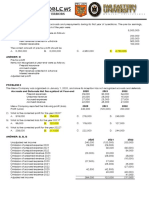

Auditing Problems

Auditing Problems

You might also like

- Auditing Problems Roque 2023-2024Document385 pagesAuditing Problems Roque 2023-2024Roisu De KuriNo ratings yet

- ReSA B46 AUD Final PB Exam Questions Answers Solutions 1Document16 pagesReSA B46 AUD Final PB Exam Questions Answers Solutions 1John Gabriel RafaelNo ratings yet

- PAS 1 Presentation of Financial Statements: Quiz 1: Multiple ChoiceDocument3 pagesPAS 1 Presentation of Financial Statements: Quiz 1: Multiple Choicetrixie mae88% (8)

- ADMS 3330 Final ExamDocument14 pagesADMS 3330 Final ExamPrincesNo ratings yet

- Quiz 2Document7 pagesQuiz 2Rodmae VersonNo ratings yet

- Case 3Document13 pagesCase 3Prezi Toli100% (1)

- Chapter 3 Audit of InventoriesDocument26 pagesChapter 3 Audit of InventoriesSteffany Roque100% (3)

- Audit of InvDocument19 pagesAudit of InvMae-shane SagayoNo ratings yet

- Audit of Allowance For Doubtful AccountsDocument4 pagesAudit of Allowance For Doubtful AccountsCJ alandyNo ratings yet

- 4 Fin571 Week 1 Study GuideDocument22 pages4 Fin571 Week 1 Study GuideGreg FowlerNo ratings yet

- Nature and Introduction of Investment DecisionsDocument7 pagesNature and Introduction of Investment Decisionsrethvi100% (2)

- Final Project On Cash Flow Analysis For Union Bank of IndiaDocument107 pagesFinal Project On Cash Flow Analysis For Union Bank of IndiaKarthik Sp79% (47)

- IAS 41 Application of Fair Value MeasurementDocument22 pagesIAS 41 Application of Fair Value MeasurementgigitoNo ratings yet

- Chapter 9 Cash To Accrual Basis, Single EntryDocument24 pagesChapter 9 Cash To Accrual Basis, Single EntrySteffany RoqueNo ratings yet

- Ix - Cash To Accrual Basis, Single Entry and Correction of Errors Problem No. 1Document29 pagesIx - Cash To Accrual Basis, Single Entry and Correction of Errors Problem No. 1Kezia GuevarraNo ratings yet

- Auditing Theory: CPA ReviewDocument11 pagesAuditing Theory: CPA ReviewAljur SalamedaNo ratings yet

- Test Bank Chapter 3 Cost Volume Profit ADocument4 pagesTest Bank Chapter 3 Cost Volume Profit AKarlo D. ReclaNo ratings yet

- Chapter 4 Audit of InvestmentsDocument27 pagesChapter 4 Audit of InvestmentsSteffany RoqueNo ratings yet

- Practice Set Audit - LiabilitiesDocument12 pagesPractice Set Audit - LiabilitiesKayla MirandaNo ratings yet

- Audit Fot Liability Problem #8Document2 pagesAudit Fot Liability Problem #8Ma Teresa B. CerezoNo ratings yet

- AP Preweek (B43)Document66 pagesAP Preweek (B43)Rodmae VersonNo ratings yet

- AT EscalaDocument18 pagesAT EscalaRaiNo ratings yet

- Audit of Bonds PayableDocument8 pagesAudit of Bonds PayableKayla MirandaNo ratings yet

- T R S A: HE Eview Chool of CcountancyDocument20 pagesT R S A: HE Eview Chool of CcountancyMae Danica CalunsagNo ratings yet

- Auditing Problem For Shareholder's EquityDocument14 pagesAuditing Problem For Shareholder's Equityblack hudieNo ratings yet

- CPAR B94 FAR Final PB Exam - Answers - SolutionsDocument8 pagesCPAR B94 FAR Final PB Exam - Answers - SolutionsJazehl ValdezNo ratings yet

