Download as pdf or txt

You might also like

- OceanLink Partners Q1 2019 LetterDocument14 pagesOceanLink Partners Q1 2019 LetterKan ZhouNo ratings yet

- 6int 2005 Jun QDocument9 pages6int 2005 Jun Qapi-19836745No ratings yet

- IMA SALARYBENCHMARKING HighlightsDocument17 pagesIMA SALARYBENCHMARKING HighlightsAbhijith PrabhakarNo ratings yet

- Avendus Wealth ManagementDocument23 pagesAvendus Wealth ManagementAbhishek NoriNo ratings yet

- 2020 SaaS Benchmarks Deck VFINALDocument53 pages2020 SaaS Benchmarks Deck VFINALAbcd123411No ratings yet

- Icici Prudential Asset Allocator Fund PPT - Jan - Investor - 2021Document17 pagesIcici Prudential Asset Allocator Fund PPT - Jan - Investor - 2021hackmeatakashNo ratings yet

- LEAPOfferings Combined PWADocument42 pagesLEAPOfferings Combined PWAsanaa.kanjianiNo ratings yet

- LEAP OfferingsDocument42 pagesLEAP Offeringssanaa.kanjianiNo ratings yet

- MOSL New Year Top Picks 2023Document19 pagesMOSL New Year Top Picks 2023dcpjimmy100% (1)

- DSP Midcap Fund Mar 2023Document44 pagesDSP Midcap Fund Mar 2023Aakash ChhariaNo ratings yet

- Eurex Factsheet - Msci - Index - Dividend - FuturesDocument2 pagesEurex Factsheet - Msci - Index - Dividend - Futures0840328818zNo ratings yet

- Barbell Income Fund BrochureDocument8 pagesBarbell Income Fund BrochurecsNo ratings yet

- Mahindra Manulife MF - Market OutlookDocument1 pageMahindra Manulife MF - Market OutlookYasahNo ratings yet

- Investor Presentation Q1 FY21 July 2020Document55 pagesInvestor Presentation Q1 FY21 July 2020vvpvarunNo ratings yet

- Module 2 - Pay For Position - Fixed Pay - FINAL - Oct2014Document101 pagesModule 2 - Pay For Position - Fixed Pay - FINAL - Oct2014zulianNo ratings yet

- Collective Insights: Minutes From Our Morning MeetingDocument2 pagesCollective Insights: Minutes From Our Morning Meetingapi-63645244No ratings yet

- StrategyDocument6 pagesStrategyjcw288No ratings yet

- The Indian Media & Entertainment Industry 2019: Trends & Analysis - Past, Present & FutureDocument63 pagesThe Indian Media & Entertainment Industry 2019: Trends & Analysis - Past, Present & FutureSharvari ShankarNo ratings yet

- Malabar Midcap Fund Monthly Factsheet - April 2024Document1 pageMalabar Midcap Fund Monthly Factsheet - April 2024Suleiman HaqNo ratings yet

- E Tailing Market - Clubfactory GMV - Ajio GMV - Redseer ConsultingDocument10 pagesE Tailing Market - Clubfactory GMV - Ajio GMV - Redseer ConsultingredseerNo ratings yet

- WING Wingstop Investor Presentation June 2018Document37 pagesWING Wingstop Investor Presentation June 2018Ala BasterNo ratings yet

- Korn Ferry Salary Movement and Forecast Survey ReportDocument17 pagesKorn Ferry Salary Movement and Forecast Survey ReportTulshidasNo ratings yet

- Sun Pharma Corporate PresentationDocument59 pagesSun Pharma Corporate PresentationRutvik ShahNo ratings yet

- EdgeReport WIPRO CaseStudy 28 12 2022 444Document35 pagesEdgeReport WIPRO CaseStudy 28 12 2022 444gann wolfNo ratings yet

- AA - REPORT Expansion SaaS Benchmarking StudyDocument43 pagesAA - REPORT Expansion SaaS Benchmarking StudyRobert KoverNo ratings yet

- AlphaIndicator INAR 20221029Document11 pagesAlphaIndicator INAR 20221029spam adsNo ratings yet

- Hayden Capital Quarterly Letter 2021 Q1Document16 pagesHayden Capital Quarterly Letter 2021 Q1fatih jumongNo ratings yet

- Sip Presentation - May 2020Document40 pagesSip Presentation - May 2020DBCGNo ratings yet

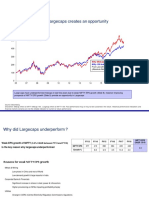

- Equity Markets Review Underperformance of Largecaps Creates An OpportunityDocument8 pagesEquity Markets Review Underperformance of Largecaps Creates An OpportunitysumeetNo ratings yet

- HDFC Asset Allocator Fund of Funds - NFO LeafletDocument4 pagesHDFC Asset Allocator Fund of Funds - NFO LeafletJignesh PatelNo ratings yet

- India Strategy - InCred - 28 AugDocument37 pagesIndia Strategy - InCred - 28 AugDeepul WadhwaNo ratings yet

