Corporate Acc 6.2.22

Corporate Acc 6.2.22

You might also like

- Corporate Finance A Focused Approach 6th Edition Ehrhardt Solutions Manual DownloadDocument38 pagesCorporate Finance A Focused Approach 6th Edition Ehrhardt Solutions Manual DownloadAndrea Howard100% (23)

- ADR Aribitrage Opportunities For DummiesDocument29 pagesADR Aribitrage Opportunities For DummiesEd McManus100% (1)

- FINAN204-21A - Tutorial 6 Week 7Document10 pagesFINAN204-21A - Tutorial 6 Week 7Danae YangNo ratings yet

- Unit 1 - QuestionsDocument4 pagesUnit 1 - QuestionsMohanNo ratings yet

- AFM ProblemsDocument4 pagesAFM ProblemskuselvNo ratings yet

- Accounts ProblemsDocument30 pagesAccounts ProblemsBalasaranyasiddhuNo ratings yet

- Absorption Questions 1Document4 pagesAbsorption Questions 1naazhim nasarNo ratings yet

- COM203 AmalgamationDocument10 pagesCOM203 AmalgamationLogeshNo ratings yet

- Module-2 Equity Valuation Numerical For StudentsDocument11 pagesModule-2 Equity Valuation Numerical For Studentsgaurav supadeNo ratings yet

- RTP Dec 18 QNDocument21 pagesRTP Dec 18 QNbinu100% (1)

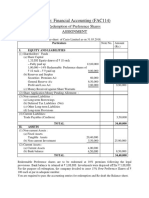

- Redemption of Preference ShareDocument6 pagesRedemption of Preference ShareAkash KamathNo ratings yet

- Problem Based On Ratio Analysis - Part - 2Document1 pageProblem Based On Ratio Analysis - Part - 2Mohd shariqNo ratings yet

- Unit II Analysis and Interpretation of Financial Statements Vertical Balance Sheet Balance Sheet As On 31/3/2022 Liabilities Rs. Assets RsDocument9 pagesUnit II Analysis and Interpretation of Financial Statements Vertical Balance Sheet Balance Sheet As On 31/3/2022 Liabilities Rs. Assets RsKirti RawatNo ratings yet

- Buy Back AssingmentDocument5 pagesBuy Back AssingmentDARK KING GamersNo ratings yet

- Ratio AnalysisDocument7 pagesRatio AnalysisDEEPA KUMARINo ratings yet

- CBCS - BCOM - HONS - Sem-5 - COMMERCE - DSE 5.2 A - CORPORATE ACCOUNTING-10992Document7 pagesCBCS - BCOM - HONS - Sem-5 - COMMERCE - DSE 5.2 A - CORPORATE ACCOUNTING-10992R3shav JaiswalNo ratings yet

- RATIO ANALYSIS Q 1 To 4Document5 pagesRATIO ANALYSIS Q 1 To 4gunjan0% (1)

- Abyas Amalgamation IPCC G 1 & 2Document34 pagesAbyas Amalgamation IPCC G 1 & 2Caramakr ManthaNo ratings yet

- 027 Practice Test 09 Accounting Test Solution Subjective Udesh RegularDocument6 pages027 Practice Test 09 Accounting Test Solution Subjective Udesh Regulardeathp006No ratings yet

- 3internal Reconstruction 230725 165705Document6 pages3internal Reconstruction 230725 165705Ruchita JanakiramNo ratings yet

- FRFSA INTERNAL Suggested QuestionsDocument3 pagesFRFSA INTERNAL Suggested QuestionsManik SaikatNo ratings yet

- Internal Reconstruction NotesDocument16 pagesInternal Reconstruction NotesAkash Mehta100% (1)

- Redemption of Preference Shares IllustrationsDocument6 pagesRedemption of Preference Shares IllustrationsManya GargNo ratings yet

- MBA AFM Probs On FS Analysis, Ratio Analysis and Com SizeDocument6 pagesMBA AFM Probs On FS Analysis, Ratio Analysis and Com SizeAngelsony AmmuNo ratings yet

- Adv Accounts - AmalgamationDocument31 pagesAdv Accounts - Amalgamationmd samser50% (2)

- Internal Question Bank MA 2022Document7 pagesInternal Question Bank MA 2022singhalsanchit321No ratings yet

