass September 2016AadhityaNo ratings yet

- Separate Legal Personality Legal Reality and Metaphor: Nichola A eDocument12 pagesSeparate Legal Personality Legal Reality and Metaphor: Nichola A eAadhityaNo ratings yet

- C Law Main Note PDFDocument415 pagesC Law Main Note PDFAadhityaNo ratings yet

- A Ripple in TimeDocument2 pagesA Ripple in TimeAadhityaNo ratings yet

- Civil Courts ActDocument12 pagesCivil Courts ActAadhityaNo ratings yet

- The Conflict Between Communal Religious Freedom and Women's Equality: A Proposal For Reform of The Hindu Succession Act of 1956Document20 pagesThe Conflict Between Communal Religious Freedom and Women's Equality: A Proposal For Reform of The Hindu Succession Act of 1956AadhityaNo ratings yet

- This Content Downloaded From 157.51.59.153 On Fri, 19 Nov 2021 15:20:32 UTCDocument5 pagesThis Content Downloaded From 157.51.59.153 On Fri, 19 Nov 2021 15:20:32 UTCAadhityaNo ratings yet

- What May Be TransferredDocument25 pagesWhat May Be TransferredAadhityaNo ratings yet

- Critical Analysis of Section 6 of The HiDocument2 pagesCritical Analysis of Section 6 of The HiAadhityaNo ratings yet

- Rationalization of Sections in Labour Codes: Total 29 1232 480Document49 pagesRationalization of Sections in Labour Codes: Total 29 1232 480AadhityaNo ratings yet

- THM 102 Zimbabwe Tourism GeographyDocument21 pagesTHM 102 Zimbabwe Tourism GeographySimba NemapareNo ratings yet

- AssignmentDocument8 pagesAssignmentpintu ram0% (1)

- Migration of Skilled Nurses From Bangladesh: An Exploratory StudyDocument32 pagesMigration of Skilled Nurses From Bangladesh: An Exploratory StudyNoman HossainNo ratings yet

- Exploring The Factors That Influence The Intentions of Filipino 4 TH Year Medical Technology Students To Work AbroadDocument11 pagesExploring The Factors That Influence The Intentions of Filipino 4 TH Year Medical Technology Students To Work AbroadInternational Journal of Innovative Science and Research TechnologyNo ratings yet

- Remittances in NepalDocument32 pagesRemittances in NepalChandan SapkotaNo ratings yet

- Triple-Win Migration: Challenges and OpportunitiesDocument16 pagesTriple-Win Migration: Challenges and OpportunitiesGerman Marshall Fund of the United StatesNo ratings yet

- Prefinal ModuleDocument12 pagesPrefinal ModuleCORES LYRICSNo ratings yet

- Impact of Chinese Goods On Indian MarketDocument18 pagesImpact of Chinese Goods On Indian MarketHiral SoniNo ratings yet

- Annual Report 2015Document300 pagesAnnual Report 2015Iqbal H Biplob100% (1)

- SASRA Supervisory Report 2011Document68 pagesSASRA Supervisory Report 2011elinzola100% (2)

- Migration AND RemittancesDocument54 pagesMigration AND RemittancesSantosh MahatoNo ratings yet

- SPECPOL Background GuideDocument37 pagesSPECPOL Background Guidemohit kumarNo ratings yet

- Milestones Bangladesh Have Crossed in 50 YearsDocument6 pagesMilestones Bangladesh Have Crossed in 50 Yearssoumic ahmedNo ratings yet

- Workers' Remittances and Economic Growth in The Philippines: July 2007Document17 pagesWorkers' Remittances and Economic Growth in The Philippines: July 2007Floramae PasculadoNo ratings yet

- Wubalem Woreket PDFDocument105 pagesWubalem Woreket PDFYisehak AbrehamNo ratings yet

- All Icai MCQ of Law Nov. 19-39-63Document25 pagesAll Icai MCQ of Law Nov. 19-39-63yakub pashaNo ratings yet

- CFLCBrazil Impact of Western Public Finance in Least Developed CountriesDocument10 pagesCFLCBrazil Impact of Western Public Finance in Least Developed Countriescluadine dinerosNo ratings yet

- English Practice Paper - 6Document12 pagesEnglish Practice Paper - 6PlayMaxNo ratings yet

- Do Victims Only CryDocument143 pagesDo Victims Only Cryivanandres2008No ratings yet

- Mobile Money Competing With Informal Channels To Accelerate The Digitisation of RemittancesDocument26 pagesMobile Money Competing With Informal Channels To Accelerate The Digitisation of RemittancesMo BenNo ratings yet

- FORM A2 Revised FormDocument6 pagesFORM A2 Revised Formcopy catNo ratings yet

- Urban Economy, and Urban Rural LinnkagesDocument26 pagesUrban Economy, and Urban Rural LinnkagesBimantara Von AikenNo ratings yet

- Current State of Nepali EconomyDocument39 pagesCurrent State of Nepali EconomyChandan SapkotaNo ratings yet

- Macroeconomic Situation in BangladeshDocument31 pagesMacroeconomic Situation in BangladeshShyam Bin JamilNo ratings yet

- Mexican Migration - Who Has The Right To MigrateDocument10 pagesMexican Migration - Who Has The Right To Migrateemilio27aNo ratings yet

- Remittance Performance of Islami Banks and Conventional Banks: A Comparative StudyDocument60 pagesRemittance Performance of Islami Banks and Conventional Banks: A Comparative Studynyeemalahad67% (3)

- Light Account Process GuideDocument26 pagesLight Account Process Guidemohamed mansourNo ratings yet

- Messari Report Asia Crypto LandscapeDocument99 pagesMessari Report Asia Crypto LandscapeDicky IrwansyahNo ratings yet

- Ethical Practice in Correspondent BankingDocument35 pagesEthical Practice in Correspondent Bankingmahesh ojhaNo ratings yet

- Caltex Vs Commission On Audit 1992Document1 pageCaltex Vs Commission On Audit 1992Praisah Marjorey PicotNo ratings yet