Download as pdf or txt

You might also like

- Fafp MCQ 1 PDFDocument10 pagesFafp MCQ 1 PDFharshita patni100% (2)

- FAFD MCQ 2 On Interviewing TechniquesDocument11 pagesFAFD MCQ 2 On Interviewing Techniquesharshita patni20% (5)

- Jake Bernstein's Seasonal Trader's Bible - The Best of The Best in Seasonal Trades - Jake Bernstein (1996) PDFDocument561 pagesJake Bernstein's Seasonal Trader's Bible - The Best of The Best in Seasonal Trades - Jake Bernstein (1996) PDF林耀明100% (4)

- Pre-Quiz KanbanDocument4 pagesPre-Quiz KanbanSunetra Mukherjee100% (1)

- MCQ Ind As Day 13Document14 pagesMCQ Ind As Day 13CAAniketGangwalNo ratings yet

- MCQ Ind As Day 16Document15 pagesMCQ Ind As Day 16CAAniketGangwalNo ratings yet

- MCQ Ind As Day 2Document14 pagesMCQ Ind As Day 2CAAniketGangwalNo ratings yet

- Develop Soft Skills That Industry DemandsDocument13 pagesDevelop Soft Skills That Industry DemandsPrabhu Ganesh R JNo ratings yet

- Law208 - Cia BankingDocument15 pagesLaw208 - Cia BankingDooms 001No ratings yet

- NQT Cognitive Mock Direction Sense Online AssessmentDocument18 pagesNQT Cognitive Mock Direction Sense Online Assessmenttjagan42No ratings yet

- CMA Pre Exam Test PDFDocument28 pagesCMA Pre Exam Test PDFVinay YerubandiNo ratings yet

- Develop Soft Skills That Industry DemandsDocument13 pagesDevelop Soft Skills That Industry DemandsDSZGNo ratings yet

- Improve Interpersonal Skills For Better Results Dinesh Marks ReportDocument15 pagesImprove Interpersonal Skills For Better Results Dinesh Marks Reportvvsaidinesh0403No ratings yet

- Learn Corporate Telephone EtiquetteDocument14 pagesLearn Corporate Telephone Etiquettejatinkumarjittu100No ratings yet

- Improve Interpersonal Skills For Better ResultsDocument14 pagesImprove Interpersonal Skills For Better ResultsSatish KumarNo ratings yet

- This Report Helps You To Achieve Your Targets As Per Below Stated ObjectivesDocument13 pagesThis Report Helps You To Achieve Your Targets As Per Below Stated ObjectivesmukulNo ratings yet

- Improve Interpersonal Skills For Better ResultsDocument15 pagesImprove Interpersonal Skills For Better Resultsmurudkaraditya110No ratings yet

- Communication SkillsDocument18 pagesCommunication SkillsAbhishek Pandit 1902300No ratings yet

- Communication SkillsDocument18 pagesCommunication SkillsPrasad DawareNo ratings yet

- Sarulatha Dhayalan: This Report Helps You To Achieve Your Targets As Per Below Stated ObjectivesDocument51 pagesSarulatha Dhayalan: This Report Helps You To Achieve Your Targets As Per Below Stated ObjectivesdhanarajNo ratings yet

- Sulochana Saini: This Report Helps You To Achieve Your Targets As Per Below Stated ObjectivesDocument12 pagesSulochana Saini: This Report Helps You To Achieve Your Targets As Per Below Stated Objectivesshuchim guptaNo ratings yet

- Make Impactful PresentationsDocument13 pagesMake Impactful PresentationsIndrajeet MishraNo ratings yet

- Learn Corporate EtiquetteDocument13 pagesLearn Corporate Etiquettemahesh d100% (2)

- This Report Helps You To Achieve Your Targets As Per Below Stated ObjectivesDocument13 pagesThis Report Helps You To Achieve Your Targets As Per Below Stated ObjectivesRakesh RajwaniNo ratings yet

- Assessment PDFDocument11 pagesAssessment PDFRashmi bansalNo ratings yet

- Mentoring SkillsDocument14 pagesMentoring SkillsZaid_SultanNo ratings yet

- ISA 3.0 E-Learning Assessment TestDocument20 pagesISA 3.0 E-Learning Assessment TestCAAniketGangwalNo ratings yet