- Cai Acc. Imp Questions (Part 1)Document100 pagesCai Acc. Imp Questions (Part 1)SheenaNo ratings yet

- Adobe Scan Jan 30, 2023Document6 pagesAdobe Scan Jan 30, 2023Karan RajakNo ratings yet

- AdvDocument19 pagesAdvashwin krishnaNo ratings yet

- Redemption of DebenturesDocument11 pagesRedemption of DebenturesUmang NagarNo ratings yet

- Company Acc PracticeDocument9 pagesCompany Acc PracticeRaffayNo ratings yet

- Unit - II Module IIIDocument7 pagesUnit - II Module IIIpltNo ratings yet

- B. Com - (H) 2020Document14 pagesB. Com - (H) 2020Gurleen Kaur KohliNo ratings yet

- Corporate Reporting Consolidation Review QuestionsDocument14 pagesCorporate Reporting Consolidation Review Questionssaidkhatib368No ratings yet

- Capital Reorganization QuestionsDocument20 pagesCapital Reorganization QuestionsProf. OBESENo ratings yet

- 5.ratio Analysis SumsDocument9 pages5.ratio Analysis Sumsvinay kumar nuwalNo ratings yet

- Semester II (Ugcf) 2412091201 ADocument9 pagesSemester II (Ugcf) 2412091201 Aindukush8No ratings yet

- 2019 Paper - DSE5.1A Sub - Corporate Accounting Time - 3 Hours Full Marks - 80Document4 pages2019 Paper - DSE5.1A Sub - Corporate Accounting Time - 3 Hours Full Marks - 80tanmoy sardarNo ratings yet

- June 2019 All Paper SuggestedDocument120 pagesJune 2019 All Paper SuggestedEdtech NepalNo ratings yet

- Unit III Amalgamation With Respect To A.S - 14 Purchase ConsiderationDocument17 pagesUnit III Amalgamation With Respect To A.S - 14 Purchase ConsiderationPaulomi LahaNo ratings yet

- Accounting Redemption of Debentures 1642416359Document19 pagesAccounting Redemption of Debentures 1642416359Shashank SikarwarNo ratings yet

- MA A-3 Ratio AnalysisDocument3 pagesMA A-3 Ratio AnalysisShilpa AroraNo ratings yet

- Advanced AccountingDocument12 pagesAdvanced AccountingmayuriNo ratings yet

- Question Papers: SEM. - (JULY 2023)Document8 pagesQuestion Papers: SEM. - (JULY 2023)arpitgupta20050No ratings yet

- Fa - 6 Amalgamation & LLPDocument10 pagesFa - 6 Amalgamation & LLPalokchowdhury111No ratings yet

- MergersDocument2 pagesMergersbriankuria21No ratings yet

- CA-Inter New Course: Advanced AccountingDocument121 pagesCA-Inter New Course: Advanced AccountingPankaj MeenaNo ratings yet

- Advanced Accounting 2BDocument4 pagesAdvanced Accounting 2BHarusiNo ratings yet

- Ratio Analysis 20 OctDocument7 pagesRatio Analysis 20 OctYogesh BandiNo ratings yet

- Problems On Internal ReconstructionDocument7 pagesProblems On Internal Reconstructionlokeshwarareddy1999No ratings yet

- Ratio Analysis ProblemsDocument4 pagesRatio Analysis ProblemsNavya SreeNo ratings yet

- Financial Analysis TestsDocument25 pagesFinancial Analysis Teststheodor_munteanuNo ratings yet

- The Commerce Villa: Time: 1.5 Hour Marks: 40 Topic: Ratio & Goodwill (AC - 07)Document15 pagesThe Commerce Villa: Time: 1.5 Hour Marks: 40 Topic: Ratio & Goodwill (AC - 07)Shreyas PremiumNo ratings yet

- Vertical Financial StatementsDocument3 pagesVertical Financial StatementsMANAN MEHTANo ratings yet

- Financial Accounting & AuditingDocument13 pagesFinancial Accounting & Auditingkashish mehtaNo ratings yet

- Adv Acc Q.P 2Document7 pagesAdv Acc Q.P 2Swetha ReddyNo ratings yet

- Chapter-4: Internal ReconstructionDocument9 pagesChapter-4: Internal ReconstructionAditi MaheshwariNo ratings yet

- Preference Shares AssignmentDocument4 pagesPreference Shares AssignmentDhairya ShahNo ratings yet