- Auditing Problem From Audit of InvestmentDocument61 pagesAuditing Problem From Audit of InvestmentNicole Anne Santiago SibuloNo ratings yet

- UntitledDocument18 pagesUntitledjeralyn juditNo ratings yet

- PROBLEM 1 Audit of Shareholders EquityDocument6 pagesPROBLEM 1 Audit of Shareholders Equityaira nialaNo ratings yet

- Auditing Problems Usl PDFDocument226 pagesAuditing Problems Usl PDFmusic niNo ratings yet

- Audit of PPE - Homework - AnswersDocument15 pagesAudit of PPE - Homework - AnswersMarnelli CatalanNo ratings yet

- UntitledDocument9 pagesUntitledJanna Mari FriasNo ratings yet

- Intermediate Acctg 3 Finals With Answers PDFDocument6 pagesIntermediate Acctg 3 Finals With Answers PDFPrincesNo ratings yet

- Audit Liability 02 Chapter 7Document1 pageAudit Liability 02 Chapter 7Ma Teresa B. CerezoNo ratings yet

- Audit Fot Liability Problem #10Document2 pagesAudit Fot Liability Problem #10Ma Teresa B. CerezoNo ratings yet

- Seatworks 01 and 02 Audit of EquityDocument6 pagesSeatworks 01 and 02 Audit of EquityPola PolzNo ratings yet

- AP-100Q: Financing Cycle: A S ' E: Udit of Tockholders QuityDocument12 pagesAP-100Q: Financing Cycle: A S ' E: Udit of Tockholders QuityShiela RengelNo ratings yet

- (Resa2019) Preweek (AP)Document30 pages(Resa2019) Preweek (AP)Dawson Dela CruzNo ratings yet

- Chapter 1-4 Review QuestionsDocument24 pagesChapter 1-4 Review QuestionsSophia JunelleNo ratings yet

- Quiz For 3rd ExamDocument2 pagesQuiz For 3rd ExamSantiago BuladacoNo ratings yet

- Problem No. 1 - Audit of Property, Plant, and Equipment (Ppe)Document2 pagesProblem No. 1 - Audit of Property, Plant, and Equipment (Ppe)John LuNo ratings yet

- Auditing Problems Test Banks - LIABILITIES Part 2Document6 pagesAuditing Problems Test Banks - LIABILITIES Part 2Alliah Mae ArbastoNo ratings yet

- At - InvestmentDocument3 pagesAt - InvestmentTroisNo ratings yet

- Audit Theory For InvestmentDocument6 pagesAudit Theory For InvestmentCharlene Mina100% (1)

- Week 4 - Long-Term Construction Contracts (LTCC) : SolutionDocument4 pagesWeek 4 - Long-Term Construction Contracts (LTCC) : SolutionJanna Mari FriasNo ratings yet

- Audit ProblemsDocument47 pagesAudit ProblemsShane TabunggaoNo ratings yet

- Audit of Receivables: Cebu Cpar Center, IncDocument10 pagesAudit of Receivables: Cebu Cpar Center, IncNuarin JJ100% (1)

- Auditing Problem 4Document4 pagesAuditing Problem 4jhobsNo ratings yet

- Audit of Accounts Receivable and Related Accounts1Document5 pagesAudit of Accounts Receivable and Related Accounts1CJ alandyNo ratings yet

- QUIZ Correction of ErrorsDocument7 pagesQUIZ Correction of ErrorsJanelleNo ratings yet

- Auditing Problems Audit of Inventory: Problem 1Document6 pagesAuditing Problems Audit of Inventory: Problem 1Mark Anthony TibuleNo ratings yet

- Audit of Liabilities Exercise 1: SolutionDocument14 pagesAudit of Liabilities Exercise 1: SolutionCharis Marie UrgelNo ratings yet