- This Report Helps You To Achieve Your Targets As Per Below Stated ObjectivesDocument13 pagesThis Report Helps You To Achieve Your Targets As Per Below Stated ObjectivesRakesh RajwaniNo ratings yet

- NQT Cognitive Mock Ratio and Proportion Online AssessmentDocument10 pagesNQT Cognitive Mock Ratio and Proportion Online AssessmentAnkush GuptaNo ratings yet

- This Report Helps You To Achieve Your Targets As Per Below Stated ObjectivesDocument13 pagesThis Report Helps You To Achieve Your Targets As Per Below Stated ObjectivesRakesh RajwaniNo ratings yet

- Ghosh Saikat2: This Report Helps You To Achieve Your Targets As Per Below Stated ObjectivesDocument31 pagesGhosh Saikat2: This Report Helps You To Achieve Your Targets As Per Below Stated ObjectivesTanmay AdhikaryNo ratings yet

- Communication SkillsDocument18 pagesCommunication SkillsSonal KumarNo ratings yet

- This Report Helps You To Achieve Your Targets As Per Below Stated ObjectivesDocument14 pagesThis Report Helps You To Achieve Your Targets As Per Below Stated ObjectivesCA Dilshad V PNo ratings yet

- Kanan Bansal: This Report Helps You To Achieve Your Targets As Per Below Stated ObjectivesDocument12 pagesKanan Bansal: This Report Helps You To Achieve Your Targets As Per Below Stated Objectivesshuchim guptaNo ratings yet

- 5 SP OPS Papers Combined 1-12 (2020)Document54 pages5 SP OPS Papers Combined 1-12 (2020)Harsha YerraNo ratings yet

- NQT Cognitive Mock Percentage Online AssessmentDocument10 pagesNQT Cognitive Mock Percentage Online AssessmentAnkush GuptaNo ratings yet

- ISA 3.0 E-Learning Assessment TestDocument24 pagesISA 3.0 E-Learning Assessment TestCA Pavan KommuriNo ratings yet

- MCQ On Interviewing Techniques PDFDocument12 pagesMCQ On Interviewing Techniques PDFRavi ShahNo ratings yet

- Aniket Sahu (108849521988689229760 - 21511016 - 1)Document19 pagesAniket Sahu (108849521988689229760 - 21511016 - 1)Technical AniketNo ratings yet

- RERA-Comprehensive Online Refresher Course Batch-1 MCQDocument34 pagesRERA-Comprehensive Online Refresher Course Batch-1 MCQDeepika RaoNo ratings yet

- General Aptitude Assessment TestDocument30 pagesGeneral Aptitude Assessment Testshrisa2002No ratings yet

- Assessment 1 Gamified QuizDocument64 pagesAssessment 1 Gamified QuizJackson Abraham ThekkekaraNo ratings yet

- Katalon Studio AssessmentDocument19 pagesKatalon Studio AssessmentJitendra BattiseNo ratings yet

- Corporate and Management AccountingDocument27 pagesCorporate and Management Accountingprashanth PrabhuNo ratings yet

- NISM VA Revision - Test 3 PDFDocument40 pagesNISM VA Revision - Test 3 PDFNila DhasNo ratings yet

- Assignment Rubric Prinsip Mikro EkonomiDocument6 pagesAssignment Rubric Prinsip Mikro EkonomiVignashNo ratings yet

- 5 6055344798582178042 PDFDocument19 pages5 6055344798582178042 PDFAshokNo ratings yet

- Engineering Mechanics: Statics of Deformable BodiesDocument18 pagesEngineering Mechanics: Statics of Deformable BodiesJohnnyNo ratings yet

- Post-Quiz - KanbanDocument4 pagesPost-Quiz - KanbanSunetra Mukherjee83% (6)

- Appraisal Form TemplateDocument16 pagesAppraisal Form TemplatePrecious Bukola Folarin (OmogePurple)No ratings yet

- Indonesian Hotel Annual ReviewDocument34 pagesIndonesian Hotel Annual ReviewSPHM HospitalityNo ratings yet

