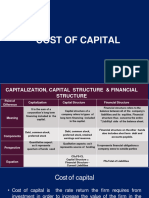

202003291623595167nimisha THE COST OF CAPITAL

202003291623595167nimisha THE COST OF CAPITAL

You might also like

- Bus HWDocument1 pageBus HWDaniel YaremenkoNo ratings yet

- John Loucks: Slides byDocument46 pagesJohn Loucks: Slides byRicky M. CalaraNo ratings yet

- CBOE 2012 Options Expiration CalendarDocument1 pageCBOE 2012 Options Expiration CalendarB_U_C_KNo ratings yet

- 40 Days To Success in Real Estate InvestingDocument266 pages40 Days To Success in Real Estate InvestingDustin Humphreys100% (1)

- Individual Assignment 2 - Issues and Ethics in FinanceDocument8 pagesIndividual Assignment 2 - Issues and Ethics in FinanceRahimah YusofNo ratings yet

- Financing Decision: The Cost of CapitalDocument23 pagesFinancing Decision: The Cost of CapitalRohit DhamijaNo ratings yet

- Cost of CapitalDocument36 pagesCost of CapitalNeelesh GaneshNo ratings yet

- Finance T3 2017 - w9Document45 pagesFinance T3 2017 - w9aabubNo ratings yet

- Chap 2 Cost of Capital MainDocument33 pagesChap 2 Cost of Capital Maintemesgen yohannesNo ratings yet

- Finman Session6bDocument71 pagesFinman Session6bLovely CabardoNo ratings yet

- Cost of CapitalDocument16 pagesCost of Capitalpadmar111No ratings yet

- SessionPlans - 47b3dcost of CapitalDocument26 pagesSessionPlans - 47b3dcost of Capitalmaahin khanNo ratings yet

- Cost of Capital and Capital StructureDocument40 pagesCost of Capital and Capital StructureJames NgonyaniNo ratings yet

- Cost of CapitalDocument31 pagesCost of Capitalharshit pandeyNo ratings yet

- Cost of CapitalDocument36 pagesCost of CapitalPrashant Kapoor0% (1)

- The Cost of CapitalDocument45 pagesThe Cost of CapitalMia KhalifaNo ratings yet

- FN1024 Chapter 7 PDF RevDocument34 pagesFN1024 Chapter 7 PDF Revduong duongNo ratings yet

- Advanced Financial Management-4Document28 pagesAdvanced Financial Management-4ቴዎድሮስNo ratings yet

- Capital CostDocument11 pagesCapital CostAdeline XuNo ratings yet

- CH 09 RevisedDocument36 pagesCH 09 RevisedNiharikaChouhanNo ratings yet

- Cost of CapitalDocument37 pagesCost of Capitalrajthakre81No ratings yet

- Cost of Capital OverviewDocument100 pagesCost of Capital Overview4279v5yhqkNo ratings yet

- CH.5 Cost of CapitalDocument28 pagesCH.5 Cost of Capitalprashantmis452No ratings yet

- L 5 Cost of CapitalDocument16 pagesL 5 Cost of CapitalMansi SainiNo ratings yet

- Financial Management1Document22 pagesFinancial Management1John DeepthiNo ratings yet

- Cost of CapitalDocument30 pagesCost of CapitalDellendo Farquharson100% (1)

- Cost of Capital: Kevin D. AsentistaDocument53 pagesCost of Capital: Kevin D. Asentistakristel rapadaNo ratings yet

- AC6101 Lecture 4 - Cost of Capital 1Document24 pagesAC6101 Lecture 4 - Cost of Capital 1Kelsey Gao0% (1)

- DCF Valuation: Merger Is A Special Type of Capital Budgeting DecisionDocument13 pagesDCF Valuation: Merger Is A Special Type of Capital Budgeting DecisionAkhilesh Kumar100% (1)

- DCF ValuationDocument74 pagesDCF ValuationCarrots TopNo ratings yet

- Cost of Capital and Capital Structure PlanningDocument32 pagesCost of Capital and Capital Structure PlanningAshiq NobitaNo ratings yet

