Download as pdf or txt

You might also like

- World Greatest Strategists - Ma HuatengDocument2 pagesWorld Greatest Strategists - Ma Huatengjojie dador100% (1)

- RCCP Title II Incorporation and Organization of Private CorporationsDocument31 pagesRCCP Title II Incorporation and Organization of Private CorporationsChet Buenfeliz TacliadNo ratings yet

- AgPart 925 - PartDocument270 pagesAgPart 925 - Partcezar delailaniNo ratings yet

- Chapter 3 With Full NotesDocument8 pagesChapter 3 With Full NotesmmaNo ratings yet

- PROPERTY REVIEWER - Usufruct To EasementsDocument4 pagesPROPERTY REVIEWER - Usufruct To EasementsChameNo ratings yet

- Land, Titles and Deeds Questions and AnswersDocument14 pagesLand, Titles and Deeds Questions and AnswersAron PanturillaNo ratings yet

- Negotiable Instruments Law Memory AidDocument5 pagesNegotiable Instruments Law Memory AidHappy SunshineNo ratings yet

- Institution of Heirs. It Will Not Result To IntestacyDocument9 pagesInstitution of Heirs. It Will Not Result To IntestacyCzara DyNo ratings yet

- Usufruct ReviewerDocument6 pagesUsufruct ReviewerAizaFerrerEbinaNo ratings yet

- Rule 102Document1 pageRule 102BrokenNo ratings yet

- Part 1 - Insights On The Discussion of Atty JavierDocument3 pagesPart 1 - Insights On The Discussion of Atty JavierKaren RefilNo ratings yet

- Part 3 Credit TransactionsDocument8 pagesPart 3 Credit TransactionsClint AbenojaNo ratings yet

- Articles 774-803 Wills & Succession (2019) Vice Dean Castillo-TaleonDocument14 pagesArticles 774-803 Wills & Succession (2019) Vice Dean Castillo-TaleonHi Law SchoolNo ratings yet

- Republic Act No. 11232-Revised Corporation CodeDocument44 pagesRepublic Act No. 11232-Revised Corporation CodeChiic-chiic SalamidaNo ratings yet

- Law On Sales, Agency, and Credit Transactions Atty. Jal A. Marquez Articles 1868-1932 Page 1 of 13Document13 pagesLaw On Sales, Agency, and Credit Transactions Atty. Jal A. Marquez Articles 1868-1932 Page 1 of 13Jal MarquezNo ratings yet

- Contract of Agency DefinitionDocument4 pagesContract of Agency DefinitionErcher TicianNo ratings yet

- Siena Realty vs. Gal-LangDocument2 pagesSiena Realty vs. Gal-LangZhai RaNo ratings yet

- 9236 - Pledge and Mortgage NotesDocument5 pages9236 - Pledge and Mortgage NotesmozoljayNo ratings yet

- Reviewer Corp Project (If Needed)Document5 pagesReviewer Corp Project (If Needed)A cNo ratings yet

- Law On Agency Chapter 2Document6 pagesLaw On Agency Chapter 2Edith DalidaNo ratings yet

- Acme Shoe, Rubber & Plastic Corp. v. CADocument2 pagesAcme Shoe, Rubber & Plastic Corp. v. CAAgee Romero-ValdesNo ratings yet

- Guaranty, Loan, DepositDocument15 pagesGuaranty, Loan, DepositKyla Valencia Ngo100% (1)

- Art 712 New Civil CodeDocument2 pagesArt 712 New Civil CodeRengie GaloNo ratings yet

- 11.strochecker V Ramirez, 44 Phil 933Document2 pages11.strochecker V Ramirez, 44 Phil 933H100% (1)

- Types of Credit Transactions As To Their ConsiderationDocument3 pagesTypes of Credit Transactions As To Their ConsiderationRafael Renz DayaoNo ratings yet

- Calubad vs. Ricarcen Dev CorpDocument27 pagesCalubad vs. Ricarcen Dev CorpLexa ClarkeNo ratings yet

- Property: (Paras, 2008)Document2 pagesProperty: (Paras, 2008)Romar TaroyNo ratings yet