- Adv Acc - 3 CHDocument21 pagesAdv Acc - 3 CHhassan nassereddineNo ratings yet

- Adobe Scan 15 Oct 2020Document3 pagesAdobe Scan 15 Oct 2020gaurav kakkarNo ratings yet

- Far320 Capital Reduction ExercisesDocument7 pagesFar320 Capital Reduction ExercisesALIA MAISARA MD AKHIRNo ratings yet

- HintDocument6 pagesHintAppleNo ratings yet

- Reverse Merger - SEBI CircularDocument13 pagesReverse Merger - SEBI CircularhimanshusabooNo ratings yet

- 05 - Chapter 2Document27 pages05 - Chapter 2shan23586No ratings yet

- Profitability RatiosDocument6 pagesProfitability RatiosdanyalNo ratings yet

- CopperDocument4 pagesCopperChip choiNo ratings yet

- File: Chapter 06 - Variable Interest Entities, Intra-Entity Debt, Consolidated Cash Flows, and Other Issues Multiple ChoiceDocument53 pagesFile: Chapter 06 - Variable Interest Entities, Intra-Entity Debt, Consolidated Cash Flows, and Other Issues Multiple Choicejana ayoubNo ratings yet

- Practice MC Questions CH 15Document4 pagesPractice MC Questions CH 15business docNo ratings yet

- Niña Joy L. Arevalo BSMA II-B 3-1. Days Sales OutstandingDocument5 pagesNiña Joy L. Arevalo BSMA II-B 3-1. Days Sales OutstandingAnimeliciousNo ratings yet

- Chapter 9 Long Term Financing CalculationDocument13 pagesChapter 9 Long Term Financing Calculationsofea yusoffNo ratings yet

- Weekly Statistics: The Indonesia Stock Exchange Composite Stock Price Index and Equity Trading ValueDocument2 pagesWeekly Statistics: The Indonesia Stock Exchange Composite Stock Price Index and Equity Trading ValueIkhlas SadiminNo ratings yet

- ReportDocument36 pagesReportdouâe takfaouiNo ratings yet

- Mini Project WorkDocument6 pagesMini Project WorkVengatesh SNo ratings yet

- Ind Nifty FMCGDocument2 pagesInd Nifty FMCGJackNo ratings yet

- Chap 2 - Ratio AnalysisDocument24 pagesChap 2 - Ratio AnalysisZubairBalochJatoi100% (1)

- Advanced Corporate Finance (Econm 2032) : Piotr Korczak P.Korczak@bristol - Ac.ukDocument10 pagesAdvanced Corporate Finance (Econm 2032) : Piotr Korczak P.Korczak@bristol - Ac.ukDavissen MoorganNo ratings yet

- Hybrid and Derivative Securities: Learning GoalsDocument42 pagesHybrid and Derivative Securities: Learning GoalsRonna Mae Ferrer0% (1)

- Final Report - Real Estate - Div C - PGDM10Document20 pagesFinal Report - Real Estate - Div C - PGDM10DIVYANSHU SHEKHARNo ratings yet

- SC Syariahcompliant 2505-2023Document39 pagesSC Syariahcompliant 2505-2023Fatimah TarmiziNo ratings yet

- Pengurusan Kewangan (Kumpulan 6)Document42 pagesPengurusan Kewangan (Kumpulan 6)Wai ChongNo ratings yet

- Book Building ProcessDocument4 pagesBook Building Processvarsh08No ratings yet

- Anna Manokha 1500 Financing PDFDocument4 pagesAnna Manokha 1500 Financing PDFCrayZeeAlexNo ratings yet

- Mutual Funds: A Beginner's ModuleDocument2 pagesMutual Funds: A Beginner's Moduledavidd121No ratings yet

- Dekmar Trades CourseDocument15 pagesDekmar Trades CourseKyle MNo ratings yet

- Discussion Topic Is Entry N Exits in Trades and Portfolio HoldingsDocument3 pagesDiscussion Topic Is Entry N Exits in Trades and Portfolio HoldingsDASI SAI TEJANo ratings yet

- Buy Back Offer (Company Update)Document60 pagesBuy Back Offer (Company Update)Shyam SunderNo ratings yet

- SEC VAL AssignmentDocument2 pagesSEC VAL Assignmentharsh7mmNo ratings yet

- Financial Statement and Ratio Analysis SolutionsDocument24 pagesFinancial Statement and Ratio Analysis SolutionsnyxNo ratings yet