- Cost of CapitalDocument39 pagesCost of Capitaladulmi325No ratings yet

- Lecture 3 - Calculating Cost of Capital PDFDocument26 pagesLecture 3 - Calculating Cost of Capital PDFNav MatharuNo ratings yet

- Cost of CapitalDocument34 pagesCost of CapitalSauravNo ratings yet

- Long Term Decision MakingDocument46 pagesLong Term Decision Makingchrystila0307No ratings yet

- MGT 302 - Financial ManagementDocument21 pagesMGT 302 - Financial ManagementNishani MudaligeNo ratings yet

- Chapter 3Document60 pagesChapter 3bouchahdamajd7No ratings yet

- ValuationDocument41 pagesValuationjpc jpcNo ratings yet

- Cost of Capital Session 1 and 2Document36 pagesCost of Capital Session 1 and 2Rishi CharanNo ratings yet

- Cost of CapitalDocument79 pagesCost of CapitalraniaNo ratings yet

- Cost of Capital-1Document40 pagesCost of Capital-1adulmi325No ratings yet

- Unit 6 SlidesDocument26 pagesUnit 6 SlidesKGOTHATSO VALENTINE MALATJINo ratings yet

- ECN 3422 - Lecture 2 - 2021.09.23Document28 pagesECN 3422 - Lecture 2 - 2021.09.23Cornelius MasikiniNo ratings yet

- Cost of Capital (English)Document11 pagesCost of Capital (English)Absalom OtienoNo ratings yet

- Amity School of Business: BBA Semister Four Financial Management-II Ashish Samarpit NoelDocument28 pagesAmity School of Business: BBA Semister Four Financial Management-II Ashish Samarpit NoelKaran MalikNo ratings yet

- Cost of Capital 1Document23 pagesCost of Capital 1shaahmookhanNo ratings yet

- Cost of CapitalDocument45 pagesCost of CapitalTaliya ShaikhNo ratings yet

- Cost of CapitalDocument26 pagesCost of CapitalShaza NaNo ratings yet

- AB1201 Financial Management Week 7: The Cost of Capital: Wacc W R (1-T) + W R + W RDocument18 pagesAB1201 Financial Management Week 7: The Cost of Capital: Wacc W R (1-T) + W R + W RElaine TohNo ratings yet

- Cost of CapitalDocument33 pagesCost of CapitalIamByker BwoeNo ratings yet

- Cost of CapitalDocument46 pagesCost of CapitalMazen SalahNo ratings yet

- Cost of Capital: What Number Goes in The Denominator?Document74 pagesCost of Capital: What Number Goes in The Denominator?Kenneth RobledoNo ratings yet

- Session 03 Corporate Finance WRDS.Document64 pagesSession 03 Corporate Finance WRDS.moadNo ratings yet

- Valuation MethodsDocument25 pagesValuation MethodsAd QasimNo ratings yet

- Roles of Finance - SlidesDocument77 pagesRoles of Finance - SlidesCrizziaNo ratings yet

- Shpenzimet Kapitale - Cost of CapitalDocument61 pagesShpenzimet Kapitale - Cost of CapitalBujar MorinaNo ratings yet

- Cost of Capital: Prof. Vanita PatelDocument44 pagesCost of Capital: Prof. Vanita PatelDurgesh ChandraNo ratings yet

- Topic 8 (1) Cost of CapitalDocument20 pagesTopic 8 (1) Cost of CapitalThe flying peguine CụtNo ratings yet

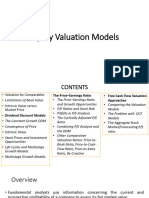

- Unit-3 4. Equity Valuation ModelsDocument46 pagesUnit-3 4. Equity Valuation ModelsJack SparrowNo ratings yet

- Unit 5 Capital Structure - TheoriesDocument39 pagesUnit 5 Capital Structure - Theoriesvishal kumarNo ratings yet

- Cost of Capital Updated (Corp. Finance)Document103 pagesCost of Capital Updated (Corp. Finance)Aditya SisodiaNo ratings yet

