Module 5 - Options-Theory-for-Professional-Trading

Module 5 - Options-Theory-for-Professional-Trading

You might also like

- Options Trading: 7 Golden Beginners Strategies to Start Trading Options Like a PRO! Perfect Guide to Learn Basics & Tactics for Investing in Stocks, Futures, Binary & Bonds. Create Passive Income FastFrom EverandOptions Trading: 7 Golden Beginners Strategies to Start Trading Options Like a PRO! Perfect Guide to Learn Basics & Tactics for Investing in Stocks, Futures, Binary & Bonds. Create Passive Income FastRating: 4.5 out of 5 stars4.5/5 (2)

- TIA Bullet Proof 2022 - NotesDocument27 pagesTIA Bullet Proof 2022 - NotesRohan ShahNo ratings yet

- The Only Options Trading Book You'll Ever Need: Options Trading Workbook for Beginners to Hedge Your Stock Market Portfolio and Generate IncomeFrom EverandThe Only Options Trading Book You'll Ever Need: Options Trading Workbook for Beginners to Hedge Your Stock Market Portfolio and Generate IncomeNo ratings yet

- Options Trading: The Basics of Options Trading for Beginners and the Best Simplified Strategies to Make MoneyFrom EverandOptions Trading: The Basics of Options Trading for Beginners and the Best Simplified Strategies to Make MoneyRating: 4 out of 5 stars4/5 (1)

- Polyphonic HMI Case PresentationDocument48 pagesPolyphonic HMI Case PresentationUtpal Biyani100% (4)

- VNP SHEQ Consulting Proposal Audit Gambling BoardDocument3 pagesVNP SHEQ Consulting Proposal Audit Gambling BoardVictorNo ratings yet

- Call Option BasicsDocument24 pagesCall Option BasicsRafael AlacornNo ratings yet

- Module 5 Options Theory For Professional Trading MergedDocument385 pagesModule 5 Options Theory For Professional Trading MergedIndranil100% (1)

- Trading Lesson Module 5 ZerosdhaDocument239 pagesTrading Lesson Module 5 Zerosdhakiritimondal41No ratings yet

- Options Theory For Professional TradingDocument134 pagesOptions Theory For Professional TradingVibhats VibhorNo ratings yet

- Professional Option TheoryDocument111 pagesProfessional Option TheoryRaam Mk100% (1)

- Call Option Basics - Varsity by ZerodhaDocument6 pagesCall Option Basics - Varsity by ZerodhadanNo ratings yet

- Var 1Document16 pagesVar 1Mathew Rigesh JohnNo ratings yet

- 001 Real0902vkliDocument5 pages001 Real0902vkliAmrit SastryNo ratings yet

- Introduction To Derivatives (Part One)Document6 pagesIntroduction To Derivatives (Part One)sandeep_bansal_8No ratings yet

- Option Theory For Professional Trading - 1Document112 pagesOption Theory For Professional Trading - 1PremNo ratings yet

- Quick Lesson: We Have Been Talking About Derivatives Recently, So What Is Derivatives ?Document13 pagesQuick Lesson: We Have Been Talking About Derivatives Recently, So What Is Derivatives ?Rushabh ShahNo ratings yet

- Derivatives Notes1Document23 pagesDerivatives Notes1Sumeet JeswaniNo ratings yet

- Futers and OptionsDocument33 pagesFuters and Optionssivannarayana katragaddaNo ratings yet

- Option Derivative:: Project Assignment On Financial Derivatives & Market Submitted by Rohan Gholam Roll No - 222Document65 pagesOption Derivative:: Project Assignment On Financial Derivatives & Market Submitted by Rohan Gholam Roll No - 222Rohan GholamNo ratings yet

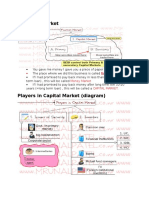

- Financial Market: Money Market Capital MarketDocument5 pagesFinancial Market: Money Market Capital MarketPreethi GopalanNo ratings yet