- Capturing Factor Premia: September 2015Document10 pagesCapturing Factor Premia: September 2015Utkarsh ChoudharyNo ratings yet

- ETF Newsletter - February - 23Document20 pagesETF Newsletter - February - 23Chuck CookNo ratings yet

- Prodn SSDocument13 pagesProdn SSMae GonzalesNo ratings yet

- Jupiter India Select Factsheet PA Retail LU0329071053 en GB PDFDocument4 pagesJupiter India Select Factsheet PA Retail LU0329071053 en GB PDFAlly Bin AssadNo ratings yet

- Nomura - India InsuranceDocument10 pagesNomura - India Insuranceudhaya kumarNo ratings yet

- UTI Aggressive Hybrid Fund (Formerly UTI Hybrid Equity Fund)Document28 pagesUTI Aggressive Hybrid Fund (Formerly UTI Hybrid Equity Fund)rinkuparekh13No ratings yet

- Average Score: Ifca MSC (Ifcamsc-Ku)Document11 pagesAverage Score: Ifca MSC (Ifcamsc-Ku)Zhi_Ming_Cheah_8136No ratings yet

- Fund Fact Sheet - March 2019Document20 pagesFund Fact Sheet - March 2019Afthon Ilman Huda Isyfi100% (1)

- Real Estate - Japan Real Estate Market Outlook Report - ENDocument22 pagesReal Estate - Japan Real Estate Market Outlook Report - ENVishaka JainNo ratings yet

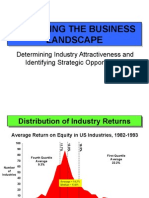

- Analyzing The Business LandscapeDocument18 pagesAnalyzing The Business Landscapedanic13No ratings yet

- EdgeReport WIPRO CaseStudy 12 07 2022 1058Document35 pagesEdgeReport WIPRO CaseStudy 12 07 2022 1058skumar412898No ratings yet

- The Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureDocument56 pagesThe Indian Media & Entertainment Industry 2018: Trends & Analysis - Past, Present & FutureAnkit TiwariNo ratings yet

- Ambit Capital - Agri Inputs - Diverging Growth Rates (Sector Update) (POSITIVE)Document65 pagesAmbit Capital - Agri Inputs - Diverging Growth Rates (Sector Update) (POSITIVE)Davuluri OmprakashNo ratings yet

- Old Mutual Top 40 Index Fund: Fund Information Fund Performance As at 31/12/2021Document2 pagesOld Mutual Top 40 Index Fund: Fund Information Fund Performance As at 31/12/2021Ardine FickNo ratings yet

- Technofunda - SIS - 27-11-2020 - 09Document5 pagesTechnofunda - SIS - 27-11-2020 - 09vicky6677No ratings yet

- Vanguard Global Stock Index FundDocument4 pagesVanguard Global Stock Index FundjorgeperezsidecarshotmailomNo ratings yet

- WING Investor Presentation IR Website 2018 WingstopDocument37 pagesWING Investor Presentation IR Website 2018 WingstopAla BasterNo ratings yet

- Gabriel India Limited: AJINKYA YADAV - 19020348002 - MBA FINANCE (EXECUTIVE) 2019-22Document22 pagesGabriel India Limited: AJINKYA YADAV - 19020348002 - MBA FINANCE (EXECUTIVE) 2019-22Ajinkya YadavNo ratings yet

- Axis Global Innovation FoF NFO LeafletDocument2 pagesAxis Global Innovation FoF NFO LeafletKamalnath SinghNo ratings yet

- SBI International Access US Equity FoFDocument26 pagesSBI International Access US Equity FoFRoshanR.NawaleNo ratings yet

- IRBT Investor Presentation Baird111120Document31 pagesIRBT Investor Presentation Baird111120ABermNo ratings yet

- Internships PGDM 2020 22 BatchDocument6 pagesInternships PGDM 2020 22 BatchSanthosh SanthuNo ratings yet

- Trend Following in Focus - September 2018Document8 pagesTrend Following in Focus - September 2018Clement VitaliNo ratings yet

- Average Score: Sap (Sap-Mi)Document11 pagesAverage Score: Sap (Sap-Mi)asraghuNo ratings yet

- HR Team Day Out - May 2012 v3Document61 pagesHR Team Day Out - May 2012 v3sashaNo ratings yet

- India Listed Pharma Healthcare May23Document6 pagesIndia Listed Pharma Healthcare May23Vansh AggarwalNo ratings yet

- STRATEGY Nifty - Bank IT 20230327 MOSL SU PG010Document10 pagesSTRATEGY Nifty - Bank IT 20230327 MOSL SU PG010Aakash ChhariaNo ratings yet

- April 2018 Investor PresentationDocument39 pagesApril 2018 Investor PresentationAlex lyuNo ratings yet

- Estimating the Job Creation Impact of Development AssistanceFrom EverandEstimating the Job Creation Impact of Development AssistanceNo ratings yet