- Concept of Cost of Capital, Cost of Debt and Preferential StockDocument6 pagesConcept of Cost of Capital, Cost of Debt and Preferential StockBibek JoshiNo ratings yet

- Cost of CapitalDocument31 pagesCost of CapitalAnamNo ratings yet

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- PPC PDFDocument77 pagesPPC PDFAkshay sachanNo ratings yet

- Strategic Management (SM) : Saurav Banerjee 1Document11 pagesStrategic Management (SM) : Saurav Banerjee 1Akshay sachanNo ratings yet

- SM II-HANDOUT 06-Takeover and Defence TacticsDocument4 pagesSM II-HANDOUT 06-Takeover and Defence TacticsAkshay sachanNo ratings yet

- SM II-HANDOUT 09-Corporate EvolutionDocument3 pagesSM II-HANDOUT 09-Corporate EvolutionAkshay sachanNo ratings yet

- SM II-HANDOUT 08-Cross Border-M&ADocument8 pagesSM II-HANDOUT 08-Cross Border-M&AAkshay sachanNo ratings yet

- SM II-handout 05-Mckinsey 7s ModelDocument6 pagesSM II-handout 05-Mckinsey 7s ModelAkshay sachanNo ratings yet

- SM II-HANDOUT 04-Corporate Culture, Corporate Politics and Use of PowerDocument9 pagesSM II-HANDOUT 04-Corporate Culture, Corporate Politics and Use of PowerAkshay sachanNo ratings yet

- Regulators in Financial System - Rbi - Sebi - IrdaDocument17 pagesRegulators in Financial System - Rbi - Sebi - IrdaAkshay sachanNo ratings yet

- SM II-HANDOUT 02-Management of Strategic ChangeDocument4 pagesSM II-HANDOUT 02-Management of Strategic ChangeAkshay sachanNo ratings yet

- SM II-HANDOUT 01-Organisational LearningDocument4 pagesSM II-HANDOUT 01-Organisational LearningAkshay sachanNo ratings yet

- Strategic Management Ii - Unit 1Document49 pagesStrategic Management Ii - Unit 1Akshay sachanNo ratings yet

- SM II-HANDOUT 03-LeadershipDocument1 pageSM II-HANDOUT 03-LeadershipAkshay sachanNo ratings yet

- MCQ of Marketing of ServicesDocument10 pagesMCQ of Marketing of ServicesAkshay sachanNo ratings yet

- Tata Tea's Leveraged Buyout of TetleyDocument20 pagesTata Tea's Leveraged Buyout of TetleySahil Singla100% (1)

- Ta3473 Ind Final ReportDocument343 pagesTa3473 Ind Final ReportSiddharth JoshiNo ratings yet

- LT R Guidebook 053112Document99 pagesLT R Guidebook 053112MarketsWikiNo ratings yet

- Little Book That Beats The Market NOTESDocument5 pagesLittle Book That Beats The Market NOTESraj78kr0% (1)

- Financial Risk Management - WikipediaDocument4 pagesFinancial Risk Management - WikipediaPranay JaipuriaNo ratings yet

- FM Textbook Solutions Review Second Edition PDFDocument18 pagesFM Textbook Solutions Review Second Edition PDFlibredescargaNo ratings yet

- Intermediate Accounting 17Th Edition Kieso Solutions Manual Full Chapter PDFDocument43 pagesIntermediate Accounting 17Th Edition Kieso Solutions Manual Full Chapter PDFDebraWhitecxgn100% (13)

- Introduction To Investment Banking - Career Guides #002Document100 pagesIntroduction To Investment Banking - Career Guides #0026bxw4nrz2hNo ratings yet

- Ey Conduct Risk BarometerDocument24 pagesEy Conduct Risk BarometerKumar SambhavNo ratings yet

- Equity Research Report SlidesDocument18 pagesEquity Research Report Slidesanton88beNo ratings yet

- Elliott Wave PrincipleDocument41 pagesElliott Wave Principlecarlos mourao100% (1)