- Currency Option Strat PDFDocument11 pagesCurrency Option Strat PDFssinha122No ratings yet

- Lec 51Document15 pagesLec 51swastikNo ratings yet

- Accounts Test No. 4Document2 pagesAccounts Test No. 4AMIN BUHARI ABDUL KHADERNo ratings yet

- ProblemsDocument6 pagesProblemsPradeep BulleNo ratings yet

- Sub: Derivatives and Risk Management Case Study No.2Document2 pagesSub: Derivatives and Risk Management Case Study No.2ankit palNo ratings yet

- Bse DerivativesDocument73 pagesBse Derivativesvaibhavshah22No ratings yet

- A Study For Management of Risks Through DerivativesDocument27 pagesA Study For Management of Risks Through DerivativesAshish PoddarNo ratings yet

- Accounts Test No. 5Document2 pagesAccounts Test No. 5AMIN BUHARI ABDUL KHADERNo ratings yet

- FMI - Module IV - Derivatives - Futures & Forwards-1Document53 pagesFMI - Module IV - Derivatives - Futures & Forwards-1Bharathi Kyathi. gNo ratings yet

- Economy Mrunal NotesDocument611 pagesEconomy Mrunal NotesJishnu Asok85% (20)

- Indian Derivatives MarketDocument3 pagesIndian Derivatives MarketVivek Singh RanaNo ratings yet

- Conference Call Transcript 2021Document9 pagesConference Call Transcript 2021yashneet kaurNo ratings yet

- What Is SEBIDocument8 pagesWhat Is SEBIPreethi GopalanNo ratings yet

- Badla MechanismDocument27 pagesBadla Mechanismdivyapillai0201_No ratings yet

- RDocument3 pagesRAminul Haque RusselNo ratings yet

- Subject No 05M: Business LawDocument11 pagesSubject No 05M: Business LawAsmar Abdul RahimNo ratings yet

- Income On Demand Guide No 2Document9 pagesIncome On Demand Guide No 2ShamusORookeNo ratings yet

- What Is SEBI?: (Economy 4 Newbie) SEBI & Stock Exchange (The Beginning)Document10 pagesWhat Is SEBI?: (Economy 4 Newbie) SEBI & Stock Exchange (The Beginning)vishesh_gNo ratings yet

- Varun Nagar CaseDocument3 pagesVarun Nagar CaseVishal MishraNo ratings yet

- Derivative 333Document3 pagesDerivative 333muntaquirNo ratings yet

- Futures Trading: Example of A Futures ContractDocument4 pagesFutures Trading: Example of A Futures ContractShrinivas Vaddepalli VNo ratings yet

- Security Law Practical QuestionsDocument18 pagesSecurity Law Practical QuestionsIsha YadavNo ratings yet

- Commonly Used Jargons - Varsity by ZerodhaDocument4 pagesCommonly Used Jargons - Varsity by ZerodhajustchilltanujNo ratings yet

- 20-06-2024 (Chapter 3&4) HW ProblemsDocument2 pages20-06-2024 (Chapter 3&4) HW ProblemsMohanNo ratings yet

- Equity Shares 5Document4 pagesEquity Shares 5Sci UpscNo ratings yet

- Accounts Test No. 4Document5 pagesAccounts Test No. 4AMIN BUHARI ABDUL KHADERNo ratings yet

- Options Trading for Beginners: Investing Strategies You Need to Know to Generate Passive Income through Options TradingFrom EverandOptions Trading for Beginners: Investing Strategies You Need to Know to Generate Passive Income through Options TradingRating: 4 out of 5 stars4/5 (2)

- First Draft Article Buying CheaperhoseDocument3 pagesFirst Draft Article Buying CheaperhoseAtul KhekadeNo ratings yet