- Cebu Cpar Center: Auditing Problems Audit of Inventories Problem No. 1Document10 pagesCebu Cpar Center: Auditing Problems Audit of Inventories Problem No. 1PaupauNo ratings yet

- Q1. ProblemsDocument9 pagesQ1. ProblemsAldrin ZolinaNo ratings yet

- 93-Final PB-AUD (SOL)Document3 pages93-Final PB-AUD (SOL)813 cafe0% (1)

- Corporate Liquidation Problem SolvingDocument21 pagesCorporate Liquidation Problem SolvingRujean Salar AltejarNo ratings yet

- 8901 Audit of Shareholders Equity Self TestDocument6 pages8901 Audit of Shareholders Equity Self TestYahlianah LeeNo ratings yet

- Auditing Theory: C. Both I and IIDocument8 pagesAuditing Theory: C. Both I and IIKIM RAGANo ratings yet

- ICARE - MAS - PreWeek - Batch 4Document18 pagesICARE - MAS - PreWeek - Batch 4john paulNo ratings yet

- Franchise QuizDocument3 pagesFranchise QuizDante Nas JocomNo ratings yet

- PRTC First Answer Key PDFDocument48 pagesPRTC First Answer Key PDFnanabaNo ratings yet

- 9420 - Government Accounting ManualDocument8 pages9420 - Government Accounting ManualShannen D. CalimagNo ratings yet

- Code of Ethics (Q&A)Document46 pagesCode of Ethics (Q&A)Rosario Garcia Catugas0% (1)

- Midterm Exam - Financial Accounting 3 With AnswersDocument11 pagesMidterm Exam - Financial Accounting 3 With Answersjanus lopezNo ratings yet

- IA3 - REVIEWER - Internediate 3Document38 pagesIA3 - REVIEWER - Internediate 3Mujahad QuirinoNo ratings yet

- FAR Test BankDocument17 pagesFAR Test BankMa. Efrelyn A. BagayNo ratings yet

- AT Code of EthicsDocument10 pagesAT Code of EthicsPrincesNo ratings yet

- The Odyssey Describes The Action and Aftermath of TheDocument4 pagesThe Odyssey Describes The Action and Aftermath of ThePrincesNo ratings yet

- AT 04 Practice - Regulation of The ProfessionDocument6 pagesAT 04 Practice - Regulation of The ProfessionPrincesNo ratings yet

- UntitledDocument10 pagesUntitledPrincesNo ratings yet

- Intermediate Acctg 3 Finals With Answers PDFDocument6 pagesIntermediate Acctg 3 Finals With Answers PDFPrincesNo ratings yet

- Auditing Problems: Ap - 01: Correction of ErrorsDocument15 pagesAuditing Problems: Ap - 01: Correction of ErrorsPrinces100% (2)

- Bp. 22 Quizzer With AnswersDocument2 pagesBp. 22 Quizzer With AnswersPrincesNo ratings yet

- 02 IndividualsDocument95 pages02 IndividualsPrincesNo ratings yet

- Strategic PositioningDocument21 pagesStrategic PositioningPrincesNo ratings yet

- Capital Budgeting Theories: Basic ConceptsDocument37 pagesCapital Budgeting Theories: Basic ConceptsPrincesNo ratings yet

- Additional Vat MSQ PDFDocument14 pagesAdditional Vat MSQ PDFPrincesNo ratings yet

- PDF 01 Introduction To Financial Management Keypdf DDDocument4 pagesPDF 01 Introduction To Financial Management Keypdf DDPrincesNo ratings yet

- Auditing Problem - Correl 2 Exercise 1: Name: Date: Professor: Section: ScoreDocument17 pagesAuditing Problem - Correl 2 Exercise 1: Name: Date: Professor: Section: ScorePrincesNo ratings yet

- World Literature: Colegio de Dagupan Arellano St. Dagupan CityDocument1 pageWorld Literature: Colegio de Dagupan Arellano St. Dagupan CityPrincesNo ratings yet