Download as pdf or txt

You might also like

- Corporate Finance A Focused Approach 6th Edition Ehrhardt Solutions Manual DownloadDocument38 pagesCorporate Finance A Focused Approach 6th Edition Ehrhardt Solutions Manual DownloadAndrea Howard100% (23)

- ADR Aribitrage Opportunities For DummiesDocument29 pagesADR Aribitrage Opportunities For DummiesEd McManus100% (1)

- FINAN204-21A - Tutorial 6 Week 7Document10 pagesFINAN204-21A - Tutorial 6 Week 7Danae YangNo ratings yet

- Unit 1 - QuestionsDocument4 pagesUnit 1 - QuestionsMohanNo ratings yet

- AFM ProblemsDocument4 pagesAFM ProblemskuselvNo ratings yet

- Accounts ProblemsDocument30 pagesAccounts ProblemsBalasaranyasiddhuNo ratings yet

- Absorption Questions 1Document4 pagesAbsorption Questions 1naazhim nasarNo ratings yet

- COM203 AmalgamationDocument10 pagesCOM203 AmalgamationLogeshNo ratings yet

- Module-2 Equity Valuation Numerical For StudentsDocument11 pagesModule-2 Equity Valuation Numerical For Studentsgaurav supadeNo ratings yet

- RTP Dec 18 QNDocument21 pagesRTP Dec 18 QNbinu100% (1)

- Redemption of Preference ShareDocument6 pagesRedemption of Preference ShareAkash KamathNo ratings yet

- Problem Based On Ratio Analysis - Part - 2Document1 pageProblem Based On Ratio Analysis - Part - 2Mohd shariqNo ratings yet

- Unit II Analysis and Interpretation of Financial Statements Vertical Balance Sheet Balance Sheet As On 31/3/2022 Liabilities Rs. Assets RsDocument9 pagesUnit II Analysis and Interpretation of Financial Statements Vertical Balance Sheet Balance Sheet As On 31/3/2022 Liabilities Rs. Assets RsKirti RawatNo ratings yet

- Buy Back AssingmentDocument5 pagesBuy Back AssingmentDARK KING GamersNo ratings yet

- Ratio AnalysisDocument7 pagesRatio AnalysisDEEPA KUMARINo ratings yet

- CBCS - BCOM - HONS - Sem-5 - COMMERCE - DSE 5.2 A - CORPORATE ACCOUNTING-10992Document7 pagesCBCS - BCOM - HONS - Sem-5 - COMMERCE - DSE 5.2 A - CORPORATE ACCOUNTING-10992R3shav JaiswalNo ratings yet

- RATIO ANALYSIS Q 1 To 4Document5 pagesRATIO ANALYSIS Q 1 To 4gunjan0% (1)

- Abyas Amalgamation IPCC G 1 & 2Document34 pagesAbyas Amalgamation IPCC G 1 & 2Caramakr ManthaNo ratings yet

- 027 Practice Test 09 Accounting Test Solution Subjective Udesh RegularDocument6 pages027 Practice Test 09 Accounting Test Solution Subjective Udesh Regulardeathp006No ratings yet

- 3internal Reconstruction 230725 165705Document6 pages3internal Reconstruction 230725 165705Ruchita JanakiramNo ratings yet

- FRFSA INTERNAL Suggested QuestionsDocument3 pagesFRFSA INTERNAL Suggested QuestionsManik SaikatNo ratings yet

- Internal Reconstruction NotesDocument16 pagesInternal Reconstruction NotesAkash Mehta100% (1)

- Redemption of Preference Shares IllustrationsDocument6 pagesRedemption of Preference Shares IllustrationsManya GargNo ratings yet

- MBA AFM Probs On FS Analysis, Ratio Analysis and Com SizeDocument6 pagesMBA AFM Probs On FS Analysis, Ratio Analysis and Com SizeAngelsony AmmuNo ratings yet

- Adv Accounts - AmalgamationDocument31 pagesAdv Accounts - Amalgamationmd samser50% (2)

- Internal Question Bank MA 2022Document7 pagesInternal Question Bank MA 2022singhalsanchit321No ratings yet

- Cai Acc. Imp Questions (Part 1)Document100 pagesCai Acc. Imp Questions (Part 1)SheenaNo ratings yet