- Basics of DerivativesDocument15 pagesBasics of DerivativescutemoneyNo ratings yet

- NiftyBank Intraday Option Buying Single Successull StrategyDocument30 pagesNiftyBank Intraday Option Buying Single Successull Strategyajayvg75% (4)

- Art of Stock Investing Indian Stock MarketDocument10 pagesArt of Stock Investing Indian Stock MarketUmesh Kamath80% (5)

- Mrunal NotesDocument511 pagesMrunal NotesRakshit JoshiNo ratings yet

- Main Script New 1.1Document3 pagesMain Script New 1.1Sarah Lopez BelinoNo ratings yet

- (English) What Is Muhurat Trading - Stock To Checkout For Long Term - Anish Singh Thakur - Booming Bulls (DownSub - Com)Document12 pages(English) What Is Muhurat Trading - Stock To Checkout For Long Term - Anish Singh Thakur - Booming Bulls (DownSub - Com)Deepria GuptaNo ratings yet

- Options Trading: A Complete Crash Course to Become an Intelligent Investor – Make Money with Options and Start Creating Your Passive IncomeFrom EverandOptions Trading: A Complete Crash Course to Become an Intelligent Investor – Make Money with Options and Start Creating Your Passive IncomeNo ratings yet

- Real Estate Investing with Lease Options - Investing in Real Estate with No Money Down: Real Estate Investing, #2From EverandReal Estate Investing with Lease Options - Investing in Real Estate with No Money Down: Real Estate Investing, #2No ratings yet

- Options Trading: How to Start Investing Consciously with this Ultimate and Practical Guide. Learn How to Become a Smart Investor by Using Technical Analysis Before Purchasing Options (2022)From EverandOptions Trading: How to Start Investing Consciously with this Ultimate and Practical Guide. Learn How to Become a Smart Investor by Using Technical Analysis Before Purchasing Options (2022)No ratings yet

- Heredity and EvolutionDocument5 pagesHeredity and EvolutionRahul Ecka100% (3)

- Insulation Resistance (IR) Values - IndexDocument8 pagesInsulation Resistance (IR) Values - IndexAbdullah Al AsikNo ratings yet

- Mastering Sketching S11 BLAD Print2Document8 pagesMastering Sketching S11 BLAD Print2Interweave0% (1)

- 4.contour Flow Conditioner PDFDocument14 pages4.contour Flow Conditioner PDFFIRMANSYAHNo ratings yet

- Design and Fabrication of Unmanned Arial Vehicle For Multi-Mission TasksDocument10 pagesDesign and Fabrication of Unmanned Arial Vehicle For Multi-Mission TasksTJPRC PublicationsNo ratings yet

- Phyu Phyu Lwin CVDocument5 pagesPhyu Phyu Lwin CVphuy phyu100% (1)

- Ageing Aura and Vanitas in Art Greek LauDocument31 pagesAgeing Aura and Vanitas in Art Greek LautaraselbulbaNo ratings yet

- NORFIELD - T-Do2014-Imperialism and Finance PDFDocument227 pagesNORFIELD - T-Do2014-Imperialism and Finance PDFLaercio Monteiro Jr.No ratings yet

- CICSDB2 Guide NotesDocument4 pagesCICSDB2 Guide Notesshobhit10aprilNo ratings yet

- March of The Metro Gnome Lesson PlanDocument2 pagesMarch of The Metro Gnome Lesson Planapi-607297153No ratings yet

- Report On VSATDocument19 pagesReport On VSATchinu meshramNo ratings yet

- Summer Farm: By: Norman Maccaig Group: Camila Luna and Estrella LinDocument8 pagesSummer Farm: By: Norman Maccaig Group: Camila Luna and Estrella LinJamieDuncanNo ratings yet

- Bad For Democracy How The Presidency Undermines The Power of The PeopleDocument272 pagesBad For Democracy How The Presidency Undermines The Power of The PeoplePaulNo ratings yet