- 40 Financial Statements TheoryDocument9 pages40 Financial Statements TheoryPrincesNo ratings yet

- UniFAST - Press ReleaseDocument3 pagesUniFAST - Press ReleasePrincesNo ratings yet

- Net Present Value: Mod. 4.3 VCMDocument27 pagesNet Present Value: Mod. 4.3 VCMPrincesNo ratings yet

- 09 Bbfa1103 T5Document37 pages09 Bbfa1103 T5djaljdNo ratings yet

- Accounts AssignmentDocument7 pagesAccounts AssignmentAishwarya SundararajNo ratings yet

- Income From Capital GainsDocument18 pagesIncome From Capital GainsRhea Vishisht100% (2)

- Entrep-Review: Use The Following Information For The Next Two QuestionsDocument3 pagesEntrep-Review: Use The Following Information For The Next Two QuestionsNeil John Santos ParasNo ratings yet

- Fund Flow StatementDocument16 pagesFund Flow StatementRavi RajputNo ratings yet

- A Study On The Impact of Insolvency and Bankruptcy Code (2016) On The Bank's Profitability - Roll71Document38 pagesA Study On The Impact of Insolvency and Bankruptcy Code (2016) On The Bank's Profitability - Roll71Aakanksha AgarwalNo ratings yet

- FY06 FY07 Interest Income: Profit & Loss StatementDocument15 pagesFY06 FY07 Interest Income: Profit & Loss StatementAziz Khan LodhiNo ratings yet

- Trust DeedDocument4 pagesTrust DeedNeetu PandeyNo ratings yet

- CH 14Document6 pagesCH 14Aminul Haque RusselNo ratings yet

- Accommodation OperationDocument21 pagesAccommodation OperationPiyush AgarwalNo ratings yet

- National Aluminium Company LTD Agro LTD: Retail ResearchDocument10 pagesNational Aluminium Company LTD Agro LTD: Retail ResearchajaykashviNo ratings yet

- (A) Fixed AssetsDocument14 pages(A) Fixed AssetsPriya GoyalNo ratings yet

- Budget TheoryDocument8 pagesBudget TheoryShubhendu VermaNo ratings yet

- Pre and Post of Accounting 2Document14 pagesPre and Post of Accounting 2Nancy AtentarNo ratings yet

- Cpar-Chapter 13: Current Liabilities and ContingenciesDocument37 pagesCpar-Chapter 13: Current Liabilities and Contingenciesspur ious100% (1)

- 12 Eco Sample T1 2021Document15 pages12 Eco Sample T1 2021Aditya KumarNo ratings yet

- CH 09Document69 pagesCH 09Navindra Jaggernauth100% (1)

- Techno Module 1BDocument22 pagesTechno Module 1BJohn Paul MorilloNo ratings yet

- Cost of Machine QuestionDocument1 pageCost of Machine QuestionRaffayNo ratings yet

- Reliance ProjectDocument26 pagesReliance ProjectKothiya RaviNo ratings yet

- Project of Taxation LawDocument5 pagesProject of Taxation Lawzaiba rehmanNo ratings yet

- Lcci Level 4 Certificate in Financial Accounting ASE20101 Resource Booklet Nov 2019Document8 pagesLcci Level 4 Certificate in Financial Accounting ASE20101 Resource Booklet Nov 2019Musthari KhanNo ratings yet

- MA A-3 Ratio AnalysisDocument3 pagesMA A-3 Ratio AnalysisShilpa AroraNo ratings yet

- MR Lokesh Goddati Employee ID: 00146914 Unit: SBU1Document5 pagesMR Lokesh Goddati Employee ID: 00146914 Unit: SBU1satyakrishna electricalsNo ratings yet

- Term Test 1 (Sol.)Document5 pagesTerm Test 1 (Sol.)iamneonkingNo ratings yet

- Philippines Eric ZerrudoDocument16 pagesPhilippines Eric ZerrudoAdriel Denzel C. LimNo ratings yet