- Case 01 Buffett 2015 F1769TNXDocument10 pagesCase 01 Buffett 2015 F1769TNXVaney Iori0% (1)

- Currency Futures, Options and Swaps PDFDocument22 pagesCurrency Futures, Options and Swaps PDFHemanth Kumar86% (7)

- Financial Statement, Taxes and Cash Flow (With Answers)Document16 pagesFinancial Statement, Taxes and Cash Flow (With Answers)Haley James ScottNo ratings yet

- Mudarba & MusharkaDocument27 pagesMudarba & Musharkakamranp1100% (1)

- Management Accounting: Roll No. Total No. of Pages: 02 Total No. of Questions: 07 - 5)Document2 pagesManagement Accounting: Roll No. Total No. of Pages: 02 Total No. of Questions: 07 - 5)sumanNo ratings yet

- Global Financial Crisis OverviDocument12 pagesGlobal Financial Crisis Overvispinor01238No ratings yet

- Project Report On Reliance MoneyDocument70 pagesProject Report On Reliance Moneysubhash_92No ratings yet

- Essays Global Financial Crisis PDFDocument343 pagesEssays Global Financial Crisis PDFHeirene Cabusbusan100% (1)

- Unit Ii Assessment Accounting Standards 2Document20 pagesUnit Ii Assessment Accounting Standards 2Chin Figura0% (1)

- Solutions Manual Chapter Twenty-Three: Answers To Chapter 23 QuestionsDocument12 pagesSolutions Manual Chapter Twenty-Three: Answers To Chapter 23 QuestionsBiloni KadakiaNo ratings yet

- Answer No. 1Document5 pagesAnswer No. 1Anurag GuptaNo ratings yet

- Bhumikanya FPC - Dal Mil - SangliDocument17 pagesBhumikanya FPC - Dal Mil - SangliSamakoi freshNo ratings yet

- Edgar Peters TalksDocument5 pagesEdgar Peters TalksocalmaviliNo ratings yet

- Smart - 17 Sept. 2017Document51 pagesSmart - 17 Sept. 2017sanny2005No ratings yet

Download as pdf or txt

You might also like

- Bus HWDocument1 pageBus HWDaniel YaremenkoNo ratings yet

- John Loucks: Slides byDocument46 pagesJohn Loucks: Slides byRicky M. CalaraNo ratings yet

- CBOE 2012 Options Expiration CalendarDocument1 pageCBOE 2012 Options Expiration CalendarB_U_C_KNo ratings yet

- 40 Days To Success in Real Estate InvestingDocument266 pages40 Days To Success in Real Estate InvestingDustin Humphreys100% (1)

- Individual Assignment 2 - Issues and Ethics in FinanceDocument8 pagesIndividual Assignment 2 - Issues and Ethics in FinanceRahimah YusofNo ratings yet

- Financing Decision: The Cost of CapitalDocument23 pagesFinancing Decision: The Cost of CapitalRohit DhamijaNo ratings yet

- Cost of CapitalDocument36 pagesCost of CapitalNeelesh GaneshNo ratings yet

- Finance T3 2017 - w9Document45 pagesFinance T3 2017 - w9aabubNo ratings yet

- Chap 2 Cost of Capital MainDocument33 pagesChap 2 Cost of Capital Maintemesgen yohannesNo ratings yet

- Finman Session6bDocument71 pagesFinman Session6bLovely CabardoNo ratings yet

- Cost of CapitalDocument16 pagesCost of Capitalpadmar111No ratings yet

- SessionPlans - 47b3dcost of CapitalDocument26 pagesSessionPlans - 47b3dcost of Capitalmaahin khanNo ratings yet

- Cost of Capital and Capital StructureDocument40 pagesCost of Capital and Capital StructureJames NgonyaniNo ratings yet

- Cost of CapitalDocument31 pagesCost of Capitalharshit pandeyNo ratings yet

- Cost of CapitalDocument36 pagesCost of CapitalPrashant Kapoor0% (1)