- Silvia Rey Resume OkDocument3 pagesSilvia Rey Resume Okapi-489656705No ratings yet

- Jody Howard Director, Social Responsibility Caterpillar, IncDocument17 pagesJody Howard Director, Social Responsibility Caterpillar, IncJanak ValakiNo ratings yet

- Slem Pc11ag Quarter1 Week8-SlmDocument22 pagesSlem Pc11ag Quarter1 Week8-SlmJuna Marie SuarezNo ratings yet

- INE MOR Program Cost Sheet 6.22.2022Document1 pageINE MOR Program Cost Sheet 6.22.2022Steven ScottNo ratings yet

- EZVIZ - Apps4u StoreDocument1 pageEZVIZ - Apps4u StorePak UliNo ratings yet

- Fausto Romitelli Six Keywords PDFDocument4 pagesFausto Romitelli Six Keywords PDFNachinsky von FriedenNo ratings yet

- Advertisement in E-CommerceDocument49 pagesAdvertisement in E-CommerceKenz VillanuevaNo ratings yet

- Part B Unit 3 DBMSDocument4 pagesPart B Unit 3 DBMSkaran.1888kNo ratings yet

- Hydraulics - Lecture 5 - DamsDocument22 pagesHydraulics - Lecture 5 - Damsmeh mehNo ratings yet

- CSO Olympiad Book For Class 1Document13 pagesCSO Olympiad Book For Class 1sanghamitrachakrabarti2007No ratings yet

- Cash Out With WhatsappDocument22 pagesCash Out With WhatsappIDRIS JAMIUNo ratings yet

- Physica Medica: Slobodan Devic, Nada Tomic, David LewisDocument16 pagesPhysica Medica: Slobodan Devic, Nada Tomic, David LewisFrederico GomesNo ratings yet

- Mels Subtype DescriptionsDocument11 pagesMels Subtype DescriptionsclaraNo ratings yet

- Spear 4 Module 3Document4 pagesSpear 4 Module 3Cherry Mae AlvaricoNo ratings yet

Download as pdf or txt

You might also like

- Options Trading: 7 Golden Beginners Strategies to Start Trading Options Like a PRO! Perfect Guide to Learn Basics & Tactics for Investing in Stocks, Futures, Binary & Bonds. Create Passive Income FastFrom EverandOptions Trading: 7 Golden Beginners Strategies to Start Trading Options Like a PRO! Perfect Guide to Learn Basics & Tactics for Investing in Stocks, Futures, Binary & Bonds. Create Passive Income FastRating: 4.5 out of 5 stars4.5/5 (2)

- TIA Bullet Proof 2022 - NotesDocument27 pagesTIA Bullet Proof 2022 - NotesRohan ShahNo ratings yet

- The Only Options Trading Book You'll Ever Need: Options Trading Workbook for Beginners to Hedge Your Stock Market Portfolio and Generate IncomeFrom EverandThe Only Options Trading Book You'll Ever Need: Options Trading Workbook for Beginners to Hedge Your Stock Market Portfolio and Generate IncomeNo ratings yet

- Options Trading: The Basics of Options Trading for Beginners and the Best Simplified Strategies to Make MoneyFrom EverandOptions Trading: The Basics of Options Trading for Beginners and the Best Simplified Strategies to Make MoneyRating: 4 out of 5 stars4/5 (1)

- Polyphonic HMI Case PresentationDocument48 pagesPolyphonic HMI Case PresentationUtpal Biyani100% (4)

- VNP SHEQ Consulting Proposal Audit Gambling BoardDocument3 pagesVNP SHEQ Consulting Proposal Audit Gambling BoardVictorNo ratings yet

- Call Option BasicsDocument24 pagesCall Option BasicsRafael AlacornNo ratings yet

- Module 5 Options Theory For Professional Trading MergedDocument385 pagesModule 5 Options Theory For Professional Trading MergedIndranil100% (1)