Download as pdf or txt

You might also like

- Auditing Problems Roque 2023-2024Document385 pagesAuditing Problems Roque 2023-2024Roisu De KuriNo ratings yet

- ReSA B46 AUD Final PB Exam Questions Answers Solutions 1Document16 pagesReSA B46 AUD Final PB Exam Questions Answers Solutions 1John Gabriel RafaelNo ratings yet

- PAS 1 Presentation of Financial Statements: Quiz 1: Multiple ChoiceDocument3 pagesPAS 1 Presentation of Financial Statements: Quiz 1: Multiple Choicetrixie mae88% (8)

- ADMS 3330 Final ExamDocument14 pagesADMS 3330 Final ExamPrincesNo ratings yet

- Quiz 2Document7 pagesQuiz 2Rodmae VersonNo ratings yet

- Case 3Document13 pagesCase 3Prezi Toli100% (1)

- Chapter 3 Audit of InventoriesDocument26 pagesChapter 3 Audit of InventoriesSteffany Roque100% (3)

- Audit of InvDocument19 pagesAudit of InvMae-shane SagayoNo ratings yet

- Audit of Allowance For Doubtful AccountsDocument4 pagesAudit of Allowance For Doubtful AccountsCJ alandyNo ratings yet

- 4 Fin571 Week 1 Study GuideDocument22 pages4 Fin571 Week 1 Study GuideGreg FowlerNo ratings yet

- Nature and Introduction of Investment DecisionsDocument7 pagesNature and Introduction of Investment Decisionsrethvi100% (2)

- Final Project On Cash Flow Analysis For Union Bank of IndiaDocument107 pagesFinal Project On Cash Flow Analysis For Union Bank of IndiaKarthik Sp79% (47)

- IAS 41 Application of Fair Value MeasurementDocument22 pagesIAS 41 Application of Fair Value MeasurementgigitoNo ratings yet

- Chapter 9 Cash To Accrual Basis, Single EntryDocument24 pagesChapter 9 Cash To Accrual Basis, Single EntrySteffany RoqueNo ratings yet

- Ix - Cash To Accrual Basis, Single Entry and Correction of Errors Problem No. 1Document29 pagesIx - Cash To Accrual Basis, Single Entry and Correction of Errors Problem No. 1Kezia GuevarraNo ratings yet

- Auditing Theory: CPA ReviewDocument11 pagesAuditing Theory: CPA ReviewAljur SalamedaNo ratings yet

- Test Bank Chapter 3 Cost Volume Profit ADocument4 pagesTest Bank Chapter 3 Cost Volume Profit AKarlo D. ReclaNo ratings yet

- Chapter 4 Audit of InvestmentsDocument27 pagesChapter 4 Audit of InvestmentsSteffany RoqueNo ratings yet

- Practice Set Audit - LiabilitiesDocument12 pagesPractice Set Audit - LiabilitiesKayla MirandaNo ratings yet

- Audit Fot Liability Problem #8Document2 pagesAudit Fot Liability Problem #8Ma Teresa B. CerezoNo ratings yet

- AP Preweek (B43)Document66 pagesAP Preweek (B43)Rodmae VersonNo ratings yet

- AT EscalaDocument18 pagesAT EscalaRaiNo ratings yet

- Audit of Bonds PayableDocument8 pagesAudit of Bonds PayableKayla MirandaNo ratings yet

- T R S A: HE Eview Chool of CcountancyDocument20 pagesT R S A: HE Eview Chool of CcountancyMae Danica CalunsagNo ratings yet

- Auditing Problem For Shareholder's EquityDocument14 pagesAuditing Problem For Shareholder's Equityblack hudieNo ratings yet

- CPAR B94 FAR Final PB Exam - Answers - SolutionsDocument8 pagesCPAR B94 FAR Final PB Exam - Answers - SolutionsJazehl ValdezNo ratings yet