- Anna University Internal Marks CalculatorDocument3 pagesAnna University Internal Marks CalculatorVasthadu Vasu KannahNo ratings yet

- Probationary Employee Review Form Hafiz Uddin, NarsingdiDocument2 pagesProbationary Employee Review Form Hafiz Uddin, NarsingdiolmezestNo ratings yet

- BBCM4103 Compensation ManagementDocument6 pagesBBCM4103 Compensation ManagementENGKU NONI ENGKU ALAMNo ratings yet

- 5S Implementation SOPDocument12 pages5S Implementation SOPsyed rawaha100% (1)

- Performance-Based Assessment HandoutsDocument6 pagesPerformance-Based Assessment HandoutsAllyzza Lopez BlancaverNo ratings yet

- Addmen Graphical Performance Analysis Report v15Document15 pagesAddmen Graphical Performance Analysis Report v15Rebel Macho GopiNo ratings yet

- Measurement, Scaling, Sampling: Dr. Paurav ShuklaDocument21 pagesMeasurement, Scaling, Sampling: Dr. Paurav ShuklafikoNo ratings yet

- Form A - Company Evaluation NewDocument6 pagesForm A - Company Evaluation NewMohd FahmiNo ratings yet

- 5.civil Case-Mahalaxmi-FinalDocument20 pages5.civil Case-Mahalaxmi-FinalCAAniketGangwalNo ratings yet

- 4.criminal Case-Purroshtam-FinalDocument19 pages4.criminal Case-Purroshtam-FinalCAAniketGangwalNo ratings yet

- Anuj Jain Vs Axis Bank Limited DefendantDocument12 pagesAnuj Jain Vs Axis Bank Limited DefendantCAAniketGangwalNo ratings yet

- MCQ Ind As Day 16Document15 pagesMCQ Ind As Day 16CAAniketGangwalNo ratings yet

- MCQ Ind As Day 2Document14 pagesMCQ Ind As Day 2CAAniketGangwalNo ratings yet

- MCQ Ind As Day 13Document14 pagesMCQ Ind As Day 13CAAniketGangwalNo ratings yet

- No. of Printed Pages: 6 1 Master'S Degree in Economics Term-End ExaminationDocument6 pagesNo. of Printed Pages: 6 1 Master'S Degree in Economics Term-End ExaminationCAAniketGangwalNo ratings yet

- Nature of WorkDocument1 pageNature of WorkCAAniketGangwalNo ratings yet

- The Cotton Corporation of India LTD - 121202284133105Document20 pagesThe Cotton Corporation of India LTD - 121202284133105CAAniketGangwalNo ratings yet

- ISA 3.0 E-Learning Assessment TestDocument20 pagesISA 3.0 E-Learning Assessment TestCAAniketGangwalNo ratings yet

- Kycubo New Company Form - Final - 18 AprilDocument4 pagesKycubo New Company Form - Final - 18 AprilCAAniketGangwalNo ratings yet

- Reply To Communication For Payment Before Issue of SCNDocument2 pagesReply To Communication For Payment Before Issue of SCNCAAniketGangwalNo ratings yet

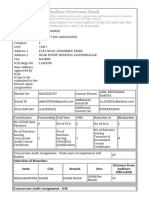

- IOB Concurrent Audit Application 2021-22Document2 pagesIOB Concurrent Audit Application 2021-22CAAniketGangwalNo ratings yet

- Brochure of Career Ascent-June 2021Document4 pagesBrochure of Career Ascent-June 2021CAAniketGangwalNo ratings yet

- RV Exam Case StudiesDocument2 pagesRV Exam Case StudiesCAAniketGangwalNo ratings yet

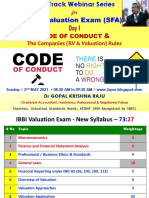

- FT11 Day1 COC GKR 02052021Document114 pagesFT11 Day1 COC GKR 02052021CAAniketGangwalNo ratings yet

- CH Grinch 589 Color ChartDocument10 pagesCH Grinch 589 Color ChartMarcos Gómez SosaNo ratings yet

- 20 Pip Forex ChallengeDocument3 pages20 Pip Forex ChallengejadtecNo ratings yet