- Trading Lesson Module 5 ZerosdhaDocument239 pagesTrading Lesson Module 5 Zerosdhakiritimondal41No ratings yet

- Options Theory For Professional TradingDocument134 pagesOptions Theory For Professional TradingVibhats VibhorNo ratings yet

- Professional Option TheoryDocument111 pagesProfessional Option TheoryRaam Mk100% (1)

- Call Option Basics - Varsity by ZerodhaDocument6 pagesCall Option Basics - Varsity by ZerodhadanNo ratings yet

- Var 1Document16 pagesVar 1Mathew Rigesh JohnNo ratings yet

- 001 Real0902vkliDocument5 pages001 Real0902vkliAmrit SastryNo ratings yet

- Introduction To Derivatives (Part One)Document6 pagesIntroduction To Derivatives (Part One)sandeep_bansal_8No ratings yet

- Option Theory For Professional Trading - 1Document112 pagesOption Theory For Professional Trading - 1PremNo ratings yet

- Quick Lesson: We Have Been Talking About Derivatives Recently, So What Is Derivatives ?Document13 pagesQuick Lesson: We Have Been Talking About Derivatives Recently, So What Is Derivatives ?Rushabh ShahNo ratings yet

- Derivatives Notes1Document23 pagesDerivatives Notes1Sumeet JeswaniNo ratings yet

- Futers and OptionsDocument33 pagesFuters and Optionssivannarayana katragaddaNo ratings yet

- Option Derivative:: Project Assignment On Financial Derivatives & Market Submitted by Rohan Gholam Roll No - 222Document65 pagesOption Derivative:: Project Assignment On Financial Derivatives & Market Submitted by Rohan Gholam Roll No - 222Rohan GholamNo ratings yet

- Financial Market: Money Market Capital MarketDocument5 pagesFinancial Market: Money Market Capital MarketPreethi GopalanNo ratings yet

- Currency Option Strat PDFDocument11 pagesCurrency Option Strat PDFssinha122No ratings yet

- Lec 51Document15 pagesLec 51swastikNo ratings yet

- Accounts Test No. 4Document2 pagesAccounts Test No. 4AMIN BUHARI ABDUL KHADERNo ratings yet

- ProblemsDocument6 pagesProblemsPradeep BulleNo ratings yet

- Sub: Derivatives and Risk Management Case Study No.2Document2 pagesSub: Derivatives and Risk Management Case Study No.2ankit palNo ratings yet

- Bse DerivativesDocument73 pagesBse Derivativesvaibhavshah22No ratings yet

- A Study For Management of Risks Through DerivativesDocument27 pagesA Study For Management of Risks Through DerivativesAshish PoddarNo ratings yet

- Accounts Test No. 5Document2 pagesAccounts Test No. 5AMIN BUHARI ABDUL KHADERNo ratings yet

- FMI - Module IV - Derivatives - Futures & Forwards-1Document53 pagesFMI - Module IV - Derivatives - Futures & Forwards-1Bharathi Kyathi. gNo ratings yet

- Economy Mrunal NotesDocument611 pagesEconomy Mrunal NotesJishnu Asok85% (20)

- Indian Derivatives MarketDocument3 pagesIndian Derivatives MarketVivek Singh RanaNo ratings yet

- Conference Call Transcript 2021Document9 pagesConference Call Transcript 2021yashneet kaurNo ratings yet

- What Is SEBIDocument8 pagesWhat Is SEBIPreethi GopalanNo ratings yet

- Badla MechanismDocument27 pagesBadla Mechanismdivyapillai0201_No ratings yet

- RDocument3 pagesRAminul Haque RusselNo ratings yet

- Subject No 05M: Business LawDocument11 pagesSubject No 05M: Business LawAsmar Abdul RahimNo ratings yet