- Auditing Problem From Audit of InvestmentDocument61 pagesAuditing Problem From Audit of InvestmentNicole Anne Santiago SibuloNo ratings yet

- UntitledDocument18 pagesUntitledjeralyn juditNo ratings yet

- PROBLEM 1 Audit of Shareholders EquityDocument6 pagesPROBLEM 1 Audit of Shareholders Equityaira nialaNo ratings yet

- Auditing Problems Usl PDFDocument226 pagesAuditing Problems Usl PDFmusic niNo ratings yet

- Audit of PPE - Homework - AnswersDocument15 pagesAudit of PPE - Homework - AnswersMarnelli CatalanNo ratings yet

- UntitledDocument9 pagesUntitledJanna Mari FriasNo ratings yet

- Intermediate Acctg 3 Finals With Answers PDFDocument6 pagesIntermediate Acctg 3 Finals With Answers PDFPrincesNo ratings yet

- Audit Liability 02 Chapter 7Document1 pageAudit Liability 02 Chapter 7Ma Teresa B. CerezoNo ratings yet

- Audit Fot Liability Problem #10Document2 pagesAudit Fot Liability Problem #10Ma Teresa B. CerezoNo ratings yet

- Seatworks 01 and 02 Audit of EquityDocument6 pagesSeatworks 01 and 02 Audit of EquityPola PolzNo ratings yet

- AP-100Q: Financing Cycle: A S ' E: Udit of Tockholders QuityDocument12 pagesAP-100Q: Financing Cycle: A S ' E: Udit of Tockholders QuityShiela RengelNo ratings yet

- (Resa2019) Preweek (AP)Document30 pages(Resa2019) Preweek (AP)Dawson Dela CruzNo ratings yet

- Chapter 1-4 Review QuestionsDocument24 pagesChapter 1-4 Review QuestionsSophia JunelleNo ratings yet

- Quiz For 3rd ExamDocument2 pagesQuiz For 3rd ExamSantiago BuladacoNo ratings yet

- Problem No. 1 - Audit of Property, Plant, and Equipment (Ppe)Document2 pagesProblem No. 1 - Audit of Property, Plant, and Equipment (Ppe)John LuNo ratings yet

- Auditing Problems Test Banks - LIABILITIES Part 2Document6 pagesAuditing Problems Test Banks - LIABILITIES Part 2Alliah Mae ArbastoNo ratings yet

- At - InvestmentDocument3 pagesAt - InvestmentTroisNo ratings yet

- Audit Theory For InvestmentDocument6 pagesAudit Theory For InvestmentCharlene Mina100% (1)

- Week 4 - Long-Term Construction Contracts (LTCC) : SolutionDocument4 pagesWeek 4 - Long-Term Construction Contracts (LTCC) : SolutionJanna Mari FriasNo ratings yet

- Audit ProblemsDocument47 pagesAudit ProblemsShane TabunggaoNo ratings yet

- Audit of Receivables: Cebu Cpar Center, IncDocument10 pagesAudit of Receivables: Cebu Cpar Center, IncNuarin JJ100% (1)

- Auditing Problem 4Document4 pagesAuditing Problem 4jhobsNo ratings yet

- Audit of Accounts Receivable and Related Accounts1Document5 pagesAudit of Accounts Receivable and Related Accounts1CJ alandyNo ratings yet

- QUIZ Correction of ErrorsDocument7 pagesQUIZ Correction of ErrorsJanelleNo ratings yet

- Auditing Problems Audit of Inventory: Problem 1Document6 pagesAuditing Problems Audit of Inventory: Problem 1Mark Anthony TibuleNo ratings yet

- Audit of Liabilities Exercise 1: SolutionDocument14 pagesAudit of Liabilities Exercise 1: SolutionCharis Marie UrgelNo ratings yet