- Green Valley Poultry v. SquibbDocument2 pagesGreen Valley Poultry v. SquibbMike Zaccahry MilcaNo ratings yet

- CIVIL LAW REVIEW 2017-2018': Villaroel V. EstradaDocument109 pagesCIVIL LAW REVIEW 2017-2018': Villaroel V. EstradaMadzGabiolaNo ratings yet

- RA 10707 (Probation Law) : Probation - Is A Disposition Under Which A Defendant, After RecognizanceDocument3 pagesRA 10707 (Probation Law) : Probation - Is A Disposition Under Which A Defendant, After RecognizanceRoldan LumawasNo ratings yet

- Pineda 2014: Partnership, Agency and TrustsDocument5 pagesPineda 2014: Partnership, Agency and TrustsPaul Christopher PinedaNo ratings yet

- 10 - Leny Villareal - 2 Legal Framework For GI Protection in TheDocument28 pages10 - Leny Villareal - 2 Legal Framework For GI Protection in TheBrunxAlabastroNo ratings yet

- Tony LA VinaDocument10 pagesTony LA VinaBenjamin HaysNo ratings yet

- Reviewer For Finals Taken From RABUYADocument9 pagesReviewer For Finals Taken From RABUYAbananayellowsharpieNo ratings yet

- Oblicon Crash CourseDocument20 pagesOblicon Crash Coursekero keropiNo ratings yet

- 47 O.G. 6241Document2 pages47 O.G. 6241Dan LocsinNo ratings yet

- Libarios vs. DabalosDocument11 pagesLibarios vs. DabalosAnthony De La CruzNo ratings yet

- Art. 447 Landowner-Bps (Lo) Owner of Materials (Om)Document4 pagesArt. 447 Landowner-Bps (Lo) Owner of Materials (Om)Francis PunoNo ratings yet

- Credit TransactionsDocument25 pagesCredit TransactionsAntonio Palpal-latocNo ratings yet

- Sanchez vs. BuenviajeDocument1 pageSanchez vs. BuenviajeVian O.No ratings yet

- Articles 1933-1961Document3 pagesArticles 1933-1961MarkNo ratings yet

- Chapter 2: Formalities of Agency: How Agency May Be ConstitutedDocument10 pagesChapter 2: Formalities of Agency: How Agency May Be ConstitutediptrinidadNo ratings yet

- NIL Bar QuestionsDocument3 pagesNIL Bar QuestionsbreeH20No ratings yet

- 7 Up To 561 POSSESSIONDocument18 pages7 Up To 561 POSSESSIONJor LonzagaNo ratings yet

- Nego Finals ReviewerDocument22 pagesNego Finals ReviewerAnna Katrina VistanNo ratings yet

- Corporation: Title ViiDocument13 pagesCorporation: Title ViiDarrel SapinosoNo ratings yet

- Civpro III e F Venue Pleadings 3 1Document64 pagesCivpro III e F Venue Pleadings 3 1TriciaNo ratings yet

- Law On Obligations and Contracts: Art. 1156 New Civil Code of PHDocument7 pagesLaw On Obligations and Contracts: Art. 1156 New Civil Code of PHJameeca MohiniNo ratings yet

- Corporatation Law Doctrines UPDATEDDocument32 pagesCorporatation Law Doctrines UPDATEDMar Jan GuyNo ratings yet

- PRE-MIDTERM REVIEWER in Credit TransactionsDocument23 pagesPRE-MIDTERM REVIEWER in Credit TransactionsSam SumaNo ratings yet

- Corporation and Basic Securities Law QA 2024 ExamDocument6 pagesCorporation and Basic Securities Law QA 2024 Examjobelleann.labuguenNo ratings yet

- Land Transfer Q and ADocument24 pagesLand Transfer Q and ARandy ZarateNo ratings yet

- Bolisay vs. Alcid, 85 SCRA 213Document7 pagesBolisay vs. Alcid, 85 SCRA 213ayam dinoNo ratings yet