- The Cost of CapitalDocument45 pagesThe Cost of CapitalMia KhalifaNo ratings yet

- FN1024 Chapter 7 PDF RevDocument34 pagesFN1024 Chapter 7 PDF Revduong duongNo ratings yet

- Advanced Financial Management-4Document28 pagesAdvanced Financial Management-4ቴዎድሮስNo ratings yet

- Capital CostDocument11 pagesCapital CostAdeline XuNo ratings yet

- CH 09 RevisedDocument36 pagesCH 09 RevisedNiharikaChouhanNo ratings yet

- Cost of CapitalDocument37 pagesCost of Capitalrajthakre81No ratings yet

- Cost of Capital OverviewDocument100 pagesCost of Capital Overview4279v5yhqkNo ratings yet

- CH.5 Cost of CapitalDocument28 pagesCH.5 Cost of Capitalprashantmis452No ratings yet

- L 5 Cost of CapitalDocument16 pagesL 5 Cost of CapitalMansi SainiNo ratings yet

- Financial Management1Document22 pagesFinancial Management1John DeepthiNo ratings yet

- Cost of CapitalDocument30 pagesCost of CapitalDellendo Farquharson100% (1)

- Cost of Capital: Kevin D. AsentistaDocument53 pagesCost of Capital: Kevin D. Asentistakristel rapadaNo ratings yet

- AC6101 Lecture 4 - Cost of Capital 1Document24 pagesAC6101 Lecture 4 - Cost of Capital 1Kelsey Gao0% (1)

- DCF Valuation: Merger Is A Special Type of Capital Budgeting DecisionDocument13 pagesDCF Valuation: Merger Is A Special Type of Capital Budgeting DecisionAkhilesh Kumar100% (1)

- DCF ValuationDocument74 pagesDCF ValuationCarrots TopNo ratings yet

- Cost of Capital and Capital Structure PlanningDocument32 pagesCost of Capital and Capital Structure PlanningAshiq NobitaNo ratings yet

- Cost of CapitalDocument39 pagesCost of Capitaladulmi325No ratings yet

- Lecture 3 - Calculating Cost of Capital PDFDocument26 pagesLecture 3 - Calculating Cost of Capital PDFNav MatharuNo ratings yet

- Cost of CapitalDocument34 pagesCost of CapitalSauravNo ratings yet

- Long Term Decision MakingDocument46 pagesLong Term Decision Makingchrystila0307No ratings yet

- MGT 302 - Financial ManagementDocument21 pagesMGT 302 - Financial ManagementNishani MudaligeNo ratings yet

- Chapter 3Document60 pagesChapter 3bouchahdamajd7No ratings yet

- ValuationDocument41 pagesValuationjpc jpcNo ratings yet

- Cost of Capital Session 1 and 2Document36 pagesCost of Capital Session 1 and 2Rishi CharanNo ratings yet

- Cost of CapitalDocument79 pagesCost of CapitalraniaNo ratings yet

- Cost of Capital-1Document40 pagesCost of Capital-1adulmi325No ratings yet

- Unit 6 SlidesDocument26 pagesUnit 6 SlidesKGOTHATSO VALENTINE MALATJINo ratings yet

- ECN 3422 - Lecture 2 - 2021.09.23Document28 pagesECN 3422 - Lecture 2 - 2021.09.23Cornelius MasikiniNo ratings yet

- Cost of Capital (English)Document11 pagesCost of Capital (English)Absalom OtienoNo ratings yet

- Amity School of Business: BBA Semister Four Financial Management-II Ashish Samarpit NoelDocument28 pagesAmity School of Business: BBA Semister Four Financial Management-II Ashish Samarpit NoelKaran MalikNo ratings yet

- Cost of Capital 1Document23 pagesCost of Capital 1shaahmookhanNo ratings yet

- Cost of CapitalDocument45 pagesCost of CapitalTaliya ShaikhNo ratings yet

- Cost of CapitalDocument26 pagesCost of CapitalShaza NaNo ratings yet

- AB1201 Financial Management Week 7: The Cost of Capital: Wacc W R (1-T) + W R + W RDocument18 pagesAB1201 Financial Management Week 7: The Cost of Capital: Wacc W R (1-T) + W R + W RElaine TohNo ratings yet