- Cebu Cpar Center: Auditing Problems Audit of Inventories Problem No. 1Document10 pagesCebu Cpar Center: Auditing Problems Audit of Inventories Problem No. 1PaupauNo ratings yet

- Q1. ProblemsDocument9 pagesQ1. ProblemsAldrin ZolinaNo ratings yet

- 93-Final PB-AUD (SOL)Document3 pages93-Final PB-AUD (SOL)813 cafe0% (1)

- Corporate Liquidation Problem SolvingDocument21 pagesCorporate Liquidation Problem SolvingRujean Salar AltejarNo ratings yet

- 8901 Audit of Shareholders Equity Self TestDocument6 pages8901 Audit of Shareholders Equity Self TestYahlianah LeeNo ratings yet

- Auditing Theory: C. Both I and IIDocument8 pagesAuditing Theory: C. Both I and IIKIM RAGANo ratings yet

- ICARE - MAS - PreWeek - Batch 4Document18 pagesICARE - MAS - PreWeek - Batch 4john paulNo ratings yet

- Franchise QuizDocument3 pagesFranchise QuizDante Nas JocomNo ratings yet

- PRTC First Answer Key PDFDocument48 pagesPRTC First Answer Key PDFnanabaNo ratings yet

- 9420 - Government Accounting ManualDocument8 pages9420 - Government Accounting ManualShannen D. CalimagNo ratings yet

- Code of Ethics (Q&A)Document46 pagesCode of Ethics (Q&A)Rosario Garcia Catugas0% (1)

- Midterm Exam - Financial Accounting 3 With AnswersDocument11 pagesMidterm Exam - Financial Accounting 3 With Answersjanus lopezNo ratings yet

- IA3 - REVIEWER - Internediate 3Document38 pagesIA3 - REVIEWER - Internediate 3Mujahad QuirinoNo ratings yet

- FAR Test BankDocument17 pagesFAR Test BankMa. Efrelyn A. BagayNo ratings yet

- AT Code of EthicsDocument10 pagesAT Code of EthicsPrincesNo ratings yet

- The Odyssey Describes The Action and Aftermath of TheDocument4 pagesThe Odyssey Describes The Action and Aftermath of ThePrincesNo ratings yet

- AT 04 Practice - Regulation of The ProfessionDocument6 pagesAT 04 Practice - Regulation of The ProfessionPrincesNo ratings yet

- UntitledDocument10 pagesUntitledPrincesNo ratings yet

- Intermediate Acctg 3 Finals With Answers PDFDocument6 pagesIntermediate Acctg 3 Finals With Answers PDFPrincesNo ratings yet

- Auditing Problems: Ap - 01: Correction of ErrorsDocument15 pagesAuditing Problems: Ap - 01: Correction of ErrorsPrinces100% (2)

- Bp. 22 Quizzer With AnswersDocument2 pagesBp. 22 Quizzer With AnswersPrincesNo ratings yet

- 02 IndividualsDocument95 pages02 IndividualsPrincesNo ratings yet

- Strategic PositioningDocument21 pagesStrategic PositioningPrincesNo ratings yet

- Capital Budgeting Theories: Basic ConceptsDocument37 pagesCapital Budgeting Theories: Basic ConceptsPrincesNo ratings yet

- Additional Vat MSQ PDFDocument14 pagesAdditional Vat MSQ PDFPrincesNo ratings yet

- PDF 01 Introduction To Financial Management Keypdf DDDocument4 pagesPDF 01 Introduction To Financial Management Keypdf DDPrincesNo ratings yet

- Auditing Problem - Correl 2 Exercise 1: Name: Date: Professor: Section: ScoreDocument17 pagesAuditing Problem - Correl 2 Exercise 1: Name: Date: Professor: Section: ScorePrincesNo ratings yet

- World Literature: Colegio de Dagupan Arellano St. Dagupan CityDocument1 pageWorld Literature: Colegio de Dagupan Arellano St. Dagupan CityPrincesNo ratings yet