- Adobe Scan Jan 30, 2023Document6 pagesAdobe Scan Jan 30, 2023Karan RajakNo ratings yet

- AdvDocument19 pagesAdvashwin krishnaNo ratings yet

- Redemption of DebenturesDocument11 pagesRedemption of DebenturesUmang NagarNo ratings yet

- Company Acc PracticeDocument9 pagesCompany Acc PracticeRaffayNo ratings yet

- Unit - II Module IIIDocument7 pagesUnit - II Module IIIpltNo ratings yet

- B. Com - (H) 2020Document14 pagesB. Com - (H) 2020Gurleen Kaur KohliNo ratings yet

- Corporate Reporting Consolidation Review QuestionsDocument14 pagesCorporate Reporting Consolidation Review Questionssaidkhatib368No ratings yet

- Capital Reorganization QuestionsDocument20 pagesCapital Reorganization QuestionsProf. OBESENo ratings yet

- 5.ratio Analysis SumsDocument9 pages5.ratio Analysis Sumsvinay kumar nuwalNo ratings yet

- Semester II (Ugcf) 2412091201 ADocument9 pagesSemester II (Ugcf) 2412091201 Aindukush8No ratings yet

- 2019 Paper - DSE5.1A Sub - Corporate Accounting Time - 3 Hours Full Marks - 80Document4 pages2019 Paper - DSE5.1A Sub - Corporate Accounting Time - 3 Hours Full Marks - 80tanmoy sardarNo ratings yet

- June 2019 All Paper SuggestedDocument120 pagesJune 2019 All Paper SuggestedEdtech NepalNo ratings yet

- Unit III Amalgamation With Respect To A.S - 14 Purchase ConsiderationDocument17 pagesUnit III Amalgamation With Respect To A.S - 14 Purchase ConsiderationPaulomi LahaNo ratings yet

- Accounting Redemption of Debentures 1642416359Document19 pagesAccounting Redemption of Debentures 1642416359Shashank SikarwarNo ratings yet

- MA A-3 Ratio AnalysisDocument3 pagesMA A-3 Ratio AnalysisShilpa AroraNo ratings yet

- Advanced AccountingDocument12 pagesAdvanced AccountingmayuriNo ratings yet

- Question Papers: SEM. - (JULY 2023)Document8 pagesQuestion Papers: SEM. - (JULY 2023)arpitgupta20050No ratings yet

- Fa - 6 Amalgamation & LLPDocument10 pagesFa - 6 Amalgamation & LLPalokchowdhury111No ratings yet

- MergersDocument2 pagesMergersbriankuria21No ratings yet

- CA-Inter New Course: Advanced AccountingDocument121 pagesCA-Inter New Course: Advanced AccountingPankaj MeenaNo ratings yet

- Advanced Accounting 2BDocument4 pagesAdvanced Accounting 2BHarusiNo ratings yet

- Ratio Analysis 20 OctDocument7 pagesRatio Analysis 20 OctYogesh BandiNo ratings yet

- Problems On Internal ReconstructionDocument7 pagesProblems On Internal Reconstructionlokeshwarareddy1999No ratings yet

- Ratio Analysis ProblemsDocument4 pagesRatio Analysis ProblemsNavya SreeNo ratings yet

- Financial Analysis TestsDocument25 pagesFinancial Analysis Teststheodor_munteanuNo ratings yet

- The Commerce Villa: Time: 1.5 Hour Marks: 40 Topic: Ratio & Goodwill (AC - 07)Document15 pagesThe Commerce Villa: Time: 1.5 Hour Marks: 40 Topic: Ratio & Goodwill (AC - 07)Shreyas PremiumNo ratings yet

- Vertical Financial StatementsDocument3 pagesVertical Financial StatementsMANAN MEHTANo ratings yet

- Financial Accounting & AuditingDocument13 pagesFinancial Accounting & Auditingkashish mehtaNo ratings yet

- Adv Acc Q.P 2Document7 pagesAdv Acc Q.P 2Swetha ReddyNo ratings yet

- Chapter-4: Internal ReconstructionDocument9 pagesChapter-4: Internal ReconstructionAditi MaheshwariNo ratings yet

- Preference Shares AssignmentDocument4 pagesPreference Shares AssignmentDhairya ShahNo ratings yet