- G.R. No. 129609. November 29, 2001. RODIL ENTERPRISES, INC., petitioner, vs. COURT OF APPEALS, CARMEN BONDOC, TERESITA BONDOC-ESTO, DIVISORIA FOOTWEAR and CHUA HUAY SOON, respondents. G.R. No. 135537. November 29, 2001. RODIL ENTERPRISES, INC., petitioner, vs. IDES O’RACCA BUILDING TENANTS ASSOCIATION, INC., respondent.Document8 pagesG.R. No. 129609. November 29, 2001. RODIL ENTERPRISES, INC., petitioner, vs. COURT OF APPEALS, CARMEN BONDOC, TERESITA BONDOC-ESTO, DIVISORIA FOOTWEAR and CHUA HUAY SOON, respondents. G.R. No. 135537. November 29, 2001. RODIL ENTERPRISES, INC., petitioner, vs. IDES O’RACCA BUILDING TENANTS ASSOCIATION, INC., respondent.Anonymous 6i1wUgzNo ratings yet

- Persons and Family Relations Reviewer 2 PDF FreeDocument20 pagesPersons and Family Relations Reviewer 2 PDF FreeLawrence Gerald Lozada BerayNo ratings yet

- Exception: Partnership by EstoppelDocument10 pagesException: Partnership by EstoppelJefNo ratings yet

- People vs. Concepcion GR L-19190Document2 pagesPeople vs. Concepcion GR L-19190Rizchelle Sampang-ManaogNo ratings yet

- Midterm Examination Crim Law 2 JD-1B 2020-2021 AYDocument9 pagesMidterm Examination Crim Law 2 JD-1B 2020-2021 AY师律No ratings yet

- Law On CorporationDocument12 pagesLaw On CorporationDaphne NgNo ratings yet

- Cavite Devt Bank V LimDocument2 pagesCavite Devt Bank V LimRocky CadizNo ratings yet

- Rural Bank of Borbon (Camarines Sur), Inc. v. CADocument2 pagesRural Bank of Borbon (Camarines Sur), Inc. v. CARuben100% (1)

- Dizon (E2024) Professor Avena: University of The Philippines College of Law Civil ProcedureDocument2 pagesDizon (E2024) Professor Avena: University of The Philippines College of Law Civil ProcedureManasseh DizonNo ratings yet

- Moldex Realty v. Sps. YuDocument3 pagesMoldex Realty v. Sps. YuManasseh DizonNo ratings yet

- Anama v. CitibankDocument2 pagesAnama v. CitibankManasseh DizonNo ratings yet

- Castillo v. Reyes - SalesDocument1 pageCastillo v. Reyes - SalesManasseh DizonNo ratings yet

- Del Prado v. Caballero - SalesDocument2 pagesDel Prado v. Caballero - SalesManasseh DizonNo ratings yet

- Abilla v. Gobonseng - SalesDocument2 pagesAbilla v. Gobonseng - SalesManasseh DizonNo ratings yet

- Paredes v. Espino - SalesDocument2 pagesParedes v. Espino - SalesManasseh DizonNo ratings yet

- Carceller v. CA - SalesDocument2 pagesCarceller v. CA - SalesManasseh DizonNo ratings yet

- Hernaez v. Hernaez - SalesDocument2 pagesHernaez v. Hernaez - SalesManasseh DizonNo ratings yet

- Tanglao v. Parungao - SalesDocument2 pagesTanglao v. Parungao - SalesManasseh DizonNo ratings yet

- Zaguirre v. CastilloDocument2 pagesZaguirre v. CastilloManasseh DizonNo ratings yet

- Creative Brief Template 36Document3 pagesCreative Brief Template 36Nashrah GullNo ratings yet

- Additional Exercises Transaction Analaysis Journalizing Posting and Unadjusted TDocument4 pagesAdditional Exercises Transaction Analaysis Journalizing Posting and Unadjusted TRenalyn Ps MewagNo ratings yet

- KidsTravel Produces Car Seats For Children From Newborn To 2 Years OldDocument2 pagesKidsTravel Produces Car Seats For Children From Newborn To 2 Years OldElliot Richard0% (1)

- Hutton AP Marcus AJ Tehranian H - 2009 - Opaque Financial Reports, R2, and Crash RiskDocument20 pagesHutton AP Marcus AJ Tehranian H - 2009 - Opaque Financial Reports, R2, and Crash RiskYara ZahrahNo ratings yet