- Cost of CapitalDocument33 pagesCost of CapitalIamByker BwoeNo ratings yet

- Cost of CapitalDocument46 pagesCost of CapitalMazen SalahNo ratings yet

- Cost of Capital: What Number Goes in The Denominator?Document74 pagesCost of Capital: What Number Goes in The Denominator?Kenneth RobledoNo ratings yet

- Session 03 Corporate Finance WRDS.Document64 pagesSession 03 Corporate Finance WRDS.moadNo ratings yet

- Valuation MethodsDocument25 pagesValuation MethodsAd QasimNo ratings yet

- Roles of Finance - SlidesDocument77 pagesRoles of Finance - SlidesCrizziaNo ratings yet

- Shpenzimet Kapitale - Cost of CapitalDocument61 pagesShpenzimet Kapitale - Cost of CapitalBujar MorinaNo ratings yet

- Cost of Capital: Prof. Vanita PatelDocument44 pagesCost of Capital: Prof. Vanita PatelDurgesh ChandraNo ratings yet

- Topic 8 (1) Cost of CapitalDocument20 pagesTopic 8 (1) Cost of CapitalThe flying peguine CụtNo ratings yet

- Unit-3 4. Equity Valuation ModelsDocument46 pagesUnit-3 4. Equity Valuation ModelsJack SparrowNo ratings yet

- Unit 5 Capital Structure - TheoriesDocument39 pagesUnit 5 Capital Structure - Theoriesvishal kumarNo ratings yet

- Cost of Capital Updated (Corp. Finance)Document103 pagesCost of Capital Updated (Corp. Finance)Aditya SisodiaNo ratings yet

- Concept of Cost of Capital, Cost of Debt and Preferential StockDocument6 pagesConcept of Cost of Capital, Cost of Debt and Preferential StockBibek JoshiNo ratings yet

- Cost of CapitalDocument31 pagesCost of CapitalAnamNo ratings yet

- Applied Corporate Finance. What is a Company worth?From EverandApplied Corporate Finance. What is a Company worth?Rating: 3 out of 5 stars3/5 (2)

- PPC PDFDocument77 pagesPPC PDFAkshay sachanNo ratings yet

- Strategic Management (SM) : Saurav Banerjee 1Document11 pagesStrategic Management (SM) : Saurav Banerjee 1Akshay sachanNo ratings yet

- SM II-HANDOUT 06-Takeover and Defence TacticsDocument4 pagesSM II-HANDOUT 06-Takeover and Defence TacticsAkshay sachanNo ratings yet

- SM II-HANDOUT 09-Corporate EvolutionDocument3 pagesSM II-HANDOUT 09-Corporate EvolutionAkshay sachanNo ratings yet

- SM II-HANDOUT 08-Cross Border-M&ADocument8 pagesSM II-HANDOUT 08-Cross Border-M&AAkshay sachanNo ratings yet

- SM II-handout 05-Mckinsey 7s ModelDocument6 pagesSM II-handout 05-Mckinsey 7s ModelAkshay sachanNo ratings yet

- SM II-HANDOUT 04-Corporate Culture, Corporate Politics and Use of PowerDocument9 pagesSM II-HANDOUT 04-Corporate Culture, Corporate Politics and Use of PowerAkshay sachanNo ratings yet

- Regulators in Financial System - Rbi - Sebi - IrdaDocument17 pagesRegulators in Financial System - Rbi - Sebi - IrdaAkshay sachanNo ratings yet

- SM II-HANDOUT 02-Management of Strategic ChangeDocument4 pagesSM II-HANDOUT 02-Management of Strategic ChangeAkshay sachanNo ratings yet

- SM II-HANDOUT 01-Organisational LearningDocument4 pagesSM II-HANDOUT 01-Organisational LearningAkshay sachanNo ratings yet