- Adv Acc - 3 CHDocument21 pagesAdv Acc - 3 CHhassan nassereddineNo ratings yet

- Adobe Scan 15 Oct 2020Document3 pagesAdobe Scan 15 Oct 2020gaurav kakkarNo ratings yet

- Far320 Capital Reduction ExercisesDocument7 pagesFar320 Capital Reduction ExercisesALIA MAISARA MD AKHIRNo ratings yet

- HintDocument6 pagesHintAppleNo ratings yet

- Reverse Merger - SEBI CircularDocument13 pagesReverse Merger - SEBI CircularhimanshusabooNo ratings yet

- 05 - Chapter 2Document27 pages05 - Chapter 2shan23586No ratings yet

- Profitability RatiosDocument6 pagesProfitability RatiosdanyalNo ratings yet

- CopperDocument4 pagesCopperChip choiNo ratings yet

- File: Chapter 06 - Variable Interest Entities, Intra-Entity Debt, Consolidated Cash Flows, and Other Issues Multiple ChoiceDocument53 pagesFile: Chapter 06 - Variable Interest Entities, Intra-Entity Debt, Consolidated Cash Flows, and Other Issues Multiple Choicejana ayoubNo ratings yet

- Practice MC Questions CH 15Document4 pagesPractice MC Questions CH 15business docNo ratings yet

- Niña Joy L. Arevalo BSMA II-B 3-1. Days Sales OutstandingDocument5 pagesNiña Joy L. Arevalo BSMA II-B 3-1. Days Sales OutstandingAnimeliciousNo ratings yet

- Chapter 9 Long Term Financing CalculationDocument13 pagesChapter 9 Long Term Financing Calculationsofea yusoffNo ratings yet

- Weekly Statistics: The Indonesia Stock Exchange Composite Stock Price Index and Equity Trading ValueDocument2 pagesWeekly Statistics: The Indonesia Stock Exchange Composite Stock Price Index and Equity Trading ValueIkhlas SadiminNo ratings yet

- ReportDocument36 pagesReportdouâe takfaouiNo ratings yet

- Mini Project WorkDocument6 pagesMini Project WorkVengatesh SNo ratings yet

- Ind Nifty FMCGDocument2 pagesInd Nifty FMCGJackNo ratings yet

- Chap 2 - Ratio AnalysisDocument24 pagesChap 2 - Ratio AnalysisZubairBalochJatoi100% (1)

- Advanced Corporate Finance (Econm 2032) : Piotr Korczak P.Korczak@bristol - Ac.ukDocument10 pagesAdvanced Corporate Finance (Econm 2032) : Piotr Korczak P.Korczak@bristol - Ac.ukDavissen MoorganNo ratings yet

- Hybrid and Derivative Securities: Learning GoalsDocument42 pagesHybrid and Derivative Securities: Learning GoalsRonna Mae Ferrer0% (1)

- Final Report - Real Estate - Div C - PGDM10Document20 pagesFinal Report - Real Estate - Div C - PGDM10DIVYANSHU SHEKHARNo ratings yet

- SC Syariahcompliant 2505-2023Document39 pagesSC Syariahcompliant 2505-2023Fatimah TarmiziNo ratings yet

- Pengurusan Kewangan (Kumpulan 6)Document42 pagesPengurusan Kewangan (Kumpulan 6)Wai ChongNo ratings yet

- Book Building ProcessDocument4 pagesBook Building Processvarsh08No ratings yet

- Anna Manokha 1500 Financing PDFDocument4 pagesAnna Manokha 1500 Financing PDFCrayZeeAlexNo ratings yet

- Mutual Funds: A Beginner's ModuleDocument2 pagesMutual Funds: A Beginner's Moduledavidd121No ratings yet

- Dekmar Trades CourseDocument15 pagesDekmar Trades CourseKyle MNo ratings yet

- Discussion Topic Is Entry N Exits in Trades and Portfolio HoldingsDocument3 pagesDiscussion Topic Is Entry N Exits in Trades and Portfolio HoldingsDASI SAI TEJANo ratings yet

- Buy Back Offer (Company Update)Document60 pagesBuy Back Offer (Company Update)Shyam SunderNo ratings yet

- SEC VAL AssignmentDocument2 pagesSEC VAL Assignmentharsh7mmNo ratings yet

- Financial Statement and Ratio Analysis SolutionsDocument24 pagesFinancial Statement and Ratio Analysis SolutionsnyxNo ratings yet