- Income On Demand Guide No 2Document9 pagesIncome On Demand Guide No 2ShamusORookeNo ratings yet

- What Is SEBI?: (Economy 4 Newbie) SEBI & Stock Exchange (The Beginning)Document10 pagesWhat Is SEBI?: (Economy 4 Newbie) SEBI & Stock Exchange (The Beginning)vishesh_gNo ratings yet

- Varun Nagar CaseDocument3 pagesVarun Nagar CaseVishal MishraNo ratings yet

- Derivative 333Document3 pagesDerivative 333muntaquirNo ratings yet

- Futures Trading: Example of A Futures ContractDocument4 pagesFutures Trading: Example of A Futures ContractShrinivas Vaddepalli VNo ratings yet

- Security Law Practical QuestionsDocument18 pagesSecurity Law Practical QuestionsIsha YadavNo ratings yet

- Commonly Used Jargons - Varsity by ZerodhaDocument4 pagesCommonly Used Jargons - Varsity by ZerodhajustchilltanujNo ratings yet

- 20-06-2024 (Chapter 3&4) HW ProblemsDocument2 pages20-06-2024 (Chapter 3&4) HW ProblemsMohanNo ratings yet

- Equity Shares 5Document4 pagesEquity Shares 5Sci UpscNo ratings yet

- Accounts Test No. 4Document5 pagesAccounts Test No. 4AMIN BUHARI ABDUL KHADERNo ratings yet

- Options Trading for Beginners: Investing Strategies You Need to Know to Generate Passive Income through Options TradingFrom EverandOptions Trading for Beginners: Investing Strategies You Need to Know to Generate Passive Income through Options TradingRating: 4 out of 5 stars4/5 (2)

- First Draft Article Buying CheaperhoseDocument3 pagesFirst Draft Article Buying CheaperhoseAtul KhekadeNo ratings yet

- Basics of DerivativesDocument15 pagesBasics of DerivativescutemoneyNo ratings yet

- NiftyBank Intraday Option Buying Single Successull StrategyDocument30 pagesNiftyBank Intraday Option Buying Single Successull Strategyajayvg75% (4)

- Art of Stock Investing Indian Stock MarketDocument10 pagesArt of Stock Investing Indian Stock MarketUmesh Kamath80% (5)

- Mrunal NotesDocument511 pagesMrunal NotesRakshit JoshiNo ratings yet

- Main Script New 1.1Document3 pagesMain Script New 1.1Sarah Lopez BelinoNo ratings yet

- (English) What Is Muhurat Trading - Stock To Checkout For Long Term - Anish Singh Thakur - Booming Bulls (DownSub - Com)Document12 pages(English) What Is Muhurat Trading - Stock To Checkout For Long Term - Anish Singh Thakur - Booming Bulls (DownSub - Com)Deepria GuptaNo ratings yet

- Options Trading: A Complete Crash Course to Become an Intelligent Investor – Make Money with Options and Start Creating Your Passive IncomeFrom EverandOptions Trading: A Complete Crash Course to Become an Intelligent Investor – Make Money with Options and Start Creating Your Passive IncomeNo ratings yet

- Real Estate Investing with Lease Options - Investing in Real Estate with No Money Down: Real Estate Investing, #2From EverandReal Estate Investing with Lease Options - Investing in Real Estate with No Money Down: Real Estate Investing, #2No ratings yet

- Options Trading: How to Start Investing Consciously with this Ultimate and Practical Guide. Learn How to Become a Smart Investor by Using Technical Analysis Before Purchasing Options (2022)From EverandOptions Trading: How to Start Investing Consciously with this Ultimate and Practical Guide. Learn How to Become a Smart Investor by Using Technical Analysis Before Purchasing Options (2022)No ratings yet

- Heredity and EvolutionDocument5 pagesHeredity and EvolutionRahul Ecka100% (3)

- Insulation Resistance (IR) Values - IndexDocument8 pagesInsulation Resistance (IR) Values - IndexAbdullah Al AsikNo ratings yet