- Asia Small and Medium-Sized Enterprise Monitor 2020: Volume IV: Technical Note—Designing a Small and Medium-Sized Enterprise Development IndexFrom EverandAsia Small and Medium-Sized Enterprise Monitor 2020: Volume IV: Technical Note—Designing a Small and Medium-Sized Enterprise Development IndexNo ratings yet

- LogarithmsDocument1 pageLogarithmsDaniel JamesNo ratings yet

- Paytm Money - Foundation MasterclassDocument35 pagesPaytm Money - Foundation MasterclassDaniel JamesNo ratings yet

- Paytm Masterclass ITI AMCDocument11 pagesPaytm Masterclass ITI AMCDaniel JamesNo ratings yet

- Patym - Masterclass Edelweiss AMCDocument15 pagesPatym - Masterclass Edelweiss AMCDaniel JamesNo ratings yet

- Bank of IndiaDocument63 pagesBank of IndiaArmaan ChhaprooNo ratings yet

- Bpme1013 Group B Introduction To Entrepreneurship (Full)Document27 pagesBpme1013 Group B Introduction To Entrepreneurship (Full)Randa RamadhanNo ratings yet

- Nmims: Entrepreneurship ManagementDocument264 pagesNmims: Entrepreneurship ManagementBhavi GolchhaNo ratings yet

- Tom Swiss Weekly Mayoral PollDocument5 pagesTom Swiss Weekly Mayoral PollThe Daily LineNo ratings yet

- China and Africa - BibliographyDocument357 pagesChina and Africa - BibliographyDavid ShinnNo ratings yet

- Report of Monument and PatternsDocument23 pagesReport of Monument and PatternsMAHEEN FATIMANo ratings yet

- Parental Involvement and Their Impact On Reading English of Students Among The Rural School in MalaysiaDocument8 pagesParental Involvement and Their Impact On Reading English of Students Among The Rural School in MalaysiaM-Hazmir HamzahNo ratings yet

- MbfiDocument29 pagesMbfiSujith DeepakNo ratings yet

- UntitledDocument18 pagesUntitledjeralyn juditNo ratings yet

- Sri Guru GitaDocument43 pagesSri Guru GitaDowlutrao Gangaram100% (1)

- Exploring Rfid'S Use in Shipping: Prepared For Kennesaw State University's Information Technology Students and StaffDocument22 pagesExploring Rfid'S Use in Shipping: Prepared For Kennesaw State University's Information Technology Students and Staffcallaway20No ratings yet

- Commets Muhammed ProposalDocument38 pagesCommets Muhammed ProposalMohammed HussenNo ratings yet

- I. Demographic Profile/Information Name: Theodore Robert Bundy (Ted Bundy) Age: 42Document5 pagesI. Demographic Profile/Information Name: Theodore Robert Bundy (Ted Bundy) Age: 42Maanne MandalNo ratings yet

- Illiashenko and Strielkowski 2018 Innovative Management LibroDocument296 pagesIlliashenko and Strielkowski 2018 Innovative Management LibroYaydikNo ratings yet

- Serres InterviewDocument9 pagesSerres InterviewhumblegeekNo ratings yet

- Accounting 1 Module 3Document20 pagesAccounting 1 Module 3Rose Marie Recorte100% (1)

- Manual For Conflict AnalysisDocument38 pagesManual For Conflict AnalysisNadine KadriNo ratings yet

- Definition:: Handover NotesDocument3 pagesDefinition:: Handover NotesRalkan KantonNo ratings yet

- Education USADocument35 pagesEducation USAPierrecassanNo ratings yet

- Unit 3 Bible Exam and MidtermDocument3 pagesUnit 3 Bible Exam and MidtermMicah BrewsterNo ratings yet

- Participating in The School's Learning Programs and ActivitiesDocument6 pagesParticipating in The School's Learning Programs and ActivitiesJoan May de Lumen77% (13)

- NV jss1Document4 pagesNV jss1Samson Oluwafemi oNo ratings yet

- AC Checklist of ToolsDocument4 pagesAC Checklist of ToolsTvet AcnNo ratings yet

- CAR BLGF Covid Response UpdateDocument8 pagesCAR BLGF Covid Response UpdatenormanNo ratings yet

- Tugas Tutorial 2 - English Morpho-SyntaxDocument2 pagesTugas Tutorial 2 - English Morpho-Syntaxlotus373No ratings yet

- Scheme of Work Form 2 English 2018: Week Types Lesson (SOW) Theme Unit (Pulse 2)Document2 pagesScheme of Work Form 2 English 2018: Week Types Lesson (SOW) Theme Unit (Pulse 2)Subramaniam Periannan100% (2)

- Tesla Supercharger Pasadena ApprovedDocument5 pagesTesla Supercharger Pasadena ApprovedJoey KlenderNo ratings yet

- Business Law NotesDocument72 pagesBusiness Law Notesnoorulhadi99100% (3)

- C&NS UNIT-5pdfDocument28 pagesC&NS UNIT-5pdfDhanush GummidiNo ratings yet