- Tanla 14858 Notice 2022Document11 pagesTanla 14858 Notice 2022Ravi KNo ratings yet

- Sub Materi Teori Akuntansi BagiankuDocument5 pagesSub Materi Teori Akuntansi BagiankuM RizalNo ratings yet

- C I Business Law: Ourse NformationDocument6 pagesC I Business Law: Ourse NformationDawoodkhan safiNo ratings yet

- Account Details Addition / Modification / Deletion Request FormDocument1 pageAccount Details Addition / Modification / Deletion Request FormVasudev BhanajiNo ratings yet

- Asset Management at Central Banks and Monetary Authorities New Practices in Managing International Foreign Exchange Reserves Jacob BjorheimDocument43 pagesAsset Management at Central Banks and Monetary Authorities New Practices in Managing International Foreign Exchange Reserves Jacob Bjorheimyvette.gonzalez261100% (10)

- Xircls IntroductionDocument20 pagesXircls Introductiondarshikamishra.rbl.16No ratings yet

- EBA Public Hearing CP Draft RTS On FRTB IMADocument17 pagesEBA Public Hearing CP Draft RTS On FRTB IMADnyaneshwar PatilNo ratings yet

- Annual Report - PAISALO - 2020 PDFDocument113 pagesAnnual Report - PAISALO - 2020 PDFMeghani NehaNo ratings yet

- Creating An Adaptive HR Tech StrategyDocument20 pagesCreating An Adaptive HR Tech StrategyMudassar IqbalNo ratings yet

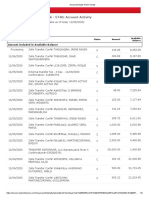

- Business Fundamentals CHK - 5740: Account Activity: All TransactionsDocument3 pagesBusiness Fundamentals CHK - 5740: Account Activity: All TransactionsAnnaly Carolina Bravo CastilloNo ratings yet

- Challenges For Sustainable Development Strategies in Oil and Gas IndustriesDocument13 pagesChallenges For Sustainable Development Strategies in Oil and Gas IndustriesAkshay Solanki100% (1)

- 2021 VMCL Wells Fargo Case 21 3Document4 pages2021 VMCL Wells Fargo Case 21 3Hy SomachariNo ratings yet

- Apos 2Document9 pagesApos 2yapklang2003No ratings yet

- Computers in Human Behavior: Mar Gómez, Carmen Lopez, Arturo Molina TDocument11 pagesComputers in Human Behavior: Mar Gómez, Carmen Lopez, Arturo Molina TTheFounders AgencyNo ratings yet

- Student Version: Project/Portfolio/Report Assessment TaskDocument6 pagesStudent Version: Project/Portfolio/Report Assessment TaskKevin SetiawanNo ratings yet

- 7p, S of Green Marketing FinalDocument11 pages7p, S of Green Marketing FinalSangeeta JainNo ratings yet

- Chapter 4 and 5Document19 pagesChapter 4 and 5nyasha praise mafungaNo ratings yet

- Summary of Ifrs 17Document7 pagesSummary of Ifrs 17Abegail Kaye BiadoNo ratings yet

- Joint and SolidaryDocument13 pagesJoint and SolidaryAmie Jane MirandaNo ratings yet

- Business CorrespondenceDocument2 pagesBusiness CorrespondenceEunice Kyla MapisaNo ratings yet

- Finals NegoDocument6 pagesFinals NegoHoward UntalanNo ratings yet

- Inox Concall FY2020 Q4 SummaryDocument2 pagesInox Concall FY2020 Q4 SummaryChristianStefanNo ratings yet

- Meseret FeteneDocument22 pagesMeseret FeteneGetaneh YenealemNo ratings yet

- Adm Module 7 SlidesDocument105 pagesAdm Module 7 SlidesZeib ShelbyNo ratings yet

- Bank Management: PGDM Iimc 2020 Praloy MajumderDocument53 pagesBank Management: PGDM Iimc 2020 Praloy MajumderLiontiniNo ratings yet