- Unit-6 Subsidiary Books PDFDocument52 pagesUnit-6 Subsidiary Books PDFShiva AggarwalNo ratings yet

- 2023 Q4 Multifamily Houston Report ColliersDocument4 pages2023 Q4 Multifamily Houston Report ColliersKevin ParkerNo ratings yet

- For LP 24 Marxism ApproachDocument27 pagesFor LP 24 Marxism ApproachRegine MoskitoNo ratings yet

- Cable Lugs Bonding WireDocument3 pagesCable Lugs Bonding WireJwalaNo ratings yet

- Vvneq1m5ymzryny1nuj2swrlwef0dz09 InvoiceDocument2 pagesVvneq1m5ymzryny1nuj2swrlwef0dz09 InvoiceTYCS35 SIDDHESH PENDURKARNo ratings yet

- Case Discussion QuestionsDocument5 pagesCase Discussion QuestionsJoana Sharmine ArrobangNo ratings yet

- Toyo - Soal Dasar Akuntansi UTS - Gasal 2122Document2 pagesToyo - Soal Dasar Akuntansi UTS - Gasal 2122Dita nNo ratings yet

- Standard Costing 8Document12 pagesStandard Costing 8suraj banNo ratings yet

- Assignment 2: I. Complete All Problems and Applications at The End of Chapter 23Document6 pagesAssignment 2: I. Complete All Problems and Applications at The End of Chapter 23Phước Đào QuangNo ratings yet

- Review - Chapter 10 Questions & AnswersDocument3 pagesReview - Chapter 10 Questions & AnswersDivyansh SinghNo ratings yet

- Activity Based Costing - Chapter 8Document52 pagesActivity Based Costing - Chapter 8Qalb e AliNo ratings yet

- Bebe Chocolat PatternDocument3 pagesBebe Chocolat PatternAgathez LaheurteNo ratings yet

- Detailed StatementDocument10 pagesDetailed Statementwolf8585.inNo ratings yet

- Chapter 5 - Relevant Information and Decision Making - StudentsDocument27 pagesChapter 5 - Relevant Information and Decision Making - StudentsDAN NGUYEN THENo ratings yet

- COSMETOLOGY 10 - Q1 - W2 - Mod2Document18 pagesCOSMETOLOGY 10 - Q1 - W2 - Mod2Rosalie RebayNo ratings yet

- Mann Whitney U TestDocument19 pagesMann Whitney U TestANGELO JOSEPH CASTILLONo ratings yet

- Data Entry QuestionsDocument9 pagesData Entry QuestionsJackson MafumboNo ratings yet

- Bank Reconciliation StatementDocument2 pagesBank Reconciliation Statementvihanjangid223No ratings yet

- CA Foundation - MCQ's - 1Document97 pagesCA Foundation - MCQ's - 1Harshit GulatiNo ratings yet

- Test Bank For Microeconomics 15th Canadian Edition Campbell R Mcconnell Stanley L Brue Sean Masaki Flynn Tom BarbieroDocument36 pagesTest Bank For Microeconomics 15th Canadian Edition Campbell R Mcconnell Stanley L Brue Sean Masaki Flynn Tom Barbieroovercloydop.qpio7p100% (45)

- BIMA - Annual Report 2019Document108 pagesBIMA - Annual Report 2019Safitri 1612No ratings yet

- Essential Foundations of Economics 7th Edition Bade Test Bank Full Chapter PDFDocument68 pagesEssential Foundations of Economics 7th Edition Bade Test Bank Full Chapter PDFTerryGonzalezkqwy100% (18)

- Assignment Brief - BMMEP Group 1 (W, T)Document6 pagesAssignment Brief - BMMEP Group 1 (W, T)Sayed Abdul WajedNo ratings yet

- CHB Back-Up ComputationDocument36 pagesCHB Back-Up Computationkhim tugasNo ratings yet

- Central Public Works Account CODE FORMSDocument243 pagesCentral Public Works Account CODE FORMSbharanivldv978% (23)

- Til Po - 374Document1 pageTil Po - 374MAHABIR GHOSHNo ratings yet

- V890Document1 pageV890Arcadie ApostolNo ratings yet