- Mastering Sketching S11 BLAD Print2Document8 pagesMastering Sketching S11 BLAD Print2Interweave0% (1)

- 4.contour Flow Conditioner PDFDocument14 pages4.contour Flow Conditioner PDFFIRMANSYAHNo ratings yet

- Design and Fabrication of Unmanned Arial Vehicle For Multi-Mission TasksDocument10 pagesDesign and Fabrication of Unmanned Arial Vehicle For Multi-Mission TasksTJPRC PublicationsNo ratings yet

- Phyu Phyu Lwin CVDocument5 pagesPhyu Phyu Lwin CVphuy phyu100% (1)

- Ageing Aura and Vanitas in Art Greek LauDocument31 pagesAgeing Aura and Vanitas in Art Greek LautaraselbulbaNo ratings yet

- NORFIELD - T-Do2014-Imperialism and Finance PDFDocument227 pagesNORFIELD - T-Do2014-Imperialism and Finance PDFLaercio Monteiro Jr.No ratings yet

- CICSDB2 Guide NotesDocument4 pagesCICSDB2 Guide Notesshobhit10aprilNo ratings yet

- March of The Metro Gnome Lesson PlanDocument2 pagesMarch of The Metro Gnome Lesson Planapi-607297153No ratings yet

- Report On VSATDocument19 pagesReport On VSATchinu meshramNo ratings yet

- Summer Farm: By: Norman Maccaig Group: Camila Luna and Estrella LinDocument8 pagesSummer Farm: By: Norman Maccaig Group: Camila Luna and Estrella LinJamieDuncanNo ratings yet

- Bad For Democracy How The Presidency Undermines The Power of The PeopleDocument272 pagesBad For Democracy How The Presidency Undermines The Power of The PeoplePaulNo ratings yet

- Silvia Rey Resume OkDocument3 pagesSilvia Rey Resume Okapi-489656705No ratings yet

- Jody Howard Director, Social Responsibility Caterpillar, IncDocument17 pagesJody Howard Director, Social Responsibility Caterpillar, IncJanak ValakiNo ratings yet

- Slem Pc11ag Quarter1 Week8-SlmDocument22 pagesSlem Pc11ag Quarter1 Week8-SlmJuna Marie SuarezNo ratings yet

- INE MOR Program Cost Sheet 6.22.2022Document1 pageINE MOR Program Cost Sheet 6.22.2022Steven ScottNo ratings yet

- EZVIZ - Apps4u StoreDocument1 pageEZVIZ - Apps4u StorePak UliNo ratings yet

- Fausto Romitelli Six Keywords PDFDocument4 pagesFausto Romitelli Six Keywords PDFNachinsky von FriedenNo ratings yet

- Advertisement in E-CommerceDocument49 pagesAdvertisement in E-CommerceKenz VillanuevaNo ratings yet

- Part B Unit 3 DBMSDocument4 pagesPart B Unit 3 DBMSkaran.1888kNo ratings yet

- Hydraulics - Lecture 5 - DamsDocument22 pagesHydraulics - Lecture 5 - Damsmeh mehNo ratings yet

- CSO Olympiad Book For Class 1Document13 pagesCSO Olympiad Book For Class 1sanghamitrachakrabarti2007No ratings yet

- Cash Out With WhatsappDocument22 pagesCash Out With WhatsappIDRIS JAMIUNo ratings yet

- Physica Medica: Slobodan Devic, Nada Tomic, David LewisDocument16 pagesPhysica Medica: Slobodan Devic, Nada Tomic, David LewisFrederico GomesNo ratings yet

- Mels Subtype DescriptionsDocument11 pagesMels Subtype DescriptionsclaraNo ratings yet

- Spear 4 Module 3Document4 pagesSpear 4 Module 3Cherry Mae AlvaricoNo ratings yet