- 40 Financial Statements TheoryDocument9 pages40 Financial Statements TheoryPrincesNo ratings yet

- UniFAST - Press ReleaseDocument3 pagesUniFAST - Press ReleasePrincesNo ratings yet

- Net Present Value: Mod. 4.3 VCMDocument27 pagesNet Present Value: Mod. 4.3 VCMPrincesNo ratings yet

- 09 Bbfa1103 T5Document37 pages09 Bbfa1103 T5djaljdNo ratings yet

- Accounts AssignmentDocument7 pagesAccounts AssignmentAishwarya SundararajNo ratings yet

- Income From Capital GainsDocument18 pagesIncome From Capital GainsRhea Vishisht100% (2)

- Entrep-Review: Use The Following Information For The Next Two QuestionsDocument3 pagesEntrep-Review: Use The Following Information For The Next Two QuestionsNeil John Santos ParasNo ratings yet

- Fund Flow StatementDocument16 pagesFund Flow StatementRavi RajputNo ratings yet

- A Study On The Impact of Insolvency and Bankruptcy Code (2016) On The Bank's Profitability - Roll71Document38 pagesA Study On The Impact of Insolvency and Bankruptcy Code (2016) On The Bank's Profitability - Roll71Aakanksha AgarwalNo ratings yet

- FY06 FY07 Interest Income: Profit & Loss StatementDocument15 pagesFY06 FY07 Interest Income: Profit & Loss StatementAziz Khan LodhiNo ratings yet

- Trust DeedDocument4 pagesTrust DeedNeetu PandeyNo ratings yet

- CH 14Document6 pagesCH 14Aminul Haque RusselNo ratings yet

- Accommodation OperationDocument21 pagesAccommodation OperationPiyush AgarwalNo ratings yet

- National Aluminium Company LTD Agro LTD: Retail ResearchDocument10 pagesNational Aluminium Company LTD Agro LTD: Retail ResearchajaykashviNo ratings yet

- (A) Fixed AssetsDocument14 pages(A) Fixed AssetsPriya GoyalNo ratings yet

- Budget TheoryDocument8 pagesBudget TheoryShubhendu VermaNo ratings yet

- Pre and Post of Accounting 2Document14 pagesPre and Post of Accounting 2Nancy AtentarNo ratings yet

- Cpar-Chapter 13: Current Liabilities and ContingenciesDocument37 pagesCpar-Chapter 13: Current Liabilities and Contingenciesspur ious100% (1)

- 12 Eco Sample T1 2021Document15 pages12 Eco Sample T1 2021Aditya KumarNo ratings yet

- CH 09Document69 pagesCH 09Navindra Jaggernauth100% (1)

- Techno Module 1BDocument22 pagesTechno Module 1BJohn Paul MorilloNo ratings yet

- Cost of Machine QuestionDocument1 pageCost of Machine QuestionRaffayNo ratings yet

- Reliance ProjectDocument26 pagesReliance ProjectKothiya RaviNo ratings yet

- Project of Taxation LawDocument5 pagesProject of Taxation Lawzaiba rehmanNo ratings yet

- Lcci Level 4 Certificate in Financial Accounting ASE20101 Resource Booklet Nov 2019Document8 pagesLcci Level 4 Certificate in Financial Accounting ASE20101 Resource Booklet Nov 2019Musthari KhanNo ratings yet

- MA A-3 Ratio AnalysisDocument3 pagesMA A-3 Ratio AnalysisShilpa AroraNo ratings yet

- MR Lokesh Goddati Employee ID: 00146914 Unit: SBU1Document5 pagesMR Lokesh Goddati Employee ID: 00146914 Unit: SBU1satyakrishna electricalsNo ratings yet

- Term Test 1 (Sol.)Document5 pagesTerm Test 1 (Sol.)iamneonkingNo ratings yet

- Philippines Eric ZerrudoDocument16 pagesPhilippines Eric ZerrudoAdriel Denzel C. LimNo ratings yet