- Strategic Management Ii - Unit 1Document49 pagesStrategic Management Ii - Unit 1Akshay sachanNo ratings yet

- SM II-HANDOUT 03-LeadershipDocument1 pageSM II-HANDOUT 03-LeadershipAkshay sachanNo ratings yet

- MCQ of Marketing of ServicesDocument10 pagesMCQ of Marketing of ServicesAkshay sachanNo ratings yet

- Tata Tea's Leveraged Buyout of TetleyDocument20 pagesTata Tea's Leveraged Buyout of TetleySahil Singla100% (1)

- Ta3473 Ind Final ReportDocument343 pagesTa3473 Ind Final ReportSiddharth JoshiNo ratings yet

- LT R Guidebook 053112Document99 pagesLT R Guidebook 053112MarketsWikiNo ratings yet

- Little Book That Beats The Market NOTESDocument5 pagesLittle Book That Beats The Market NOTESraj78kr0% (1)

- Financial Risk Management - WikipediaDocument4 pagesFinancial Risk Management - WikipediaPranay JaipuriaNo ratings yet

- FM Textbook Solutions Review Second Edition PDFDocument18 pagesFM Textbook Solutions Review Second Edition PDFlibredescargaNo ratings yet

- Intermediate Accounting 17Th Edition Kieso Solutions Manual Full Chapter PDFDocument43 pagesIntermediate Accounting 17Th Edition Kieso Solutions Manual Full Chapter PDFDebraWhitecxgn100% (13)

- Introduction To Investment Banking - Career Guides #002Document100 pagesIntroduction To Investment Banking - Career Guides #0026bxw4nrz2hNo ratings yet

- Ey Conduct Risk BarometerDocument24 pagesEy Conduct Risk BarometerKumar SambhavNo ratings yet

- Equity Research Report SlidesDocument18 pagesEquity Research Report Slidesanton88beNo ratings yet

- Elliott Wave PrincipleDocument41 pagesElliott Wave Principlecarlos mourao100% (1)

- Case 01 Buffett 2015 F1769TNXDocument10 pagesCase 01 Buffett 2015 F1769TNXVaney Iori0% (1)

- Currency Futures, Options and Swaps PDFDocument22 pagesCurrency Futures, Options and Swaps PDFHemanth Kumar86% (7)

- Financial Statement, Taxes and Cash Flow (With Answers)Document16 pagesFinancial Statement, Taxes and Cash Flow (With Answers)Haley James ScottNo ratings yet

- Mudarba & MusharkaDocument27 pagesMudarba & Musharkakamranp1100% (1)

- Management Accounting: Roll No. Total No. of Pages: 02 Total No. of Questions: 07 - 5)Document2 pagesManagement Accounting: Roll No. Total No. of Pages: 02 Total No. of Questions: 07 - 5)sumanNo ratings yet

- Global Financial Crisis OverviDocument12 pagesGlobal Financial Crisis Overvispinor01238No ratings yet

- Project Report On Reliance MoneyDocument70 pagesProject Report On Reliance Moneysubhash_92No ratings yet

- Essays Global Financial Crisis PDFDocument343 pagesEssays Global Financial Crisis PDFHeirene Cabusbusan100% (1)

- Unit Ii Assessment Accounting Standards 2Document20 pagesUnit Ii Assessment Accounting Standards 2Chin Figura0% (1)

- Solutions Manual Chapter Twenty-Three: Answers To Chapter 23 QuestionsDocument12 pagesSolutions Manual Chapter Twenty-Three: Answers To Chapter 23 QuestionsBiloni KadakiaNo ratings yet

- Answer No. 1Document5 pagesAnswer No. 1Anurag GuptaNo ratings yet

- Bhumikanya FPC - Dal Mil - SangliDocument17 pagesBhumikanya FPC - Dal Mil - SangliSamakoi freshNo ratings yet

- Edgar Peters TalksDocument5 pagesEdgar Peters TalksocalmaviliNo ratings yet

- Smart - 17 Sept. 2017Document51 pagesSmart - 17 Sept. 2017sanny2005No ratings yet